Corem Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

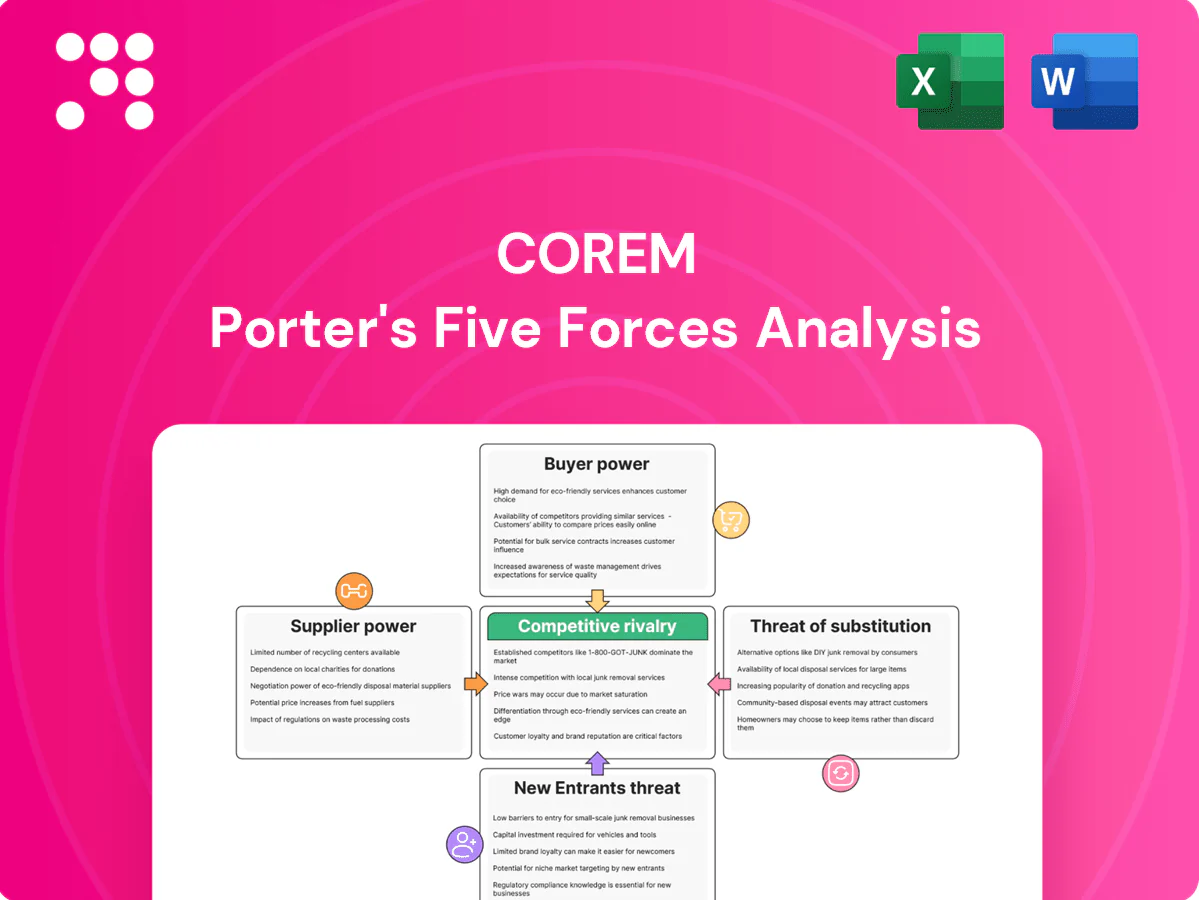

Corem's Porter’s Five Forces snapshot highlights buyer and supplier leverage, competitive rivalry, entry barriers, and substitute risks shaping its profitability, offering a concise view of strategic pressures and opportunities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Corem’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce zoned land

Prime plots near transport hubs are limited in 2024, giving landowners leverage on price and terms. Competition for these sites often triggers bidding wars and option premiums, pushing acquisition prices materially higher. This elevates acquisition costs and can lengthen deal cycles by several months. Corem must secure land early and cultivate sellers to mitigate spikes and timing risk.

Fragmented contractors

The supplier base for construction and maintenance is highly fragmented, giving Corem multiple switching options and keeping supplier concentration low; public framework agreements and competitive tenders in 2024 have been shown to compress supplier margins by around 10%, capping pricing power. Specialized logistics builds with high clear heights and dock-door configurations narrow the pool of qualified vendors. For complex, bespoke projects this concentration can temporarily boost supplier influence and lead times.

