Core Molding Technologies Porter's Five Forces Analysis

Don't Miss the Bigger Picture

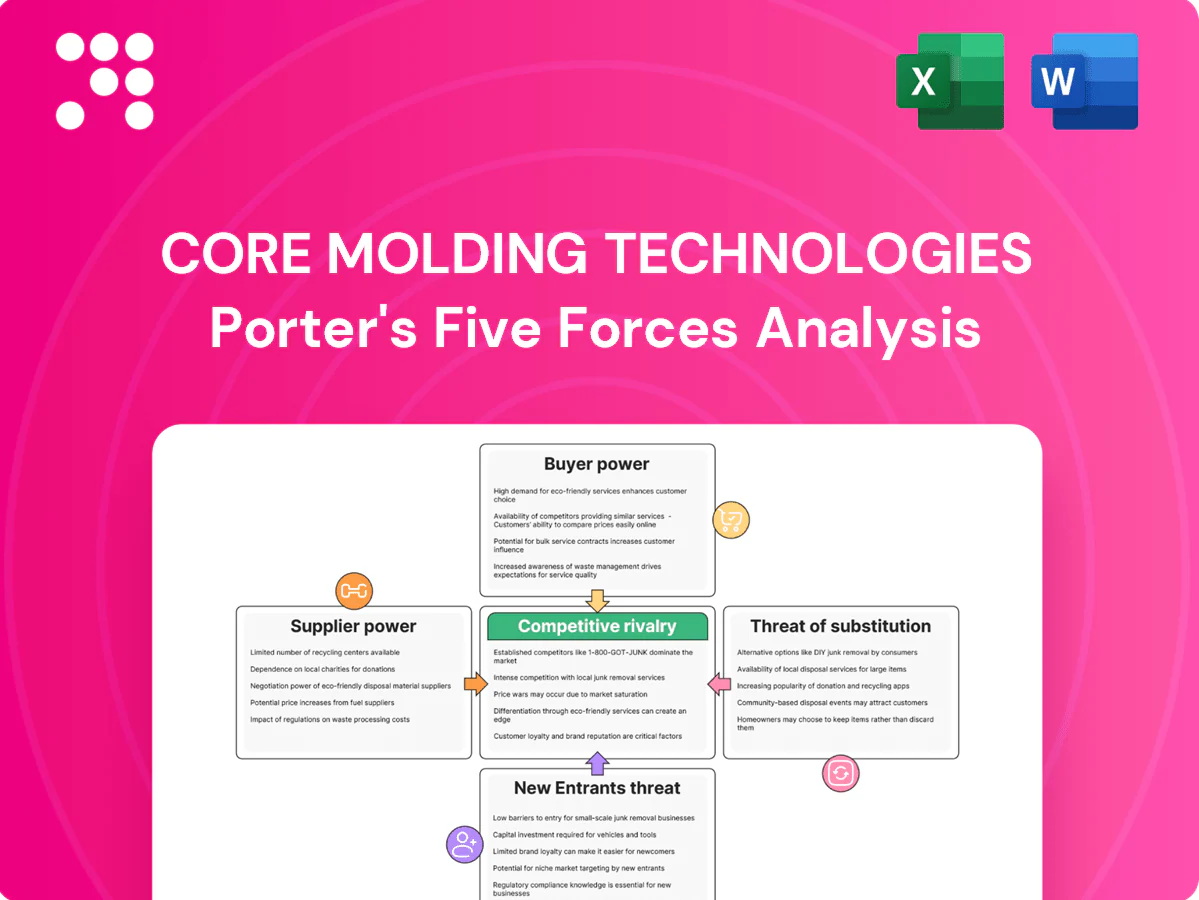

Core Molding Technologies faces moderate supplier power, niche customer segments with bargaining leverage, and steady rivalry from regional molders; threat of new entrants is limited by capital and expertise requirements while substitutes are sector-specific. This snapshot highlights key pressures shaping CMT’s strategy. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights for investment or strategic planning.

