Consumer Portfolio Services Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

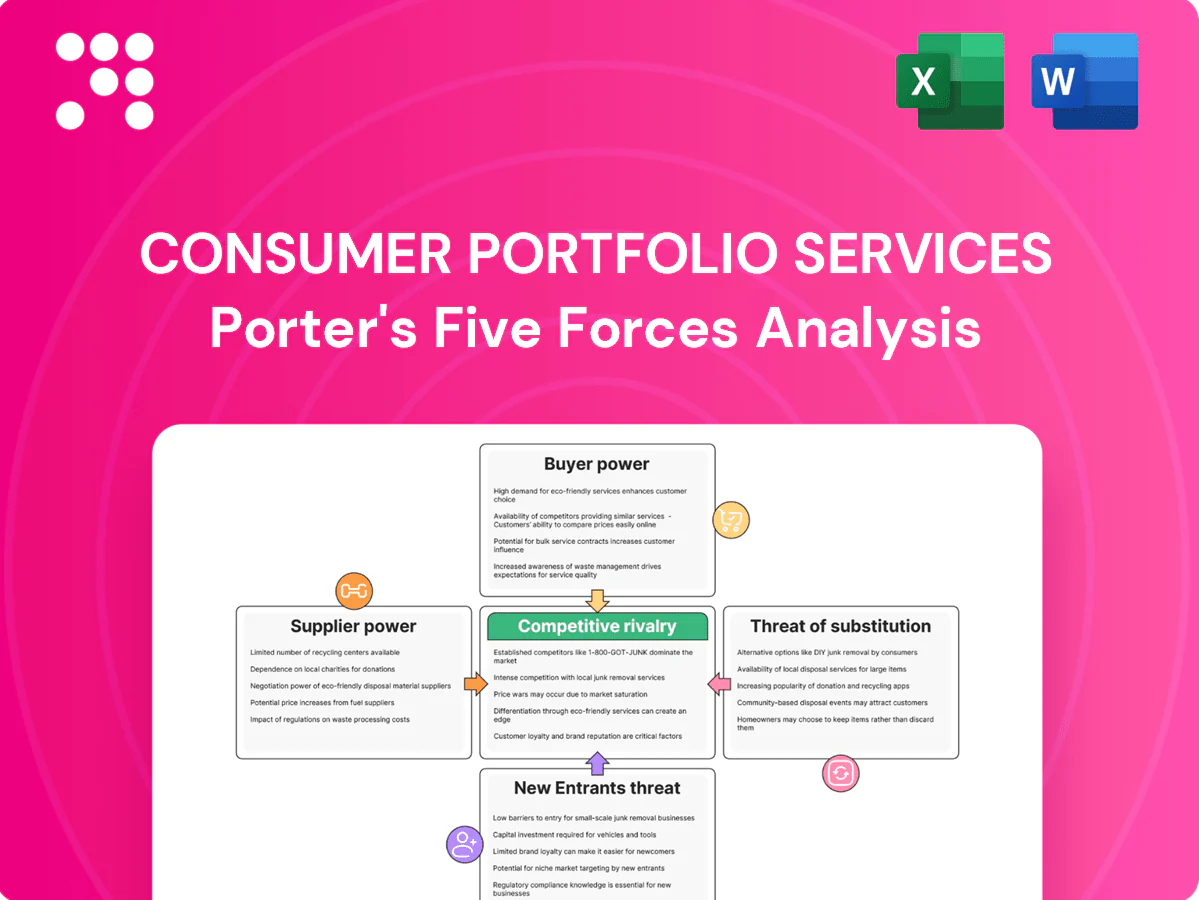

Consumer Portfolio Services faces moderate buyer power, niche supplier leverage, and mounting substitute risks as fintech and captive lenders reshape auto finance; barriers to entry remain moderate due to regulatory and capital demands. Competitive rivalry is intense among specialized servicers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Consumer Portfolio Services’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dealer contract supply concentration

Auto dealerships originate most contracts CPS purchases, making dealers pivotal suppliers; in a US auto loan market of about $1.5 trillion in 2024 their leverage is material. High-performing dealers can extract better advance rates, faster funding and fewer stipulations. In competitive metros dealer bargaining rises as lenders bid for subprime paper, so CPS diversifies dealer networks and tightens scorecards to mitigate concentration risk.