Input cost volatility

Steel, concrete and energy are highly cyclical and inflation-sensitive; global crude averaged about $80/bbl in 2024 and many markets saw finished steel prices near 10% higher year‑on‑year, compressing development yields when spikes occur unless hedged or passed through. Index‑linked contracts and value engineering mitigate but rarely eliminate pressure, so timing and procurement strategy materially affect returns.

Regulatory gatekeepers

Facility services dependence

Critical services (HVAC, security, facility tech, ESG monitoring) create concentrated reliance on a few vendors, making suppliers strategically powerful; switching entails integration risk and measurable downtime. Multi-year SLAs, typically 3–5 years, can lock in terms that become unfavorable if markets shift. Dual-sourcing and strict performance KPIs rebalance bargaining power.

- Concentration risk: few specialist vendors

- SLA length: 3–5 years

- Mitigation: dual-sourcing + KPI-linked fees

Land scarcity lifts bids; crude $80, steel +10%

Supplier power is mixed: scarce prime land near hubs raises bid premiums and delays; fragmented construction suppliers compressed margins ~10% in 2024 but specialization boosts power for bespoke works and critical services with SLAs of 3–5 years. Input inflation (crude ~ $80/bbl, steel +10% YoY 2024) increases development costs unless hedged or passed through.

| Factor | 2024 metric | Impact |

|---|---|---|

| Land scarcity | High near hubs | Higher acquisition prices, longer cycles |

| Construction margins | Compression ~10% | Lower supplier pricing power |

| Permits | Median 12 weeks (Sweden) | Timing risk |

| Inputs | Crude ~$80/bbl; steel +10% YoY | Costs up, compresses yields |

| Critical services | SLA 3–5 yrs | Concentration risk |

What is included in the product

Concise Porter's Five Forces assessment for Corem that diagnoses competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlights strategic levers and vulnerabilities affecting Corem’s pricing, margins, and market positioning.

Corem Porter's Five Forces delivers a concise one-sheet snapshot of competitive pressures—customizable force levels and an intuitive radar chart let teams quickly diagnose threats and prioritize strategic responses.

Customers Bargaining Power

Concentrated anchor tenants

Large 3PLs, e-commerce and retail chains lease big-box logistics sites often >20,000 sqm and, by scale, secure rent concessions and tenant-improvement packages that can reduce effective rents by 10–20% versus headline rents; Amazon held ~38% of US marketplace sales in 2023, amplifying bargaining leverage. Losing a single anchor can cut site-level occupancy and NOI materially—often by 10–30%—so diversifying tenant mix reduces single-tenant leverage.

Vacancy sensitivity

Buyer power rises when market vacancy increases; by 2024 Swedish office vacancy approached ~12%, letting tenants shop comparable sites and extract larger incentives. Tenants routinely negotiate fit-out contributions and rent-free periods, pressuring landlords. In tight submarkets near hubs, landlords regain pricing power, so monitoring local absorption rates guides leasing strategy.

Customization demands

Tenants frequently demand racking, mezzanines and specialized loading, driving tenant-improvement (TI) costs that often reach tens of dollars per sq ft and can materially shift capex to landlords.

Build-to-suit transactions in 2024 embedded tenant leverage during design and leasing, increasing landlord exposure on bespoke specs and longer lease-up horizons.

Standardized specs and re-lettable designs preserve economics by limiting TI write-offs and improving remarketing to multiple users.

Switching costs

Switching costs — operational disruption, relocation expenses and re-permitting — create tenant stickiness that moderates buyer power at renewal, especially for optimized sites; in 2024 surveys about 60% of occupiers cited disruption as a primary relocation barrier and relocation often exceeds six months’ rent. Break clauses and flexible terms can offset stickiness, while proactive asset management raises renewal capture rates and lease roll-through.

- Operational disruption: ~60% cite as major barrier (2024)

- Relocation cost: often >6 months’ rent

- Re-permitting delays: months to >1 year

- Mitigants: break clauses, flexible terms, proactive asset management

ESG and green leases

Large tenants now demand measurable energy efficiency, certifications, and transparent consumption data; in 2024 the EU carbon price averaged about €100/t, raising operating scrutiny and capex for retrofits.

Compliance raises upfront capex but can enable rent premiums and lower vacancy; green leases shift OpEx via pass-throughs and performance metrics, converting buyer power into partnership value.

