Corem Boston Consulting Group Matrix

See the Bigger Picture

Want to stop guessing and start allocating capital with confidence? This Corem BCG Matrix preview shows the headline — but the full report maps every product into Stars, Cash Cows, Dogs, or Question Marks and gives data-backed moves to act on. Purchase the complete BCG Matrix for quadrant-level analysis, strategic recommendations, and ready-to-use Word + Excel files you can present to your board. Skip the homework — buy now and get clarity fast.

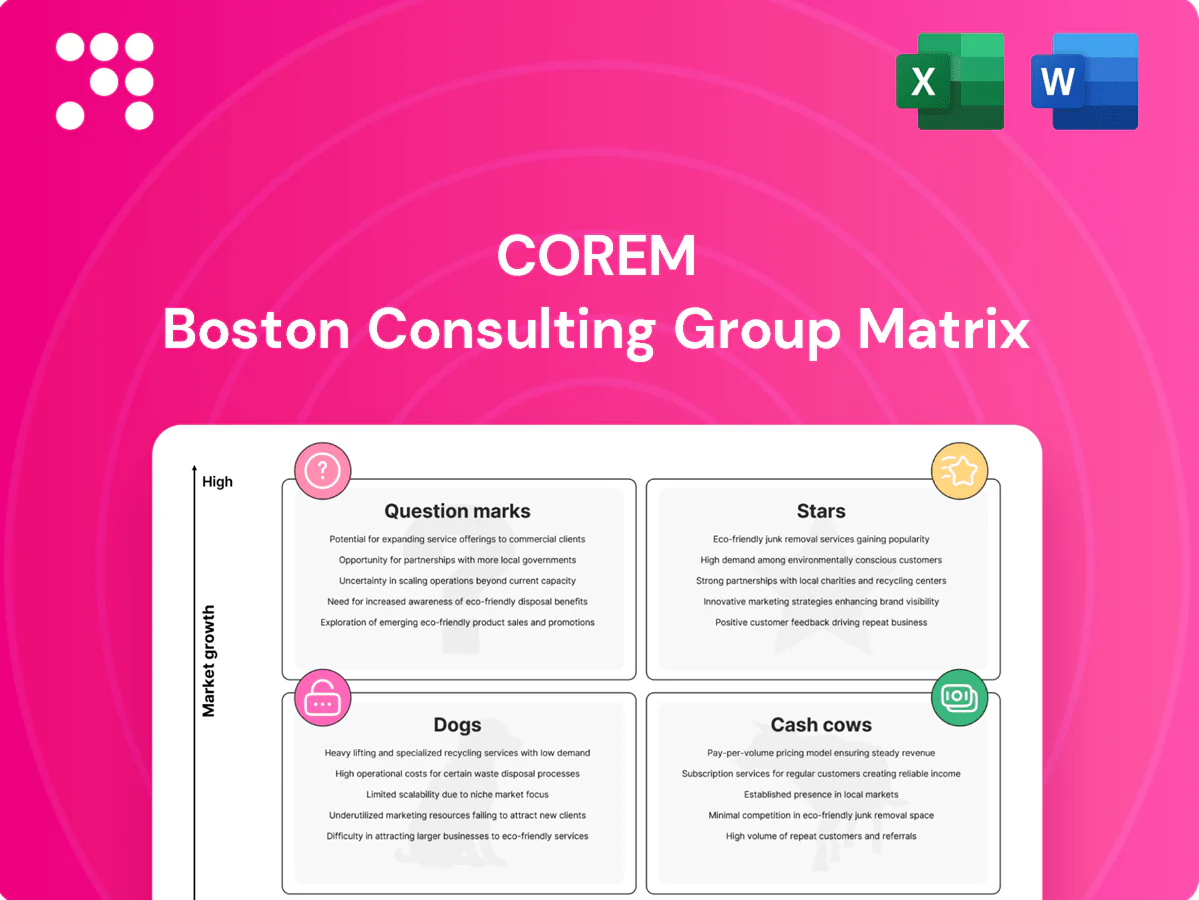

Stars

Prime logistics hubs by ports/air cargo

Global e-commerce reached about $6.4 trillion in 2024, swelling throughput at major sea and air gateways and lifting demand for Corem’s big-box logistics near ports and airports. These assets are market leaders with sticky tenants, typically achieving c.96% occupancy and strong lease renewal rates. They absorb capex for high-spec builds, automation and tenant improvements (often €50–€150/sqm) which translate into rent premia and NOI uplift. Hold share and these hubs increasingly behave like low-volatility cash machines.

