Contec Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

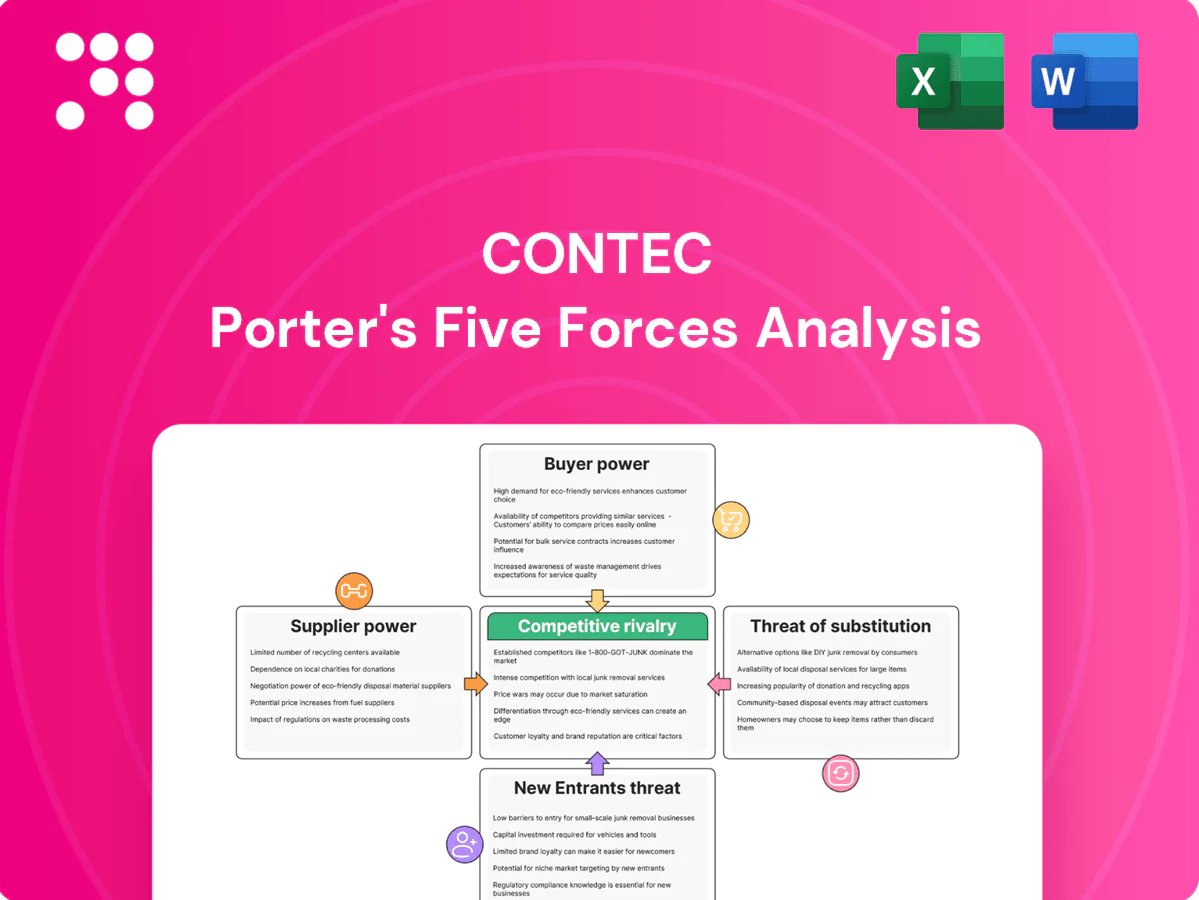

Contec’s Porter's Five Forces snapshot highlights competitive dynamics, supplier and buyer power, threat of substitutes, and barriers to entry shaping its sector. This brief identifies key pressure points and strategic levers but stops short of force-by-force ratings and visual evidence. Unlock the full Porter's Five Forces Analysis for detailed ratings, charts, and actionable strategic recommendations to inform investment or planning decisions.

Suppliers Bargaining Power

Semiconductor and specialty component concentration

Contec depends on CPUs, FPGAs, memory and rugged power ICs from a concentrated set of global vendors (TSMC/Intel foundry-led ecosystems; FPGA duopoly AMD/Intel; memory top 3 Samsung/SK Hynix/Micron ~75–80% share), giving upstream firms pricing and allocation leverage. Silicon roadmaps, allocation cycles and EOL notices drive lead times often 20–40+ weeks and qualification windows of months, limiting swift supplier switches. Multi-sourcing and design-to-availability reduce risk but cannot fully remove supplier bargaining power.