- Tenant demands: certifications, data transparency

- 2024 carbon price: ~€100/t (EU)

- Capex vs rent premium trade-off

- Green leases: OpEx pass-throughs, KPI-linked rents

Anchors squeeze landlords - loss can cut NOI 10-30%; vacancy rises, carbon costs surge

Customer bargaining is high: large 3PLs and e-commerce anchors (Amazon ~38% US marketplace sales 2023) extract rent concessions and TI, and losing an anchor can cut NOI 10–30%. Vacancy rose (Swedish office ~12% 2024), boosting tenant leverage; 60% cite disruption as a major relocation barrier. Energy rules matter: EU carbon ~€100/t (2024) shifts capex to landlords.

| Metric | 2024 |

|---|---|

| Anchor impact on NOI | 10–30% |

| Swedish office vacancy | ~12% |

| Occupiers citing disruption | ~60% |

| EU carbon price | ~€100/t |

Same Document Delivered

Corem Porter's Five Forces Analysis

This preview shows the exact Corem Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is the full, professionally formatted file, ready for download and use the moment you buy. You'll get this same deliverable with clear insights on competitive rivalry, supplier and buyer power, threats of substitution and entry.

A Must-Have Tool for Decision-Makers

Corem's Porter’s Five Forces snapshot highlights buyer and supplier leverage, competitive rivalry, entry barriers, and substitute risks shaping its profitability, offering a concise view of strategic pressures and opportunities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Corem’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce zoned land

Prime plots near transport hubs are limited in 2024, giving landowners leverage on price and terms. Competition for these sites often triggers bidding wars and option premiums, pushing acquisition prices materially higher. This elevates acquisition costs and can lengthen deal cycles by several months. Corem must secure land early and cultivate sellers to mitigate spikes and timing risk.

Fragmented contractors

The supplier base for construction and maintenance is highly fragmented, giving Corem multiple switching options and keeping supplier concentration low; public framework agreements and competitive tenders in 2024 have been shown to compress supplier margins by around 10%, capping pricing power. Specialized logistics builds with high clear heights and dock-door configurations narrow the pool of qualified vendors. For complex, bespoke projects this concentration can temporarily boost supplier influence and lead times.

Input cost volatility

Steel, concrete and energy are highly cyclical and inflation-sensitive; global crude averaged about $80/bbl in 2024 and many markets saw finished steel prices near 10% higher year‑on‑year, compressing development yields when spikes occur unless hedged or passed through. Index‑linked contracts and value engineering mitigate but rarely eliminate pressure, so timing and procurement strategy materially affect returns.

Regulatory gatekeepers

Facility services dependence

Critical services (HVAC, security, facility tech, ESG monitoring) create concentrated reliance on a few vendors, making suppliers strategically powerful; switching entails integration risk and measurable downtime. Multi-year SLAs, typically 3–5 years, can lock in terms that become unfavorable if markets shift. Dual-sourcing and strict performance KPIs rebalance bargaining power.

- Concentration risk: few specialist vendors

- SLA length: 3–5 years

- Mitigation: dual-sourcing + KPI-linked fees

Land scarcity lifts bids; crude $80, steel +10%

Supplier power is mixed: scarce prime land near hubs raises bid premiums and delays; fragmented construction suppliers compressed margins ~10% in 2024 but specialization boosts power for bespoke works and critical services with SLAs of 3–5 years. Input inflation (crude ~ $80/bbl, steel +10% YoY 2024) increases development costs unless hedged or passed through.

| Factor | 2024 metric | Impact |

|---|---|---|

| Land scarcity | High near hubs | Higher acquisition prices, longer cycles |

| Construction margins | Compression ~10% | Lower supplier pricing power |

| Permits | Median 12 weeks (Sweden) | Timing risk |

| Inputs | Crude ~$80/bbl; steel +10% YoY | Costs up, compresses yields |

| Critical services | SLA 3–5 yrs | Concentration risk |

What is included in the product

Concise Porter's Five Forces assessment for Corem that diagnoses competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlights strategic levers and vulnerabilities affecting Corem’s pricing, margins, and market positioning.

Corem Porter's Five Forces delivers a concise one-sheet snapshot of competitive pressures—customizable force levels and an intuitive radar chart let teams quickly diagnose threats and prioritize strategic responses.

Customers Bargaining Power

Concentrated anchor tenants

Large 3PLs, e-commerce and retail chains lease big-box logistics sites often >20,000 sqm and, by scale, secure rent concessions and tenant-improvement packages that can reduce effective rents by 10–20% versus headline rents; Amazon held ~38% of US marketplace sales in 2023, amplifying bargaining leverage. Losing a single anchor can cut site-level occupancy and NOI materially—often by 10–30%—so diversifying tenant mix reduces single-tenant leverage.

Vacancy sensitivity

Buyer power rises when market vacancy increases; by 2024 Swedish office vacancy approached ~12%, letting tenants shop comparable sites and extract larger incentives. Tenants routinely negotiate fit-out contributions and rent-free periods, pressuring landlords. In tight submarkets near hubs, landlords regain pricing power, so monitoring local absorption rates guides leasing strategy.