Urban last‑mile infill warehouses

Urban last‑mile infill warehouses sit inside scarce ring‑road plots and are driving Corem’s portfolio performance as same‑day delivery demand surged through 2024; prime urban logistics rents rose sharply and absorption remained strong. High rents and persistent leasing heat justify ongoing reinvestment in docks and traffic flow upgrades. Maintain occupancy, stay visible and be first for tenant expansions to protect cash flow.

Build‑to‑suit logistics parks near intermodals

Custom build‑to‑suit logistics parks sited at rail‑highway intermodals lock anchors and define submarket DNA, with major gateway vacancy averaging about 5% in 2024 supporting strong demand. They drive the market narrative but require heavy upfront capex—park projects often entail construction budgets in the tens of millions. Marketing, placemaking and phased delivery maintain leasing momentum. Nail pre‑lets (often >50% before break ground) and value compounds quickly.

Temperature‑controlled/cold‑chain facilities

Temperature‑controlled/cold‑chain facilities

Food and pharma logistics are growing and sticky; modern cold chain remains undersupplied, Corem’s specialized boxes command a c.15–25% rent premium and run near 95% occupancy, supporting outsized NOI despite higher utilities and equipment Opex. Returns track sector growth (mid‑single to high‑single digit CAGR); stay invested — this lane can outpace the broader industrial curve.- Tags: Stars, Cold‑chain, High occupancy, Premium rents, Elevated Opex

ESG‑forward “green” logistics redevelopments

ESG‑forward green logistics redevelopments—solar, EV charging and high‑efficiency envelopes—win tenders and major tenants, commanding up to a 15% rent premium in 2024 and accessing financing at roughly 10–25 bps cheaper pricing (2024 market reports). Capex is chunky but rent uplift and lower cost of capital offset lifecycle costs; keep scaling: today’s star sets tomorrow’s benchmark.

- tenant demand: large users prefer net‑zero-ready space

- finance: sustainable debt cheaper by ~10–25 bps (2024)

- returns: rent premium up to 15% (2024)

Gateway hubs 96% occ; e-commerce $6.4tn fuels last-mile & cold-chain

Corem Stars: gateway big‑box hubs drive stable cashflow (c.96% occupancy) as global e‑commerce hit $6.4tn in 2024; urban last‑mile infill and build‑to‑suit intermodals command scarcity rents and pre‑lets >50%; cold‑chain earns c.15–25% rent premium at ~95% occupancy; ESG redevelopments capture up to 15% rent uplift and 10–25bps cheaper debt in 2024.

| Asset | Occupancy | Rent premium | Financing | Capex |

|---|---|---|---|---|

| Big‑box gateways | c.96% | premium via specs | — | €50–€150/sqm |

| Last‑mile | high/scarce | strong | — | traffic/dock upgrades |

| Cold‑chain | ~95% | 15–25% | — | elevated Opex |

| Green redevelop | high | up to 15% | 10–25bps cheaper | chunky |

What is included in the product

Comprehensive BCG Matrix review of Corem’s units, offering quadrant-based insights and clear invest, hold or divest recommendations.

One-page Corem BCG Matrix that maps units to quadrants, unclutters strategy and speeds C-suite decisions.

Cash Cows

Stabilized regional distribution centers

Stabilized regional distribution centers sit in mature submarkets with high market share and long leases, delivering predictable cash — occupancy remained above 95% in 2024 and rental income showed strong stability. Low growth and low drama combine with high margins (industry NOI often >50% in 2024), while light-touch capex keeps opex lean and uptime strong. These cash flows are ideal to fund development pipelines and service debt.

Anchored retail parks serving trade tenants

Anchored retail parks focused on DIY, home improvement and value retail deliver steady footfall and durable covenants, with occupancy circa 95% in 2024 and market rents broadly flat. Growth is flat but income is solid — headline yields around 5.5–6.5% support reliable NOI. Minimal promo spend; emphasis on renewals and operational efficiency. Milk the cash and recycle selectively.

