Cooley PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological change are reshaping Cooley’s strategy with our focused PESTLE Analysis. This concise briefing highlights key external risks and opportunities to inform investment and planning decisions. Purchase the full report for a complete, actionable breakdown ready for immediate use.

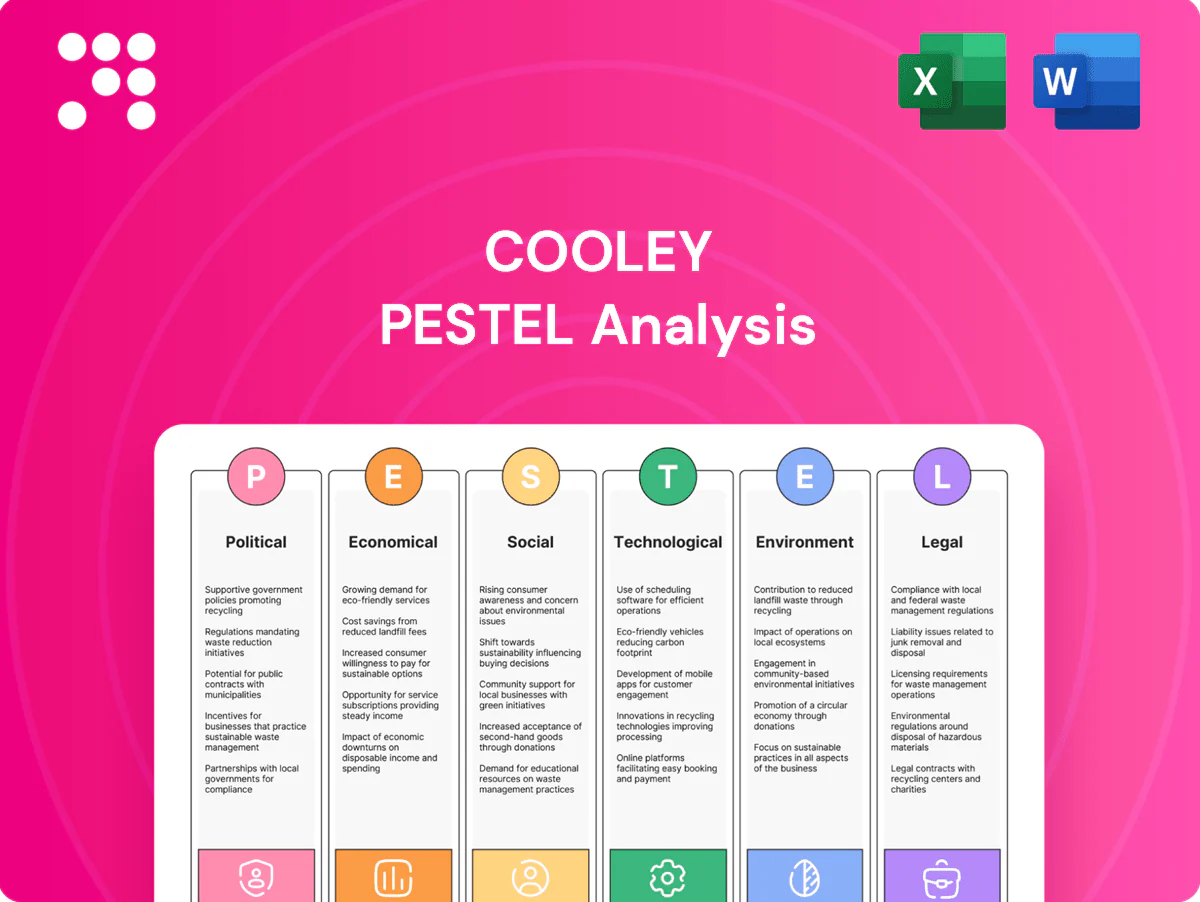

Political factors

Shifting enforcement priorities

Administration shifts redirect DOJ/FTC/SEC focus, reshaping antitrust, securities and white-collar risk for clients and forcing Cooley to recalibrate deal terms, disclosures and litigation posture rapidly. Policy swings can widen or narrow growth equity and IPO windows—US IPO activity rose to ~160 deals in 2024, highlighting timing sensitivity. Proactive regulatory engagement and monitoring SEC/FTC guidance (agencies totaling ~4,700 staff in 2024) mitigates surprise scrutiny.