Funding and liquidity providers

Consumer Portfolio Services depends on warehouse credit lines, whole-loan buyers and ABS investors to finance originations, exposing it to supplier leverage. When credit markets tighten lenders and investors can demand wider spreads, stricter covenants and lower advance rates, raising CPS’s cost of funds and compressing net interest margins. With the federal funds rate around 5.25–5.50% in 2024, funding pressure is acute. Strong performance data and overcollateralization help CPS negotiate better terms.

Credit bureaus and data vendors

Underwriting relies on credit bureaus, alternative data and fraud tools, with the three national bureaus (Experian, TransUnion, Equifax) housing credit files for over 220 million US consumers and controlling >90% of report access, giving them moderate pricing power. Service interruptions or policy changes can disrupt decisioning and raise acquisition costs; CPS mitigates risk via multi-vendor setups to lower single-source dependency.

Servicing, recovery, and repo vendors

Repossession agents, auction houses, and skip-trace vendors materially affect loss severity and recovery timing for Consumer Portfolio Services; tight vendor capacity during high-default periods raises fees and extends timelines, while geographic coverage gaps increase friction and transport costs. Preferred networks and performance-based contracts can mitigate supplier leverage by aligning incentives and stabilizing pricing.

- Repossession agents: impact recovery speed

- Auction houses: affect recovery proceeds

- Skip-trace vendors: reduce location failure

- Preferred networks: lower costs, improve timelines

Technology and payment infrastructure

Loan-servicing systems, payment gateways and compliance tools are highly specialized and sticky, enabling vendors to impose periodic price escalators and integration fees; standard SLAs target 99.9% uptime while downtime can trigger regulatory penalties and severe customer-experience loss, reinforcing supplier leverage. Building internal tooling and modular integrations reduces this lock-in.

Dealers extract leverage in $1.5T auto market; funding costs at 5.25–5.50%

Dealers hold material leverage in a $1.5T US auto loan market (2024), extracting better advance rates; funding partners drive cost via spreads as the fed funds rate sits ~5.25–5.50% (2024). Three bureaus control credit files for ~220M US consumers (>90% access), while recovery and tech vendors exert pricing power via capacity and 99.9% SLA demands.

| Supplier | Leverage metric | 2024 stat |

|---|---|---|

| Dealers | Market origination share | $1.5T auto loans |

| Funding | Cost pressure | Fed funds 5.25–5.50% |

| Bureaus | File control | ~220M consumers, >90% |

| Vendors | SLA/capacity | 99.9% SLA |

What is included in the product

Tailored Porter’s Five Forces for Consumer Portfolio Services examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, identifying key drivers, disruptive risks, and strategic levers for profitability.

A concise one-sheet Porter's Five Forces for Consumer Portfolio Services—perfect for quick decision-making, board decks, and investor briefs, with customizable pressure levels to reflect evolving market trends or regulatory shifts.

Customers Bargaining Power

Subprime borrower price sensitivity

Subprime borrowers are payment-constrained and highly sensitive to APR and monthly payment, with industry reports in 2024 showing subprime APRs frequently exceed 15%. Limited access to prime credit reduces their negotiating leverage, keeping CPS pricing power intact. State rate caps (commonly around 36% APR in some jurisdictions) and regulatory scrutiny constrain pricing flexibility. Clear disclosures and affordability checks improve retention and compliance.