Suppliers Bargaining Power

Resin and glass concentration

Core relies on a concentrated set of suppliers for polyester/vinyl ester resins and fiberglass reinforcements; the top global petrochemical and glass-fiber players control around half of capacity, giving them pricing and allocation power. Resin prices surged roughly 30% in 2021–22 and stayed elevated into 2023–24, increasing surcharge and lead-time volatility. Multi-sourcing mitigates risk but true substitutes for spec’d materials remain limited.

Qualification switching costs

Switching materials or suppliers requires requalification, PPAP submissions and OEM customer approvals, often involving PPAP level 3 documentation and dimensional/process studies. Validation cycles for safety‑critical or aesthetic parts commonly run 3–12 months, creating technical and time costs that give incumbents negotiation leverage. That lock‑in has translated into less favorable terms and extended lead times during supply shocks (eg 2021–22 global disruptions).

Petrochemical price pass-through

Resin pricing closely tracks crude and derivatives—Brent averaged about $86/bbl in 2024—so suppliers frequently attempt pass-throughs, squeezing OEM margins when contracts lack indexing. Suppliers historically raise prices faster than they cut them, leading to short-term margin compression. Hedging and indexed contracts reduce volatility exposure but do not eliminate it, leaving residual margin risk.

Tooling and equipment lock-in

Presses, RTM equipment and tooling systems create dependence on a handful of OEMs (eg Dieffenbacher, Siempelkamp) and specialized service providers; proprietary components and multi-year maintenance agreements raise switching costs, while long lead times for large presses (6–12 months) and molds (4–9 months) in 2024 constrain operational flexibility and shift bargaining power toward equipment suppliers.

- Concentration: limited OEM pool

- Switching costs: proprietary parts + maintenance contracts

- Lead times 2024: presses 6–12 months, molds 4–9 months

- Net effect: supplier-side bargaining power ↑

Logistics and EHS constraints

Logistics and EHS constraints—hazmat handling, styrene emission controls and refrigeration for SMC/resins—shrink the supplier pool and raise switching costs; 2024 global container schedule reliability was about 41%, so regional disruptions or port delays can quickly halt production.

Strict compliance underpins supplier leverage: vendors certifying proper hazmat handling, emission mitigation and cold-chain services command premiums and can charge 8–12% higher rates for guaranteed, compliant deliveries in 2024.

- Hazmat handling limits vendors

- Styrene emissions require controls

- Refrigeration adds cold-chain cost

- 41% container schedule reliability (2024)

- Compliant delivery premium ~8–12% (2024)

Supplier power tight as resin costs rose 30% and Brent $86

Supplier power is high due to concentration in resins/fiberglass, long equipment/tooling lead times and costly requalification, which lock in buyers and allow price pass-throughs. Resin costs jumped ~30% in 2021–22 and remained elevated into 2024 with Brent ~86/bbl, compressing OEM margins. Logistics/EHS limits (41% container reliability) and compliant-delivery premiums (8–12%) further strengthen suppliers.

| Metric | 2024 value |

|---|---|

| Brent | $86/bbl |

| Press lead time | 6–12 months |

| Mold lead time | 4–9 months |

| Container reliability | 41% |

| Compliant premium | 8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Core Molding Technologies revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share, with actionable insights on disruptive trends and entry barriers.

A concise one-sheet Porter's Five Forces for Core Molding Technologies—clarifies supplier, buyer, entrant and substitute pressures and competitive rivalry for faster strategic decisions and pitch-ready slides.

Customers Bargaining Power

Concentrated OEM base

Medium/heavy truck, marine and powersports OEMs are few but large, with U.S. Class 8 production near 250,000 units in 2024, concentrating buying power. Their volume scale and procurement sophistication give strong negotiating leverage, enabling consolidated award strategies and routine price concessions. Losing a single key account can materially reduce facility utilization and margins for suppliers like Core Molding.