Geopolitics and FDI reviews

Since FIRRMA (2018) and expanding allied regimes, CFIUS-style reviews have increasingly complicated cross-border exits and investments, with UNCTAD reporting global FDI fell about 12% to roughly $1.06 trillion in 2023. Tech and life‑sciences assets now face deeper national‑security scrutiny, extending deal timelines and conditionality. Cooley adds value via early risk mapping and mitigation structures; deal certainty often hinges on filing strategy and remedy design.

Sanctions and export controls

Expanding sanctions and dual-use export controls since 2022 increasingly target semiconductors, AI chips and biotools, with the global semiconductor market at roughly $602B in 2023 (WSTS). Clients now require real-time screening, licensing and supply‑chain rerouting to avoid disruptions. Regulatory missteps trigger enforcement, reputational damage and valuation hits. Cooley’s compliance frameworks are critical in diligence and ongoing operations.

Public funding and health policy

Public funding steers capital: NIH's $49.6B FY2024 budget and BARDA's roughly $1.7B annual appropriation direct grants and de-risk pipelines, while IRA-driven Medicare negotiation (CBO ~98B savings over 10 years) and pricing reforms reshape investor returns and deal math, with reimbursement changes able to re-rate biotech pipelines overnight. Advisory must align clinical, regulatory, and commercialization paths to evolving policy.

- NIH $49.6B FY2024

- BARDA ~ $1.7B

- IRA Medicare negotiation CBO ~ $98B(10y)

- Reimbursement shifts alter M&A and market access

Digital sovereignty agendas

Cooley advises on architecture, contracting, and compliance to preserve scalability and avoid expensive remediation; early structuring cuts delay and costs versus late fixes tied to regulatory blockers.

- Data: >60 jurisdictions with localization rules (2024)

- Cloud: global public cloud market >$500B (2024)

- Risk: early design lowers remediation spend and time

DOJ/FTC/SEC 4,700 staff boost scrutiny; FDI -12%, data localization up

Administration shifts reshape antitrust/securities focus (DOJ/FTC/SEC ~4,700 staff in 2024), altering deal terms and litigation posture; CFIUS/FIRRMA complexity cuts cross‑border certainty (global FDI ~$1.06T, -12% in 2023). Sanctions/export controls hit semiconductors (~$602B market 2023) and AI; public funding (NIH $49.6B FY2024; BARDA ~$1.7B) and IRA pricing changes (~$98B 10y CBO) reprice biotech risk. Data localization (>60 jurisdictions 2024) forces architecture and M&A fixes.

| Metric | Value | Impact |

|---|---|---|

| DOJ/FTC/SEC staff | ~4,700 (2024) | Higher scrutiny |

| Global FDI | $1.06T (-12% 2023) | Deal delays |

| Semiconductors | $602B (2023) | Export risk |

| NIH/BARDA | $49.6B / ~$1.7B | R&D funding |

| Data localization | >60 jurisdictions (2024) | Compliance costs |

What is included in the product

Explores how macro-environmental factors uniquely affect Cooley across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

Cooley PESTLE Analysis condenses complex external-factor research into a visually segmented, easily shareable summary for quick interpretation in meetings and presentations, while allowing editable notes for region- or business-specific context.

Economic factors

Capital market cyclicality

Capital market cyclicality drives Cooley’s work mix as IPO, SPAC and follow-on windows open and close with shifting risk appetite; 2024 saw muted SPAC issuance after the 2020–21 peak and global IPO proceeds remained well below pandemic highs. M&A volumes and valuations track interest rates and equity multiples—global M&A value was roughly $2.5 trillion in 2024, compressing deal counts and multiples. Cooley pivots between public offerings, private rounds and restructuring, using flexible staffing and pricing to preserve margins across cycles.

Interest rates and VC liquidity

With fed funds near 5.25–5.50% in 2025, higher rates compress venture deployment, elongate runways and raise down-round risk as VC deal volume remains >30% below 2021 peaks; clients increasingly seek extensions, secondaries and structured equity, making Cooley’s financing creativity and investor networks differentiators while unit-economics diligence tightens in term sheets.