Dealer influence at point of sale

Dealers control the customer funnel and routinely steer contracts to competing lenders, negotiating buy rates, fees and deal stipulations to close sales; per Experian 2024, roughly 70% of vehicle finance contracts are originated at dealerships. Incentive programs and service speed materially sway dealer choice. CPS’s dealer-facing tech and sub-24‑hour funding turnaround reduce churn and win share.

Switching costs and alternatives

Borrowers face moderate switching costs after selecting a vehicle and lender, but at the pre-funding stage they can pivot quickly, especially in 2024 as pre-approvals and soft-pull offers became more common among lenders. Online fintechs and captive finance arms expanded alternatives for near-prime borrowers in 2023–24, increasing competitive pressure. For deeper subprime tiers alternatives narrow, lowering buyer power. Anchored pre-approvals shift selection earlier in the funnel.

Delinquency leverage

In hardship, borrowers increasingly seek extensions or loan modifications, directly affecting CPS cash flows; regulators report hundreds of thousands of debt-collection complaints annually (CFPB, 2023), pushing servicers to temper aggressive recovery. Collections must balance recovery with compliance and reputation, as regulatory scrutiny and consent orders modestly shift leverage to consumers. Proactive hardship programs reduce charge-offs and complaints, preserving recoveries and brand value.

Information transparency

Rate-shopping tools and dealer networks in 2024 increased visible pricing for many borrowers, but opaque F&I bundling still blocks true apples-to-apples comparison. CPS clarity on total cost and ancillary fees directly affects perceived fairness and retention; transparent pricing correlates with fewer disputes in 2024 market studies. Digital portals and clear disclosures lower chargebacks and customer service costs.

- 2024 trend: wider rate-shopping visibility

- Opaque F&I limits comparison

- CPS fee clarity boosts retention

- Digital disclosures reduce disputes

APRs >15%, dealer originations ~70% squeeze borrowers

Customers have limited leverage: subprime APRs commonly exceed 15% (2024), dealers originate ~70% of auto loans (Experian 2024) and steer business, while regulatory pressure and hundreds of thousands of CFPB complaints (2023) raise consumer negotiating power on collections and disclosures.

| Metric | Value | Implication |

|---|---|---|

| Subprime APRs | >15% (2024) | Low borrower leverage |

| Dealer originations | ~70% (2024) | Dealer bargaining power |

| CFPB complaints | Hundreds of thousands (2023) | Regulatory leverage for consumers |

Same Document Delivered

Consumer Portfolio Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Consumer Portfolio Services you'll receive—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download after purchase. What you see here is the final deliverable, available instantly upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Consumer Portfolio Services faces moderate buyer power, niche supplier leverage, and mounting substitute risks as fintech and captive lenders reshape auto finance; barriers to entry remain moderate due to regulatory and capital demands. Competitive rivalry is intense among specialized servicers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Consumer Portfolio Services’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dealer contract supply concentration

Auto dealerships originate most contracts CPS purchases, making dealers pivotal suppliers; in a US auto loan market of about $1.5 trillion in 2024 their leverage is material. High-performing dealers can extract better advance rates, faster funding and fewer stipulations. In competitive metros dealer bargaining rises as lenders bid for subprime paper, so CPS diversifies dealer networks and tightens scorecards to mitigate concentration risk.

Funding and liquidity providers

Consumer Portfolio Services depends on warehouse credit lines, whole-loan buyers and ABS investors to finance originations, exposing it to supplier leverage. When credit markets tighten lenders and investors can demand wider spreads, stricter covenants and lower advance rates, raising CPS’s cost of funds and compressing net interest margins. With the federal funds rate around 5.25–5.50% in 2024, funding pressure is acute. Strong performance data and overcollateralization help CPS negotiate better terms.

Credit bureaus and data vendors

Underwriting relies on credit bureaus, alternative data and fraud tools, with the three national bureaus (Experian, TransUnion, Equifax) housing credit files for over 220 million US consumers and controlling >90% of report access, giving them moderate pricing power. Service interruptions or policy changes can disrupt decisioning and raise acquisition costs; CPS mitigates risk via multi-vendor setups to lower single-source dependency.

