CPI Boston Consulting Group Matrix

Download Your Competitive Advantage

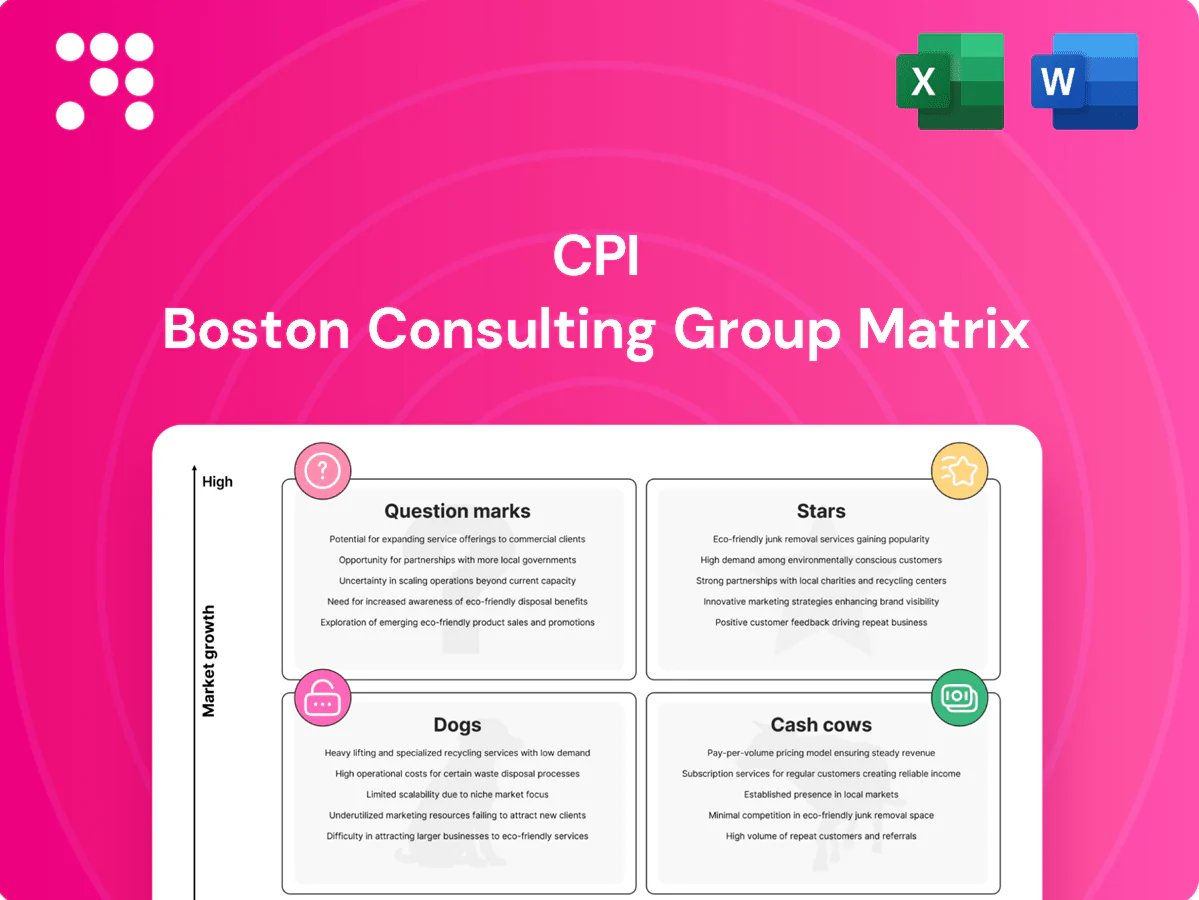

The CPI BCG Matrix slices this company’s portfolio into clear quadrants—Stars, Cash Cows, Question Marks, and Dogs—so you can see where growth or drain is happening at a glance. This preview teases the shape of opportunity; the full report maps every product into a quadrant with data-backed rationale and tactical next steps. Buy the complete BCG Matrix for a downloadable Word report plus an Excel summary you can present and act on immediately. Invest now and stop guessing—plan with clarity.

Stars

State DOT highway expansions

Backlog remains strong as federal IIJA funding includes roughly 110 billion for roads and bridges, and state DOT budgets in fast-growing Southeast corridors are accelerating. CPI is capturing meaningful work in select districts, leveraging high local market share and steady population gains (Florida ~22.2 million in 2023) to keep volumes up. Promotion focuses on proven capacity and past performance; keep feeding crews and plants — this can mature into dependable cash.

