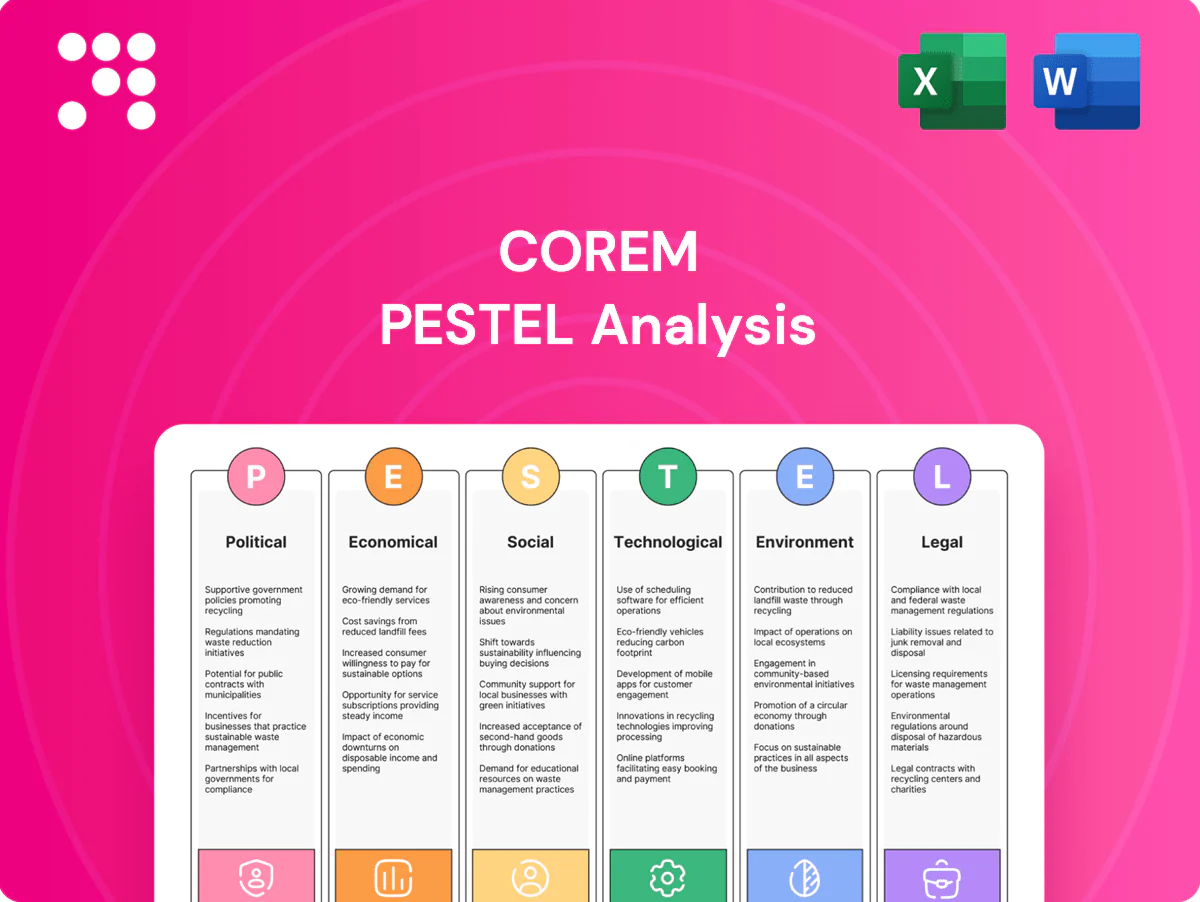

Corem PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and environmental regulations are reshaping Corem’s strategic landscape in our concise PESTLE snapshot. Packed with actionable insights, it highlights risks and growth levers investors and strategists need. Ready-made and fully editable—buy the full PESTLE analysis now to access the complete, data-driven briefing instantly.

Political factors

Urban planning and zoning priorities

National and municipal development agendas steer land-use approvals for logistics, warehousing and retail, directly affecting Corem’s ability to convert land into income-producing assets. Priority for transit-oriented and industrial zones can accelerate Corem’s pipeline and shorten delivery timelines. Political shifts may redirect growth to new corridors, and entitlement delays commonly add 6–18 months to projects. Proactive engagement with city planners reduces entitlement risk and preserves project value.

