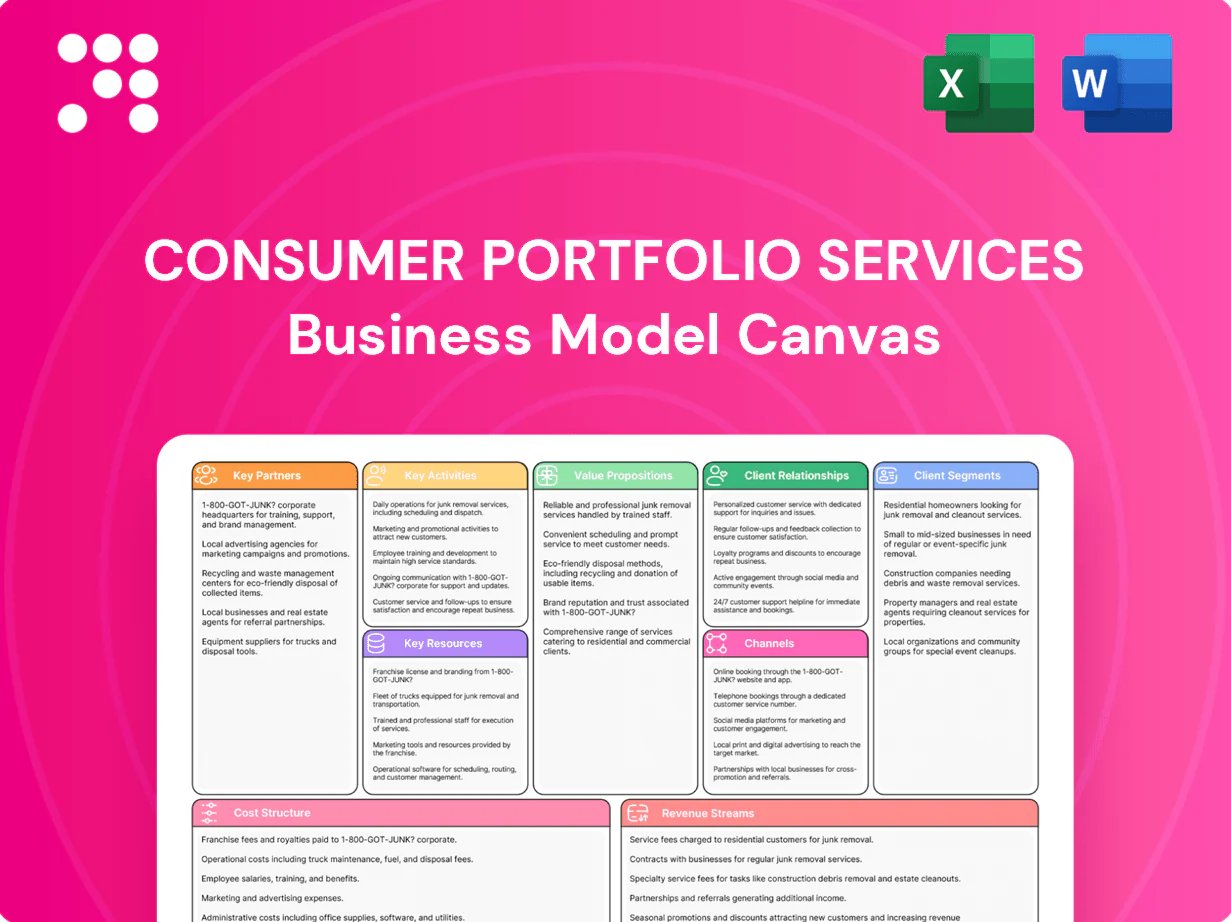

Consumer Portfolio Services Business Model Canvas

Subprime Auto Lender Canvas: Dealer Partnerships, Servicing, Interest Spread Monetization

Explore Consumer Portfolio Services’s Business Model Canvas to uncover how it targets niche subprime auto borrowers, leverages dealer partnerships, and monetizes through loan servicing and interest spreads. This concise snapshot highlights key partners, revenue streams, and cost drivers. Purchase the full Canvas for the editable, section-by-section analysis and actionable strategic insights.

