Cooley Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

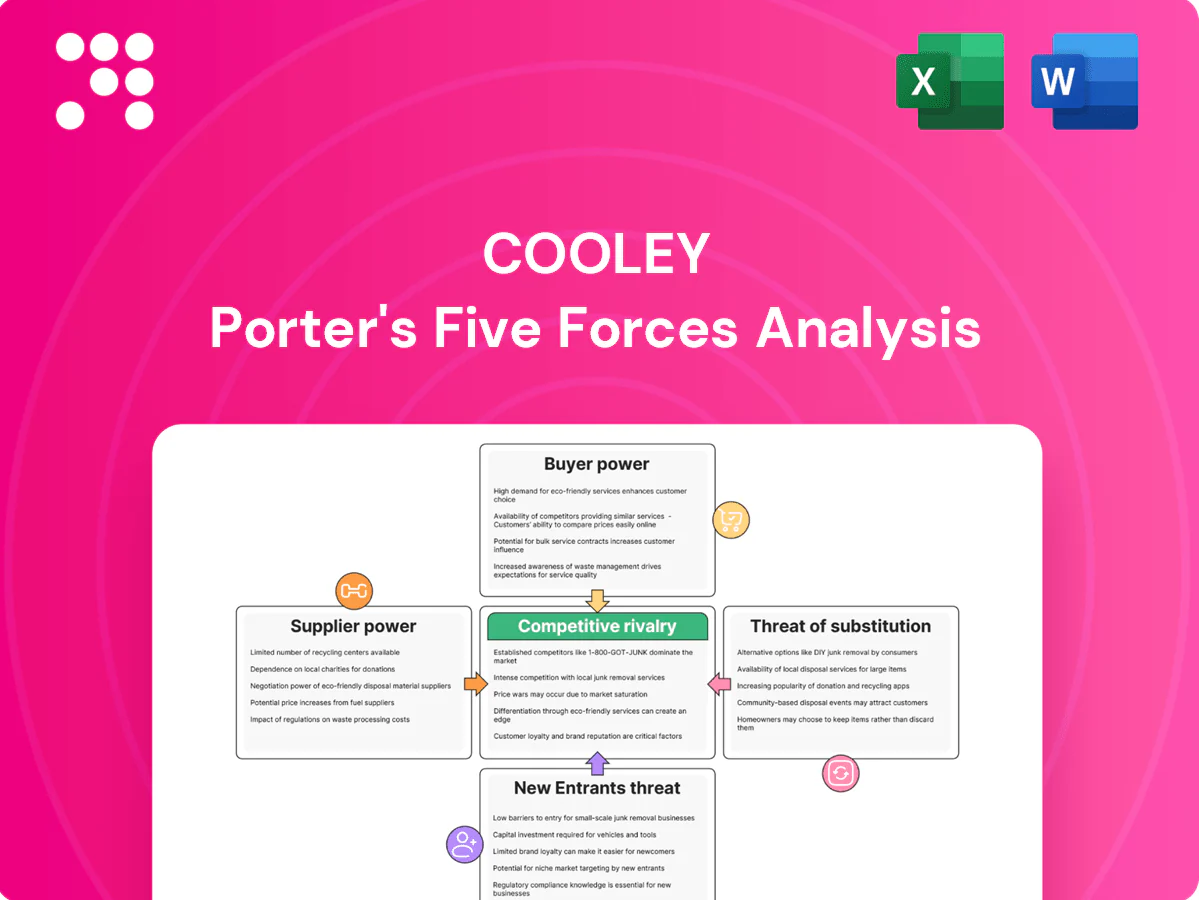

Cooley’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, barriers to entry, and substitute threats shaping its market position. The analysis uncovers where Cooley holds advantages and where pressure could erode margins. Want deeper force-by-force ratings, visuals, and strategic implications? Unlock the full Porter's Five Forces Analysis for a complete, consultant-grade breakdown.

Suppliers Bargaining Power

Elite legal talent scarcity

Top-tier partners and associates in tech and life sciences are scarce, with many Am Law firms maintaining a $215,000 first-year associate scale in 2024, driving wage pressure and higher retention costs for Cooley.

Specialist experts and co-counsel

IP experts, regulatory specialists, and expert witnesses are pivotal in high-stakes Cooley matters, with typical expert rates commonly $300–$1,200/hour and trial-day fees up to $10,000/day, giving them pricing and scheduling leverage. Limited availability for niche tech or cross-border issues amplifies dependence, sometimes forcing 20–40% premium markups for urgent bookings. Preferred-vendor panels and long-term co-counsel relationships often temper rates and improve access.