Infrastructure investment and transport policy

Public spending on roads, rail and ports (EU Connecting Europe Facility 2021–2027 at 33.7bn EUR) directly shapes site attractiveness near hubs, boosting rent and occupancy for logistics assets. Pro-logistics policies and urban consolidation can cut last-mile costs — last-mile is ~53% of delivery cost — raising asset values. Budget constraints or reallocations, common in 2024 fiscal trade-offs, can delay network upgrades. Monitoring national and regional transport masterplans guides timing and location of acquisitions.

Government incentives and regional development

Tax credits and grants for job creation, brownfield renewal or sustainability can materially lift project IRRs, supported by EU cohesion funding of about €330bn (2021–27) and the €17.5bn Just Transition Fund targeting redevelopment. Regions vying for logistics clusters often offer favorable tax or land terms; policy reversals can erase these expected uplifts. Structuring deals with clawback protections and binding incentive agreements mitigates downside.

Trade policy and geopolitical stability

Supply chains are sensitive to customs regimes, sanctions (eg post-2022 Russia measures) and rising trade friction, driving firms to reconfigure routes; stable EU single market and Nordic cooperation continue to underpin cross-border flows that sustain warehouse demand. Geopolitical shocks have already rerouted logistics corridors, altering location premiums and requiring scenario planning to align portfolio exposure.

- Supply-chain risk: customs/sanctions impact routing

- EU/Nordic stability: supports cross-border logistics

- Shocks reshape location premiums; scenario planning required

Political climate on real estate taxation

Changes to property tax, stamp duties or interest deductibility materially affect yields; in Sweden stamp duty is 1.5% for individuals and 4.25% for legal entities, while Riksbank's policy rate near 4.0% in mid‑2025 keeps financing costs elevated. Populist pressure can target commercial owners, but predictable tax regimes support long‑term value creation. Hedging via lease indexation and geographic diversification increases resilience.

- Tax impact: stamp duty 1.5%/4.25%

- Financing: policy rate ~4.0% (mid‑2025)

- Risk: populist targeting of commercial assets

- Mitigation: lease indexation, diversified geographies

Political priorities, entitlement delays and EU infrastructure lift logistics premiums

Political priorities (transit/industrial zones) and entitlement delays (6–18 months) drive Corem’s pipeline timing and value; infrastructure spend (CEF €33.7bn, Cohesion €330bn, Just Transition €17.5bn) raises logistics premiums. Trade policy, sanctions and EU/Nordic stability shape cross‑border flows; last‑mile ~53% of delivery cost. Tax changes (stamp duty 1.5%/4.25%) and Riksbank rate ~4.0% (mid‑2025) affect yields.

| Factor | Key number |

|---|---|

| Entitlement delay | 6–18 months |

| CEF (2021–27) | €33.7bn |

| Cohesion fund (2021–27) | €330bn |

| Just Transition | €17.5bn |

| Last‑mile cost | ~53% |

| Stamp duty SE | 1.5% / 4.25% |

| Policy rate (Riksbank) | ~4.0% (mid‑2025) |

What is included in the product

Explores how macro-environmental factors uniquely impact Corem across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples. Designed for executives and investors, it offers forward-looking insights and ready-to-use formatting to inform strategy, risk mitigation, and funding decisions.

A concise, visually segmented Corem PESTLE summary that’s editable and easily shareable, enabling quick alignment across teams and seamless insertion into presentations or planning sessions.

Economic factors

Interest rates and cap rates

Monetary policy drives funding costs and valuation multiples; with US Fed funds at 5.25–5.50% and the ECB deposit rate near 4.00% (mid‑2025), borrowing costs remain elevated. Rising rates have compressed development spreads and pushed commercial cap rates outward, reducing immediate transaction activity. Stabilizing or falling rates can unlock refinancing and transactions, while active asset management—leasing, re‑positioning and cost control—can offset cap‑rate expansion.

Industrial demand and e-commerce growth

E-commerce penetration in the EU reached about 16% of retail turnover in 2023, while the global 3PL market was roughly $1.3 trillion in 2023, underpinning modern warehouse absorption. A shift from just-in-time to just-in-case inventory has sustained demand for space. Retail logistics growth near population centers supports rent increases. Corem benefits from assets located close to key transport nodes in Sweden and Denmark.