Partnerships

Franchised and independent auto dealers

Franchised and independent dealers are CPSs primary origination source, funneling approved buyers at the point of sale and supplying a steady pipeline of retail contracts. TransUnion reported indirect auto originations at roughly 73% of retail volume in 2024, underscoring dealer importance. Preferred programs, training, and funding speed improve dealer loyalty and conversion. Volume incentives and performance scorecards align quality with flow.

Warehouse lenders and credit facilities

Consumer Portfolio Services funds loan purchases with short-term warehouse lines before securitization, with industry advance rates commonly in the 70–90% range and pre-securitization funding often covering 60–80% of loan cost; tighter covenants raise the effective cost of funds. Ongoing covenant compliance and transparent monthly reporting sustain lender trust, and using multiple facilities lowers concentration and liquidity risk.

Securitization investors and trustees

ABS investors provide term funding and risk transfer for CPS pools, with US ABS primary issuance topping roughly $420 billion in 2024 supporting market liquidity. Trustees, rating agencies and underwriters ensure structure, surveillance and market access, preserving investor confidence. Consistent collateral performance keeps execution reliable and spreads tight, and repeat issuance deepens and diversifies the investor base.

Third-party service providers and data vendors

- credit-bureaus: ~300M US consumer records

- fraud/verification: improve approval precision

- payment-processors: fees 1.5–3%

- skip-trace/repossession: collections support

- tech-partners: LOS/servicing/analytics

- vendor-risk: compliance & uptime

Regulatory and compliance advisors

Regulatory and compliance advisors — legal counsel, auditors, and consultants — guide CPS through complex federal and state rules, supporting UDAAP, fair lending, privacy, and servicing standards; 2024 saw elevated CFPB scrutiny and enforcement activity. Proactive guidance and regular policy updates reduce enforcement and litigation risk, where recent penalties frequently exceed $10 million per action. Ongoing training keeps operations current and audit-ready.

Indirect dealers ~73% drive originations; ABS $420B fuels funding

Franchised and independent dealers supply ~73% of indirect retail originations (TransUnion 2024) and are incentivized via preferred programs and scorecards. Warehouse lenders fund 60–80% pre-securitization advance rates with 70–90% industry advance norms. ABS investors provided liquidity as US primary ABS issuance ~ $420B in 2024; vendors and regulators (300M consumer records; >$10M enforcement risk) sustain operations.

| Partner | Role | 2024 Key Data |

|---|---|---|

| Dealers | Originations | ~73% indirect volume |

| Warehouse lenders | Short-term funding | Advance rates 70–90% |

| ABS investors | Term funding | US ABS $420B |

| Vendors | Underwriting/collections | Payment fees 1.5–3%; 300M records |

| Regulators/advisors | Compliance | Enforcement risk >$10M |

What is included in the product

A comprehensive, pre-written business model tailored to Consumer Portfolio Services' strategy, detailing customer segments, channels, value propositions, revenue streams, cost structure, and key resources. Organized into 9 BMC blocks with competitive analysis, SWOT linkages, and investor-ready narratives to support decision-making and funding discussions.

Editable one-page Business Model Canvas that distills Consumer Portfolio Services’ loan servicing, investor relations, and risk management into a concise format—ideal for identifying pain points, aligning teams, and accelerating strategic fixes.

Activities

Dealer onboarding and program management

Recruit, vet, and train dealers on CPS programs and submission processes, targeting 90%+ certification completion within 30 days and onboarding throughput improvements seen in 2024 fintech benchmarks. Monitor performance metrics—aiming for early payment default under 2% and repurchase rates below 1%—with real-time dashboards. Provide rapid decisioning and funding (90% same‑day funding target) to win deals. Maintain field reps (approx. 1 rep per 40 dealers) to strengthen relationships and resolve issues.

Risk-based underwriting and pricing

Assess credit using FICO (subprime <620, prime 620–739, super-prime ≥740), income verification, collateral valuation and employment/stability indicators.

