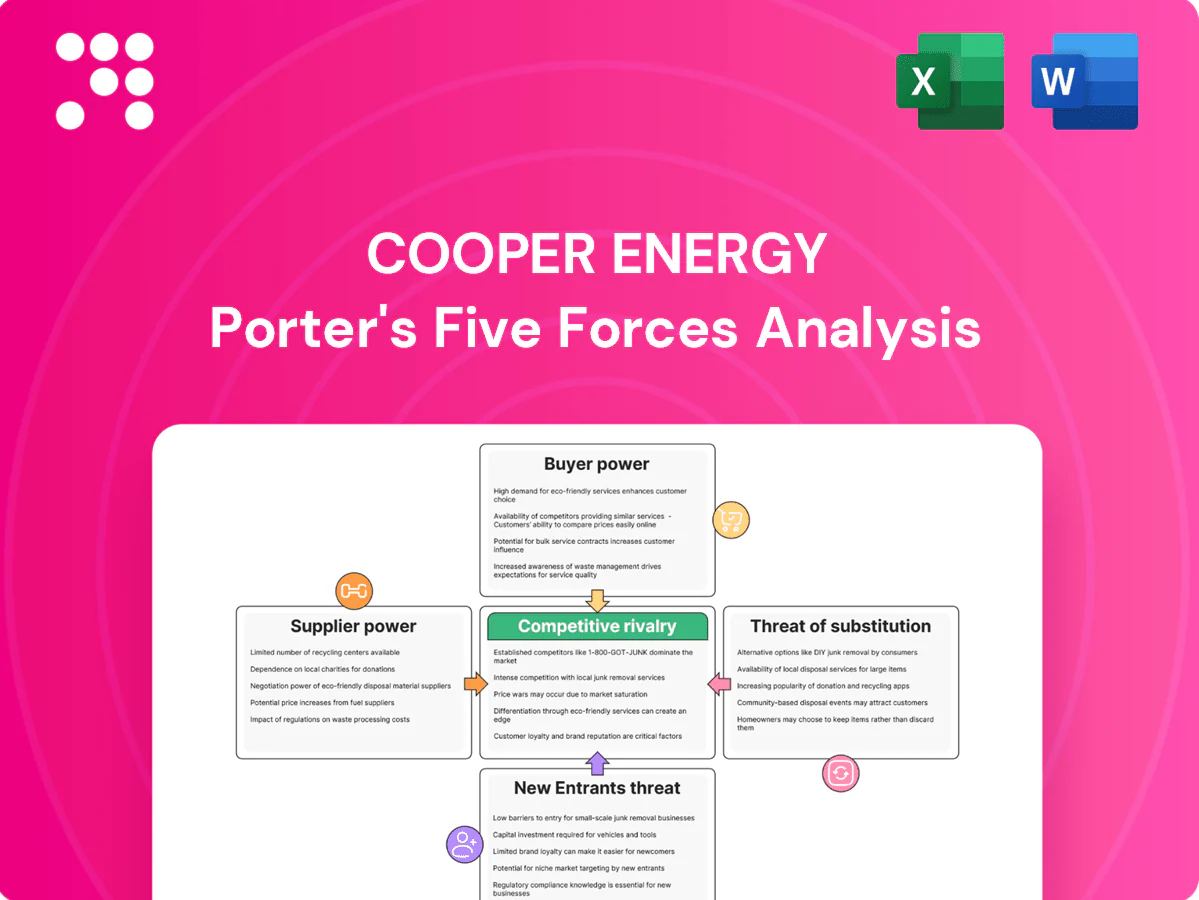

Cooper Energy Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Cooper Energy faces moderate supplier leverage, evolving buyer demands, and growing substitute and regulatory pressures that together shape a cautious growth outlook; competitive rivalry is nuanced by asset-specific advantages and project timelines. This snapshot highlights key tensions—unlock the full Porter's Five Forces Analysis to see force ratings, visuals, and actionable strategy recommendations for Cooper Energy.

Suppliers Bargaining Power

Concentrated midstream processors

Cooper Energy depends on limited third-party gas processing capacity in southeast Australia, notably Victoria plants such as Iona and Orbost, concentrating midstream control. Owners/operators of these key plants can influence pricing and availability through tolling terms, maintenance scheduling and performance standards. Slow, costly switching—due to pipeline links, gas-spec requirements and permitting—heightens supplier leverage over throughput and margins.

