CPI PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

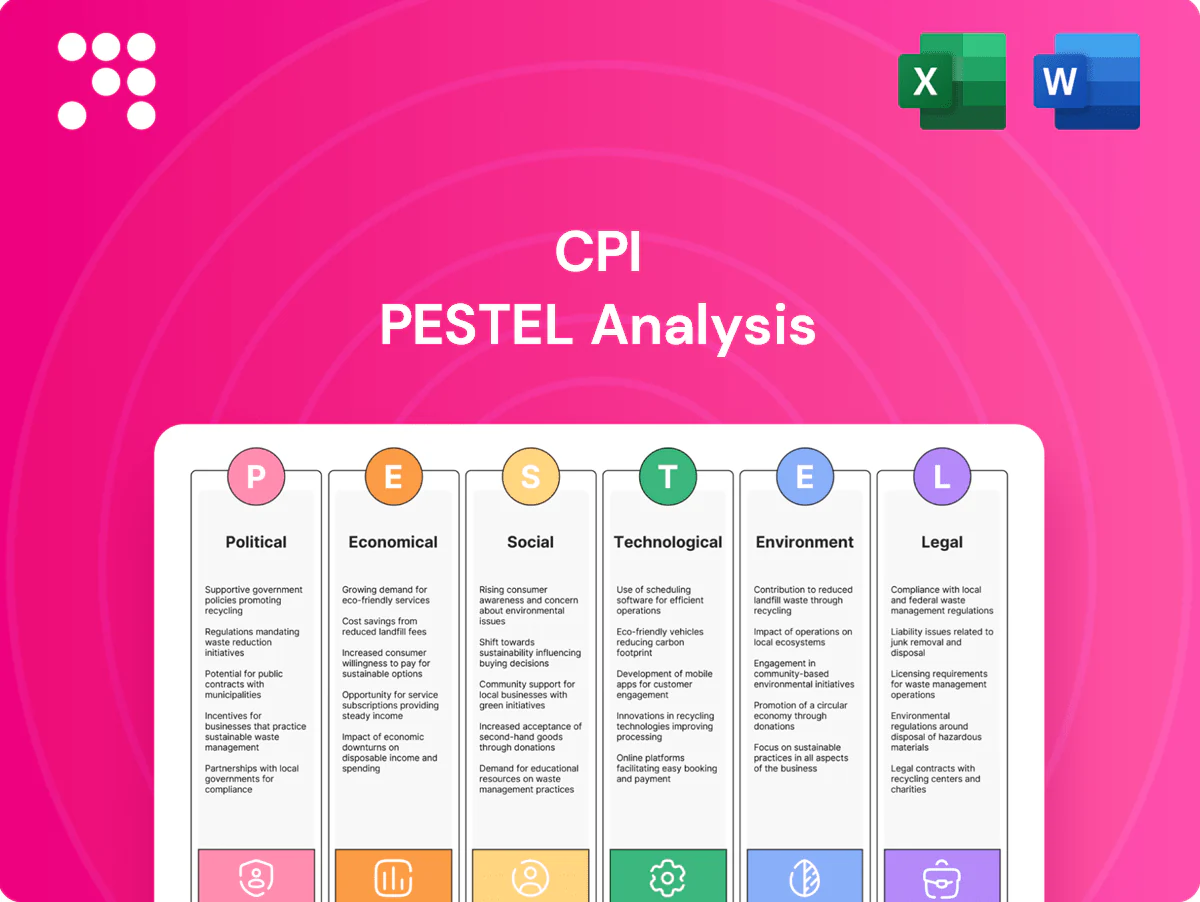

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping CPI’s strategic outlook. Our concise PESTLE snapshot highlights immediate risks and opportunities. Buy the full analysis to access detailed, actionable intelligence and ready-to-use recommendations.

Political factors

Federal and state infrastructure funding

Revenue visibility hinges on appropriations such as the IIJA, which authorized roughly 550 billion dollars in new infrastructure investments, plus annual DOT appropriations and state transportation trust funds; multi‑year IIJA programs underpin sizable, stable backlogs but continuing resolutions can defer lettings and slow cash flow. Monitoring the federal gas tax (18.4 cents/gal) and state gas‑tax changes, toll adoption or mileage fees is critical for pipeline predictability. Strategic alignment with high‑spend states like Texas, Florida and Georgia mitigates funding volatility.