Asphalt paving & resurfacing in growth metros

Urban and suburban sprawl (U.S. urbanization ~82% in 2024) drives constant mill-and-fill work, new arterials, and widening projects with typical resurfacing cycles of 10–15 years. CPI’s scale, crews, and scheduling secure lead-dog status in metros, especially in a U.S. asphalt paving market near $25B in 2024. Margins remain stable when CPI controls plant time and logistics. Continued investment in plant uptime and crews delivers rapid payback through higher utilization and lower downtime.

Vertical integration: company-controlled asphalt supply

Owning or tightly partnering on asphalt production stabilizes costs and boosts bid competitiveness, especially as sustained federal infrastructure funding — including the IIJA’s roughly 110 billion for highways — keeps demand elevated in 2024. In hot markets that edge converts directly into share gains; protecting feedstock and optimizing mix designs lock margin and win rate advantages. The model soaks cash for plant maintenance and upgrades, but high throughput justifies the capex. Run hard and prioritize preventive maintenance to sustain output.

Recurring roadway maintenance programs

Recurring roadway maintenance programs are Stars in CPIs BCG matrix: the IIJA allocated 110 billion to roads and bridges, creating sustained, multi‑year contract opportunities in high‑growth counties; CPI frequently appears on preferred vendor lists, accelerating awards. As county budgets expand, task orders scale quickly. Maintain crisp service levels and tight response times to lock in volume and margin.

- Predictable volumes from multi‑year contracts

- Preferred vendor status speeds procurement

- Task orders scale with expanding budgets

- High retention via fast response and consistent SLAs

Site development for large private projects

Site development for large private projects is a Star: Southeast industrial, logistics, and residential booms drove heavy dirt and paving demand in 2024, and CPI’s integrated civil, paving, and site teams win complex, compressed timelines others stumble on. Growth is hot and CPI’s share is strong in markets where deep relationships accelerate repeat work; keeping preconstruction sharp — speed to mobilize wins.

- Market: Southeast construction surge 2024

- Edge: integrated delivery beats segmented bids

- Advantage: deep client relationships = higher share

- Priority: preconstruction speed to mobilize

Convert IIJA ~$110B and $25B asphalt demand into steady cash: scale plants, crews, mobilize fast

Stars: multi‑year IIJA road spend (~110B) and a ~25B U.S. asphalt market (2024) drive high-volume, high-utilization bids; CPI’s plant ownership and preferred vendor status convert demand into durable cash flow. Southeast growth (FL pop 22.2M in 2023; U.S. urbanization ~82% in 2024) fuels site development and repeat municipal resurfacing. Prioritize plant uptime, crew scale, and rapid mobilization to sustain margins.

| Metric | 2023–24 |

|---|---|

| IIJA roads & bridges | ~110B |

| U.S. asphalt market | ~25B (2024) |

| FL population | 22.2M (2023) |

| U.S. urbanization | ~82% (2024) |

What is included in the product

Comprehensive CPI BCG Matrix review identifying Stars, Cash Cows, Question Marks, Dogs with investment and divestment advice.

One-page CPI BCG Matrix highlighting growth vs share to spot underperformers and prioritize fixes for faster impact.

Cash Cows

Municipal resurfacing cycles in mature towns

Municipal resurfacing cycles in mature towns follow stable 10–15 year programs with predictable scopes and repeatable unit costs; CPI leverages steady tax bases and route knowledge to capture low-growth, high-margin work. Typical overlay unit costs run roughly $50,000–$100,000 per lane-mile (2024 market ranges), enabling minimal promo spend; focus is on reliability, crew utilization (75–85%), night shifts and tight haul windows to milk efficiencies.

Routine milling, striping, and small rehab

Routine milling, striping, and small rehab are commodity work but deliver high throughput and low drama, often generating gross margins in the 20–35% range for scale contractors; CPI’s volume reduces cost per lane-mile by roughly 10–15% versus small operators. Cash in exceeds cash out when scheduling stays dense—projects back-to-back can push utilization above 85% and improve weekly lane-mile output to the 100–200 range. Standardize crews and keep the gear turning to sustain these unit economics and convert steady revenue into reliable free cash flow.