Specialized offshore services

Drilling rigs, subsea contractors and OEMs (eg, Aker Solutions, Subsea 7, TechnipFMC) are few and in high demand, giving suppliers strong leverage; high-spec equipment lead times stretched to roughly 12–24 months in 2024. Dayrates and mobilization costs spiked during regional upcycles, causing project schedules to hinge on supplier availability and increasing cost and timing risk. Limited substitutes for complex subsea kit further strengthens supplier bargaining power.

Skilled labor and HSE compliance

Specialist engineering, operations and HSE personnel are scarce for Cooper Energy, with industry wage inflation around 4% in 2024 and specialist pay premiums often near 30% above national averages, giving suppliers leverage. Unionized workforces in energy and construction (sector rates often >20%) can drive higher costs and schedule risk. Mandatory compliance training and accreditations (eg BOSIET/AWES courses ~AUD 1,200 in 2024) reduce switching flexibility and strengthen supplier negotiating power.

Regulatory permits and licences

Regulatory permits and licences act as a supplier for Cooper Energy: governments control approvals, access, and environmental consents, and stricter ESG scrutiny, consultation and decommissioning requirements add time and cost. Delays or onerous conditions can materially reshape project economics and financing, amplifying supplier-like power over project schedules and budgets. This regulatory gatekeeping forces contingency and risk premiums into project valuations.

- Governments as gatekeepers

- ESG, consultation, decommissioning increase time/cost

- Delays reshape economics

- Regulatory risk raises contingency/risk premia

Pipelines and transport access

Access to the Victorian and southeast pipeline network is essential; APA Group owns about 15,000 km of Australian gas transmission pipelines and controls major east‑coast assets, giving operators leverage over capacity, tariffs and maintenance windows.

While regulatory access regimes (AER oversight, common carriage principles) exist, practical alternatives to the established pipeline network are limited for Cooper Energy’s gas flows.

Transport providers therefore materially influence netbacks and delivery certainty, directly affecting realised prices and contract performance.

- Pipeline ownership concentration: APA ~15,000 km

- Regulatory oversight: AER governs access/tariffs

- Impact: transport tariffs and outages reduce netbacks

- Alternatives: limited spare pipeline capacity in SE Australia

Midstream tolling and 12–24 month rig lead times amplify supplier risk

Cooper Energy faces high supplier power from concentrated midstream (Victoria tolling at Iona/Orbost), limited rig/subsea capacity (lead times ~12–24 months in 2024) and specialist labour (wage inflation ~4% in 2024; skill premiums ~30%). APA’s ~15,000 km pipeline network and AER-regulated access constrain alternatives, raising tariffs and outage risk. Regulatory permitting and ESG requirements add delays and contingency costs.

| Factor | 2024 metric |

|---|---|

| Pipeline control | APA ~15,000 km |

| Rig/subsea lead time | 12–24 months |

| Labour inflation | ~4% (pay premiums ~30%) |

| BOSIET cost | AUD 1,200 |

What is included in the product

Concise Porter's Five Forces analysis for Cooper Energy, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications for pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Cooper Energy—clarifies competitive pressures, supplier/customer risks and new-entrant threats so executives can make faster, confident strategic and investment decisions.

Customers Bargaining Power

Concentrated large buyers

Southeast Australian gas buyers are concentrated among a handful of retailers, generators and industrials; as of 2024 four major retailers—AGL, Origin Energy, EnergyAustralia and Alinta—dominate offtake. This concentration enables tougher negotiations on price, quality and contract terms. Portfolio procurement and access to spot/STTM markets reduce buyers’ switching costs. In oversupplied windows producers’ margins are visibly compressed by short‑term price dips in 2023–24.

Contracting and hub pricing

Cooper Energy faces buyers using take-or-pay GSAs alongside exposure to the Victorian wholesale gas market, where hub-indexed contracts (AEMO STTM) dominated 2024 pricing; the Victorian STTM averaged around A$7.00/GJ in 2024, letting buyers benchmark and push for indexation and flex clauses. Market transparency—AEMO publishing daily prices and volumes—enables renegotiation and spot hedging, pressuring producers when spot prices soften.