Construction costs and supply pipeline

Material and labor inflation—input prices rose about 9% YoY in 2022–23—erodes development feasibility and compresses returns on Corem projects. Supply bottlenecks have delayed deliveries, tightening vacancy and supporting rents as observed in Swedish logistics/office markets with vacancy falling ~1–2 percentage points in 2023–24. Cyclical upswings raise overbuilding risk, notably where starts jump >20%. Phased development and fixed-price contracts are used to manage cost volatility.

Tenant credit and sector mix

Tenant credit quality across logistics, light industrial and retail drives cash-flow durability, with logistics and light industrial generally showing stronger rent collection and lower churn while discretionary retail remains most cyclical.

Proactive leasing, diversified covenants and rent indexation mechanisms protect NOI and reduce concentration risk during downturns.

- Tenant credit: stabilizes cash flow

- Sector mix: logistics resilient, retail cyclical

- Diversified covenants: lower concentration risk

- Leasing/indexation: protect NOI

FX and macro exposure

Operating across Nordic and EU markets means FX moves between SEK and EUR can materially affect reported returns and translated cash flows, while inflation-linked leases help preserve real rental income against rising consumer prices.

Strong GDP growth concentrated in urban regions supports continued space absorption and rental demand, and disciplined balance sheet management preserves Corem’s capacity for selective acquisitions and capex.

- FX exposure: SEK/EUR translation risk

- Inflation hedge: index-linked leases

- Demand driver: urban GDP growth sustains absorption

- Liquidity: conservative leverage enables investment

Political priorities, entitlement delays and EU infrastructure lift logistics premiums

Monetary tightening (US Fed 5.25–5.50% & ECB ~4.00% mid‑2025) keeps cap rates elevated but stabilizing rates could unlock refinancing; e‑commerce (EU ~16% of retail 2023) and a $1.3T global 3PL market (2023) sustain logistics demand. Input costs rose ~9% YoY (2022–23), tightening development feasibility; vacancy in Nordic logistics fell ~1–2pp (2023–24), supporting rents and NOI protection via indexation.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| ECB deposit (mid‑2025) | ~4.00% |

| EU e‑commerce (2023) | ~16% |

| Global 3PL (2023) | $1.3T |

| Input price change (2022–23) | +~9% YoY |

| Nordic logistics vacancy (2023–24) | -1–2 pp |

Same Document Delivered

Corem PESTLE Analysis

The preview shown here is the exact Corem PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and visuals in this preview are the final version; there are no placeholders or hidden sections. After payment you’ll instantly download the same professionally structured file displayed here.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and environmental regulations are reshaping Corem’s strategic landscape in our concise PESTLE snapshot. Packed with actionable insights, it highlights risks and growth levers investors and strategists need. Ready-made and fully editable—buy the full PESTLE analysis now to access the complete, data-driven briefing instantly.

Political factors

Urban planning and zoning priorities

National and municipal development agendas steer land-use approvals for logistics, warehousing and retail, directly affecting Corem’s ability to convert land into income-producing assets. Priority for transit-oriented and industrial zones can accelerate Corem’s pipeline and shorten delivery timelines. Political shifts may redirect growth to new corridors, and entitlement delays commonly add 6–18 months to projects. Proactive engagement with city planners reduces entitlement risk and preserves project value.

Infrastructure investment and transport policy

Public spending on roads, rail and ports (EU Connecting Europe Facility 2021–2027 at 33.7bn EUR) directly shapes site attractiveness near hubs, boosting rent and occupancy for logistics assets. Pro-logistics policies and urban consolidation can cut last-mile costs — last-mile is ~53% of delivery cost — raising asset values. Budget constraints or reallocations, common in 2024 fiscal trade-offs, can delay network upgrades. Monitoring national and regional transport masterplans guides timing and location of acquisitions.

Government incentives and regional development

Tax credits and grants for job creation, brownfield renewal or sustainability can materially lift project IRRs, supported by EU cohesion funding of about €330bn (2021–27) and the €17.5bn Just Transition Fund targeting redevelopment. Regions vying for logistics clusters often offer favorable tax or land terms; policy reversals can erase these expected uplifts. Structuring deals with clawback protections and binding incentive agreements mitigates downside.

Trade policy and geopolitical stability

Supply chains are sensitive to customs regimes, sanctions (eg post-2022 Russia measures) and rising trade friction, driving firms to reconfigure routes; stable EU single market and Nordic cooperation continue to underpin cross-border flows that sustain warehouse demand. Geopolitical shocks have already rerouted logistics corridors, altering location premiums and requiring scenario planning to align portfolio exposure.