Procurement and bidding dynamics

Low-bid statutes, prequalification, and DB/DBB delivery models drive tighter margins and shift risk to contractors, while political priorities—evidenced by federal small-business contracting reaching 27.6% in FY2023—boost awards to small/minority firms, joint ventures, or alternative delivery. Recent procurement updates in states and agencies increasingly weight lifecycle cost and resilience, rewarding quality and innovation over lowest price. Strong agency relationships measurably improve win rates and change-order outcomes.

Transportation policy priorities

Safety, congestion relief, and rural connectivity shape project choices, driving targeted investments to reduce crashes and delays. The federal IIJA/BIL channels roughly 110 billion USD to roads and bridges, including about 40 billion for bridge repair and 5 billion for NEVI EV charging, prioritizing bridges, freight corridors, and EV corridors. Southeast states emphasize port access and hurricane evacuation routes, and industry advocacy steers standards and grant allocations.

Labor and immigration stance

Visa limits like the 66,000 annual H-2B cap and 26 states requiring E-Verify (2024) tighten craft-labor availability, pushing wages higher and raising hiring compliance costs. State public-works labor standards (prevailing wage, PLAs) elevate wage floors and administrative burden. Expanded federal/state technical-education and apprenticeship funding since IIJA has increased pipelines. Stronger worker-classification enforcement (AB5, more audits) constrains subcontracting models.

- 26 states require E-Verify (2024)

- H-2B cap 66,000 annually

- Construction employment ~7.6M (BLS 2024)

- AB5/audit focus limits subcontracting flexibility

Permitting and local governance

County and municipal politics control zoning, right-of-way and utility-relocation timelines and routinely impose permitting windows that extend project delivery timelines.

Local resistance or support can accelerate approvals or stall projects; coordination with more than 400 MPOs and state DOTs is essential for staging, detours and funding alignment.

The 2021 Bipartisan Infrastructure Law provided about 550 billion in new infrastructure funding, and election cycles (2–4 years) frequently reprioritize capital plans and maintenance schedules.

- Permitting delays: adds months to delivery

- Local politics: can stop or speed projects

- MPOs: >400 for regional coordination

- Funding: ~550 billion from 2021 BIL

- Elections: 2–4 year reprioritization

IIJA/BIL funding sustains backlog while procurement rules and labor caps squeeze margins

Policy drives revenue and risk: IIJA/BIL ≈550 billion sustains backlogs but continuing resolutions disrupt cash flow. Procurement rules and DB/DBB lower margins while small-business set‑asides (27.6% FY2023) shift awards. Labor constraints (H‑2B 66,000 cap; 26 states E‑Verify) tighten crews and raise costs.

| Metric | Value |

|---|---|

| IIJA/BIL | ≈550 billion |

| Federal gas tax | 18.4 cents/gal |

| H‑2B cap | 66,000 |

| Construction employment (BLS 2024) | ≈7.6M |

| States E‑Verify (2024) | 26 |

| MPOs | >400 |

What is included in the product

Explores how macro-environmental factors uniquely affect the CPI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends; designed for executives, consultants, and entrepreneurs to identify threats, opportunities, and support scenario planning, funding pitches, and strategy alignment with real market and regulatory dynamics.

Condenses CPI-related political, economic, social, technological, legal and environmental impacts into a clear, visually segmented brief that teams can share, edit, and drop into presentations to speed alignment and reduce analysis friction.

Economic factors

Material and fuel cost volatility

Asphalt cement, aggregates, cement and diesel can account for roughly 40–60% of COGS in paving, with asphalt cement often 15–25%. Index pricing and escalation clauses partially hedge spikes but typically lag spot moves by weeks to months. Vertical integration of HMA plants and quarries commonly boosts gross margins by ~200 basis points and secures supply. Diesel averaged about $4.00/gal in 2024; hedging and logistics cut energy exposure materially.

Interest rates and capital intensity

Equipment fleets and plants require ongoing capex often financed amid a Federal Funds rate near 5.25–5.50% in 2024–25, raising borrowing and bond issuance costs (10‑yr Treasury ~4.2% mid‑2025). Higher rates push up required hurdle returns and bonding spreads, compressing bid competitiveness and margin. Public owners facing higher cost of capital have delayed or resized infrastructure projects. Rigorous fleet utilization and disciplined lease‑vs‑buy decisions preserve ROIC.