Servicing, recovery, and repo vendors

Repossession agents, auction houses, and skip-trace vendors materially affect loss severity and recovery timing for Consumer Portfolio Services; tight vendor capacity during high-default periods raises fees and extends timelines, while geographic coverage gaps increase friction and transport costs. Preferred networks and performance-based contracts can mitigate supplier leverage by aligning incentives and stabilizing pricing.

- Repossession agents: impact recovery speed

- Auction houses: affect recovery proceeds

- Skip-trace vendors: reduce location failure

- Preferred networks: lower costs, improve timelines

Technology and payment infrastructure

Loan-servicing systems, payment gateways and compliance tools are highly specialized and sticky, enabling vendors to impose periodic price escalators and integration fees; standard SLAs target 99.9% uptime while downtime can trigger regulatory penalties and severe customer-experience loss, reinforcing supplier leverage. Building internal tooling and modular integrations reduces this lock-in.

Dealers extract leverage in $1.5T auto market; funding costs at 5.25–5.50%

Dealers hold material leverage in a $1.5T US auto loan market (2024), extracting better advance rates; funding partners drive cost via spreads as the fed funds rate sits ~5.25–5.50% (2024). Three bureaus control credit files for ~220M US consumers (>90% access), while recovery and tech vendors exert pricing power via capacity and 99.9% SLA demands.

| Supplier | Leverage metric | 2024 stat |

|---|---|---|

| Dealers | Market origination share | $1.5T auto loans |

| Funding | Cost pressure | Fed funds 5.25–5.50% |

| Bureaus | File control | ~220M consumers, >90% |

| Vendors | SLA/capacity | 99.9% SLA |

What is included in the product

Tailored Porter’s Five Forces for Consumer Portfolio Services examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, identifying key drivers, disruptive risks, and strategic levers for profitability.

A concise one-sheet Porter's Five Forces for Consumer Portfolio Services—perfect for quick decision-making, board decks, and investor briefs, with customizable pressure levels to reflect evolving market trends or regulatory shifts.

Customers Bargaining Power

Subprime borrower price sensitivity

Subprime borrowers are payment-constrained and highly sensitive to APR and monthly payment, with industry reports in 2024 showing subprime APRs frequently exceed 15%. Limited access to prime credit reduces their negotiating leverage, keeping CPS pricing power intact. State rate caps (commonly around 36% APR in some jurisdictions) and regulatory scrutiny constrain pricing flexibility. Clear disclosures and affordability checks improve retention and compliance.

Dealer influence at point of sale

Dealers control the customer funnel and routinely steer contracts to competing lenders, negotiating buy rates, fees and deal stipulations to close sales; per Experian 2024, roughly 70% of vehicle finance contracts are originated at dealerships. Incentive programs and service speed materially sway dealer choice. CPS’s dealer-facing tech and sub-24‑hour funding turnaround reduce churn and win share.

Switching costs and alternatives

Borrowers face moderate switching costs after selecting a vehicle and lender, but at the pre-funding stage they can pivot quickly, especially in 2024 as pre-approvals and soft-pull offers became more common among lenders. Online fintechs and captive finance arms expanded alternatives for near-prime borrowers in 2023–24, increasing competitive pressure. For deeper subprime tiers alternatives narrow, lowering buyer power. Anchored pre-approvals shift selection earlier in the funnel.

Delinquency leverage

In hardship, borrowers increasingly seek extensions or loan modifications, directly affecting CPS cash flows; regulators report hundreds of thousands of debt-collection complaints annually (CFPB, 2023), pushing servicers to temper aggressive recovery. Collections must balance recovery with compliance and reputation, as regulatory scrutiny and consent orders modestly shift leverage to consumers. Proactive hardship programs reduce charge-offs and complaints, preserving recoveries and brand value.