Legal tech and research platforms

Dependence on e-discovery, AI review, and research databases creates significant switching frictions, with top e-discovery/knowledge platforms capturing roughly 60% of enterprise spend in 2024. A few scaled vendors concentrate bargaining power, offering volume discounts commonly up to 25% while mission-critical integrations limit optionality. Cooley can dual-source and invest in internal tooling to offset vendor leverage and reduce recurring costs.

Real estate and premium locations

Prestige offices near clients and courts remain supply-constrained, keeping bargaining power with landlords in 2024; top tech and life‑science hubs can command a 10–30% rent and stricter term premium versus secondary markets. Hybrid models have cut occupier footprints roughly 20–30% for many firms but preserve branding value in flagship locations, while flexible workspace and coworking strategies reduce direct landlord exposure.

- Supply constraint: prestige locations

- Landlord leverage: 10–30% premium

- Hybrid impact: −20–30% footprint

- Mitigation: flexible workspace adoption

Referral and deal-flow channels

- Gatekeepers: venture funds, banks, incubators

- 2024 global VC funding ~ $300B

- Impact: origination > pricing

- Mitigation: diversify channels, join syndicates

Talent scarcity heats pay: 1L $215,000; experts $300–1,200/hr; vendors ~60%

Top-tier associates and specialists are scarce; 2024 first‑year pay ~ $215,000, raising wage and retention pressure on Cooley.

IP/regulatory experts bill $300–$1,200/hr, trials up to $10,000/day; niche scarcity can impose 20–40% premium, though panels reduce exposure.

E‑discovery/knowledge vendors take ~60% enterprise spend; landlords command 10–30% premium in flagship hubs; hybrid models cut footprints ~20–30%.

| Metric | 2024 |

|---|---|

| 1L scale | $215,000 |

| Expert rates | $300–$1,200/hr |

| Vendor share | ~60% |

| Rent premium | 10–30% |

What is included in the product

Tailored Porter’s Five Forces analysis for Cooley that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, plus strategic implications for pricing, profitability and market positioning.

A concise Cooley Porter's Five Forces summary that maps competitive pressures to decision-ready actions, with editable inputs and a radar chart for instant, boardroom-ready visuals and scenario comparisons.

Customers Bargaining Power

Institutional client concentration

VCs, growth equity and late-stage tech/life-science clients control concentrated fee pools—PitchBook reported global VC dry powder at $233B end-2023, remaining >$200B into 2024—giving them leverage. They run panel reviews and competitive RFPs to compress rates and tighten terms. Consolidation among buyers amplifies negotiating clout, yet Cooley’s deep sector expertise and strong outcomes support premium fee tiers despite pressure.

Alternative fee arrangements

Clients increasingly demand capped, fixed, or success-based fees—by 2024 about 48% of in-house legal teams reported regular use of alternative fee arrangements, shifting risk to firms and compressing margins on predictable work. Data-driven scoping and matter analytics help defend profitability by reducing overruns and pricing error. Cooley can blend AFAs with premium hourly rates for complex, uncertain matters to preserve margin.

Switching costs and relationship lock-in

Knowledge of a client’s cap table, IP and regulatory history creates moderate switching costs by embedding firm-specific intelligence; institutional procurement and standardized onboarding, however, often ease transitions across advisors. Trusted partner relationships and conflict-free coverage reduce churn; Bain reports a 5% increase in retention can raise profits 25–95%. Proactive client service and embedded teams further strengthen stickiness.

Price transparency and benchmarking

By 2024 clients increasingly benchmark market rates for venture financings, IPOs, and litigation phases, comparing peer firms on like-for-like matters. Transparency drives stronger discount demands for commoditizing tasks while differentiation shifts to speed, risk mitigation, and demonstrable deal outcomes. Firms losing measurable advantages face margin compression.

- Benchmarking: market-rate comparisons across peers

- Pressure: higher discount requests on commoditized work

- Edge: speed, risk mitigation, and outcomes

Conflicts and limited choice

High ecosystem overlap restricts client options as conflicts between incumbent partners and new bidders limit feasible firms. In hot 2024 sectors conflict screens have reduced buyer leverage, yet time-sensitive deals let clients negotiate harder. Effective capacity management and robust conflicts systems preserve win rates and conversion in competitive processes.