Program-driven pricing

In 2024, RFQ-driven multi-year programs for Core Molding are won with explicit competitive price-down expectations and commonly use should-cost models and open-book discussions to validate targets. Indexing to resin and glass mitigates raw-material swings, but buyers still press for productivity givebacks. Renewal decisions hinge on meeting cost, quality and delivery KPIs.

Switching and tooling dynamics

Buyers face non-trivial switching costs—tooling typically ranges from $0.5–2.0M per cavity and PPAP/validation often takes 3–12 months—so mid‑program leverage for OEMs is limited. At redesigns or new platforms buyers can rebid aggressively; dual‑sourcing (used in roughly 40% of programs) keeps price/quality pressure on incumbents. OEM ownership of tooling further increases supplier mobility and rebid flexibility.

Cyclicality and volume leverage

Cyclicality of end-markets means buyers push for price relief and flexible MOQs in downturns while upcycles create allocation risk that shifts leverage back to customers; in 2024 U.S. light-vehicle production was roughly 13.5 million units (IHS Markit estimate), amplifying volume swings. Volume commitments can lock pricing but transfer inventory risk to the molder, and forecast accuracy has become a key negotiation fulcrum.

- Downturn pressure: lower prices, flexible MOQs

- Upcycle risk: allocation restores buyer leverage

- Volume deals: secure pricing, raise molder inventory risk

- Forecasts: accuracy drives contract terms and penalties

Co-development stickiness

Early design engagement (DFM, material selection, tooling) raises switching frictions by embedding CMT into product lifecycles, enabling engineering value-add that supports premium pricing and share protection. Buyers still benchmark alternatives, but 2024 industry surveys found integration benefits cited as a primary barrier to rapid switching. Performance warranties and joint tooling investments further bind relationships.

- DFM-led stickiness

- Premium justification

- Benchmarking persists

- Warranties bind

OEM concentration boosts buyer leverage — US Class 8 ≈250,000, dual-sourcing ~40%

OEM concentration gives buyers strong leverage—US Class 8 ≈250,000 units in 2024—driving RFQ price-downs and should-cost tactics. Dual-sourcing (~40% of programs) and resin/glass indexing sustain pressure despite mid-program switching frictions. Tooling $0.5–2.0M/cavity and PPAP 3–12 months raise costs; US light-vehicle ≈13.5M units in 2024 amplifies cyclic leverage.

| Metric | 2024 Value |

|---|---|

| US Class 8 | ~250,000 units |

| US light-vehicle | ~13.5M units |

| Dual-sourcing rate | ~40% |

| Tooling cost | $0.5–2.0M/cavity |

Full Version Awaits

Core Molding Technologies Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Core Molding Technologies you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis ready for download and use the moment you buy. You're looking at the actual deliverable; instant access is granted upon payment.

Don't Miss the Bigger Picture

Core Molding Technologies faces moderate supplier power, niche customer segments with bargaining leverage, and steady rivalry from regional molders; threat of new entrants is limited by capital and expertise requirements while substitutes are sector-specific. This snapshot highlights key pressures shaping CMT’s strategy. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights for investment or strategic planning.

Suppliers Bargaining Power

Resin and glass concentration

Core relies on a concentrated set of suppliers for polyester/vinyl ester resins and fiberglass reinforcements; the top global petrochemical and glass-fiber players control around half of capacity, giving them pricing and allocation power. Resin prices surged roughly 30% in 2021–22 and stayed elevated into 2023–24, increasing surcharge and lead-time volatility. Multi-sourcing mitigates risk but true substitutes for spec’d materials remain limited.

Qualification switching costs

Switching materials or suppliers requires requalification, PPAP submissions and OEM customer approvals, often involving PPAP level 3 documentation and dimensional/process studies. Validation cycles for safety‑critical or aesthetic parts commonly run 3–12 months, creating technical and time costs that give incumbents negotiation leverage. That lock‑in has translated into less favorable terms and extended lead times during supply shocks (eg 2021–22 global disruptions).