Policy and price interventions

Government caps and conduct rules, such as domestic supply directions and market monitoring, constrain upstream pricing power during tight periods, allowing buyers to seek regulator intervention over fairness and supply security. Buyers can appeal to bodies like the ACCC for remedies, reinforcing institutional leverage. This framework limits producers’ ability to capture upside in constrained markets and raises bargaining power for large customers.

Alternative sourcing options

Buyers can source gas from multiple basins and from global LNG markets — Australia’s LNG export capacity was about 88 mtpa in 2024 — while potential import terminals in the region expand options. Storage, demand response and fuel-switching (gas to oil/coal or renewables) add short-term flexibility and strengthen buyers’ leverage. Even perceived alternatives reduce dependence on any single supplier and compress pricing power.

- Multiple sourcing routes

- 88 mtpa Australian LNG capacity (2024)

- Storage & demand response = short-term flexibility

- Perceived alternatives boost negotiation

Quality and reliability demands

Power and industrial buyers impose strict specs and delivery profiles on Cooper Energy, tying penalties for outages or off-spec gas to commercial exposure and shifting operational risk to producers. Buyers increasingly use performance metrics and uptime targets as bargaining levers to extract price or term concessions, making reliability central in negotiations. Reliability performance thus directly influences contract pricing and term length.

- Strict specs and delivery profiles

- Penalties for outages/off-spec gas shift risk to producers

- Performance metrics used to extract concessions

- Reliability drives price and term negotiations

Buyer concentration and market transparency boost bargaining power; 88 mtpa LNG

Southeast Australian buyers are concentrated among four major retailers, giving them strong leverage over price, terms and quality. Market transparency (AEMO STTM avg A$7.00/GJ in 2024) and portfolio procurement lower switching costs and enable spot hedging, compressing producer margins in oversupply. Regulatory levers and 88 mtpa LNG export capacity (2024) increase alternative supply options, boosting buyer bargaining power.

| Metric | 2024 Value |

|---|---|

| Major retailers | AGL, Origin, EnergyAustralia, Alinta |

| Victorian STTM avg | A$7.00/GJ |

| Australian LNG capacity | 88 mtpa |

What You See Is What You Get

Cooper Energy Porter's Five Forces Analysis

This preview shows the exact Cooper Energy Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is the final, fully formatted document and will be available for instant download upon payment. Use it immediately for reporting, presentations, or strategic planning.

From Overview to Strategy Blueprint

Cooper Energy faces moderate supplier leverage, evolving buyer demands, and growing substitute and regulatory pressures that together shape a cautious growth outlook; competitive rivalry is nuanced by asset-specific advantages and project timelines. This snapshot highlights key tensions—unlock the full Porter's Five Forces Analysis to see force ratings, visuals, and actionable strategy recommendations for Cooper Energy.

Suppliers Bargaining Power

Concentrated midstream processors

Cooper Energy depends on limited third-party gas processing capacity in southeast Australia, notably Victoria plants such as Iona and Orbost, concentrating midstream control. Owners/operators of these key plants can influence pricing and availability through tolling terms, maintenance scheduling and performance standards. Slow, costly switching—due to pipeline links, gas-spec requirements and permitting—heightens supplier leverage over throughput and margins.

Specialized offshore services

Drilling rigs, subsea contractors and OEMs (eg, Aker Solutions, Subsea 7, TechnipFMC) are few and in high demand, giving suppliers strong leverage; high-spec equipment lead times stretched to roughly 12–24 months in 2024. Dayrates and mobilization costs spiked during regional upcycles, causing project schedules to hinge on supplier availability and increasing cost and timing risk. Limited substitutes for complex subsea kit further strengthens supplier bargaining power.

Skilled labor and HSE compliance

Specialist engineering, operations and HSE personnel are scarce for Cooper Energy, with industry wage inflation around 4% in 2024 and specialist pay premiums often near 30% above national averages, giving suppliers leverage. Unionized workforces in energy and construction (sector rates often >20%) can drive higher costs and schedule risk. Mandatory compliance training and accreditations (eg BOSIET/AWES courses ~AUD 1,200 in 2024) reduce switching flexibility and strengthen supplier negotiating power.