Regional growth in the Southeast

Rapid population and industrial in-migration in Southeast MSAs (Atlanta ~6.2m, Charlotte ~2.8m in 2024) expands road demand and local tax bases. Port expansions—Savannah handled about 5m TEU in 2023—and manufacturing reshoring plus rising housing starts drive ancillary roads, utilities and logistics infrastructure needs. Seasonality and hurricanes still dent productivity despite growth. Market concentration in select MSAs supports pricing power for transport and construction firms.

Labor market tightness

Skilled operators and paving crews remain scarce — about 80% of contractors reported hiring difficulty in 2024, pushing wage and overtime costs up roughly 5% year-over-year; productivity gains from training and tech (GPS/automation) offset some cost pressure. Subcontractor availability raises schedule risk and compresses bid margins. Retention programs cut rehire/onboarding costs across cycles.

- Hiring difficulty ~80% (AGC 2024)

- Wage growth ~5% YoY (2024)

- Tech/training boost productivity, lower unit labor cost

- Retention reduces rehire/onboarding spend

Backlog health and cash conversion

Strong backlog of about $2.8B (2024) stabilizes utilization near 85% and evens revenue cadence across quarters.

Higher share of public maintenance (~60%) versus large new-builds (~40%) supports steadier margins while new-build wins drive upside.

Mobilization timing, 5–10% retainage norms and slower change-order recovery lengthen working capital cycles; disciplined bidding preserved gross margin in 2024.

- Backlog $2.8B (2024)

- Utilization ~85%

- Public maintenance ~60%

- Retainage 5–10%

IIJA/BIL funding sustains backlog while procurement rules and labor caps squeeze margins

Input costs (asphalt/aggr/cement/diesel) drive 40–60% COGS; asphalt 15–25%; diesel ~$4.00/gal (2024). Fed funds ~5.25–5.50% and 10‑yr ~4.2% (mid‑2025) raise capex/bonding costs. Backlog ~$2.8B, utilization ~85%, public maintenance ~60%; hiring difficulty ~80%, wage growth ~5% (2024).

| Metric | Value |

|---|---|

| COGS share | 40–60% |

| Asphalt | 15–25% |

| Diesel (2024) | $4.00/gal |

| Fed funds | 5.25–5.50% |

| 10‑yr | ~4.2% |

| Backlog | $2.8B |

| Utilization | ~85% |

| Hiring difficulty | ~80% |

What You See Is What You Get

CPI PESTLE Analysis

The preview shown here is the exact CPI PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and layout match the downloadable file. No placeholders or surprises; this is the final product.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping CPI’s strategic outlook. Our concise PESTLE snapshot highlights immediate risks and opportunities. Buy the full analysis to access detailed, actionable intelligence and ready-to-use recommendations.

Political factors

Federal and state infrastructure funding

Revenue visibility hinges on appropriations such as the IIJA, which authorized roughly 550 billion dollars in new infrastructure investments, plus annual DOT appropriations and state transportation trust funds; multi‑year IIJA programs underpin sizable, stable backlogs but continuing resolutions can defer lettings and slow cash flow. Monitoring the federal gas tax (18.4 cents/gal) and state gas‑tax changes, toll adoption or mileage fees is critical for pipeline predictability. Strategic alignment with high‑spend states like Texas, Florida and Georgia mitigates funding volatility.

Procurement and bidding dynamics

Low-bid statutes, prequalification, and DB/DBB delivery models drive tighter margins and shift risk to contractors, while political priorities—evidenced by federal small-business contracting reaching 27.6% in FY2023—boost awards to small/minority firms, joint ventures, or alternative delivery. Recent procurement updates in states and agencies increasingly weight lifecycle cost and resilience, rewarding quality and innovation over lowest price. Strong agency relationships measurably improve win rates and change-order outcomes.

Transportation policy priorities

Safety, congestion relief, and rural connectivity shape project choices, driving targeted investments to reduce crashes and delays. The federal IIJA/BIL channels roughly 110 billion USD to roads and bridges, including about 40 billion for bridge repair and 5 billion for NEVI EV charging, prioritizing bridges, freight corridors, and EV corridors. Southeast states emphasize port access and hurricane evacuation routes, and industry advocacy steers standards and grant allocations.

Labor and immigration stance

Visa limits like the 66,000 annual H-2B cap and 26 states requiring E-Verify (2024) tighten craft-labor availability, pushing wages higher and raising hiring compliance costs. State public-works labor standards (prevailing wage, PLAs) elevate wage floors and administrative burden. Expanded federal/state technical-education and apprenticeship funding since IIJA has increased pipelines. Stronger worker-classification enforcement (AB5, more audits) constrains subcontracting models.