- Supply-chain risk: customs/sanctions impact routing

- EU/Nordic stability: supports cross-border logistics

- Shocks reshape location premiums; scenario planning required

Political climate on real estate taxation

Changes to property tax, stamp duties or interest deductibility materially affect yields; in Sweden stamp duty is 1.5% for individuals and 4.25% for legal entities, while Riksbank's policy rate near 4.0% in mid‑2025 keeps financing costs elevated. Populist pressure can target commercial owners, but predictable tax regimes support long‑term value creation. Hedging via lease indexation and geographic diversification increases resilience.

- Tax impact: stamp duty 1.5%/4.25%

- Financing: policy rate ~4.0% (mid‑2025)

- Risk: populist targeting of commercial assets

- Mitigation: lease indexation, diversified geographies

Political priorities, entitlement delays and EU infrastructure lift logistics premiums

Political priorities (transit/industrial zones) and entitlement delays (6–18 months) drive Corem’s pipeline timing and value; infrastructure spend (CEF €33.7bn, Cohesion €330bn, Just Transition €17.5bn) raises logistics premiums. Trade policy, sanctions and EU/Nordic stability shape cross‑border flows; last‑mile ~53% of delivery cost. Tax changes (stamp duty 1.5%/4.25%) and Riksbank rate ~4.0% (mid‑2025) affect yields.

| Factor | Key number |

|---|---|

| Entitlement delay | 6–18 months |

| CEF (2021–27) | €33.7bn |

| Cohesion fund (2021–27) | €330bn |

| Just Transition | €17.5bn |

| Last‑mile cost | ~53% |

| Stamp duty SE | 1.5% / 4.25% |

| Policy rate (Riksbank) | ~4.0% (mid‑2025) |

What is included in the product

Explores how macro-environmental factors uniquely impact Corem across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples. Designed for executives and investors, it offers forward-looking insights and ready-to-use formatting to inform strategy, risk mitigation, and funding decisions.

A concise, visually segmented Corem PESTLE summary that’s editable and easily shareable, enabling quick alignment across teams and seamless insertion into presentations or planning sessions.

Economic factors

Interest rates and cap rates

Monetary policy drives funding costs and valuation multiples; with US Fed funds at 5.25–5.50% and the ECB deposit rate near 4.00% (mid‑2025), borrowing costs remain elevated. Rising rates have compressed development spreads and pushed commercial cap rates outward, reducing immediate transaction activity. Stabilizing or falling rates can unlock refinancing and transactions, while active asset management—leasing, re‑positioning and cost control—can offset cap‑rate expansion.

Industrial demand and e-commerce growth

E-commerce penetration in the EU reached about 16% of retail turnover in 2023, while the global 3PL market was roughly $1.3 trillion in 2023, underpinning modern warehouse absorption. A shift from just-in-time to just-in-case inventory has sustained demand for space. Retail logistics growth near population centers supports rent increases. Corem benefits from assets located close to key transport nodes in Sweden and Denmark.

Construction costs and supply pipeline

Material and labor inflation—input prices rose about 9% YoY in 2022–23—erodes development feasibility and compresses returns on Corem projects. Supply bottlenecks have delayed deliveries, tightening vacancy and supporting rents as observed in Swedish logistics/office markets with vacancy falling ~1–2 percentage points in 2023–24. Cyclical upswings raise overbuilding risk, notably where starts jump >20%. Phased development and fixed-price contracts are used to manage cost volatility.

Tenant credit and sector mix

Tenant credit quality across logistics, light industrial and retail drives cash-flow durability, with logistics and light industrial generally showing stronger rent collection and lower churn while discretionary retail remains most cyclical.

Proactive leasing, diversified covenants and rent indexation mechanisms protect NOI and reduce concentration risk during downturns.

- Tenant credit: stabilizes cash flow

- Sector mix: logistics resilient, retail cyclical

- Diversified covenants: lower concentration risk

- Leasing/indexation: protect NOI

FX and macro exposure

Operating across Nordic and EU markets means FX moves between SEK and EUR can materially affect reported returns and translated cash flows, while inflation-linked leases help preserve real rental income against rising consumer prices.

Strong GDP growth concentrated in urban regions supports continued space absorption and rental demand, and disciplined balance sheet management preserves Corem’s capacity for selective acquisitions and capex.