Industrial-grade specs and certifications

Industrial-temperature, shock/vibration, EMC, safety and medical/rail approvals force Contec to buy certified components from niche suppliers that typically command 20–40% price premiums and minimum order quantities often of 100–1,000 units; substitution triggers revalidation programs that can cost $50k–$250k and extend qualification cycles, while approved-vendor lists lock designs and increase supplier dependence.

Contract manufacturing and EMS dependence

For boards and system integration, EMS partners control capacity, yields and costs, giving them leverage especially when regional supply constraints and tight labor markets limit alternatives. Transitioning EMS is costly due to tooling, NPI learning curves and extended quality ramp-up, raising switching barriers. Companies commonly use long-term agreements and volume commitments to lock capacity and mitigate supplier bargaining power.

Software stacks and OS licensing

Software stacks and OS licensing (real-time OS, Windows IoT, Linux distros, middleware) materially affect Contec’s BOM and lifecycle support; license terms, patch cadence and LTS fees give software suppliers leverage, and kernel/driver compatibility can tie hardware refresh cycles to vendor roadmaps. Contec can lower exposure with open-source adoption and in-house expertise, though paid support SLAs remain critical.

- Real-time OS vs Windows IoT vs Linux

- License, patch cadence, LTS fees

- Kernel/driver lock-in ties refresh

- Mitigation: open-source + in-house + SLAs

Interconnects, sensors, and module ecosystems

Rugged connectors, DAQ modules, and wireless modems are sourced from specialized vendors, giving suppliers measurable leverage as form-factor standards like PCIe, PXI, and COM Express constrain substitutions; in 2024 supply lead times often exceeded 12 weeks for niche modules, tightening negotiation power. Performance and durability specs further narrow the supplier pool, while strategic alliances and buffer inventory are used to stabilize supply risk.

- Specialized vendors: limited substitutes

- Form-factor lock-in: PCIe/PXI/COM Express

- Lead times: >12 weeks in 2024

- Mitigants: alliances + buffer inventory

Supplier concentration risks: memory top-3 75-80%, long lead times

Contec faces high supplier power: memory top-3 hold ~75–80% share and FPGA/CPU ecosystems concentrate sourcing, creating pricing/allocation leverage and 20–40+ week lead times. Certified industrial components carry 20–40% price premiums and revalidation can cost $50k–$250k, raising switching barriers. EMS, niche modules and software licenses add capacity, certification and lifecycle lock-in, mitigated via multi-sourcing, inventory and long-term agreements.

| Metric | 2024 Value |

|---|---|

| Memory market share (top3) | 75–80% |

| Component lead times | 20–40+ weeks |

| Price premium (certified) | 20–40% |

| Revalidation cost | $50k–$250k |

| Niche module lead times | >12 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Contec that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive trends and strategic levers to protect or grow market share.

A compact one-sheet Porter's Five Forces for Contec—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart; clean layout fits decks or dashboards with no macros required.

Customers Bargaining Power

Large OEMs and system integrators

Contec’s core customers—large OEMs and system integrators—buy in multi-million-dollar volumes and exert strong negotiation clout, pushing for customizations, lifecycle guarantees and service credits. Competitive bidding among IPC vendors amplifies buyer leverage and compresses margins. Framework agreements and dual-sourcing are standard procurement strategies, forcing suppliers to offer tighter terms and rapid support.

High switching costs with qualification

Industrial and medical deployments often require 6–18 months of validation before design-in, locking buyers post-award and raising real switching costs; however, pre-design buyers typically extract 5–20% price concessions by leveraging alternative vendors. Decisions lean on total cost of ownership rather than unit price, and long product lifecycles (7–15 years) both amortize switching friction and intensify pre-award bargaining pressure.

Price sensitivity in commoditized segments

Standard embedded PCs, SBCs and IoT gateways face high price transparency, with industry buyer surveys in 2024 citing typical price differentials of 15–25% between branded players (Advantech, Kontron) and white-label ODMs.

Buyers benchmark rigorously against Advantech and Kontron; volume discounts and value-add bundling now determine procurement decisions in >50% of enterprise RFPs.

Differentiation through ruggedness certifications and premium service contracts is required to defend 8–12% higher margins versus ODM commodity levels.