- Conflicts limit choices; time pressure can restore buyer leverage; strong conflicts controls protect win rates

Fee pressure from $233B VC dry powder and 48% AFA use squeezes margins

Clients hold concentrated fee power—VC dry powder was $233B end-2023, staying >$200B into 2024—enabling aggressive RFPs and rate pressure. About 48% of in-house teams used alternative fee arrangements in 2024, shifting risk to firms and compressing margins. Cooley’s sector expertise and client-embedded knowledge create moderate switching costs that protect premium fees.

| Metric | Stat | Impact |

|---|---|---|

| VC dry powder | $233B (end‑2023) | Buyer leverage |

| AFA adoption | 48% (2024) | Margin pressure |

| Retention effect | 5% ↑ retention → 25–95% profit | Value of stickiness |

Preview the Actual Deliverable

Cooley Porter's Five Forces Analysis

This preview shows the exact Cooley Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use upon payment. You’re viewing the final deliverable with actionable insights on industry rivalry, buyer and supplier power, threats of entry and substitutes.

A Must-Have Tool for Decision-Makers

Cooley’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, barriers to entry, and substitute threats shaping its market position. The analysis uncovers where Cooley holds advantages and where pressure could erode margins. Want deeper force-by-force ratings, visuals, and strategic implications? Unlock the full Porter's Five Forces Analysis for a complete, consultant-grade breakdown.

Suppliers Bargaining Power

Elite legal talent scarcity

Top-tier partners and associates in tech and life sciences are scarce, with many Am Law firms maintaining a $215,000 first-year associate scale in 2024, driving wage pressure and higher retention costs for Cooley.

Specialist experts and co-counsel

IP experts, regulatory specialists, and expert witnesses are pivotal in high-stakes Cooley matters, with typical expert rates commonly $300–$1,200/hour and trial-day fees up to $10,000/day, giving them pricing and scheduling leverage. Limited availability for niche tech or cross-border issues amplifies dependence, sometimes forcing 20–40% premium markups for urgent bookings. Preferred-vendor panels and long-term co-counsel relationships often temper rates and improve access.

Legal tech and research platforms

Dependence on e-discovery, AI review, and research databases creates significant switching frictions, with top e-discovery/knowledge platforms capturing roughly 60% of enterprise spend in 2024. A few scaled vendors concentrate bargaining power, offering volume discounts commonly up to 25% while mission-critical integrations limit optionality. Cooley can dual-source and invest in internal tooling to offset vendor leverage and reduce recurring costs.

Real estate and premium locations

Prestige offices near clients and courts remain supply-constrained, keeping bargaining power with landlords in 2024; top tech and life‑science hubs can command a 10–30% rent and stricter term premium versus secondary markets. Hybrid models have cut occupier footprints roughly 20–30% for many firms but preserve branding value in flagship locations, while flexible workspace and coworking strategies reduce direct landlord exposure.

- Supply constraint: prestige locations

- Landlord leverage: 10–30% premium

- Hybrid impact: −20–30% footprint

- Mitigation: flexible workspace adoption

Referral and deal-flow channels

- Gatekeepers: venture funds, banks, incubators

- 2024 global VC funding ~ $300B

- Impact: origination > pricing

- Mitigation: diversify channels, join syndicates

Talent scarcity heats pay: 1L $215,000; experts $300–1,200/hr; vendors ~60%

Top-tier associates and specialists are scarce; 2024 first‑year pay ~ $215,000, raising wage and retention pressure on Cooley.

IP/regulatory experts bill $300–$1,200/hr, trials up to $10,000/day; niche scarcity can impose 20–40% premium, though panels reduce exposure.

E‑discovery/knowledge vendors take ~60% enterprise spend; landlords command 10–30% premium in flagship hubs; hybrid models cut footprints ~20–30%.

| Metric | 2024 |

|---|---|

| 1L scale | $215,000 |

| Expert rates | $300–$1,200/hr |

| Vendor share | ~60% |

| Rent premium | 10–30% |

What is included in the product

Tailored Porter’s Five Forces analysis for Cooley that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, plus strategic implications for pricing, profitability and market positioning.

A concise Cooley Porter's Five Forces summary that maps competitive pressures to decision-ready actions, with editable inputs and a radar chart for instant, boardroom-ready visuals and scenario comparisons.

Customers Bargaining Power

Institutional client concentration

VCs, growth equity and late-stage tech/life-science clients control concentrated fee pools—PitchBook reported global VC dry powder at $233B end-2023, remaining >$200B into 2024—giving them leverage. They run panel reviews and competitive RFPs to compress rates and tighten terms. Consolidation among buyers amplifies negotiating clout, yet Cooley’s deep sector expertise and strong outcomes support premium fee tiers despite pressure.