- FX exposure: SEK/EUR translation risk

- Inflation hedge: index-linked leases

- Demand driver: urban GDP growth sustains absorption

- Liquidity: conservative leverage enables investment

Political priorities, entitlement delays and EU infrastructure lift logistics premiums

Monetary tightening (US Fed 5.25–5.50% & ECB ~4.00% mid‑2025) keeps cap rates elevated but stabilizing rates could unlock refinancing; e‑commerce (EU ~16% of retail 2023) and a $1.3T global 3PL market (2023) sustain logistics demand. Input costs rose ~9% YoY (2022–23), tightening development feasibility; vacancy in Nordic logistics fell ~1–2pp (2023–24), supporting rents and NOI protection via indexation.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| ECB deposit (mid‑2025) | ~4.00% |

| EU e‑commerce (2023) | ~16% |

| Global 3PL (2023) | $1.3T |

| Input price change (2022–23) | +~9% YoY |

| Nordic logistics vacancy (2023–24) | -1–2 pp |

Same Document Delivered

Corem PESTLE Analysis

The preview shown here is the exact Corem PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and visuals in this preview are the final version; there are no placeholders or hidden sections. After payment you’ll instantly download the same professionally structured file displayed here.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and environmental regulations are reshaping Corem’s strategic landscape in our concise PESTLE snapshot. Packed with actionable insights, it highlights risks and growth levers investors and strategists need. Ready-made and fully editable—buy the full PESTLE analysis now to access the complete, data-driven briefing instantly.

Political factors

Urban planning and zoning priorities

National and municipal development agendas steer land-use approvals for logistics, warehousing and retail, directly affecting Corem’s ability to convert land into income-producing assets. Priority for transit-oriented and industrial zones can accelerate Corem’s pipeline and shorten delivery timelines. Political shifts may redirect growth to new corridors, and entitlement delays commonly add 6–18 months to projects. Proactive engagement with city planners reduces entitlement risk and preserves project value.

Infrastructure investment and transport policy

Public spending on roads, rail and ports (EU Connecting Europe Facility 2021–2027 at 33.7bn EUR) directly shapes site attractiveness near hubs, boosting rent and occupancy for logistics assets. Pro-logistics policies and urban consolidation can cut last-mile costs — last-mile is ~53% of delivery cost — raising asset values. Budget constraints or reallocations, common in 2024 fiscal trade-offs, can delay network upgrades. Monitoring national and regional transport masterplans guides timing and location of acquisitions.

Government incentives and regional development

Tax credits and grants for job creation, brownfield renewal or sustainability can materially lift project IRRs, supported by EU cohesion funding of about €330bn (2021–27) and the €17.5bn Just Transition Fund targeting redevelopment. Regions vying for logistics clusters often offer favorable tax or land terms; policy reversals can erase these expected uplifts. Structuring deals with clawback protections and binding incentive agreements mitigates downside.

Trade policy and geopolitical stability

Supply chains are sensitive to customs regimes, sanctions (eg post-2022 Russia measures) and rising trade friction, driving firms to reconfigure routes; stable EU single market and Nordic cooperation continue to underpin cross-border flows that sustain warehouse demand. Geopolitical shocks have already rerouted logistics corridors, altering location premiums and requiring scenario planning to align portfolio exposure.

- Supply-chain risk: customs/sanctions impact routing

- EU/Nordic stability: supports cross-border logistics

- Shocks reshape location premiums; scenario planning required

Political climate on real estate taxation

Changes to property tax, stamp duties or interest deductibility materially affect yields; in Sweden stamp duty is 1.5% for individuals and 4.25% for legal entities, while Riksbank's policy rate near 4.0% in mid‑2025 keeps financing costs elevated. Populist pressure can target commercial owners, but predictable tax regimes support long‑term value creation. Hedging via lease indexation and geographic diversification increases resilience.