Regulatory permits and licences

Regulatory permits and licences act as a supplier for Cooper Energy: governments control approvals, access, and environmental consents, and stricter ESG scrutiny, consultation and decommissioning requirements add time and cost. Delays or onerous conditions can materially reshape project economics and financing, amplifying supplier-like power over project schedules and budgets. This regulatory gatekeeping forces contingency and risk premiums into project valuations.

- Governments as gatekeepers

- ESG, consultation, decommissioning increase time/cost

- Delays reshape economics

- Regulatory risk raises contingency/risk premia

Pipelines and transport access

Access to the Victorian and southeast pipeline network is essential; APA Group owns about 15,000 km of Australian gas transmission pipelines and controls major east‑coast assets, giving operators leverage over capacity, tariffs and maintenance windows.

While regulatory access regimes (AER oversight, common carriage principles) exist, practical alternatives to the established pipeline network are limited for Cooper Energy’s gas flows.

Transport providers therefore materially influence netbacks and delivery certainty, directly affecting realised prices and contract performance.

- Pipeline ownership concentration: APA ~15,000 km

- Regulatory oversight: AER governs access/tariffs

- Impact: transport tariffs and outages reduce netbacks

- Alternatives: limited spare pipeline capacity in SE Australia

Midstream tolling and 12–24 month rig lead times amplify supplier risk

Cooper Energy faces high supplier power from concentrated midstream (Victoria tolling at Iona/Orbost), limited rig/subsea capacity (lead times ~12–24 months in 2024) and specialist labour (wage inflation ~4% in 2024; skill premiums ~30%). APA’s ~15,000 km pipeline network and AER-regulated access constrain alternatives, raising tariffs and outage risk. Regulatory permitting and ESG requirements add delays and contingency costs.

| Factor | 2024 metric |

|---|---|

| Pipeline control | APA ~15,000 km |

| Rig/subsea lead time | 12–24 months |

| Labour inflation | ~4% (pay premiums ~30%) |

| BOSIET cost | AUD 1,200 |

What is included in the product

Concise Porter's Five Forces analysis for Cooper Energy, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications for pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Cooper Energy—clarifies competitive pressures, supplier/customer risks and new-entrant threats so executives can make faster, confident strategic and investment decisions.

Customers Bargaining Power

Concentrated large buyers

Southeast Australian gas buyers are concentrated among a handful of retailers, generators and industrials; as of 2024 four major retailers—AGL, Origin Energy, EnergyAustralia and Alinta—dominate offtake. This concentration enables tougher negotiations on price, quality and contract terms. Portfolio procurement and access to spot/STTM markets reduce buyers’ switching costs. In oversupplied windows producers’ margins are visibly compressed by short‑term price dips in 2023–24.

Contracting and hub pricing

Cooper Energy faces buyers using take-or-pay GSAs alongside exposure to the Victorian wholesale gas market, where hub-indexed contracts (AEMO STTM) dominated 2024 pricing; the Victorian STTM averaged around A$7.00/GJ in 2024, letting buyers benchmark and push for indexation and flex clauses. Market transparency—AEMO publishing daily prices and volumes—enables renegotiation and spot hedging, pressuring producers when spot prices soften.

Policy and price interventions

Government caps and conduct rules, such as domestic supply directions and market monitoring, constrain upstream pricing power during tight periods, allowing buyers to seek regulator intervention over fairness and supply security. Buyers can appeal to bodies like the ACCC for remedies, reinforcing institutional leverage. This framework limits producers’ ability to capture upside in constrained markets and raises bargaining power for large customers.

Alternative sourcing options

Buyers can source gas from multiple basins and from global LNG markets — Australia’s LNG export capacity was about 88 mtpa in 2024 — while potential import terminals in the region expand options. Storage, demand response and fuel-switching (gas to oil/coal or renewables) add short-term flexibility and strengthen buyers’ leverage. Even perceived alternatives reduce dependence on any single supplier and compress pricing power.

- Multiple sourcing routes

- 88 mtpa Australian LNG capacity (2024)

- Storage & demand response = short-term flexibility

- Perceived alternatives boost negotiation

Quality and reliability demands

Power and industrial buyers impose strict specs and delivery profiles on Cooper Energy, tying penalties for outages or off-spec gas to commercial exposure and shifting operational risk to producers. Buyers increasingly use performance metrics and uptime targets as bargaining levers to extract price or term concessions, making reliability central in negotiations. Reliability performance thus directly influences contract pricing and term length.