- 26 states require E-Verify (2024)

- H-2B cap 66,000 annually

- Construction employment ~7.6M (BLS 2024)

- AB5/audit focus limits subcontracting flexibility

Permitting and local governance

County and municipal politics control zoning, right-of-way and utility-relocation timelines and routinely impose permitting windows that extend project delivery timelines.

Local resistance or support can accelerate approvals or stall projects; coordination with more than 400 MPOs and state DOTs is essential for staging, detours and funding alignment.

The 2021 Bipartisan Infrastructure Law provided about 550 billion in new infrastructure funding, and election cycles (2–4 years) frequently reprioritize capital plans and maintenance schedules.

- Permitting delays: adds months to delivery

- Local politics: can stop or speed projects

- MPOs: >400 for regional coordination

- Funding: ~550 billion from 2021 BIL

- Elections: 2–4 year reprioritization

IIJA/BIL funding sustains backlog while procurement rules and labor caps squeeze margins

Policy drives revenue and risk: IIJA/BIL ≈550 billion sustains backlogs but continuing resolutions disrupt cash flow. Procurement rules and DB/DBB lower margins while small-business set‑asides (27.6% FY2023) shift awards. Labor constraints (H‑2B 66,000 cap; 26 states E‑Verify) tighten crews and raise costs.

| Metric | Value |

|---|---|

| IIJA/BIL | ≈550 billion |

| Federal gas tax | 18.4 cents/gal |

| H‑2B cap | 66,000 |

| Construction employment (BLS 2024) | ≈7.6M |

| States E‑Verify (2024) | 26 |

| MPOs | >400 |

What is included in the product

Explores how macro-environmental factors uniquely affect the CPI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends; designed for executives, consultants, and entrepreneurs to identify threats, opportunities, and support scenario planning, funding pitches, and strategy alignment with real market and regulatory dynamics.

Condenses CPI-related political, economic, social, technological, legal and environmental impacts into a clear, visually segmented brief that teams can share, edit, and drop into presentations to speed alignment and reduce analysis friction.

Economic factors

Material and fuel cost volatility

Asphalt cement, aggregates, cement and diesel can account for roughly 40–60% of COGS in paving, with asphalt cement often 15–25%. Index pricing and escalation clauses partially hedge spikes but typically lag spot moves by weeks to months. Vertical integration of HMA plants and quarries commonly boosts gross margins by ~200 basis points and secures supply. Diesel averaged about $4.00/gal in 2024; hedging and logistics cut energy exposure materially.

Interest rates and capital intensity

Equipment fleets and plants require ongoing capex often financed amid a Federal Funds rate near 5.25–5.50% in 2024–25, raising borrowing and bond issuance costs (10‑yr Treasury ~4.2% mid‑2025). Higher rates push up required hurdle returns and bonding spreads, compressing bid competitiveness and margin. Public owners facing higher cost of capital have delayed or resized infrastructure projects. Rigorous fleet utilization and disciplined lease‑vs‑buy decisions preserve ROIC.

Regional growth in the Southeast

Rapid population and industrial in-migration in Southeast MSAs (Atlanta ~6.2m, Charlotte ~2.8m in 2024) expands road demand and local tax bases. Port expansions—Savannah handled about 5m TEU in 2023—and manufacturing reshoring plus rising housing starts drive ancillary roads, utilities and logistics infrastructure needs. Seasonality and hurricanes still dent productivity despite growth. Market concentration in select MSAs supports pricing power for transport and construction firms.

Labor market tightness

Skilled operators and paving crews remain scarce — about 80% of contractors reported hiring difficulty in 2024, pushing wage and overtime costs up roughly 5% year-over-year; productivity gains from training and tech (GPS/automation) offset some cost pressure. Subcontractor availability raises schedule risk and compresses bid margins. Retention programs cut rehire/onboarding costs across cycles.

- Hiring difficulty ~80% (AGC 2024)

- Wage growth ~5% YoY (2024)

- Tech/training boost productivity, lower unit labor cost

- Retention reduces rehire/onboarding spend

Backlog health and cash conversion

Strong backlog of about $2.8B (2024) stabilizes utilization near 85% and evens revenue cadence across quarters.

Higher share of public maintenance (~60%) versus large new-builds (~40%) supports steadier margins while new-build wins drive upside.