Customization demands

Tenants frequently demand racking, mezzanines and specialized loading, driving tenant-improvement (TI) costs that often reach tens of dollars per sq ft and can materially shift capex to landlords.

Build-to-suit transactions in 2024 embedded tenant leverage during design and leasing, increasing landlord exposure on bespoke specs and longer lease-up horizons.

Standardized specs and re-lettable designs preserve economics by limiting TI write-offs and improving remarketing to multiple users.

Switching costs

Switching costs — operational disruption, relocation expenses and re-permitting — create tenant stickiness that moderates buyer power at renewal, especially for optimized sites; in 2024 surveys about 60% of occupiers cited disruption as a primary relocation barrier and relocation often exceeds six months’ rent. Break clauses and flexible terms can offset stickiness, while proactive asset management raises renewal capture rates and lease roll-through.

- Operational disruption: ~60% cite as major barrier (2024)

- Relocation cost: often >6 months’ rent

- Re-permitting delays: months to >1 year

- Mitigants: break clauses, flexible terms, proactive asset management

ESG and green leases

Large tenants now demand measurable energy efficiency, certifications, and transparent consumption data; in 2024 the EU carbon price averaged about €100/t, raising operating scrutiny and capex for retrofits.

Compliance raises upfront capex but can enable rent premiums and lower vacancy; green leases shift OpEx via pass-throughs and performance metrics, converting buyer power into partnership value.

- Tenant demands: certifications, data transparency

- 2024 carbon price: ~€100/t (EU)

- Capex vs rent premium trade-off

- Green leases: OpEx pass-throughs, KPI-linked rents

Anchors squeeze landlords - loss can cut NOI 10-30%; vacancy rises, carbon costs surge

Customer bargaining is high: large 3PLs and e-commerce anchors (Amazon ~38% US marketplace sales 2023) extract rent concessions and TI, and losing an anchor can cut NOI 10–30%. Vacancy rose (Swedish office ~12% 2024), boosting tenant leverage; 60% cite disruption as a major relocation barrier. Energy rules matter: EU carbon ~€100/t (2024) shifts capex to landlords.

| Metric | 2024 |

|---|---|

| Anchor impact on NOI | 10–30% |

| Swedish office vacancy | ~12% |

| Occupiers citing disruption | ~60% |

| EU carbon price | ~€100/t |

Same Document Delivered

Corem Porter's Five Forces Analysis

This preview shows the exact Corem Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is the full, professionally formatted file, ready for download and use the moment you buy. You'll get this same deliverable with clear insights on competitive rivalry, supplier and buyer power, threats of substitution and entry.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Corem's Porter’s Five Forces snapshot highlights buyer and supplier leverage, competitive rivalry, entry barriers, and substitute risks shaping its profitability, offering a concise view of strategic pressures and opportunities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Corem’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce zoned land

Prime plots near transport hubs are limited in 2024, giving landowners leverage on price and terms. Competition for these sites often triggers bidding wars and option premiums, pushing acquisition prices materially higher. This elevates acquisition costs and can lengthen deal cycles by several months. Corem must secure land early and cultivate sellers to mitigate spikes and timing risk.

Fragmented contractors

The supplier base for construction and maintenance is highly fragmented, giving Corem multiple switching options and keeping supplier concentration low; public framework agreements and competitive tenders in 2024 have been shown to compress supplier margins by around 10%, capping pricing power. Specialized logistics builds with high clear heights and dock-door configurations narrow the pool of qualified vendors. For complex, bespoke projects this concentration can temporarily boost supplier influence and lead times.

Input cost volatility

Steel, concrete and energy are highly cyclical and inflation-sensitive; global crude averaged about $80/bbl in 2024 and many markets saw finished steel prices near 10% higher year‑on‑year, compressing development yields when spikes occur unless hedged or passed through. Index‑linked contracts and value engineering mitigate but rarely eliminate pressure, so timing and procurement strategy materially affect returns.

Regulatory gatekeepers

Facility services dependence

Critical services (HVAC, security, facility tech, ESG monitoring) create concentrated reliance on a few vendors, making suppliers strategically powerful; switching entails integration risk and measurable downtime. Multi-year SLAs, typically 3–5 years, can lock in terms that become unfavorable if markets shift. Dual-sourcing and strict performance KPIs rebalance bargaining power.