Information transparency

Rate-shopping tools and dealer networks in 2024 increased visible pricing for many borrowers, but opaque F&I bundling still blocks true apples-to-apples comparison. CPS clarity on total cost and ancillary fees directly affects perceived fairness and retention; transparent pricing correlates with fewer disputes in 2024 market studies. Digital portals and clear disclosures lower chargebacks and customer service costs.

- 2024 trend: wider rate-shopping visibility

- Opaque F&I limits comparison

- CPS fee clarity boosts retention

- Digital disclosures reduce disputes

APRs >15%, dealer originations ~70% squeeze borrowers

Customers have limited leverage: subprime APRs commonly exceed 15% (2024), dealers originate ~70% of auto loans (Experian 2024) and steer business, while regulatory pressure and hundreds of thousands of CFPB complaints (2023) raise consumer negotiating power on collections and disclosures.

| Metric | Value | Implication |

|---|---|---|

| Subprime APRs | >15% (2024) | Low borrower leverage |

| Dealer originations | ~70% (2024) | Dealer bargaining power |

| CFPB complaints | Hundreds of thousands (2023) | Regulatory leverage for consumers |

Same Document Delivered

Consumer Portfolio Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Consumer Portfolio Services you'll receive—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download after purchase. What you see here is the final deliverable, available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Consumer Portfolio Services faces moderate buyer power, niche supplier leverage, and mounting substitute risks as fintech and captive lenders reshape auto finance; barriers to entry remain moderate due to regulatory and capital demands. Competitive rivalry is intense among specialized servicers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Consumer Portfolio Services’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dealer contract supply concentration

Auto dealerships originate most contracts CPS purchases, making dealers pivotal suppliers; in a US auto loan market of about $1.5 trillion in 2024 their leverage is material. High-performing dealers can extract better advance rates, faster funding and fewer stipulations. In competitive metros dealer bargaining rises as lenders bid for subprime paper, so CPS diversifies dealer networks and tightens scorecards to mitigate concentration risk.

Funding and liquidity providers

Consumer Portfolio Services depends on warehouse credit lines, whole-loan buyers and ABS investors to finance originations, exposing it to supplier leverage. When credit markets tighten lenders and investors can demand wider spreads, stricter covenants and lower advance rates, raising CPS’s cost of funds and compressing net interest margins. With the federal funds rate around 5.25–5.50% in 2024, funding pressure is acute. Strong performance data and overcollateralization help CPS negotiate better terms.

Credit bureaus and data vendors

Underwriting relies on credit bureaus, alternative data and fraud tools, with the three national bureaus (Experian, TransUnion, Equifax) housing credit files for over 220 million US consumers and controlling >90% of report access, giving them moderate pricing power. Service interruptions or policy changes can disrupt decisioning and raise acquisition costs; CPS mitigates risk via multi-vendor setups to lower single-source dependency.

Servicing, recovery, and repo vendors

Repossession agents, auction houses, and skip-trace vendors materially affect loss severity and recovery timing for Consumer Portfolio Services; tight vendor capacity during high-default periods raises fees and extends timelines, while geographic coverage gaps increase friction and transport costs. Preferred networks and performance-based contracts can mitigate supplier leverage by aligning incentives and stabilizing pricing.

- Repossession agents: impact recovery speed

- Auction houses: affect recovery proceeds

- Skip-trace vendors: reduce location failure

- Preferred networks: lower costs, improve timelines

Technology and payment infrastructure

Loan-servicing systems, payment gateways and compliance tools are highly specialized and sticky, enabling vendors to impose periodic price escalators and integration fees; standard SLAs target 99.9% uptime while downtime can trigger regulatory penalties and severe customer-experience loss, reinforcing supplier leverage. Building internal tooling and modular integrations reduces this lock-in.