Mobilization timing, 5–10% retainage norms and slower change-order recovery lengthen working capital cycles; disciplined bidding preserved gross margin in 2024.

- Backlog $2.8B (2024)

- Utilization ~85%

- Public maintenance ~60%

- Retainage 5–10%

IIJA/BIL funding sustains backlog while procurement rules and labor caps squeeze margins

Input costs (asphalt/aggr/cement/diesel) drive 40–60% COGS; asphalt 15–25%; diesel ~$4.00/gal (2024). Fed funds ~5.25–5.50% and 10‑yr ~4.2% (mid‑2025) raise capex/bonding costs. Backlog ~$2.8B, utilization ~85%, public maintenance ~60%; hiring difficulty ~80%, wage growth ~5% (2024).

| Metric | Value |

|---|---|

| COGS share | 40–60% |

| Asphalt | 15–25% |

| Diesel (2024) | $4.00/gal |

| Fed funds | 5.25–5.50% |

| 10‑yr | ~4.2% |

| Backlog | $2.8B |

| Utilization | ~85% |

| Hiring difficulty | ~80% |

What You See Is What You Get

CPI PESTLE Analysis

The preview shown here is the exact CPI PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and layout match the downloadable file. No placeholders or surprises; this is the final product.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping CPI’s strategic outlook. Our concise PESTLE snapshot highlights immediate risks and opportunities. Buy the full analysis to access detailed, actionable intelligence and ready-to-use recommendations.

Political factors

Federal and state infrastructure funding

Revenue visibility hinges on appropriations such as the IIJA, which authorized roughly 550 billion dollars in new infrastructure investments, plus annual DOT appropriations and state transportation trust funds; multi‑year IIJA programs underpin sizable, stable backlogs but continuing resolutions can defer lettings and slow cash flow. Monitoring the federal gas tax (18.4 cents/gal) and state gas‑tax changes, toll adoption or mileage fees is critical for pipeline predictability. Strategic alignment with high‑spend states like Texas, Florida and Georgia mitigates funding volatility.

Procurement and bidding dynamics

Low-bid statutes, prequalification, and DB/DBB delivery models drive tighter margins and shift risk to contractors, while political priorities—evidenced by federal small-business contracting reaching 27.6% in FY2023—boost awards to small/minority firms, joint ventures, or alternative delivery. Recent procurement updates in states and agencies increasingly weight lifecycle cost and resilience, rewarding quality and innovation over lowest price. Strong agency relationships measurably improve win rates and change-order outcomes.

Transportation policy priorities

Safety, congestion relief, and rural connectivity shape project choices, driving targeted investments to reduce crashes and delays. The federal IIJA/BIL channels roughly 110 billion USD to roads and bridges, including about 40 billion for bridge repair and 5 billion for NEVI EV charging, prioritizing bridges, freight corridors, and EV corridors. Southeast states emphasize port access and hurricane evacuation routes, and industry advocacy steers standards and grant allocations.

Labor and immigration stance

Visa limits like the 66,000 annual H-2B cap and 26 states requiring E-Verify (2024) tighten craft-labor availability, pushing wages higher and raising hiring compliance costs. State public-works labor standards (prevailing wage, PLAs) elevate wage floors and administrative burden. Expanded federal/state technical-education and apprenticeship funding since IIJA has increased pipelines. Stronger worker-classification enforcement (AB5, more audits) constrains subcontracting models.

- 26 states require E-Verify (2024)

- H-2B cap 66,000 annually

- Construction employment ~7.6M (BLS 2024)

- AB5/audit focus limits subcontracting flexibility

Permitting and local governance

County and municipal politics control zoning, right-of-way and utility-relocation timelines and routinely impose permitting windows that extend project delivery timelines.

Local resistance or support can accelerate approvals or stall projects; coordination with more than 400 MPOs and state DOTs is essential for staging, detours and funding alignment.

The 2021 Bipartisan Infrastructure Law provided about 550 billion in new infrastructure funding, and election cycles (2–4 years) frequently reprioritize capital plans and maintenance schedules.