County-level patching and preventive maintenance

County-level patching and preventive maintenance generates steady cash flows by filling work orders between large capital projects, keeping crews and plants utilized with flat top-line growth but reliable margins. Routing and rapid-deploy strategies reduce deadhead, which industry reports peg at about 20% of miles, improving operating margins materially. Prioritize routing software upgrades and analytics to cut deadhead miles and lift cash conversion.

Private parking lots and commercial paving

Private parking lots and commercial paving are classic cash cows for CPI BCG Matrix: not glamorous but highly bankable, delivering steady work from repeat clients with quick turns and tight scopes. Typical job cycles convert to revenue in 15–30 days and industry gross margins averaged about 25% in 2024, providing reliable cash flow to smooth plant loads. Low bid effort and high schedule control make them ideal buffers.

- Repeat clients

- Quick turns

- Tight scopes

- Low bid effort

- High schedule control

- 15–30 day cash conversion

- ~25% gross margin (2024)

Utility tie-ins and small drainage fixes

Utility tie-ins and small drainage fixes are high-turn cash cows for CPI: average 2024 ticket ~$325 with steady demand allowing crews to slot 10–15 of these jobs weekly between larger projects; inspections are simple, change orders typically under 5% of job value, and overhead runs below 10% on these tasks.

- Small tickets

- Consistent demand

- Simple inspections

- Lean mobile team

- Standard kits

Cash cows: overlays, parking lots and utility fixes — steady, high-margin income

Cash cows: municipal overlays, routine rehab, parking lots and small utility fixes deliver steady, low-growth high-margin cash flow for CPI; 2024 benchmarks: overlay unit $50–100k/lane‑mile, gross margins 20–35%, private lots ~25% GM, quick 15–30 day cash conversion, avg utility ticket ~$325, crew utilization 75–85%.

| Segment | 2024 Metric | Margin |

|---|---|---|

| Overlays | $50–100k/lane‑mile | 20–35% |

| Parking lots | 15–30d conversion | ~25% |

| Utility fixes | $325 avg ticket | — |

What You See Is What You Get

CPI BCG Matrix

The CPI BCG Matrix you're previewing here is the exact file you'll receive after purchase — no watermarks, no placeholders, just the finished report. It's fully formatted and ready for immediate use in presentations, planning sessions, or client briefs. Once you buy, the same document is delivered straight to your inbox for editing or printing. Simple, professional, and built for strategic clarity.

Download Your Competitive Advantage

The CPI BCG Matrix slices this company’s portfolio into clear quadrants—Stars, Cash Cows, Question Marks, and Dogs—so you can see where growth or drain is happening at a glance. This preview teases the shape of opportunity; the full report maps every product into a quadrant with data-backed rationale and tactical next steps. Buy the complete BCG Matrix for a downloadable Word report plus an Excel summary you can present and act on immediately. Invest now and stop guessing—plan with clarity.

Stars

State DOT highway expansions

Backlog remains strong as federal IIJA funding includes roughly 110 billion for roads and bridges, and state DOT budgets in fast-growing Southeast corridors are accelerating. CPI is capturing meaningful work in select districts, leveraging high local market share and steady population gains (Florida ~22.2 million in 2023) to keep volumes up. Promotion focuses on proven capacity and past performance; keep feeding crews and plants — this can mature into dependable cash.

Asphalt paving & resurfacing in growth metros

Urban and suburban sprawl (U.S. urbanization ~82% in 2024) drives constant mill-and-fill work, new arterials, and widening projects with typical resurfacing cycles of 10–15 years. CPI’s scale, crews, and scheduling secure lead-dog status in metros, especially in a U.S. asphalt paving market near $25B in 2024. Margins remain stable when CPI controls plant time and logistics. Continued investment in plant uptime and crews delivers rapid payback through higher utilization and lower downtime.

Vertical integration: company-controlled asphalt supply

Owning or tightly partnering on asphalt production stabilizes costs and boosts bid competitiveness, especially as sustained federal infrastructure funding — including the IIJA’s roughly 110 billion for highways — keeps demand elevated in 2024. In hot markets that edge converts directly into share gains; protecting feedstock and optimizing mix designs lock margin and win rate advantages. The model soaks cash for plant maintenance and upgrades, but high throughput justifies the capex. Run hard and prioritize preventive maintenance to sustain output.