Alternative fee arrangements

Clients increasingly demand capped, fixed, or success-based fees—by 2024 about 48% of in-house legal teams reported regular use of alternative fee arrangements, shifting risk to firms and compressing margins on predictable work. Data-driven scoping and matter analytics help defend profitability by reducing overruns and pricing error. Cooley can blend AFAs with premium hourly rates for complex, uncertain matters to preserve margin.

Switching costs and relationship lock-in

Knowledge of a client’s cap table, IP and regulatory history creates moderate switching costs by embedding firm-specific intelligence; institutional procurement and standardized onboarding, however, often ease transitions across advisors. Trusted partner relationships and conflict-free coverage reduce churn; Bain reports a 5% increase in retention can raise profits 25–95%. Proactive client service and embedded teams further strengthen stickiness.

Price transparency and benchmarking

By 2024 clients increasingly benchmark market rates for venture financings, IPOs, and litigation phases, comparing peer firms on like-for-like matters. Transparency drives stronger discount demands for commoditizing tasks while differentiation shifts to speed, risk mitigation, and demonstrable deal outcomes. Firms losing measurable advantages face margin compression.

- Benchmarking: market-rate comparisons across peers

- Pressure: higher discount requests on commoditized work

- Edge: speed, risk mitigation, and outcomes

Conflicts and limited choice

High ecosystem overlap restricts client options as conflicts between incumbent partners and new bidders limit feasible firms. In hot 2024 sectors conflict screens have reduced buyer leverage, yet time-sensitive deals let clients negotiate harder. Effective capacity management and robust conflicts systems preserve win rates and conversion in competitive processes.

- Conflicts limit choices; time pressure can restore buyer leverage; strong conflicts controls protect win rates

Fee pressure from $233B VC dry powder and 48% AFA use squeezes margins

Clients hold concentrated fee power—VC dry powder was $233B end-2023, staying >$200B into 2024—enabling aggressive RFPs and rate pressure. About 48% of in-house teams used alternative fee arrangements in 2024, shifting risk to firms and compressing margins. Cooley’s sector expertise and client-embedded knowledge create moderate switching costs that protect premium fees.

| Metric | Stat | Impact |

|---|---|---|

| VC dry powder | $233B (end‑2023) | Buyer leverage |

| AFA adoption | 48% (2024) | Margin pressure |

| Retention effect | 5% ↑ retention → 25–95% profit | Value of stickiness |

Preview the Actual Deliverable

Cooley Porter's Five Forces Analysis

This preview shows the exact Cooley Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use upon payment. You’re viewing the final deliverable with actionable insights on industry rivalry, buyer and supplier power, threats of entry and substitutes.

Description

A Must-Have Tool for Decision-Makers

Cooley’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, barriers to entry, and substitute threats shaping its market position. The analysis uncovers where Cooley holds advantages and where pressure could erode margins. Want deeper force-by-force ratings, visuals, and strategic implications? Unlock the full Porter's Five Forces Analysis for a complete, consultant-grade breakdown.

Suppliers Bargaining Power

Elite legal talent scarcity

Top-tier partners and associates in tech and life sciences are scarce, with many Am Law firms maintaining a $215,000 first-year associate scale in 2024, driving wage pressure and higher retention costs for Cooley.

Specialist experts and co-counsel

IP experts, regulatory specialists, and expert witnesses are pivotal in high-stakes Cooley matters, with typical expert rates commonly $300–$1,200/hour and trial-day fees up to $10,000/day, giving them pricing and scheduling leverage. Limited availability for niche tech or cross-border issues amplifies dependence, sometimes forcing 20–40% premium markups for urgent bookings. Preferred-vendor panels and long-term co-counsel relationships often temper rates and improve access.

Legal tech and research platforms

Dependence on e-discovery, AI review, and research databases creates significant switching frictions, with top e-discovery/knowledge platforms capturing roughly 60% of enterprise spend in 2024. A few scaled vendors concentrate bargaining power, offering volume discounts commonly up to 25% while mission-critical integrations limit optionality. Cooley can dual-source and invest in internal tooling to offset vendor leverage and reduce recurring costs.

Real estate and premium locations

Prestige offices near clients and courts remain supply-constrained, keeping bargaining power with landlords in 2024; top tech and life‑science hubs can command a 10–30% rent and stricter term premium versus secondary markets. Hybrid models have cut occupier footprints roughly 20–30% for many firms but preserve branding value in flagship locations, while flexible workspace and coworking strategies reduce direct landlord exposure.