Demand for uptime and SLAs

Factory automation and transportation customers demand high reliability and rapid RMA turnaround (typical SLAs target 99.9% uptime and 24–72 hour RMAs in 2024), giving them leverage to negotiate strict penalties. They push stringent SLAs that raise switching costs; vendors offering predictive maintenance and remote support — shown in 2024 studies to cut unplanned downtime ~30% — can justify 10–15% premium pricing. Service quality heavily influences rebids and renewals, with SLA breaches reducing renewal rates materially.

- 99.9% uptime targets (2024)

- 24–72h RMA expectations

- ~30% downtime reduction via predictive maintenance (2024)

- 10–15% premium for integrated service offerings

Interoperability and open standards

Buyers now insist on native support for OPC UA, MQTT, EtherCAT and major cloud platforms; 2024 surveys show over 60% of industrial buyers rate open standards as critical to purchase decisions. Open standards materially lower vendor lock-in and increase switching; Contec must sustain broad driver and protocol support to remain shortlisted. Certification programs and reference architectures improve account retention and shorten deployment cycles.

- compatibility: OPC UA, MQTT, EtherCAT, cloud

- market metric: >60% buyers prioritize open standards (2024)

- strategy: broad driver support + certification + reference architectures

OEM leverage squeezes margins; SLAs & open standards unlock 10–15% service premiums

Contec’s large OEM buyers wield strong price and SLA leverage, extracting 5–20% pre-design concessions and driving framework/dual-sourcing that compresses margins. High price transparency yields 15–25% branded vs ODM gaps, while >50% enterprise RFPs prioritize volume discounts and bundling. Open standards matter: >60% of industrial buyers rate them critical. Service SLAs (99.9% uptime, 24–72h RMA) and predictive maintenance (~30% downtime reduction) dictate premiums of 10–15%.

| Metric | 2024 datapoint |

|---|---|

| Pre-design price concessions | 5–20% |

| Branded vs ODM price gap | 15–25% |

| Buyers prioritizing open standards | >60% |

| Enterprise RFPs using volume discounts | >50% |

| Uptime SLA | 99.9% |

| RMA expectation | 24–72h |

| Downtime reduction via PdM | ~30% |

| Service premium achievable | 10–15% |

What You See Is What You Get

Contec Porter's Five Forces Analysis

This preview shows the exact Contec Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the full, final deliverable; instant access to this same file is provided upon payment.

A Must-Have Tool for Decision-Makers

Contec’s Porter's Five Forces snapshot highlights competitive dynamics, supplier and buyer power, threat of substitutes, and barriers to entry shaping its sector. This brief identifies key pressure points and strategic levers but stops short of force-by-force ratings and visual evidence. Unlock the full Porter's Five Forces Analysis for detailed ratings, charts, and actionable strategic recommendations to inform investment or planning decisions.

Suppliers Bargaining Power

Semiconductor and specialty component concentration

Contec depends on CPUs, FPGAs, memory and rugged power ICs from a concentrated set of global vendors (TSMC/Intel foundry-led ecosystems; FPGA duopoly AMD/Intel; memory top 3 Samsung/SK Hynix/Micron ~75–80% share), giving upstream firms pricing and allocation leverage. Silicon roadmaps, allocation cycles and EOL notices drive lead times often 20–40+ weeks and qualification windows of months, limiting swift supplier switches. Multi-sourcing and design-to-availability reduce risk but cannot fully remove supplier bargaining power.

Industrial-grade specs and certifications

Industrial-temperature, shock/vibration, EMC, safety and medical/rail approvals force Contec to buy certified components from niche suppliers that typically command 20–40% price premiums and minimum order quantities often of 100–1,000 units; substitution triggers revalidation programs that can cost $50k–$250k and extend qualification cycles, while approved-vendor lists lock designs and increase supplier dependence.

Contract manufacturing and EMS dependence

For boards and system integration, EMS partners control capacity, yields and costs, giving them leverage especially when regional supply constraints and tight labor markets limit alternatives. Transitioning EMS is costly due to tooling, NPI learning curves and extended quality ramp-up, raising switching barriers. Companies commonly use long-term agreements and volume commitments to lock capacity and mitigate supplier bargaining power.

Software stacks and OS licensing

Software stacks and OS licensing (real-time OS, Windows IoT, Linux distros, middleware) materially affect Contec’s BOM and lifecycle support; license terms, patch cadence and LTS fees give software suppliers leverage, and kernel/driver compatibility can tie hardware refresh cycles to vendor roadmaps. Contec can lower exposure with open-source adoption and in-house expertise, though paid support SLAs remain critical.