Core urban light‑industrial clusters

Core urban light-industrial clusters are small-bay, multi-tenant assets delivering 95%+ occupancy in established corridors, with manageable churn and tenant retention supporting steady cash flow. Healthy rental spreads and demand-driven rent growth sustain margins, while low-cost incremental upgrades typically lift NOI by mid-single-digit percentages. They serve as a reliable engine room for the portfolio, funding growth and stabilizing returns.

Long‑leased logistics with investment‑grade tenants

Long‑leased logistics with investment‑grade tenants deliver locked‑in rent streams, very low vacancy risk and limited headline growth—Corem’s logistics arm reported c.98.5% occupancy in 2024 and stable contractual escalations supporting predictable cash flow.

Maintenance capex dominates spend, yielding high NOI margins and steady free cash flow that funds growth bets while assets quietly compound value.

- Locked‑in rent: long leases

- Vacancy: c.98.5% occupied (2024)

- Growth: headline limited

- Capex: maintenance only

- Outcome: margin rich, steady FCF

Land parcels with ground rents

Land parcels with ground rents are simple structures with passive escalators and near-zero capex, delivering steady, predictable cash rather than flash; they act as a strong collateral and liquidity buffer for Corem, enabling a hold strategy where time compounds returns. Hold and let the clock do the work.

- Simple structures

- Passive escalators

- Near-zero capex

- Strong collateral/liquidity

Stable cash cows: high-margin DCs, logistics & retail powering steady FCF

Corem cash cows deliver steady, high-margin cash: stabilized DCs and light-industrial at 95%+ occupancy in 2024, logistics c.98.5% occupancy, industry NOI often >50% (2024) and retail yields ~5.5–6.5%; low growth, maintenance capex and predictable escalators make them primary FCF engines to fund development and service debt.

| Asset | Occupancy (2024) | NOI margin (2024) | Yield |

|---|---|---|---|

| Regional DCs | 95–99% | 50–60% | 4.5–5.5% |

| Retail parks | ≈95% | 45–55% | 5.5–6.5% |

| Light‑industrial | 95%+ | 50–60% | 5–6% |

| Logistics (IG tenants) | ≈98.5% | 55–65% | 3.5–4.5% |

| Land parcels | NA | NA | Stable ground rent |

Full Transparency, Always

Corem BCG Matrix

The file you're previewing is the Corem BCG Matrix you'll receive after purchase. No watermarks, no demo notes—just the fully formatted, analysis-ready report designed for strategic clarity. Once bought it downloads immediately and is editable for presentations or planning. It's the exact final document, crafted for busy founders and CFOs who want results, fast.

See the Bigger Picture

Want to stop guessing and start allocating capital with confidence? This Corem BCG Matrix preview shows the headline — but the full report maps every product into Stars, Cash Cows, Dogs, or Question Marks and gives data-backed moves to act on. Purchase the complete BCG Matrix for quadrant-level analysis, strategic recommendations, and ready-to-use Word + Excel files you can present to your board. Skip the homework — buy now and get clarity fast.

Stars

Prime logistics hubs by ports/air cargo

Global e-commerce reached about $6.4 trillion in 2024, swelling throughput at major sea and air gateways and lifting demand for Corem’s big-box logistics near ports and airports. These assets are market leaders with sticky tenants, typically achieving c.96% occupancy and strong lease renewal rates. They absorb capex for high-spec builds, automation and tenant improvements (often €50–€150/sqm) which translate into rent premia and NOI uplift. Hold share and these hubs increasingly behave like low-volatility cash machines.

Urban last‑mile infill warehouses

Urban last‑mile infill warehouses sit inside scarce ring‑road plots and are driving Corem’s portfolio performance as same‑day delivery demand surged through 2024; prime urban logistics rents rose sharply and absorption remained strong. High rents and persistent leasing heat justify ongoing reinvestment in docks and traffic flow upgrades. Maintain occupancy, stay visible and be first for tenant expansions to protect cash flow.

Build‑to‑suit logistics parks near intermodals

Custom build‑to‑suit logistics parks sited at rail‑highway intermodals lock anchors and define submarket DNA, with major gateway vacancy averaging about 5% in 2024 supporting strong demand. They drive the market narrative but require heavy upfront capex—park projects often entail construction budgets in the tens of millions. Marketing, placemaking and phased delivery maintain leasing momentum. Nail pre‑lets (often >50% before break ground) and value compounds quickly.