- Tax impact: stamp duty 1.5%/4.25%

- Financing: policy rate ~4.0% (mid‑2025)

- Risk: populist targeting of commercial assets

- Mitigation: lease indexation, diversified geographies

Political priorities, entitlement delays and EU infrastructure lift logistics premiums

Political priorities (transit/industrial zones) and entitlement delays (6–18 months) drive Corem’s pipeline timing and value; infrastructure spend (CEF €33.7bn, Cohesion €330bn, Just Transition €17.5bn) raises logistics premiums. Trade policy, sanctions and EU/Nordic stability shape cross‑border flows; last‑mile ~53% of delivery cost. Tax changes (stamp duty 1.5%/4.25%) and Riksbank rate ~4.0% (mid‑2025) affect yields.

| Factor | Key number |

|---|---|

| Entitlement delay | 6–18 months |

| CEF (2021–27) | €33.7bn |

| Cohesion fund (2021–27) | €330bn |

| Just Transition | €17.5bn |

| Last‑mile cost | ~53% |

| Stamp duty SE | 1.5% / 4.25% |

| Policy rate (Riksbank) | ~4.0% (mid‑2025) |

What is included in the product

Explores how macro-environmental factors uniquely impact Corem across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples. Designed for executives and investors, it offers forward-looking insights and ready-to-use formatting to inform strategy, risk mitigation, and funding decisions.

A concise, visually segmented Corem PESTLE summary that’s editable and easily shareable, enabling quick alignment across teams and seamless insertion into presentations or planning sessions.

Economic factors

Interest rates and cap rates

Monetary policy drives funding costs and valuation multiples; with US Fed funds at 5.25–5.50% and the ECB deposit rate near 4.00% (mid‑2025), borrowing costs remain elevated. Rising rates have compressed development spreads and pushed commercial cap rates outward, reducing immediate transaction activity. Stabilizing or falling rates can unlock refinancing and transactions, while active asset management—leasing, re‑positioning and cost control—can offset cap‑rate expansion.

Industrial demand and e-commerce growth

E-commerce penetration in the EU reached about 16% of retail turnover in 2023, while the global 3PL market was roughly $1.3 trillion in 2023, underpinning modern warehouse absorption. A shift from just-in-time to just-in-case inventory has sustained demand for space. Retail logistics growth near population centers supports rent increases. Corem benefits from assets located close to key transport nodes in Sweden and Denmark.

Construction costs and supply pipeline

Material and labor inflation—input prices rose about 9% YoY in 2022–23—erodes development feasibility and compresses returns on Corem projects. Supply bottlenecks have delayed deliveries, tightening vacancy and supporting rents as observed in Swedish logistics/office markets with vacancy falling ~1–2 percentage points in 2023–24. Cyclical upswings raise overbuilding risk, notably where starts jump >20%. Phased development and fixed-price contracts are used to manage cost volatility.

Tenant credit and sector mix

Tenant credit quality across logistics, light industrial and retail drives cash-flow durability, with logistics and light industrial generally showing stronger rent collection and lower churn while discretionary retail remains most cyclical.

Proactive leasing, diversified covenants and rent indexation mechanisms protect NOI and reduce concentration risk during downturns.

- Tenant credit: stabilizes cash flow

- Sector mix: logistics resilient, retail cyclical

- Diversified covenants: lower concentration risk

- Leasing/indexation: protect NOI

FX and macro exposure

Operating across Nordic and EU markets means FX moves between SEK and EUR can materially affect reported returns and translated cash flows, while inflation-linked leases help preserve real rental income against rising consumer prices.

Strong GDP growth concentrated in urban regions supports continued space absorption and rental demand, and disciplined balance sheet management preserves Corem’s capacity for selective acquisitions and capex.

- FX exposure: SEK/EUR translation risk

- Inflation hedge: index-linked leases

- Demand driver: urban GDP growth sustains absorption

- Liquidity: conservative leverage enables investment

Political priorities, entitlement delays and EU infrastructure lift logistics premiums

Monetary tightening (US Fed 5.25–5.50% & ECB ~4.00% mid‑2025) keeps cap rates elevated but stabilizing rates could unlock refinancing; e‑commerce (EU ~16% of retail 2023) and a $1.3T global 3PL market (2023) sustain logistics demand. Input costs rose ~9% YoY (2022–23), tightening development feasibility; vacancy in Nordic logistics fell ~1–2pp (2023–24), supporting rents and NOI protection via indexation.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| ECB deposit (mid‑2025) | ~4.00% |

| EU e‑commerce (2023) | ~16% |

| Global 3PL (2023) | $1.3T |

| Input price change (2022–23) | +~9% YoY |

| Nordic logistics vacancy (2023–24) | -1–2 pp |

Same Document Delivered

Corem PESTLE Analysis

The preview shown here is the exact Corem PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and visuals in this preview are the final version; there are no placeholders or hidden sections. After payment you’ll instantly download the same professionally structured file displayed here.