- Strict specs and delivery profiles

- Penalties for outages/off-spec gas shift risk to producers

- Performance metrics used to extract concessions

- Reliability drives price and term negotiations

Buyer concentration and market transparency boost bargaining power; 88 mtpa LNG

Southeast Australian buyers are concentrated among four major retailers, giving them strong leverage over price, terms and quality. Market transparency (AEMO STTM avg A$7.00/GJ in 2024) and portfolio procurement lower switching costs and enable spot hedging, compressing producer margins in oversupply. Regulatory levers and 88 mtpa LNG export capacity (2024) increase alternative supply options, boosting buyer bargaining power.

| Metric | 2024 Value |

|---|---|

| Major retailers | AGL, Origin, EnergyAustralia, Alinta |

| Victorian STTM avg | A$7.00/GJ |

| Australian LNG capacity | 88 mtpa |

What You See Is What You Get

Cooper Energy Porter's Five Forces Analysis

This preview shows the exact Cooper Energy Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is the final, fully formatted document and will be available for instant download upon payment. Use it immediately for reporting, presentations, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Cooper Energy faces moderate supplier leverage, evolving buyer demands, and growing substitute and regulatory pressures that together shape a cautious growth outlook; competitive rivalry is nuanced by asset-specific advantages and project timelines. This snapshot highlights key tensions—unlock the full Porter's Five Forces Analysis to see force ratings, visuals, and actionable strategy recommendations for Cooper Energy.

Suppliers Bargaining Power

Concentrated midstream processors

Cooper Energy depends on limited third-party gas processing capacity in southeast Australia, notably Victoria plants such as Iona and Orbost, concentrating midstream control. Owners/operators of these key plants can influence pricing and availability through tolling terms, maintenance scheduling and performance standards. Slow, costly switching—due to pipeline links, gas-spec requirements and permitting—heightens supplier leverage over throughput and margins.

Specialized offshore services

Drilling rigs, subsea contractors and OEMs (eg, Aker Solutions, Subsea 7, TechnipFMC) are few and in high demand, giving suppliers strong leverage; high-spec equipment lead times stretched to roughly 12–24 months in 2024. Dayrates and mobilization costs spiked during regional upcycles, causing project schedules to hinge on supplier availability and increasing cost and timing risk. Limited substitutes for complex subsea kit further strengthens supplier bargaining power.

Skilled labor and HSE compliance

Specialist engineering, operations and HSE personnel are scarce for Cooper Energy, with industry wage inflation around 4% in 2024 and specialist pay premiums often near 30% above national averages, giving suppliers leverage. Unionized workforces in energy and construction (sector rates often >20%) can drive higher costs and schedule risk. Mandatory compliance training and accreditations (eg BOSIET/AWES courses ~AUD 1,200 in 2024) reduce switching flexibility and strengthen supplier negotiating power.

Regulatory permits and licences

Regulatory permits and licences act as a supplier for Cooper Energy: governments control approvals, access, and environmental consents, and stricter ESG scrutiny, consultation and decommissioning requirements add time and cost. Delays or onerous conditions can materially reshape project economics and financing, amplifying supplier-like power over project schedules and budgets. This regulatory gatekeeping forces contingency and risk premiums into project valuations.

- Governments as gatekeepers

- ESG, consultation, decommissioning increase time/cost

- Delays reshape economics

- Regulatory risk raises contingency/risk premia

Pipelines and transport access

Access to the Victorian and southeast pipeline network is essential; APA Group owns about 15,000 km of Australian gas transmission pipelines and controls major east‑coast assets, giving operators leverage over capacity, tariffs and maintenance windows.

While regulatory access regimes (AER oversight, common carriage principles) exist, practical alternatives to the established pipeline network are limited for Cooper Energy’s gas flows.

Transport providers therefore materially influence netbacks and delivery certainty, directly affecting realised prices and contract performance.