Apply tiered pricing, advance limits and stipulations to balance yield and risk across segments.

Use scorecards and machine learning to refine cutoffs and back-test models monthly against realized portfolio outcomes.

Loan servicing and customer support

Manage payment processing, account maintenance, hardship requests and extensions across portfolios, handling high-volume flows to limit charge-offs; industry charge-off benchmarks in 2024 hovered near 3–4% for unsecured consumer credit. Offer omnichannel support (phone, SMS, email, app) to reduce delinquency friction—studies show engagement can lower delinquency 15–25%. Implement early intervention (prior-contact cure rates can rise up to ~30%) for at-risk accounts and ensure accurate, CFPB-aligned compliant communications to avoid regulatory penalties.

Collections, recovery, and loss mitigation

Collections, recovery, and loss mitigation deploy segmented strategies by risk, days past due, and behavior to prioritize early cure vs. repossession; industry subprime auto recovery rates ranged broadly 10–30% in 2024, with cost-per-recovery benchmarks guiding trade-offs. Use skip tracing and tailored payment plans, resorting to repossession only when recovery economics justify it; optimize remarketing via auctions and direct channels and track recovery rates and costs to refine tactics.

- Segment by risk/DPD

- Skip tracing & payment plans

- Repossession as last resort

- Auctions + direct remarketing

- Track recovery rate & cost per recovery

Securitization and capital markets execution

Aggregate homogeneous pools, structure multi-tranche ABS deals and manage ratings/disclosure while hedging interest-rate exposure and monitoring spread movements against a 2024 fed funds range near 5.25–5.50% to protect economics. Maintain investor relations with detailed data tapes and monthly performance reports and recycle capital to sustain originations and funding velocity.

Drive dealers: 90% cert/30d, <2% early default, FICO bands

Recruit/train dealers (90% cert/30d), monitor performance (early default <2%, repurchase <1%), 90% same‑day funding, 1 rep per 40 dealers. Use FICO bands (sub<620, prime 620–739, super≥740), ML scorecards, charge-off 3–4% (2024), delinquency reduction 15–25%, recovery 10–30% (2024).

| Metric | Target/2024 |

|---|---|

| Cert rate | 90%/30d |

| Early default | <2% |

| Same‑day funding | 90% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Consumer Portfolio Services Business Model Canvas, not a mockup. When you purchase, you’ll receive this exact file with all sections included, ready to edit and present. Formats provided are Word and Excel, matching what you see here.

Subprime Auto Lender Canvas: Dealer Partnerships, Servicing, Interest Spread Monetization

Explore Consumer Portfolio Services’s Business Model Canvas to uncover how it targets niche subprime auto borrowers, leverages dealer partnerships, and monetizes through loan servicing and interest spreads. This concise snapshot highlights key partners, revenue streams, and cost drivers. Purchase the full Canvas for the editable, section-by-section analysis and actionable strategic insights.

Partnerships

Franchised and independent auto dealers

Franchised and independent dealers are CPSs primary origination source, funneling approved buyers at the point of sale and supplying a steady pipeline of retail contracts. TransUnion reported indirect auto originations at roughly 73% of retail volume in 2024, underscoring dealer importance. Preferred programs, training, and funding speed improve dealer loyalty and conversion. Volume incentives and performance scorecards align quality with flow.

Warehouse lenders and credit facilities

Consumer Portfolio Services funds loan purchases with short-term warehouse lines before securitization, with industry advance rates commonly in the 70–90% range and pre-securitization funding often covering 60–80% of loan cost; tighter covenants raise the effective cost of funds. Ongoing covenant compliance and transparent monthly reporting sustain lender trust, and using multiple facilities lowers concentration and liquidity risk.

Securitization investors and trustees

ABS investors provide term funding and risk transfer for CPS pools, with US ABS primary issuance topping roughly $420 billion in 2024 supporting market liquidity. Trustees, rating agencies and underwriters ensure structure, surveillance and market access, preserving investor confidence. Consistent collateral performance keeps execution reliable and spreads tight, and repeat issuance deepens and diversifies the investor base.