Petrochemical price pass-through

Resin pricing closely tracks crude and derivatives—Brent averaged about $86/bbl in 2024—so suppliers frequently attempt pass-throughs, squeezing OEM margins when contracts lack indexing. Suppliers historically raise prices faster than they cut them, leading to short-term margin compression. Hedging and indexed contracts reduce volatility exposure but do not eliminate it, leaving residual margin risk.

Tooling and equipment lock-in

Presses, RTM equipment and tooling systems create dependence on a handful of OEMs (eg Dieffenbacher, Siempelkamp) and specialized service providers; proprietary components and multi-year maintenance agreements raise switching costs, while long lead times for large presses (6–12 months) and molds (4–9 months) in 2024 constrain operational flexibility and shift bargaining power toward equipment suppliers.

- Concentration: limited OEM pool

- Switching costs: proprietary parts + maintenance contracts

- Lead times 2024: presses 6–12 months, molds 4–9 months

- Net effect: supplier-side bargaining power ↑

Logistics and EHS constraints

Logistics and EHS constraints—hazmat handling, styrene emission controls and refrigeration for SMC/resins—shrink the supplier pool and raise switching costs; 2024 global container schedule reliability was about 41%, so regional disruptions or port delays can quickly halt production.

Strict compliance underpins supplier leverage: vendors certifying proper hazmat handling, emission mitigation and cold-chain services command premiums and can charge 8–12% higher rates for guaranteed, compliant deliveries in 2024.

- Hazmat handling limits vendors

- Styrene emissions require controls

- Refrigeration adds cold-chain cost

- 41% container schedule reliability (2024)

- Compliant delivery premium ~8–12% (2024)

Supplier power tight as resin costs rose 30% and Brent $86

Supplier power is high due to concentration in resins/fiberglass, long equipment/tooling lead times and costly requalification, which lock in buyers and allow price pass-throughs. Resin costs jumped ~30% in 2021–22 and remained elevated into 2024 with Brent ~86/bbl, compressing OEM margins. Logistics/EHS limits (41% container reliability) and compliant-delivery premiums (8–12%) further strengthen suppliers.

| Metric | 2024 value |

|---|---|

| Brent | $86/bbl |

| Press lead time | 6–12 months |

| Mold lead time | 4–9 months |

| Container reliability | 41% |

| Compliant premium | 8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Core Molding Technologies revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share, with actionable insights on disruptive trends and entry barriers.

A concise one-sheet Porter's Five Forces for Core Molding Technologies—clarifies supplier, buyer, entrant and substitute pressures and competitive rivalry for faster strategic decisions and pitch-ready slides.

Customers Bargaining Power

Concentrated OEM base

Medium/heavy truck, marine and powersports OEMs are few but large, with U.S. Class 8 production near 250,000 units in 2024, concentrating buying power. Their volume scale and procurement sophistication give strong negotiating leverage, enabling consolidated award strategies and routine price concessions. Losing a single key account can materially reduce facility utilization and margins for suppliers like Core Molding.

Program-driven pricing

In 2024, RFQ-driven multi-year programs for Core Molding are won with explicit competitive price-down expectations and commonly use should-cost models and open-book discussions to validate targets. Indexing to resin and glass mitigates raw-material swings, but buyers still press for productivity givebacks. Renewal decisions hinge on meeting cost, quality and delivery KPIs.

Switching and tooling dynamics

Buyers face non-trivial switching costs—tooling typically ranges from $0.5–2.0M per cavity and PPAP/validation often takes 3–12 months—so mid‑program leverage for OEMs is limited. At redesigns or new platforms buyers can rebid aggressively; dual‑sourcing (used in roughly 40% of programs) keeps price/quality pressure on incumbents. OEM ownership of tooling further increases supplier mobility and rebid flexibility.