- Supply constraint: prestige locations

- Landlord leverage: 10–30% premium

- Hybrid impact: −20–30% footprint

- Mitigation: flexible workspace adoption

Referral and deal-flow channels

- Gatekeepers: venture funds, banks, incubators

- 2024 global VC funding ~ $300B

- Impact: origination > pricing

- Mitigation: diversify channels, join syndicates

Talent scarcity heats pay: 1L $215,000; experts $300–1,200/hr; vendors ~60%

Top-tier associates and specialists are scarce; 2024 first‑year pay ~ $215,000, raising wage and retention pressure on Cooley.

IP/regulatory experts bill $300–$1,200/hr, trials up to $10,000/day; niche scarcity can impose 20–40% premium, though panels reduce exposure.

E‑discovery/knowledge vendors take ~60% enterprise spend; landlords command 10–30% premium in flagship hubs; hybrid models cut footprints ~20–30%.

| Metric | 2024 |

|---|---|

| 1L scale | $215,000 |

| Expert rates | $300–$1,200/hr |

| Vendor share | ~60% |

| Rent premium | 10–30% |

What is included in the product

Tailored Porter’s Five Forces analysis for Cooley that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, plus strategic implications for pricing, profitability and market positioning.

A concise Cooley Porter's Five Forces summary that maps competitive pressures to decision-ready actions, with editable inputs and a radar chart for instant, boardroom-ready visuals and scenario comparisons.

Customers Bargaining Power

Institutional client concentration

VCs, growth equity and late-stage tech/life-science clients control concentrated fee pools—PitchBook reported global VC dry powder at $233B end-2023, remaining >$200B into 2024—giving them leverage. They run panel reviews and competitive RFPs to compress rates and tighten terms. Consolidation among buyers amplifies negotiating clout, yet Cooley’s deep sector expertise and strong outcomes support premium fee tiers despite pressure.

Alternative fee arrangements

Clients increasingly demand capped, fixed, or success-based fees—by 2024 about 48% of in-house legal teams reported regular use of alternative fee arrangements, shifting risk to firms and compressing margins on predictable work. Data-driven scoping and matter analytics help defend profitability by reducing overruns and pricing error. Cooley can blend AFAs with premium hourly rates for complex, uncertain matters to preserve margin.

Switching costs and relationship lock-in

Knowledge of a client’s cap table, IP and regulatory history creates moderate switching costs by embedding firm-specific intelligence; institutional procurement and standardized onboarding, however, often ease transitions across advisors. Trusted partner relationships and conflict-free coverage reduce churn; Bain reports a 5% increase in retention can raise profits 25–95%. Proactive client service and embedded teams further strengthen stickiness.

Price transparency and benchmarking

By 2024 clients increasingly benchmark market rates for venture financings, IPOs, and litigation phases, comparing peer firms on like-for-like matters. Transparency drives stronger discount demands for commoditizing tasks while differentiation shifts to speed, risk mitigation, and demonstrable deal outcomes. Firms losing measurable advantages face margin compression.

- Benchmarking: market-rate comparisons across peers

- Pressure: higher discount requests on commoditized work

- Edge: speed, risk mitigation, and outcomes

Conflicts and limited choice

High ecosystem overlap restricts client options as conflicts between incumbent partners and new bidders limit feasible firms. In hot 2024 sectors conflict screens have reduced buyer leverage, yet time-sensitive deals let clients negotiate harder. Effective capacity management and robust conflicts systems preserve win rates and conversion in competitive processes.

- Conflicts limit choices; time pressure can restore buyer leverage; strong conflicts controls protect win rates

Fee pressure from $233B VC dry powder and 48% AFA use squeezes margins

Clients hold concentrated fee power—VC dry powder was $233B end-2023, staying >$200B into 2024—enabling aggressive RFPs and rate pressure. About 48% of in-house teams used alternative fee arrangements in 2024, shifting risk to firms and compressing margins. Cooley’s sector expertise and client-embedded knowledge create moderate switching costs that protect premium fees.

| Metric | Stat | Impact |

|---|---|---|

| VC dry powder | $233B (end‑2023) | Buyer leverage |

| AFA adoption | 48% (2024) | Margin pressure |

| Retention effect | 5% ↑ retention → 25–95% profit | Value of stickiness |

Preview the Actual Deliverable

Cooley Porter's Five Forces Analysis

This preview shows the exact Cooley Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use upon payment. You’re viewing the final deliverable with actionable insights on industry rivalry, buyer and supplier power, threats of entry and substitutes.