Third-party service providers and data vendors

- credit-bureaus: ~300M US consumer records

- fraud/verification: improve approval precision

- payment-processors: fees 1.5–3%

- skip-trace/repossession: collections support

- tech-partners: LOS/servicing/analytics

- vendor-risk: compliance & uptime

Regulatory and compliance advisors

Regulatory and compliance advisors — legal counsel, auditors, and consultants — guide CPS through complex federal and state rules, supporting UDAAP, fair lending, privacy, and servicing standards; 2024 saw elevated CFPB scrutiny and enforcement activity. Proactive guidance and regular policy updates reduce enforcement and litigation risk, where recent penalties frequently exceed $10 million per action. Ongoing training keeps operations current and audit-ready.

Indirect dealers ~73% drive originations; ABS $420B fuels funding

Franchised and independent dealers supply ~73% of indirect retail originations (TransUnion 2024) and are incentivized via preferred programs and scorecards. Warehouse lenders fund 60–80% pre-securitization advance rates with 70–90% industry advance norms. ABS investors provided liquidity as US primary ABS issuance ~ $420B in 2024; vendors and regulators (300M consumer records; >$10M enforcement risk) sustain operations.

| Partner | Role | 2024 Key Data |

|---|---|---|

| Dealers | Originations | ~73% indirect volume |

| Warehouse lenders | Short-term funding | Advance rates 70–90% |

| ABS investors | Term funding | US ABS $420B |

| Vendors | Underwriting/collections | Payment fees 1.5–3%; 300M records |

| Regulators/advisors | Compliance | Enforcement risk >$10M |

What is included in the product

A comprehensive, pre-written business model tailored to Consumer Portfolio Services' strategy, detailing customer segments, channels, value propositions, revenue streams, cost structure, and key resources. Organized into 9 BMC blocks with competitive analysis, SWOT linkages, and investor-ready narratives to support decision-making and funding discussions.

Editable one-page Business Model Canvas that distills Consumer Portfolio Services’ loan servicing, investor relations, and risk management into a concise format—ideal for identifying pain points, aligning teams, and accelerating strategic fixes.

Activities

Dealer onboarding and program management

Recruit, vet, and train dealers on CPS programs and submission processes, targeting 90%+ certification completion within 30 days and onboarding throughput improvements seen in 2024 fintech benchmarks. Monitor performance metrics—aiming for early payment default under 2% and repurchase rates below 1%—with real-time dashboards. Provide rapid decisioning and funding (90% same‑day funding target) to win deals. Maintain field reps (approx. 1 rep per 40 dealers) to strengthen relationships and resolve issues.

Risk-based underwriting and pricing

Assess credit using FICO (subprime <620, prime 620–739, super-prime ≥740), income verification, collateral valuation and employment/stability indicators.

Apply tiered pricing, advance limits and stipulations to balance yield and risk across segments.

Use scorecards and machine learning to refine cutoffs and back-test models monthly against realized portfolio outcomes.

Loan servicing and customer support

Manage payment processing, account maintenance, hardship requests and extensions across portfolios, handling high-volume flows to limit charge-offs; industry charge-off benchmarks in 2024 hovered near 3–4% for unsecured consumer credit. Offer omnichannel support (phone, SMS, email, app) to reduce delinquency friction—studies show engagement can lower delinquency 15–25%. Implement early intervention (prior-contact cure rates can rise up to ~30%) for at-risk accounts and ensure accurate, CFPB-aligned compliant communications to avoid regulatory penalties.

Collections, recovery, and loss mitigation

Collections, recovery, and loss mitigation deploy segmented strategies by risk, days past due, and behavior to prioritize early cure vs. repossession; industry subprime auto recovery rates ranged broadly 10–30% in 2024, with cost-per-recovery benchmarks guiding trade-offs. Use skip tracing and tailored payment plans, resorting to repossession only when recovery economics justify it; optimize remarketing via auctions and direct channels and track recovery rates and costs to refine tactics.