Cyclicality and volume leverage

Cyclicality of end-markets means buyers push for price relief and flexible MOQs in downturns while upcycles create allocation risk that shifts leverage back to customers; in 2024 U.S. light-vehicle production was roughly 13.5 million units (IHS Markit estimate), amplifying volume swings. Volume commitments can lock pricing but transfer inventory risk to the molder, and forecast accuracy has become a key negotiation fulcrum.

- Downturn pressure: lower prices, flexible MOQs

- Upcycle risk: allocation restores buyer leverage

- Volume deals: secure pricing, raise molder inventory risk

- Forecasts: accuracy drives contract terms and penalties

Co-development stickiness

Early design engagement (DFM, material selection, tooling) raises switching frictions by embedding CMT into product lifecycles, enabling engineering value-add that supports premium pricing and share protection. Buyers still benchmark alternatives, but 2024 industry surveys found integration benefits cited as a primary barrier to rapid switching. Performance warranties and joint tooling investments further bind relationships.

- DFM-led stickiness

- Premium justification

- Benchmarking persists

- Warranties bind

OEM concentration boosts buyer leverage — US Class 8 ≈250,000, dual-sourcing ~40%

OEM concentration gives buyers strong leverage—US Class 8 ≈250,000 units in 2024—driving RFQ price-downs and should-cost tactics. Dual-sourcing (~40% of programs) and resin/glass indexing sustain pressure despite mid-program switching frictions. Tooling $0.5–2.0M/cavity and PPAP 3–12 months raise costs; US light-vehicle ≈13.5M units in 2024 amplifies cyclic leverage.

| Metric | 2024 Value |

|---|---|

| US Class 8 | ~250,000 units |

| US light-vehicle | ~13.5M units |

| Dual-sourcing rate | ~40% |

| Tooling cost | $0.5–2.0M/cavity |

Full Version Awaits

Core Molding Technologies Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Core Molding Technologies you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis ready for download and use the moment you buy. You're looking at the actual deliverable; instant access is granted upon payment.

Description

Don't Miss the Bigger Picture

Core Molding Technologies faces moderate supplier power, niche customer segments with bargaining leverage, and steady rivalry from regional molders; threat of new entrants is limited by capital and expertise requirements while substitutes are sector-specific. This snapshot highlights key pressures shaping CMT’s strategy. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights for investment or strategic planning.

Suppliers Bargaining Power

Resin and glass concentration

Core relies on a concentrated set of suppliers for polyester/vinyl ester resins and fiberglass reinforcements; the top global petrochemical and glass-fiber players control around half of capacity, giving them pricing and allocation power. Resin prices surged roughly 30% in 2021–22 and stayed elevated into 2023–24, increasing surcharge and lead-time volatility. Multi-sourcing mitigates risk but true substitutes for spec’d materials remain limited.

Qualification switching costs

Switching materials or suppliers requires requalification, PPAP submissions and OEM customer approvals, often involving PPAP level 3 documentation and dimensional/process studies. Validation cycles for safety‑critical or aesthetic parts commonly run 3–12 months, creating technical and time costs that give incumbents negotiation leverage. That lock‑in has translated into less favorable terms and extended lead times during supply shocks (eg 2021–22 global disruptions).

Petrochemical price pass-through

Resin pricing closely tracks crude and derivatives—Brent averaged about $86/bbl in 2024—so suppliers frequently attempt pass-throughs, squeezing OEM margins when contracts lack indexing. Suppliers historically raise prices faster than they cut them, leading to short-term margin compression. Hedging and indexed contracts reduce volatility exposure but do not eliminate it, leaving residual margin risk.

Tooling and equipment lock-in

Presses, RTM equipment and tooling systems create dependence on a handful of OEMs (eg Dieffenbacher, Siempelkamp) and specialized service providers; proprietary components and multi-year maintenance agreements raise switching costs, while long lead times for large presses (6–12 months) and molds (4–9 months) in 2024 constrain operational flexibility and shift bargaining power toward equipment suppliers.