Recurring roadway maintenance programs

Recurring roadway maintenance programs are Stars in CPIs BCG matrix: the IIJA allocated 110 billion to roads and bridges, creating sustained, multi‑year contract opportunities in high‑growth counties; CPI frequently appears on preferred vendor lists, accelerating awards. As county budgets expand, task orders scale quickly. Maintain crisp service levels and tight response times to lock in volume and margin.

- Predictable volumes from multi‑year contracts

- Preferred vendor status speeds procurement

- Task orders scale with expanding budgets

- High retention via fast response and consistent SLAs

Site development for large private projects

Site development for large private projects is a Star: Southeast industrial, logistics, and residential booms drove heavy dirt and paving demand in 2024, and CPI’s integrated civil, paving, and site teams win complex, compressed timelines others stumble on. Growth is hot and CPI’s share is strong in markets where deep relationships accelerate repeat work; keeping preconstruction sharp — speed to mobilize wins.

- Market: Southeast construction surge 2024

- Edge: integrated delivery beats segmented bids

- Advantage: deep client relationships = higher share

- Priority: preconstruction speed to mobilize

Convert IIJA ~$110B and $25B asphalt demand into steady cash: scale plants, crews, mobilize fast

Stars: multi‑year IIJA road spend (~110B) and a ~25B U.S. asphalt market (2024) drive high-volume, high-utilization bids; CPI’s plant ownership and preferred vendor status convert demand into durable cash flow. Southeast growth (FL pop 22.2M in 2023; U.S. urbanization ~82% in 2024) fuels site development and repeat municipal resurfacing. Prioritize plant uptime, crew scale, and rapid mobilization to sustain margins.

| Metric | 2023–24 |

|---|---|

| IIJA roads & bridges | ~110B |

| U.S. asphalt market | ~25B (2024) |

| FL population | 22.2M (2023) |

| U.S. urbanization | ~82% (2024) |

What is included in the product

Comprehensive CPI BCG Matrix review identifying Stars, Cash Cows, Question Marks, Dogs with investment and divestment advice.

One-page CPI BCG Matrix highlighting growth vs share to spot underperformers and prioritize fixes for faster impact.

Cash Cows

Municipal resurfacing cycles in mature towns

Municipal resurfacing cycles in mature towns follow stable 10–15 year programs with predictable scopes and repeatable unit costs; CPI leverages steady tax bases and route knowledge to capture low-growth, high-margin work. Typical overlay unit costs run roughly $50,000–$100,000 per lane-mile (2024 market ranges), enabling minimal promo spend; focus is on reliability, crew utilization (75–85%), night shifts and tight haul windows to milk efficiencies.

Routine milling, striping, and small rehab

Routine milling, striping, and small rehab are commodity work but deliver high throughput and low drama, often generating gross margins in the 20–35% range for scale contractors; CPI’s volume reduces cost per lane-mile by roughly 10–15% versus small operators. Cash in exceeds cash out when scheduling stays dense—projects back-to-back can push utilization above 85% and improve weekly lane-mile output to the 100–200 range. Standardize crews and keep the gear turning to sustain these unit economics and convert steady revenue into reliable free cash flow.

County-level patching and preventive maintenance

County-level patching and preventive maintenance generates steady cash flows by filling work orders between large capital projects, keeping crews and plants utilized with flat top-line growth but reliable margins. Routing and rapid-deploy strategies reduce deadhead, which industry reports peg at about 20% of miles, improving operating margins materially. Prioritize routing software upgrades and analytics to cut deadhead miles and lift cash conversion.

Private parking lots and commercial paving

Private parking lots and commercial paving are classic cash cows for CPI BCG Matrix: not glamorous but highly bankable, delivering steady work from repeat clients with quick turns and tight scopes. Typical job cycles convert to revenue in 15–30 days and industry gross margins averaged about 25% in 2024, providing reliable cash flow to smooth plant loads. Low bid effort and high schedule control make them ideal buffers.

- Repeat clients

- Quick turns

- Tight scopes

- Low bid effort

- High schedule control

- 15–30 day cash conversion

- ~25% gross margin (2024)

Utility tie-ins and small drainage fixes

Utility tie-ins and small drainage fixes are high-turn cash cows for CPI: average 2024 ticket ~$325 with steady demand allowing crews to slot 10–15 of these jobs weekly between larger projects; inspections are simple, change orders typically under 5% of job value, and overhead runs below 10% on these tasks.