Dealers extract leverage in $1.5T auto market; funding costs at 5.25–5.50%

Dealers hold material leverage in a $1.5T US auto loan market (2024), extracting better advance rates; funding partners drive cost via spreads as the fed funds rate sits ~5.25–5.50% (2024). Three bureaus control credit files for ~220M US consumers (>90% access), while recovery and tech vendors exert pricing power via capacity and 99.9% SLA demands.

| Supplier | Leverage metric | 2024 stat |

|---|---|---|

| Dealers | Market origination share | $1.5T auto loans |

| Funding | Cost pressure | Fed funds 5.25–5.50% |

| Bureaus | File control | ~220M consumers, >90% |

| Vendors | SLA/capacity | 99.9% SLA |

What is included in the product

Tailored Porter’s Five Forces for Consumer Portfolio Services examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, identifying key drivers, disruptive risks, and strategic levers for profitability.

A concise one-sheet Porter's Five Forces for Consumer Portfolio Services—perfect for quick decision-making, board decks, and investor briefs, with customizable pressure levels to reflect evolving market trends or regulatory shifts.

Customers Bargaining Power

Subprime borrower price sensitivity

Subprime borrowers are payment-constrained and highly sensitive to APR and monthly payment, with industry reports in 2024 showing subprime APRs frequently exceed 15%. Limited access to prime credit reduces their negotiating leverage, keeping CPS pricing power intact. State rate caps (commonly around 36% APR in some jurisdictions) and regulatory scrutiny constrain pricing flexibility. Clear disclosures and affordability checks improve retention and compliance.

Dealer influence at point of sale

Dealers control the customer funnel and routinely steer contracts to competing lenders, negotiating buy rates, fees and deal stipulations to close sales; per Experian 2024, roughly 70% of vehicle finance contracts are originated at dealerships. Incentive programs and service speed materially sway dealer choice. CPS’s dealer-facing tech and sub-24‑hour funding turnaround reduce churn and win share.

Switching costs and alternatives

Borrowers face moderate switching costs after selecting a vehicle and lender, but at the pre-funding stage they can pivot quickly, especially in 2024 as pre-approvals and soft-pull offers became more common among lenders. Online fintechs and captive finance arms expanded alternatives for near-prime borrowers in 2023–24, increasing competitive pressure. For deeper subprime tiers alternatives narrow, lowering buyer power. Anchored pre-approvals shift selection earlier in the funnel.

Delinquency leverage

In hardship, borrowers increasingly seek extensions or loan modifications, directly affecting CPS cash flows; regulators report hundreds of thousands of debt-collection complaints annually (CFPB, 2023), pushing servicers to temper aggressive recovery. Collections must balance recovery with compliance and reputation, as regulatory scrutiny and consent orders modestly shift leverage to consumers. Proactive hardship programs reduce charge-offs and complaints, preserving recoveries and brand value.

Information transparency

Rate-shopping tools and dealer networks in 2024 increased visible pricing for many borrowers, but opaque F&I bundling still blocks true apples-to-apples comparison. CPS clarity on total cost and ancillary fees directly affects perceived fairness and retention; transparent pricing correlates with fewer disputes in 2024 market studies. Digital portals and clear disclosures lower chargebacks and customer service costs.

- 2024 trend: wider rate-shopping visibility

- Opaque F&I limits comparison

- CPS fee clarity boosts retention

- Digital disclosures reduce disputes

APRs >15%, dealer originations ~70% squeeze borrowers

Customers have limited leverage: subprime APRs commonly exceed 15% (2024), dealers originate ~70% of auto loans (Experian 2024) and steer business, while regulatory pressure and hundreds of thousands of CFPB complaints (2023) raise consumer negotiating power on collections and disclosures.

| Metric | Value | Implication |

|---|---|---|

| Subprime APRs | >15% (2024) | Low borrower leverage |

| Dealer originations | ~70% (2024) | Dealer bargaining power |

| CFPB complaints | Hundreds of thousands (2023) | Regulatory leverage for consumers |

Same Document Delivered

Consumer Portfolio Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Consumer Portfolio Services you'll receive—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download after purchase. What you see here is the final deliverable, available instantly upon payment.