Cost pressure and AFAs

Clients increasingly push for alternative fee arrangements and efficiency, driving matter budgeting, nearshoring, and tech-enabled delivery to protect profitability. Transparent scoping builds trust amid market uncertainty, while outcome-based fees align incentives in litigation and regulatory matters. These shifts force law firms to standardize pricing and invest in process and technology to sustain margins.

Currency and cross-border exposure

FX swings materially affect multinational deal pricing, earnouts, and revenue recognition—movements of 3–8% commonly shift transaction economics and post-close earnouts; hedging provisions and currency-adjusted consideration are key negotiation levers. Cooley standardizes protections in SPA and financing docs, using collars, escrow structures, and cash/FX netting to limit exposure. Predictability from these clauses improves closing certainty and reduces post-closing disputes.

- FX impact: 3–8% deal value variance

- Levers: hedges, collars, currency-adjusted consideration

- Docs: standardized SPA/financing clauses

- Outcome: higher closing certainty, fewer disputes

Competitive legal market

Am Law consolidation and specialist boutiques intensify competition for Cooley as clients favor firms with deep sector practices, partner mobility, and global reach when awarding mandates.

Differentiated IP, regulatory, and life sciences benches capture premium work and higher rates, while thought leadership and published deal/tx expertise sustain brand visibility and pipeline.

- Competitive pressure: sector depth

- Client drivers: partner mobility, global footprint

- Win factors: IP, regulatory, life sciences

- Pipeline: thought leadership

DOJ/FTC/SEC 4,700 staff boost scrutiny; FDI -12%, data localization up

Capital-market cyclicality and Fed funds near 5.25–5.50% in 2025 compress IPO/SPAC windows and valuations, driving Cooley toward financings, restructurings and fee innovation; global M&A was roughly $2.5T in 2024. Venture deal volume remains >30% below 2021 peaks, boosting extensions, secondaries and structured equity demand. FX moves of 3–8% materially shift deal economics, so standardized hedges and collars raise closing certainty.

| Metric | 2024–25 |

|---|---|

| Global M&A | $2.5T (2024) |

| Fed funds | 5.25–5.50% (2025) |

| VC volume vs 2021 | >30% below |

| FX deal variance | 3–8% |

Same Document Delivered

Cooley PESTLE Analysis

The preview shown here is the exact Cooley PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This professional, final file contains the same content, layout, and structure visible now. No placeholders, no surprises; download immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological change are reshaping Cooley’s strategy with our focused PESTLE Analysis. This concise briefing highlights key external risks and opportunities to inform investment and planning decisions. Purchase the full report for a complete, actionable breakdown ready for immediate use.

Political factors

Shifting enforcement priorities

Administration shifts redirect DOJ/FTC/SEC focus, reshaping antitrust, securities and white-collar risk for clients and forcing Cooley to recalibrate deal terms, disclosures and litigation posture rapidly. Policy swings can widen or narrow growth equity and IPO windows—US IPO activity rose to ~160 deals in 2024, highlighting timing sensitivity. Proactive regulatory engagement and monitoring SEC/FTC guidance (agencies totaling ~4,700 staff in 2024) mitigates surprise scrutiny.

Geopolitics and FDI reviews

Since FIRRMA (2018) and expanding allied regimes, CFIUS-style reviews have increasingly complicated cross-border exits and investments, with UNCTAD reporting global FDI fell about 12% to roughly $1.06 trillion in 2023. Tech and life‑sciences assets now face deeper national‑security scrutiny, extending deal timelines and conditionality. Cooley adds value via early risk mapping and mitigation structures; deal certainty often hinges on filing strategy and remedy design.

Sanctions and export controls

Expanding sanctions and dual-use export controls since 2022 increasingly target semiconductors, AI chips and biotools, with the global semiconductor market at roughly $602B in 2023 (WSTS). Clients now require real-time screening, licensing and supply‑chain rerouting to avoid disruptions. Regulatory missteps trigger enforcement, reputational damage and valuation hits. Cooley’s compliance frameworks are critical in diligence and ongoing operations.