- Permitting delays: adds months to delivery

- Local politics: can stop or speed projects

- MPOs: >400 for regional coordination

- Funding: ~550 billion from 2021 BIL

- Elections: 2–4 year reprioritization

IIJA/BIL funding sustains backlog while procurement rules and labor caps squeeze margins

Policy drives revenue and risk: IIJA/BIL ≈550 billion sustains backlogs but continuing resolutions disrupt cash flow. Procurement rules and DB/DBB lower margins while small-business set‑asides (27.6% FY2023) shift awards. Labor constraints (H‑2B 66,000 cap; 26 states E‑Verify) tighten crews and raise costs.

| Metric | Value |

|---|---|

| IIJA/BIL | ≈550 billion |

| Federal gas tax | 18.4 cents/gal |

| H‑2B cap | 66,000 |

| Construction employment (BLS 2024) | ≈7.6M |

| States E‑Verify (2024) | 26 |

| MPOs | >400 |

What is included in the product

Explores how macro-environmental factors uniquely affect the CPI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends; designed for executives, consultants, and entrepreneurs to identify threats, opportunities, and support scenario planning, funding pitches, and strategy alignment with real market and regulatory dynamics.

Condenses CPI-related political, economic, social, technological, legal and environmental impacts into a clear, visually segmented brief that teams can share, edit, and drop into presentations to speed alignment and reduce analysis friction.

Economic factors

Material and fuel cost volatility

Asphalt cement, aggregates, cement and diesel can account for roughly 40–60% of COGS in paving, with asphalt cement often 15–25%. Index pricing and escalation clauses partially hedge spikes but typically lag spot moves by weeks to months. Vertical integration of HMA plants and quarries commonly boosts gross margins by ~200 basis points and secures supply. Diesel averaged about $4.00/gal in 2024; hedging and logistics cut energy exposure materially.

Interest rates and capital intensity

Equipment fleets and plants require ongoing capex often financed amid a Federal Funds rate near 5.25–5.50% in 2024–25, raising borrowing and bond issuance costs (10‑yr Treasury ~4.2% mid‑2025). Higher rates push up required hurdle returns and bonding spreads, compressing bid competitiveness and margin. Public owners facing higher cost of capital have delayed or resized infrastructure projects. Rigorous fleet utilization and disciplined lease‑vs‑buy decisions preserve ROIC.

Regional growth in the Southeast

Rapid population and industrial in-migration in Southeast MSAs (Atlanta ~6.2m, Charlotte ~2.8m in 2024) expands road demand and local tax bases. Port expansions—Savannah handled about 5m TEU in 2023—and manufacturing reshoring plus rising housing starts drive ancillary roads, utilities and logistics infrastructure needs. Seasonality and hurricanes still dent productivity despite growth. Market concentration in select MSAs supports pricing power for transport and construction firms.

Labor market tightness

Skilled operators and paving crews remain scarce — about 80% of contractors reported hiring difficulty in 2024, pushing wage and overtime costs up roughly 5% year-over-year; productivity gains from training and tech (GPS/automation) offset some cost pressure. Subcontractor availability raises schedule risk and compresses bid margins. Retention programs cut rehire/onboarding costs across cycles.

- Hiring difficulty ~80% (AGC 2024)

- Wage growth ~5% YoY (2024)

- Tech/training boost productivity, lower unit labor cost

- Retention reduces rehire/onboarding spend

Backlog health and cash conversion

Strong backlog of about $2.8B (2024) stabilizes utilization near 85% and evens revenue cadence across quarters.

Higher share of public maintenance (~60%) versus large new-builds (~40%) supports steadier margins while new-build wins drive upside.

Mobilization timing, 5–10% retainage norms and slower change-order recovery lengthen working capital cycles; disciplined bidding preserved gross margin in 2024.

- Backlog $2.8B (2024)

- Utilization ~85%

- Public maintenance ~60%

- Retainage 5–10%

IIJA/BIL funding sustains backlog while procurement rules and labor caps squeeze margins

Input costs (asphalt/aggr/cement/diesel) drive 40–60% COGS; asphalt 15–25%; diesel ~$4.00/gal (2024). Fed funds ~5.25–5.50% and 10‑yr ~4.2% (mid‑2025) raise capex/bonding costs. Backlog ~$2.8B, utilization ~85%, public maintenance ~60%; hiring difficulty ~80%, wage growth ~5% (2024).

| Metric | Value |

|---|---|

| COGS share | 40–60% |

| Asphalt | 15–25% |

| Diesel (2024) | $4.00/gal |

| Fed funds | 5.25–5.50% |

| 10‑yr | ~4.2% |

| Backlog | $2.8B |

| Utilization | ~85% |

| Hiring difficulty | ~80% |

What You See Is What You Get

CPI PESTLE Analysis

The preview shown here is the exact CPI PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and layout match the downloadable file. No placeholders or surprises; this is the final product.