- Segment by risk/DPD

- Skip tracing & payment plans

- Repossession as last resort

- Auctions + direct remarketing

- Track recovery rate & cost per recovery

Securitization and capital markets execution

Aggregate homogeneous pools, structure multi-tranche ABS deals and manage ratings/disclosure while hedging interest-rate exposure and monitoring spread movements against a 2024 fed funds range near 5.25–5.50% to protect economics. Maintain investor relations with detailed data tapes and monthly performance reports and recycle capital to sustain originations and funding velocity.

Drive dealers: 90% cert/30d, <2% early default, FICO bands

Recruit/train dealers (90% cert/30d), monitor performance (early default <2%, repurchase <1%), 90% same‑day funding, 1 rep per 40 dealers. Use FICO bands (sub<620, prime 620–739, super≥740), ML scorecards, charge-off 3–4% (2024), delinquency reduction 15–25%, recovery 10–30% (2024).

| Metric | Target/2024 |

|---|---|

| Cert rate | 90%/30d |

| Early default | <2% |

| Same‑day funding | 90% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Consumer Portfolio Services Business Model Canvas, not a mockup. When you purchase, you’ll receive this exact file with all sections included, ready to edit and present. Formats provided are Word and Excel, matching what you see here.

Description

Subprime Auto Lender Canvas: Dealer Partnerships, Servicing, Interest Spread Monetization

Explore Consumer Portfolio Services’s Business Model Canvas to uncover how it targets niche subprime auto borrowers, leverages dealer partnerships, and monetizes through loan servicing and interest spreads. This concise snapshot highlights key partners, revenue streams, and cost drivers. Purchase the full Canvas for the editable, section-by-section analysis and actionable strategic insights.

Partnerships

Franchised and independent auto dealers

Franchised and independent dealers are CPSs primary origination source, funneling approved buyers at the point of sale and supplying a steady pipeline of retail contracts. TransUnion reported indirect auto originations at roughly 73% of retail volume in 2024, underscoring dealer importance. Preferred programs, training, and funding speed improve dealer loyalty and conversion. Volume incentives and performance scorecards align quality with flow.

Warehouse lenders and credit facilities

Consumer Portfolio Services funds loan purchases with short-term warehouse lines before securitization, with industry advance rates commonly in the 70–90% range and pre-securitization funding often covering 60–80% of loan cost; tighter covenants raise the effective cost of funds. Ongoing covenant compliance and transparent monthly reporting sustain lender trust, and using multiple facilities lowers concentration and liquidity risk.

Securitization investors and trustees

ABS investors provide term funding and risk transfer for CPS pools, with US ABS primary issuance topping roughly $420 billion in 2024 supporting market liquidity. Trustees, rating agencies and underwriters ensure structure, surveillance and market access, preserving investor confidence. Consistent collateral performance keeps execution reliable and spreads tight, and repeat issuance deepens and diversifies the investor base.

Third-party service providers and data vendors

- credit-bureaus: ~300M US consumer records

- fraud/verification: improve approval precision

- payment-processors: fees 1.5–3%

- skip-trace/repossession: collections support

- tech-partners: LOS/servicing/analytics

- vendor-risk: compliance & uptime

Regulatory and compliance advisors

Regulatory and compliance advisors — legal counsel, auditors, and consultants — guide CPS through complex federal and state rules, supporting UDAAP, fair lending, privacy, and servicing standards; 2024 saw elevated CFPB scrutiny and enforcement activity. Proactive guidance and regular policy updates reduce enforcement and litigation risk, where recent penalties frequently exceed $10 million per action. Ongoing training keeps operations current and audit-ready.