- Pipeline ownership concentration: APA ~15,000 km

- Regulatory oversight: AER governs access/tariffs

- Impact: transport tariffs and outages reduce netbacks

- Alternatives: limited spare pipeline capacity in SE Australia

Midstream tolling and 12–24 month rig lead times amplify supplier risk

Cooper Energy faces high supplier power from concentrated midstream (Victoria tolling at Iona/Orbost), limited rig/subsea capacity (lead times ~12–24 months in 2024) and specialist labour (wage inflation ~4% in 2024; skill premiums ~30%). APA’s ~15,000 km pipeline network and AER-regulated access constrain alternatives, raising tariffs and outage risk. Regulatory permitting and ESG requirements add delays and contingency costs.

| Factor | 2024 metric |

|---|---|

| Pipeline control | APA ~15,000 km |

| Rig/subsea lead time | 12–24 months |

| Labour inflation | ~4% (pay premiums ~30%) |

| BOSIET cost | AUD 1,200 |

What is included in the product

Concise Porter's Five Forces analysis for Cooper Energy, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications for pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Cooper Energy—clarifies competitive pressures, supplier/customer risks and new-entrant threats so executives can make faster, confident strategic and investment decisions.

Customers Bargaining Power

Concentrated large buyers

Southeast Australian gas buyers are concentrated among a handful of retailers, generators and industrials; as of 2024 four major retailers—AGL, Origin Energy, EnergyAustralia and Alinta—dominate offtake. This concentration enables tougher negotiations on price, quality and contract terms. Portfolio procurement and access to spot/STTM markets reduce buyers’ switching costs. In oversupplied windows producers’ margins are visibly compressed by short‑term price dips in 2023–24.

Contracting and hub pricing

Cooper Energy faces buyers using take-or-pay GSAs alongside exposure to the Victorian wholesale gas market, where hub-indexed contracts (AEMO STTM) dominated 2024 pricing; the Victorian STTM averaged around A$7.00/GJ in 2024, letting buyers benchmark and push for indexation and flex clauses. Market transparency—AEMO publishing daily prices and volumes—enables renegotiation and spot hedging, pressuring producers when spot prices soften.

Policy and price interventions

Government caps and conduct rules, such as domestic supply directions and market monitoring, constrain upstream pricing power during tight periods, allowing buyers to seek regulator intervention over fairness and supply security. Buyers can appeal to bodies like the ACCC for remedies, reinforcing institutional leverage. This framework limits producers’ ability to capture upside in constrained markets and raises bargaining power for large customers.

Alternative sourcing options

Buyers can source gas from multiple basins and from global LNG markets — Australia’s LNG export capacity was about 88 mtpa in 2024 — while potential import terminals in the region expand options. Storage, demand response and fuel-switching (gas to oil/coal or renewables) add short-term flexibility and strengthen buyers’ leverage. Even perceived alternatives reduce dependence on any single supplier and compress pricing power.

- Multiple sourcing routes

- 88 mtpa Australian LNG capacity (2024)

- Storage & demand response = short-term flexibility

- Perceived alternatives boost negotiation

Quality and reliability demands

Power and industrial buyers impose strict specs and delivery profiles on Cooper Energy, tying penalties for outages or off-spec gas to commercial exposure and shifting operational risk to producers. Buyers increasingly use performance metrics and uptime targets as bargaining levers to extract price or term concessions, making reliability central in negotiations. Reliability performance thus directly influences contract pricing and term length.

- Strict specs and delivery profiles

- Penalties for outages/off-spec gas shift risk to producers

- Performance metrics used to extract concessions

- Reliability drives price and term negotiations

Buyer concentration and market transparency boost bargaining power; 88 mtpa LNG

Southeast Australian buyers are concentrated among four major retailers, giving them strong leverage over price, terms and quality. Market transparency (AEMO STTM avg A$7.00/GJ in 2024) and portfolio procurement lower switching costs and enable spot hedging, compressing producer margins in oversupply. Regulatory levers and 88 mtpa LNG export capacity (2024) increase alternative supply options, boosting buyer bargaining power.

| Metric | 2024 Value |

|---|---|

| Major retailers | AGL, Origin, EnergyAustralia, Alinta |

| Victorian STTM avg | A$7.00/GJ |

| Australian LNG capacity | 88 mtpa |

What You See Is What You Get

Cooper Energy Porter's Five Forces Analysis

This preview shows the exact Cooper Energy Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is the final, fully formatted document and will be available for instant download upon payment. Use it immediately for reporting, presentations, or strategic planning.