Temperature‑controlled/cold‑chain facilities

Temperature‑controlled/cold‑chain facilities

Food and pharma logistics are growing and sticky; modern cold chain remains undersupplied, Corem’s specialized boxes command a c.15–25% rent premium and run near 95% occupancy, supporting outsized NOI despite higher utilities and equipment Opex. Returns track sector growth (mid‑single to high‑single digit CAGR); stay invested — this lane can outpace the broader industrial curve.- Tags: Stars, Cold‑chain, High occupancy, Premium rents, Elevated Opex

ESG‑forward “green” logistics redevelopments

ESG‑forward green logistics redevelopments—solar, EV charging and high‑efficiency envelopes—win tenders and major tenants, commanding up to a 15% rent premium in 2024 and accessing financing at roughly 10–25 bps cheaper pricing (2024 market reports). Capex is chunky but rent uplift and lower cost of capital offset lifecycle costs; keep scaling: today’s star sets tomorrow’s benchmark.

- tenant demand: large users prefer net‑zero-ready space

- finance: sustainable debt cheaper by ~10–25 bps (2024)

- returns: rent premium up to 15% (2024)

Gateway hubs 96% occ; e-commerce $6.4tn fuels last-mile & cold-chain

Corem Stars: gateway big‑box hubs drive stable cashflow (c.96% occupancy) as global e‑commerce hit $6.4tn in 2024; urban last‑mile infill and build‑to‑suit intermodals command scarcity rents and pre‑lets >50%; cold‑chain earns c.15–25% rent premium at ~95% occupancy; ESG redevelopments capture up to 15% rent uplift and 10–25bps cheaper debt in 2024.

| Asset | Occupancy | Rent premium | Financing | Capex |

|---|---|---|---|---|

| Big‑box gateways | c.96% | premium via specs | — | €50–€150/sqm |

| Last‑mile | high/scarce | strong | — | traffic/dock upgrades |

| Cold‑chain | ~95% | 15–25% | — | elevated Opex |

| Green redevelop | high | up to 15% | 10–25bps cheaper | chunky |

What is included in the product

Comprehensive BCG Matrix review of Corem’s units, offering quadrant-based insights and clear invest, hold or divest recommendations.

One-page Corem BCG Matrix that maps units to quadrants, unclutters strategy and speeds C-suite decisions.

Cash Cows

Stabilized regional distribution centers

Stabilized regional distribution centers sit in mature submarkets with high market share and long leases, delivering predictable cash — occupancy remained above 95% in 2024 and rental income showed strong stability. Low growth and low drama combine with high margins (industry NOI often >50% in 2024), while light-touch capex keeps opex lean and uptime strong. These cash flows are ideal to fund development pipelines and service debt.

Anchored retail parks serving trade tenants

Anchored retail parks focused on DIY, home improvement and value retail deliver steady footfall and durable covenants, with occupancy circa 95% in 2024 and market rents broadly flat. Growth is flat but income is solid — headline yields around 5.5–6.5% support reliable NOI. Minimal promo spend; emphasis on renewals and operational efficiency. Milk the cash and recycle selectively.

Core urban light‑industrial clusters

Core urban light-industrial clusters are small-bay, multi-tenant assets delivering 95%+ occupancy in established corridors, with manageable churn and tenant retention supporting steady cash flow. Healthy rental spreads and demand-driven rent growth sustain margins, while low-cost incremental upgrades typically lift NOI by mid-single-digit percentages. They serve as a reliable engine room for the portfolio, funding growth and stabilizing returns.

Long‑leased logistics with investment‑grade tenants

Long‑leased logistics with investment‑grade tenants deliver locked‑in rent streams, very low vacancy risk and limited headline growth—Corem’s logistics arm reported c.98.5% occupancy in 2024 and stable contractual escalations supporting predictable cash flow.

Maintenance capex dominates spend, yielding high NOI margins and steady free cash flow that funds growth bets while assets quietly compound value.

- Locked‑in rent: long leases

- Vacancy: c.98.5% occupied (2024)

- Growth: headline limited

- Capex: maintenance only

- Outcome: margin rich, steady FCF

Land parcels with ground rents

Land parcels with ground rents are simple structures with passive escalators and near-zero capex, delivering steady, predictable cash rather than flash; they act as a strong collateral and liquidity buffer for Corem, enabling a hold strategy where time compounds returns. Hold and let the clock do the work.