- Real-time OS vs Windows IoT vs Linux

- License, patch cadence, LTS fees

- Kernel/driver lock-in ties refresh

- Mitigation: open-source + in-house + SLAs

Interconnects, sensors, and module ecosystems

Rugged connectors, DAQ modules, and wireless modems are sourced from specialized vendors, giving suppliers measurable leverage as form-factor standards like PCIe, PXI, and COM Express constrain substitutions; in 2024 supply lead times often exceeded 12 weeks for niche modules, tightening negotiation power. Performance and durability specs further narrow the supplier pool, while strategic alliances and buffer inventory are used to stabilize supply risk.

- Specialized vendors: limited substitutes

- Form-factor lock-in: PCIe/PXI/COM Express

- Lead times: >12 weeks in 2024

- Mitigants: alliances + buffer inventory

Supplier concentration risks: memory top-3 75-80%, long lead times

Contec faces high supplier power: memory top-3 hold ~75–80% share and FPGA/CPU ecosystems concentrate sourcing, creating pricing/allocation leverage and 20–40+ week lead times. Certified industrial components carry 20–40% price premiums and revalidation can cost $50k–$250k, raising switching barriers. EMS, niche modules and software licenses add capacity, certification and lifecycle lock-in, mitigated via multi-sourcing, inventory and long-term agreements.

| Metric | 2024 Value |

|---|---|

| Memory market share (top3) | 75–80% |

| Component lead times | 20–40+ weeks |

| Price premium (certified) | 20–40% |

| Revalidation cost | $50k–$250k |

| Niche module lead times | >12 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Contec that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive trends and strategic levers to protect or grow market share.

A compact one-sheet Porter's Five Forces for Contec—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart; clean layout fits decks or dashboards with no macros required.

Customers Bargaining Power

Large OEMs and system integrators

Contec’s core customers—large OEMs and system integrators—buy in multi-million-dollar volumes and exert strong negotiation clout, pushing for customizations, lifecycle guarantees and service credits. Competitive bidding among IPC vendors amplifies buyer leverage and compresses margins. Framework agreements and dual-sourcing are standard procurement strategies, forcing suppliers to offer tighter terms and rapid support.

High switching costs with qualification

Industrial and medical deployments often require 6–18 months of validation before design-in, locking buyers post-award and raising real switching costs; however, pre-design buyers typically extract 5–20% price concessions by leveraging alternative vendors. Decisions lean on total cost of ownership rather than unit price, and long product lifecycles (7–15 years) both amortize switching friction and intensify pre-award bargaining pressure.

Price sensitivity in commoditized segments

Standard embedded PCs, SBCs and IoT gateways face high price transparency, with industry buyer surveys in 2024 citing typical price differentials of 15–25% between branded players (Advantech, Kontron) and white-label ODMs.

Buyers benchmark rigorously against Advantech and Kontron; volume discounts and value-add bundling now determine procurement decisions in >50% of enterprise RFPs.

Differentiation through ruggedness certifications and premium service contracts is required to defend 8–12% higher margins versus ODM commodity levels.

Demand for uptime and SLAs

Factory automation and transportation customers demand high reliability and rapid RMA turnaround (typical SLAs target 99.9% uptime and 24–72 hour RMAs in 2024), giving them leverage to negotiate strict penalties. They push stringent SLAs that raise switching costs; vendors offering predictive maintenance and remote support — shown in 2024 studies to cut unplanned downtime ~30% — can justify 10–15% premium pricing. Service quality heavily influences rebids and renewals, with SLA breaches reducing renewal rates materially.

- 99.9% uptime targets (2024)

- 24–72h RMA expectations

- ~30% downtime reduction via predictive maintenance (2024)

- 10–15% premium for integrated service offerings

Interoperability and open standards

Buyers now insist on native support for OPC UA, MQTT, EtherCAT and major cloud platforms; 2024 surveys show over 60% of industrial buyers rate open standards as critical to purchase decisions. Open standards materially lower vendor lock-in and increase switching; Contec must sustain broad driver and protocol support to remain shortlisted. Certification programs and reference architectures improve account retention and shorten deployment cycles.