Public funding and health policy

Public funding steers capital: NIH's $49.6B FY2024 budget and BARDA's roughly $1.7B annual appropriation direct grants and de-risk pipelines, while IRA-driven Medicare negotiation (CBO ~98B savings over 10 years) and pricing reforms reshape investor returns and deal math, with reimbursement changes able to re-rate biotech pipelines overnight. Advisory must align clinical, regulatory, and commercialization paths to evolving policy.

- NIH $49.6B FY2024

- BARDA ~ $1.7B

- IRA Medicare negotiation CBO ~ $98B(10y)

- Reimbursement shifts alter M&A and market access

Digital sovereignty agendas

Cooley advises on architecture, contracting, and compliance to preserve scalability and avoid expensive remediation; early structuring cuts delay and costs versus late fixes tied to regulatory blockers.

- Data: >60 jurisdictions with localization rules (2024)

- Cloud: global public cloud market >$500B (2024)

- Risk: early design lowers remediation spend and time

DOJ/FTC/SEC 4,700 staff boost scrutiny; FDI -12%, data localization up

Administration shifts reshape antitrust/securities focus (DOJ/FTC/SEC ~4,700 staff in 2024), altering deal terms and litigation posture; CFIUS/FIRRMA complexity cuts cross‑border certainty (global FDI ~$1.06T, -12% in 2023). Sanctions/export controls hit semiconductors (~$602B market 2023) and AI; public funding (NIH $49.6B FY2024; BARDA ~$1.7B) and IRA pricing changes (~$98B 10y CBO) reprice biotech risk. Data localization (>60 jurisdictions 2024) forces architecture and M&A fixes.

| Metric | Value | Impact |

|---|---|---|

| DOJ/FTC/SEC staff | ~4,700 (2024) | Higher scrutiny |

| Global FDI | $1.06T (-12% 2023) | Deal delays |

| Semiconductors | $602B (2023) | Export risk |

| NIH/BARDA | $49.6B / ~$1.7B | R&D funding |

| Data localization | >60 jurisdictions (2024) | Compliance costs |

What is included in the product

Explores how macro-environmental factors uniquely affect Cooley across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

Cooley PESTLE Analysis condenses complex external-factor research into a visually segmented, easily shareable summary for quick interpretation in meetings and presentations, while allowing editable notes for region- or business-specific context.

Economic factors

Capital market cyclicality

Capital market cyclicality drives Cooley’s work mix as IPO, SPAC and follow-on windows open and close with shifting risk appetite; 2024 saw muted SPAC issuance after the 2020–21 peak and global IPO proceeds remained well below pandemic highs. M&A volumes and valuations track interest rates and equity multiples—global M&A value was roughly $2.5 trillion in 2024, compressing deal counts and multiples. Cooley pivots between public offerings, private rounds and restructuring, using flexible staffing and pricing to preserve margins across cycles.

Interest rates and VC liquidity

With fed funds near 5.25–5.50% in 2025, higher rates compress venture deployment, elongate runways and raise down-round risk as VC deal volume remains >30% below 2021 peaks; clients increasingly seek extensions, secondaries and structured equity, making Cooley’s financing creativity and investor networks differentiators while unit-economics diligence tightens in term sheets.

Cost pressure and AFAs

Clients increasingly push for alternative fee arrangements and efficiency, driving matter budgeting, nearshoring, and tech-enabled delivery to protect profitability. Transparent scoping builds trust amid market uncertainty, while outcome-based fees align incentives in litigation and regulatory matters. These shifts force law firms to standardize pricing and invest in process and technology to sustain margins.

Currency and cross-border exposure

FX swings materially affect multinational deal pricing, earnouts, and revenue recognition—movements of 3–8% commonly shift transaction economics and post-close earnouts; hedging provisions and currency-adjusted consideration are key negotiation levers. Cooley standardizes protections in SPA and financing docs, using collars, escrow structures, and cash/FX netting to limit exposure. Predictability from these clauses improves closing certainty and reduces post-closing disputes.

- FX impact: 3–8% deal value variance

- Levers: hedges, collars, currency-adjusted consideration

- Docs: standardized SPA/financing clauses

- Outcome: higher closing certainty, fewer disputes

Competitive legal market

Am Law consolidation and specialist boutiques intensify competition for Cooley as clients favor firms with deep sector practices, partner mobility, and global reach when awarding mandates.