- Simple structures

- Passive escalators

- Near-zero capex

- Strong collateral/liquidity

Stable cash cows: high-margin DCs, logistics & retail powering steady FCF

Corem cash cows deliver steady, high-margin cash: stabilized DCs and light-industrial at 95%+ occupancy in 2024, logistics c.98.5% occupancy, industry NOI often >50% (2024) and retail yields ~5.5–6.5%; low growth, maintenance capex and predictable escalators make them primary FCF engines to fund development and service debt.

| Asset | Occupancy (2024) | NOI margin (2024) | Yield |

|---|---|---|---|

| Regional DCs | 95–99% | 50–60% | 4.5–5.5% |

| Retail parks | ≈95% | 45–55% | 5.5–6.5% |

| Light‑industrial | 95%+ | 50–60% | 5–6% |

| Logistics (IG tenants) | ≈98.5% | 55–65% | 3.5–4.5% |

| Land parcels | NA | NA | Stable ground rent |

Full Transparency, Always

Corem BCG Matrix

The file you're previewing is the Corem BCG Matrix you'll receive after purchase. No watermarks, no demo notes—just the fully formatted, analysis-ready report designed for strategic clarity. Once bought it downloads immediately and is editable for presentations or planning. It's the exact final document, crafted for busy founders and CFOs who want results, fast.

Description

See the Bigger Picture

Want to stop guessing and start allocating capital with confidence? This Corem BCG Matrix preview shows the headline — but the full report maps every product into Stars, Cash Cows, Dogs, or Question Marks and gives data-backed moves to act on. Purchase the complete BCG Matrix for quadrant-level analysis, strategic recommendations, and ready-to-use Word + Excel files you can present to your board. Skip the homework — buy now and get clarity fast.

Stars

Prime logistics hubs by ports/air cargo

Global e-commerce reached about $6.4 trillion in 2024, swelling throughput at major sea and air gateways and lifting demand for Corem’s big-box logistics near ports and airports. These assets are market leaders with sticky tenants, typically achieving c.96% occupancy and strong lease renewal rates. They absorb capex for high-spec builds, automation and tenant improvements (often €50–€150/sqm) which translate into rent premia and NOI uplift. Hold share and these hubs increasingly behave like low-volatility cash machines.

Urban last‑mile infill warehouses

Urban last‑mile infill warehouses sit inside scarce ring‑road plots and are driving Corem’s portfolio performance as same‑day delivery demand surged through 2024; prime urban logistics rents rose sharply and absorption remained strong. High rents and persistent leasing heat justify ongoing reinvestment in docks and traffic flow upgrades. Maintain occupancy, stay visible and be first for tenant expansions to protect cash flow.

Build‑to‑suit logistics parks near intermodals

Custom build‑to‑suit logistics parks sited at rail‑highway intermodals lock anchors and define submarket DNA, with major gateway vacancy averaging about 5% in 2024 supporting strong demand. They drive the market narrative but require heavy upfront capex—park projects often entail construction budgets in the tens of millions. Marketing, placemaking and phased delivery maintain leasing momentum. Nail pre‑lets (often >50% before break ground) and value compounds quickly.

Temperature‑controlled/cold‑chain facilities

Temperature‑controlled/cold‑chain facilities

Food and pharma logistics are growing and sticky; modern cold chain remains undersupplied, Corem’s specialized boxes command a c.15–25% rent premium and run near 95% occupancy, supporting outsized NOI despite higher utilities and equipment Opex. Returns track sector growth (mid‑single to high‑single digit CAGR); stay invested — this lane can outpace the broader industrial curve.- Tags: Stars, Cold‑chain, High occupancy, Premium rents, Elevated Opex

ESG‑forward “green” logistics redevelopments

ESG‑forward green logistics redevelopments—solar, EV charging and high‑efficiency envelopes—win tenders and major tenants, commanding up to a 15% rent premium in 2024 and accessing financing at roughly 10–25 bps cheaper pricing (2024 market reports). Capex is chunky but rent uplift and lower cost of capital offset lifecycle costs; keep scaling: today’s star sets tomorrow’s benchmark.