- compatibility: OPC UA, MQTT, EtherCAT, cloud

- market metric: >60% buyers prioritize open standards (2024)

- strategy: broad driver support + certification + reference architectures

OEM leverage squeezes margins; SLAs & open standards unlock 10–15% service premiums

Contec’s large OEM buyers wield strong price and SLA leverage, extracting 5–20% pre-design concessions and driving framework/dual-sourcing that compresses margins. High price transparency yields 15–25% branded vs ODM gaps, while >50% enterprise RFPs prioritize volume discounts and bundling. Open standards matter: >60% of industrial buyers rate them critical. Service SLAs (99.9% uptime, 24–72h RMA) and predictive maintenance (~30% downtime reduction) dictate premiums of 10–15%.

| Metric | 2024 datapoint |

|---|---|

| Pre-design price concessions | 5–20% |

| Branded vs ODM price gap | 15–25% |

| Buyers prioritizing open standards | >60% |

| Enterprise RFPs using volume discounts | >50% |

| Uptime SLA | 99.9% |

| RMA expectation | 24–72h |

| Downtime reduction via PdM | ~30% |

| Service premium achievable | 10–15% |

What You See Is What You Get

Contec Porter's Five Forces Analysis

This preview shows the exact Contec Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the full, final deliverable; instant access to this same file is provided upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Contec’s Porter's Five Forces snapshot highlights competitive dynamics, supplier and buyer power, threat of substitutes, and barriers to entry shaping its sector. This brief identifies key pressure points and strategic levers but stops short of force-by-force ratings and visual evidence. Unlock the full Porter's Five Forces Analysis for detailed ratings, charts, and actionable strategic recommendations to inform investment or planning decisions.

Suppliers Bargaining Power

Semiconductor and specialty component concentration

Contec depends on CPUs, FPGAs, memory and rugged power ICs from a concentrated set of global vendors (TSMC/Intel foundry-led ecosystems; FPGA duopoly AMD/Intel; memory top 3 Samsung/SK Hynix/Micron ~75–80% share), giving upstream firms pricing and allocation leverage. Silicon roadmaps, allocation cycles and EOL notices drive lead times often 20–40+ weeks and qualification windows of months, limiting swift supplier switches. Multi-sourcing and design-to-availability reduce risk but cannot fully remove supplier bargaining power.

Industrial-grade specs and certifications

Industrial-temperature, shock/vibration, EMC, safety and medical/rail approvals force Contec to buy certified components from niche suppliers that typically command 20–40% price premiums and minimum order quantities often of 100–1,000 units; substitution triggers revalidation programs that can cost $50k–$250k and extend qualification cycles, while approved-vendor lists lock designs and increase supplier dependence.

Contract manufacturing and EMS dependence

For boards and system integration, EMS partners control capacity, yields and costs, giving them leverage especially when regional supply constraints and tight labor markets limit alternatives. Transitioning EMS is costly due to tooling, NPI learning curves and extended quality ramp-up, raising switching barriers. Companies commonly use long-term agreements and volume commitments to lock capacity and mitigate supplier bargaining power.

Software stacks and OS licensing

Software stacks and OS licensing (real-time OS, Windows IoT, Linux distros, middleware) materially affect Contec’s BOM and lifecycle support; license terms, patch cadence and LTS fees give software suppliers leverage, and kernel/driver compatibility can tie hardware refresh cycles to vendor roadmaps. Contec can lower exposure with open-source adoption and in-house expertise, though paid support SLAs remain critical.

- Real-time OS vs Windows IoT vs Linux

- License, patch cadence, LTS fees

- Kernel/driver lock-in ties refresh

- Mitigation: open-source + in-house + SLAs

Interconnects, sensors, and module ecosystems

Rugged connectors, DAQ modules, and wireless modems are sourced from specialized vendors, giving suppliers measurable leverage as form-factor standards like PCIe, PXI, and COM Express constrain substitutions; in 2024 supply lead times often exceeded 12 weeks for niche modules, tightening negotiation power. Performance and durability specs further narrow the supplier pool, while strategic alliances and buffer inventory are used to stabilize supply risk.