Differentiated IP, regulatory, and life sciences benches capture premium work and higher rates, while thought leadership and published deal/tx expertise sustain brand visibility and pipeline.

- Competitive pressure: sector depth

- Client drivers: partner mobility, global footprint

- Win factors: IP, regulatory, life sciences

- Pipeline: thought leadership

DOJ/FTC/SEC 4,700 staff boost scrutiny; FDI -12%, data localization up

Capital-market cyclicality and Fed funds near 5.25–5.50% in 2025 compress IPO/SPAC windows and valuations, driving Cooley toward financings, restructurings and fee innovation; global M&A was roughly $2.5T in 2024. Venture deal volume remains >30% below 2021 peaks, boosting extensions, secondaries and structured equity demand. FX moves of 3–8% materially shift deal economics, so standardized hedges and collars raise closing certainty.

| Metric | 2024–25 |

|---|---|

| Global M&A | $2.5T (2024) |

| Fed funds | 5.25–5.50% (2025) |

| VC volume vs 2021 | >30% below |

| FX deal variance | 3–8% |

Same Document Delivered

Cooley PESTLE Analysis

The preview shown here is the exact Cooley PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This professional, final file contains the same content, layout, and structure visible now. No placeholders, no surprises; download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological change are reshaping Cooley’s strategy with our focused PESTLE Analysis. This concise briefing highlights key external risks and opportunities to inform investment and planning decisions. Purchase the full report for a complete, actionable breakdown ready for immediate use.

Political factors

Shifting enforcement priorities

Administration shifts redirect DOJ/FTC/SEC focus, reshaping antitrust, securities and white-collar risk for clients and forcing Cooley to recalibrate deal terms, disclosures and litigation posture rapidly. Policy swings can widen or narrow growth equity and IPO windows—US IPO activity rose to ~160 deals in 2024, highlighting timing sensitivity. Proactive regulatory engagement and monitoring SEC/FTC guidance (agencies totaling ~4,700 staff in 2024) mitigates surprise scrutiny.

Geopolitics and FDI reviews

Since FIRRMA (2018) and expanding allied regimes, CFIUS-style reviews have increasingly complicated cross-border exits and investments, with UNCTAD reporting global FDI fell about 12% to roughly $1.06 trillion in 2023. Tech and life‑sciences assets now face deeper national‑security scrutiny, extending deal timelines and conditionality. Cooley adds value via early risk mapping and mitigation structures; deal certainty often hinges on filing strategy and remedy design.

Sanctions and export controls

Expanding sanctions and dual-use export controls since 2022 increasingly target semiconductors, AI chips and biotools, with the global semiconductor market at roughly $602B in 2023 (WSTS). Clients now require real-time screening, licensing and supply‑chain rerouting to avoid disruptions. Regulatory missteps trigger enforcement, reputational damage and valuation hits. Cooley’s compliance frameworks are critical in diligence and ongoing operations.

Public funding and health policy

Public funding steers capital: NIH's $49.6B FY2024 budget and BARDA's roughly $1.7B annual appropriation direct grants and de-risk pipelines, while IRA-driven Medicare negotiation (CBO ~98B savings over 10 years) and pricing reforms reshape investor returns and deal math, with reimbursement changes able to re-rate biotech pipelines overnight. Advisory must align clinical, regulatory, and commercialization paths to evolving policy.

- NIH $49.6B FY2024

- BARDA ~ $1.7B

- IRA Medicare negotiation CBO ~ $98B(10y)

- Reimbursement shifts alter M&A and market access

Digital sovereignty agendas

Cooley advises on architecture, contracting, and compliance to preserve scalability and avoid expensive remediation; early structuring cuts delay and costs versus late fixes tied to regulatory blockers.