- Small tickets

- Consistent demand

- Simple inspections

- Lean mobile team

- Standard kits

Cash cows: overlays, parking lots and utility fixes — steady, high-margin income

Cash cows: municipal overlays, routine rehab, parking lots and small utility fixes deliver steady, low-growth high-margin cash flow for CPI; 2024 benchmarks: overlay unit $50–100k/lane‑mile, gross margins 20–35%, private lots ~25% GM, quick 15–30 day cash conversion, avg utility ticket ~$325, crew utilization 75–85%.

| Segment | 2024 Metric | Margin |

|---|---|---|

| Overlays | $50–100k/lane‑mile | 20–35% |

| Parking lots | 15–30d conversion | ~25% |

| Utility fixes | $325 avg ticket | — |

What You See Is What You Get

CPI BCG Matrix

The CPI BCG Matrix you're previewing here is the exact file you'll receive after purchase — no watermarks, no placeholders, just the finished report. It's fully formatted and ready for immediate use in presentations, planning sessions, or client briefs. Once you buy, the same document is delivered straight to your inbox for editing or printing. Simple, professional, and built for strategic clarity.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

The CPI BCG Matrix slices this company’s portfolio into clear quadrants—Stars, Cash Cows, Question Marks, and Dogs—so you can see where growth or drain is happening at a glance. This preview teases the shape of opportunity; the full report maps every product into a quadrant with data-backed rationale and tactical next steps. Buy the complete BCG Matrix for a downloadable Word report plus an Excel summary you can present and act on immediately. Invest now and stop guessing—plan with clarity.

Stars

State DOT highway expansions

Backlog remains strong as federal IIJA funding includes roughly 110 billion for roads and bridges, and state DOT budgets in fast-growing Southeast corridors are accelerating. CPI is capturing meaningful work in select districts, leveraging high local market share and steady population gains (Florida ~22.2 million in 2023) to keep volumes up. Promotion focuses on proven capacity and past performance; keep feeding crews and plants — this can mature into dependable cash.

Asphalt paving & resurfacing in growth metros

Urban and suburban sprawl (U.S. urbanization ~82% in 2024) drives constant mill-and-fill work, new arterials, and widening projects with typical resurfacing cycles of 10–15 years. CPI’s scale, crews, and scheduling secure lead-dog status in metros, especially in a U.S. asphalt paving market near $25B in 2024. Margins remain stable when CPI controls plant time and logistics. Continued investment in plant uptime and crews delivers rapid payback through higher utilization and lower downtime.

Vertical integration: company-controlled asphalt supply

Owning or tightly partnering on asphalt production stabilizes costs and boosts bid competitiveness, especially as sustained federal infrastructure funding — including the IIJA’s roughly 110 billion for highways — keeps demand elevated in 2024. In hot markets that edge converts directly into share gains; protecting feedstock and optimizing mix designs lock margin and win rate advantages. The model soaks cash for plant maintenance and upgrades, but high throughput justifies the capex. Run hard and prioritize preventive maintenance to sustain output.

Recurring roadway maintenance programs

Recurring roadway maintenance programs are Stars in CPIs BCG matrix: the IIJA allocated 110 billion to roads and bridges, creating sustained, multi‑year contract opportunities in high‑growth counties; CPI frequently appears on preferred vendor lists, accelerating awards. As county budgets expand, task orders scale quickly. Maintain crisp service levels and tight response times to lock in volume and margin.

- Predictable volumes from multi‑year contracts

- Preferred vendor status speeds procurement

- Task orders scale with expanding budgets

- High retention via fast response and consistent SLAs

Site development for large private projects

Site development for large private projects is a Star: Southeast industrial, logistics, and residential booms drove heavy dirt and paving demand in 2024, and CPI’s integrated civil, paving, and site teams win complex, compressed timelines others stumble on. Growth is hot and CPI’s share is strong in markets where deep relationships accelerate repeat work; keeping preconstruction sharp — speed to mobilize wins.