- Specialized vendors: limited substitutes

- Form-factor lock-in: PCIe/PXI/COM Express

- Lead times: >12 weeks in 2024

- Mitigants: alliances + buffer inventory

Supplier concentration risks: memory top-3 75-80%, long lead times

Contec faces high supplier power: memory top-3 hold ~75–80% share and FPGA/CPU ecosystems concentrate sourcing, creating pricing/allocation leverage and 20–40+ week lead times. Certified industrial components carry 20–40% price premiums and revalidation can cost $50k–$250k, raising switching barriers. EMS, niche modules and software licenses add capacity, certification and lifecycle lock-in, mitigated via multi-sourcing, inventory and long-term agreements.

| Metric | 2024 Value |

|---|---|

| Memory market share (top3) | 75–80% |

| Component lead times | 20–40+ weeks |

| Price premium (certified) | 20–40% |

| Revalidation cost | $50k–$250k |

| Niche module lead times | >12 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Contec that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive trends and strategic levers to protect or grow market share.

A compact one-sheet Porter's Five Forces for Contec—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart; clean layout fits decks or dashboards with no macros required.

Customers Bargaining Power

Large OEMs and system integrators

Contec’s core customers—large OEMs and system integrators—buy in multi-million-dollar volumes and exert strong negotiation clout, pushing for customizations, lifecycle guarantees and service credits. Competitive bidding among IPC vendors amplifies buyer leverage and compresses margins. Framework agreements and dual-sourcing are standard procurement strategies, forcing suppliers to offer tighter terms and rapid support.

High switching costs with qualification

Industrial and medical deployments often require 6–18 months of validation before design-in, locking buyers post-award and raising real switching costs; however, pre-design buyers typically extract 5–20% price concessions by leveraging alternative vendors. Decisions lean on total cost of ownership rather than unit price, and long product lifecycles (7–15 years) both amortize switching friction and intensify pre-award bargaining pressure.

Price sensitivity in commoditized segments

Standard embedded PCs, SBCs and IoT gateways face high price transparency, with industry buyer surveys in 2024 citing typical price differentials of 15–25% between branded players (Advantech, Kontron) and white-label ODMs.

Buyers benchmark rigorously against Advantech and Kontron; volume discounts and value-add bundling now determine procurement decisions in >50% of enterprise RFPs.

Differentiation through ruggedness certifications and premium service contracts is required to defend 8–12% higher margins versus ODM commodity levels.

Demand for uptime and SLAs

Factory automation and transportation customers demand high reliability and rapid RMA turnaround (typical SLAs target 99.9% uptime and 24–72 hour RMAs in 2024), giving them leverage to negotiate strict penalties. They push stringent SLAs that raise switching costs; vendors offering predictive maintenance and remote support — shown in 2024 studies to cut unplanned downtime ~30% — can justify 10–15% premium pricing. Service quality heavily influences rebids and renewals, with SLA breaches reducing renewal rates materially.

- 99.9% uptime targets (2024)

- 24–72h RMA expectations

- ~30% downtime reduction via predictive maintenance (2024)

- 10–15% premium for integrated service offerings

Interoperability and open standards

Buyers now insist on native support for OPC UA, MQTT, EtherCAT and major cloud platforms; 2024 surveys show over 60% of industrial buyers rate open standards as critical to purchase decisions. Open standards materially lower vendor lock-in and increase switching; Contec must sustain broad driver and protocol support to remain shortlisted. Certification programs and reference architectures improve account retention and shorten deployment cycles.

- compatibility: OPC UA, MQTT, EtherCAT, cloud

- market metric: >60% buyers prioritize open standards (2024)

- strategy: broad driver support + certification + reference architectures

OEM leverage squeezes margins; SLAs & open standards unlock 10–15% service premiums

Contec’s large OEM buyers wield strong price and SLA leverage, extracting 5–20% pre-design concessions and driving framework/dual-sourcing that compresses margins. High price transparency yields 15–25% branded vs ODM gaps, while >50% enterprise RFPs prioritize volume discounts and bundling. Open standards matter: >60% of industrial buyers rate them critical. Service SLAs (99.9% uptime, 24–72h RMA) and predictive maintenance (~30% downtime reduction) dictate premiums of 10–15%.

| Metric | 2024 datapoint |

|---|---|

| Pre-design price concessions | 5–20% |

| Branded vs ODM price gap | 15–25% |

| Buyers prioritizing open standards | >60% |

| Enterprise RFPs using volume discounts | >50% |

| Uptime SLA | 99.9% |

| RMA expectation | 24–72h |

| Downtime reduction via PdM | ~30% |

| Service premium achievable | 10–15% |

What You See Is What You Get

Contec Porter's Five Forces Analysis

This preview shows the exact Contec Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the full, final deliverable; instant access to this same file is provided upon payment.