- Data: >60 jurisdictions with localization rules (2024)

- Cloud: global public cloud market >$500B (2024)

- Risk: early design lowers remediation spend and time

DOJ/FTC/SEC 4,700 staff boost scrutiny; FDI -12%, data localization up

Administration shifts reshape antitrust/securities focus (DOJ/FTC/SEC ~4,700 staff in 2024), altering deal terms and litigation posture; CFIUS/FIRRMA complexity cuts cross‑border certainty (global FDI ~$1.06T, -12% in 2023). Sanctions/export controls hit semiconductors (~$602B market 2023) and AI; public funding (NIH $49.6B FY2024; BARDA ~$1.7B) and IRA pricing changes (~$98B 10y CBO) reprice biotech risk. Data localization (>60 jurisdictions 2024) forces architecture and M&A fixes.

| Metric | Value | Impact |

|---|---|---|

| DOJ/FTC/SEC staff | ~4,700 (2024) | Higher scrutiny |

| Global FDI | $1.06T (-12% 2023) | Deal delays |

| Semiconductors | $602B (2023) | Export risk |

| NIH/BARDA | $49.6B / ~$1.7B | R&D funding |

| Data localization | >60 jurisdictions (2024) | Compliance costs |

What is included in the product

Explores how macro-environmental factors uniquely affect Cooley across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

Cooley PESTLE Analysis condenses complex external-factor research into a visually segmented, easily shareable summary for quick interpretation in meetings and presentations, while allowing editable notes for region- or business-specific context.

Economic factors

Capital market cyclicality

Capital market cyclicality drives Cooley’s work mix as IPO, SPAC and follow-on windows open and close with shifting risk appetite; 2024 saw muted SPAC issuance after the 2020–21 peak and global IPO proceeds remained well below pandemic highs. M&A volumes and valuations track interest rates and equity multiples—global M&A value was roughly $2.5 trillion in 2024, compressing deal counts and multiples. Cooley pivots between public offerings, private rounds and restructuring, using flexible staffing and pricing to preserve margins across cycles.

Interest rates and VC liquidity

With fed funds near 5.25–5.50% in 2025, higher rates compress venture deployment, elongate runways and raise down-round risk as VC deal volume remains >30% below 2021 peaks; clients increasingly seek extensions, secondaries and structured equity, making Cooley’s financing creativity and investor networks differentiators while unit-economics diligence tightens in term sheets.

Cost pressure and AFAs

Clients increasingly push for alternative fee arrangements and efficiency, driving matter budgeting, nearshoring, and tech-enabled delivery to protect profitability. Transparent scoping builds trust amid market uncertainty, while outcome-based fees align incentives in litigation and regulatory matters. These shifts force law firms to standardize pricing and invest in process and technology to sustain margins.

Currency and cross-border exposure

FX swings materially affect multinational deal pricing, earnouts, and revenue recognition—movements of 3–8% commonly shift transaction economics and post-close earnouts; hedging provisions and currency-adjusted consideration are key negotiation levers. Cooley standardizes protections in SPA and financing docs, using collars, escrow structures, and cash/FX netting to limit exposure. Predictability from these clauses improves closing certainty and reduces post-closing disputes.

- FX impact: 3–8% deal value variance

- Levers: hedges, collars, currency-adjusted consideration

- Docs: standardized SPA/financing clauses

- Outcome: higher closing certainty, fewer disputes

Competitive legal market

Am Law consolidation and specialist boutiques intensify competition for Cooley as clients favor firms with deep sector practices, partner mobility, and global reach when awarding mandates.

Differentiated IP, regulatory, and life sciences benches capture premium work and higher rates, while thought leadership and published deal/tx expertise sustain brand visibility and pipeline.

- Competitive pressure: sector depth

- Client drivers: partner mobility, global footprint

- Win factors: IP, regulatory, life sciences

- Pipeline: thought leadership

DOJ/FTC/SEC 4,700 staff boost scrutiny; FDI -12%, data localization up

Capital-market cyclicality and Fed funds near 5.25–5.50% in 2025 compress IPO/SPAC windows and valuations, driving Cooley toward financings, restructurings and fee innovation; global M&A was roughly $2.5T in 2024. Venture deal volume remains >30% below 2021 peaks, boosting extensions, secondaries and structured equity demand. FX moves of 3–8% materially shift deal economics, so standardized hedges and collars raise closing certainty.

| Metric | 2024–25 |

|---|---|

| Global M&A | $2.5T (2024) |

| Fed funds | 5.25–5.50% (2025) |

| VC volume vs 2021 | >30% below |

| FX deal variance | 3–8% |

Same Document Delivered

Cooley PESTLE Analysis

The preview shown here is the exact Cooley PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This professional, final file contains the same content, layout, and structure visible now. No placeholders, no surprises; download immediately after checkout.