- Market: Southeast construction surge 2024

- Edge: integrated delivery beats segmented bids

- Advantage: deep client relationships = higher share

- Priority: preconstruction speed to mobilize

Convert IIJA ~$110B and $25B asphalt demand into steady cash: scale plants, crews, mobilize fast

Stars: multi‑year IIJA road spend (~110B) and a ~25B U.S. asphalt market (2024) drive high-volume, high-utilization bids; CPI’s plant ownership and preferred vendor status convert demand into durable cash flow. Southeast growth (FL pop 22.2M in 2023; U.S. urbanization ~82% in 2024) fuels site development and repeat municipal resurfacing. Prioritize plant uptime, crew scale, and rapid mobilization to sustain margins.

| Metric | 2023–24 |

|---|---|

| IIJA roads & bridges | ~110B |

| U.S. asphalt market | ~25B (2024) |

| FL population | 22.2M (2023) |

| U.S. urbanization | ~82% (2024) |

What is included in the product

Comprehensive CPI BCG Matrix review identifying Stars, Cash Cows, Question Marks, Dogs with investment and divestment advice.

One-page CPI BCG Matrix highlighting growth vs share to spot underperformers and prioritize fixes for faster impact.

Cash Cows

Municipal resurfacing cycles in mature towns

Municipal resurfacing cycles in mature towns follow stable 10–15 year programs with predictable scopes and repeatable unit costs; CPI leverages steady tax bases and route knowledge to capture low-growth, high-margin work. Typical overlay unit costs run roughly $50,000–$100,000 per lane-mile (2024 market ranges), enabling minimal promo spend; focus is on reliability, crew utilization (75–85%), night shifts and tight haul windows to milk efficiencies.

Routine milling, striping, and small rehab

Routine milling, striping, and small rehab are commodity work but deliver high throughput and low drama, often generating gross margins in the 20–35% range for scale contractors; CPI’s volume reduces cost per lane-mile by roughly 10–15% versus small operators. Cash in exceeds cash out when scheduling stays dense—projects back-to-back can push utilization above 85% and improve weekly lane-mile output to the 100–200 range. Standardize crews and keep the gear turning to sustain these unit economics and convert steady revenue into reliable free cash flow.

County-level patching and preventive maintenance

County-level patching and preventive maintenance generates steady cash flows by filling work orders between large capital projects, keeping crews and plants utilized with flat top-line growth but reliable margins. Routing and rapid-deploy strategies reduce deadhead, which industry reports peg at about 20% of miles, improving operating margins materially. Prioritize routing software upgrades and analytics to cut deadhead miles and lift cash conversion.

Private parking lots and commercial paving

Private parking lots and commercial paving are classic cash cows for CPI BCG Matrix: not glamorous but highly bankable, delivering steady work from repeat clients with quick turns and tight scopes. Typical job cycles convert to revenue in 15–30 days and industry gross margins averaged about 25% in 2024, providing reliable cash flow to smooth plant loads. Low bid effort and high schedule control make them ideal buffers.

- Repeat clients

- Quick turns

- Tight scopes

- Low bid effort

- High schedule control

- 15–30 day cash conversion

- ~25% gross margin (2024)

Utility tie-ins and small drainage fixes

Utility tie-ins and small drainage fixes are high-turn cash cows for CPI: average 2024 ticket ~$325 with steady demand allowing crews to slot 10–15 of these jobs weekly between larger projects; inspections are simple, change orders typically under 5% of job value, and overhead runs below 10% on these tasks.

- Small tickets

- Consistent demand

- Simple inspections

- Lean mobile team

- Standard kits

Cash cows: overlays, parking lots and utility fixes — steady, high-margin income

Cash cows: municipal overlays, routine rehab, parking lots and small utility fixes deliver steady, low-growth high-margin cash flow for CPI; 2024 benchmarks: overlay unit $50–100k/lane‑mile, gross margins 20–35%, private lots ~25% GM, quick 15–30 day cash conversion, avg utility ticket ~$325, crew utilization 75–85%.

| Segment | 2024 Metric | Margin |

|---|---|---|

| Overlays | $50–100k/lane‑mile | 20–35% |

| Parking lots | 15–30d conversion | ~25% |

| Utility fixes | $325 avg ticket | — |

What You See Is What You Get

CPI BCG Matrix

The CPI BCG Matrix you're previewing here is the exact file you'll receive after purchase — no watermarks, no placeholders, just the finished report. It's fully formatted and ready for immediate use in presentations, planning sessions, or client briefs. Once you buy, the same document is delivered straight to your inbox for editing or printing. Simple, professional, and built for strategic clarity.