- Concentration risk: few specialist vendors

- SLA length: 3–5 years

- Mitigation: dual-sourcing + KPI-linked fees

Land scarcity lifts bids; crude $80, steel +10%

Supplier power is mixed: scarce prime land near hubs raises bid premiums and delays; fragmented construction suppliers compressed margins ~10% in 2024 but specialization boosts power for bespoke works and critical services with SLAs of 3–5 years. Input inflation (crude ~ $80/bbl, steel +10% YoY 2024) increases development costs unless hedged or passed through.

| Factor | 2024 metric | Impact |

|---|---|---|

| Land scarcity | High near hubs | Higher acquisition prices, longer cycles |

| Construction margins | Compression ~10% | Lower supplier pricing power |

| Permits | Median 12 weeks (Sweden) | Timing risk |

| Inputs | Crude ~$80/bbl; steel +10% YoY | Costs up, compresses yields |

| Critical services | SLA 3–5 yrs | Concentration risk |

What is included in the product

Concise Porter's Five Forces assessment for Corem that diagnoses competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlights strategic levers and vulnerabilities affecting Corem’s pricing, margins, and market positioning.

Corem Porter's Five Forces delivers a concise one-sheet snapshot of competitive pressures—customizable force levels and an intuitive radar chart let teams quickly diagnose threats and prioritize strategic responses.

Customers Bargaining Power

Concentrated anchor tenants

Large 3PLs, e-commerce and retail chains lease big-box logistics sites often >20,000 sqm and, by scale, secure rent concessions and tenant-improvement packages that can reduce effective rents by 10–20% versus headline rents; Amazon held ~38% of US marketplace sales in 2023, amplifying bargaining leverage. Losing a single anchor can cut site-level occupancy and NOI materially—often by 10–30%—so diversifying tenant mix reduces single-tenant leverage.

Vacancy sensitivity

Buyer power rises when market vacancy increases; by 2024 Swedish office vacancy approached ~12%, letting tenants shop comparable sites and extract larger incentives. Tenants routinely negotiate fit-out contributions and rent-free periods, pressuring landlords. In tight submarkets near hubs, landlords regain pricing power, so monitoring local absorption rates guides leasing strategy.

Customization demands

Tenants frequently demand racking, mezzanines and specialized loading, driving tenant-improvement (TI) costs that often reach tens of dollars per sq ft and can materially shift capex to landlords.

Build-to-suit transactions in 2024 embedded tenant leverage during design and leasing, increasing landlord exposure on bespoke specs and longer lease-up horizons.

Standardized specs and re-lettable designs preserve economics by limiting TI write-offs and improving remarketing to multiple users.

Switching costs

Switching costs — operational disruption, relocation expenses and re-permitting — create tenant stickiness that moderates buyer power at renewal, especially for optimized sites; in 2024 surveys about 60% of occupiers cited disruption as a primary relocation barrier and relocation often exceeds six months’ rent. Break clauses and flexible terms can offset stickiness, while proactive asset management raises renewal capture rates and lease roll-through.

- Operational disruption: ~60% cite as major barrier (2024)

- Relocation cost: often >6 months’ rent

- Re-permitting delays: months to >1 year

- Mitigants: break clauses, flexible terms, proactive asset management

ESG and green leases

Large tenants now demand measurable energy efficiency, certifications, and transparent consumption data; in 2024 the EU carbon price averaged about €100/t, raising operating scrutiny and capex for retrofits.

Compliance raises upfront capex but can enable rent premiums and lower vacancy; green leases shift OpEx via pass-throughs and performance metrics, converting buyer power into partnership value.

- Tenant demands: certifications, data transparency

- 2024 carbon price: ~€100/t (EU)

- Capex vs rent premium trade-off

- Green leases: OpEx pass-throughs, KPI-linked rents

Anchors squeeze landlords - loss can cut NOI 10-30%; vacancy rises, carbon costs surge

Customer bargaining is high: large 3PLs and e-commerce anchors (Amazon ~38% US marketplace sales 2023) extract rent concessions and TI, and losing an anchor can cut NOI 10–30%. Vacancy rose (Swedish office ~12% 2024), boosting tenant leverage; 60% cite disruption as a major relocation barrier. Energy rules matter: EU carbon ~€100/t (2024) shifts capex to landlords.

| Metric | 2024 |

|---|---|

| Anchor impact on NOI | 10–30% |

| Swedish office vacancy | ~12% |

| Occupiers citing disruption | ~60% |

| EU carbon price | ~€100/t |

Same Document Delivered

Corem Porter's Five Forces Analysis

This preview shows the exact Corem Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is the full, professionally formatted file, ready for download and use the moment you buy. You'll get this same deliverable with clear insights on competitive rivalry, supplier and buyer power, threats of substitution and entry.