Indirect dealers ~73% drive originations; ABS $420B fuels funding

Franchised and independent dealers supply ~73% of indirect retail originations (TransUnion 2024) and are incentivized via preferred programs and scorecards. Warehouse lenders fund 60–80% pre-securitization advance rates with 70–90% industry advance norms. ABS investors provided liquidity as US primary ABS issuance ~ $420B in 2024; vendors and regulators (300M consumer records; >$10M enforcement risk) sustain operations.

| Partner | Role | 2024 Key Data |

|---|---|---|

| Dealers | Originations | ~73% indirect volume |

| Warehouse lenders | Short-term funding | Advance rates 70–90% |

| ABS investors | Term funding | US ABS $420B |

| Vendors | Underwriting/collections | Payment fees 1.5–3%; 300M records |

| Regulators/advisors | Compliance | Enforcement risk >$10M |

What is included in the product

A comprehensive, pre-written business model tailored to Consumer Portfolio Services' strategy, detailing customer segments, channels, value propositions, revenue streams, cost structure, and key resources. Organized into 9 BMC blocks with competitive analysis, SWOT linkages, and investor-ready narratives to support decision-making and funding discussions.

Editable one-page Business Model Canvas that distills Consumer Portfolio Services’ loan servicing, investor relations, and risk management into a concise format—ideal for identifying pain points, aligning teams, and accelerating strategic fixes.

Activities

Dealer onboarding and program management

Recruit, vet, and train dealers on CPS programs and submission processes, targeting 90%+ certification completion within 30 days and onboarding throughput improvements seen in 2024 fintech benchmarks. Monitor performance metrics—aiming for early payment default under 2% and repurchase rates below 1%—with real-time dashboards. Provide rapid decisioning and funding (90% same‑day funding target) to win deals. Maintain field reps (approx. 1 rep per 40 dealers) to strengthen relationships and resolve issues.

Risk-based underwriting and pricing

Assess credit using FICO (subprime <620, prime 620–739, super-prime ≥740), income verification, collateral valuation and employment/stability indicators.

Apply tiered pricing, advance limits and stipulations to balance yield and risk across segments.

Use scorecards and machine learning to refine cutoffs and back-test models monthly against realized portfolio outcomes.

Loan servicing and customer support

Manage payment processing, account maintenance, hardship requests and extensions across portfolios, handling high-volume flows to limit charge-offs; industry charge-off benchmarks in 2024 hovered near 3–4% for unsecured consumer credit. Offer omnichannel support (phone, SMS, email, app) to reduce delinquency friction—studies show engagement can lower delinquency 15–25%. Implement early intervention (prior-contact cure rates can rise up to ~30%) for at-risk accounts and ensure accurate, CFPB-aligned compliant communications to avoid regulatory penalties.

Collections, recovery, and loss mitigation

Collections, recovery, and loss mitigation deploy segmented strategies by risk, days past due, and behavior to prioritize early cure vs. repossession; industry subprime auto recovery rates ranged broadly 10–30% in 2024, with cost-per-recovery benchmarks guiding trade-offs. Use skip tracing and tailored payment plans, resorting to repossession only when recovery economics justify it; optimize remarketing via auctions and direct channels and track recovery rates and costs to refine tactics.

- Segment by risk/DPD

- Skip tracing & payment plans

- Repossession as last resort

- Auctions + direct remarketing

- Track recovery rate & cost per recovery

Securitization and capital markets execution

Aggregate homogeneous pools, structure multi-tranche ABS deals and manage ratings/disclosure while hedging interest-rate exposure and monitoring spread movements against a 2024 fed funds range near 5.25–5.50% to protect economics. Maintain investor relations with detailed data tapes and monthly performance reports and recycle capital to sustain originations and funding velocity.

Drive dealers: 90% cert/30d, <2% early default, FICO bands

Recruit/train dealers (90% cert/30d), monitor performance (early default <2%, repurchase <1%), 90% same‑day funding, 1 rep per 40 dealers. Use FICO bands (sub<620, prime 620–739, super≥740), ML scorecards, charge-off 3–4% (2024), delinquency reduction 15–25%, recovery 10–30% (2024).

| Metric | Target/2024 |

|---|---|

| Cert rate | 90%/30d |

| Early default | <2% |

| Same‑day funding | 90% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Consumer Portfolio Services Business Model Canvas, not a mockup. When you purchase, you’ll receive this exact file with all sections included, ready to edit and present. Formats provided are Word and Excel, matching what you see here.