- tenant demand: large users prefer net‑zero-ready space

- finance: sustainable debt cheaper by ~10–25 bps (2024)

- returns: rent premium up to 15% (2024)

Gateway hubs 96% occ; e-commerce $6.4tn fuels last-mile & cold-chain

Corem Stars: gateway big‑box hubs drive stable cashflow (c.96% occupancy) as global e‑commerce hit $6.4tn in 2024; urban last‑mile infill and build‑to‑suit intermodals command scarcity rents and pre‑lets >50%; cold‑chain earns c.15–25% rent premium at ~95% occupancy; ESG redevelopments capture up to 15% rent uplift and 10–25bps cheaper debt in 2024.

| Asset | Occupancy | Rent premium | Financing | Capex |

|---|---|---|---|---|

| Big‑box gateways | c.96% | premium via specs | — | €50–€150/sqm |

| Last‑mile | high/scarce | strong | — | traffic/dock upgrades |

| Cold‑chain | ~95% | 15–25% | — | elevated Opex |

| Green redevelop | high | up to 15% | 10–25bps cheaper | chunky |

What is included in the product

Comprehensive BCG Matrix review of Corem’s units, offering quadrant-based insights and clear invest, hold or divest recommendations.

One-page Corem BCG Matrix that maps units to quadrants, unclutters strategy and speeds C-suite decisions.

Cash Cows

Stabilized regional distribution centers

Stabilized regional distribution centers sit in mature submarkets with high market share and long leases, delivering predictable cash — occupancy remained above 95% in 2024 and rental income showed strong stability. Low growth and low drama combine with high margins (industry NOI often >50% in 2024), while light-touch capex keeps opex lean and uptime strong. These cash flows are ideal to fund development pipelines and service debt.

Anchored retail parks serving trade tenants

Anchored retail parks focused on DIY, home improvement and value retail deliver steady footfall and durable covenants, with occupancy circa 95% in 2024 and market rents broadly flat. Growth is flat but income is solid — headline yields around 5.5–6.5% support reliable NOI. Minimal promo spend; emphasis on renewals and operational efficiency. Milk the cash and recycle selectively.

Core urban light‑industrial clusters

Core urban light-industrial clusters are small-bay, multi-tenant assets delivering 95%+ occupancy in established corridors, with manageable churn and tenant retention supporting steady cash flow. Healthy rental spreads and demand-driven rent growth sustain margins, while low-cost incremental upgrades typically lift NOI by mid-single-digit percentages. They serve as a reliable engine room for the portfolio, funding growth and stabilizing returns.

Long‑leased logistics with investment‑grade tenants

Long‑leased logistics with investment‑grade tenants deliver locked‑in rent streams, very low vacancy risk and limited headline growth—Corem’s logistics arm reported c.98.5% occupancy in 2024 and stable contractual escalations supporting predictable cash flow.

Maintenance capex dominates spend, yielding high NOI margins and steady free cash flow that funds growth bets while assets quietly compound value.

- Locked‑in rent: long leases

- Vacancy: c.98.5% occupied (2024)

- Growth: headline limited

- Capex: maintenance only

- Outcome: margin rich, steady FCF

Land parcels with ground rents

Land parcels with ground rents are simple structures with passive escalators and near-zero capex, delivering steady, predictable cash rather than flash; they act as a strong collateral and liquidity buffer for Corem, enabling a hold strategy where time compounds returns. Hold and let the clock do the work.

- Simple structures

- Passive escalators

- Near-zero capex

- Strong collateral/liquidity

Stable cash cows: high-margin DCs, logistics & retail powering steady FCF

Corem cash cows deliver steady, high-margin cash: stabilized DCs and light-industrial at 95%+ occupancy in 2024, logistics c.98.5% occupancy, industry NOI often >50% (2024) and retail yields ~5.5–6.5%; low growth, maintenance capex and predictable escalators make them primary FCF engines to fund development and service debt.

| Asset | Occupancy (2024) | NOI margin (2024) | Yield |

|---|---|---|---|

| Regional DCs | 95–99% | 50–60% | 4.5–5.5% |

| Retail parks | ≈95% | 45–55% | 5.5–6.5% |

| Light‑industrial | 95%+ | 50–60% | 5–6% |

| Logistics (IG tenants) | ≈98.5% | 55–65% | 3.5–4.5% |

| Land parcels | NA | NA | Stable ground rent |

Full Transparency, Always

Corem BCG Matrix

The file you're previewing is the Corem BCG Matrix you'll receive after purchase. No watermarks, no demo notes—just the fully formatted, analysis-ready report designed for strategic clarity. Once bought it downloads immediately and is editable for presentations or planning. It's the exact final document, crafted for busy founders and CFOs who want results, fast.