- Concentration: limited OEM pool

- Switching costs: proprietary parts + maintenance contracts

- Lead times 2024: presses 6–12 months, molds 4–9 months

- Net effect: supplier-side bargaining power ↑

Logistics and EHS constraints

Logistics and EHS constraints—hazmat handling, styrene emission controls and refrigeration for SMC/resins—shrink the supplier pool and raise switching costs; 2024 global container schedule reliability was about 41%, so regional disruptions or port delays can quickly halt production.

Strict compliance underpins supplier leverage: vendors certifying proper hazmat handling, emission mitigation and cold-chain services command premiums and can charge 8–12% higher rates for guaranteed, compliant deliveries in 2024.

- Hazmat handling limits vendors

- Styrene emissions require controls

- Refrigeration adds cold-chain cost

- 41% container schedule reliability (2024)

- Compliant delivery premium ~8–12% (2024)

Supplier power tight as resin costs rose 30% and Brent $86

Supplier power is high due to concentration in resins/fiberglass, long equipment/tooling lead times and costly requalification, which lock in buyers and allow price pass-throughs. Resin costs jumped ~30% in 2021–22 and remained elevated into 2024 with Brent ~86/bbl, compressing OEM margins. Logistics/EHS limits (41% container reliability) and compliant-delivery premiums (8–12%) further strengthen suppliers.

| Metric | 2024 value |

|---|---|

| Brent | $86/bbl |

| Press lead time | 6–12 months |

| Mold lead time | 4–9 months |

| Container reliability | 41% |

| Compliant premium | 8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Core Molding Technologies revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share, with actionable insights on disruptive trends and entry barriers.

A concise one-sheet Porter's Five Forces for Core Molding Technologies—clarifies supplier, buyer, entrant and substitute pressures and competitive rivalry for faster strategic decisions and pitch-ready slides.

Customers Bargaining Power

Concentrated OEM base

Medium/heavy truck, marine and powersports OEMs are few but large, with U.S. Class 8 production near 250,000 units in 2024, concentrating buying power. Their volume scale and procurement sophistication give strong negotiating leverage, enabling consolidated award strategies and routine price concessions. Losing a single key account can materially reduce facility utilization and margins for suppliers like Core Molding.

Program-driven pricing

In 2024, RFQ-driven multi-year programs for Core Molding are won with explicit competitive price-down expectations and commonly use should-cost models and open-book discussions to validate targets. Indexing to resin and glass mitigates raw-material swings, but buyers still press for productivity givebacks. Renewal decisions hinge on meeting cost, quality and delivery KPIs.

Switching and tooling dynamics

Buyers face non-trivial switching costs—tooling typically ranges from $0.5–2.0M per cavity and PPAP/validation often takes 3–12 months—so mid‑program leverage for OEMs is limited. At redesigns or new platforms buyers can rebid aggressively; dual‑sourcing (used in roughly 40% of programs) keeps price/quality pressure on incumbents. OEM ownership of tooling further increases supplier mobility and rebid flexibility.

Cyclicality and volume leverage

Cyclicality of end-markets means buyers push for price relief and flexible MOQs in downturns while upcycles create allocation risk that shifts leverage back to customers; in 2024 U.S. light-vehicle production was roughly 13.5 million units (IHS Markit estimate), amplifying volume swings. Volume commitments can lock pricing but transfer inventory risk to the molder, and forecast accuracy has become a key negotiation fulcrum.

- Downturn pressure: lower prices, flexible MOQs

- Upcycle risk: allocation restores buyer leverage

- Volume deals: secure pricing, raise molder inventory risk

- Forecasts: accuracy drives contract terms and penalties

Co-development stickiness

Early design engagement (DFM, material selection, tooling) raises switching frictions by embedding CMT into product lifecycles, enabling engineering value-add that supports premium pricing and share protection. Buyers still benchmark alternatives, but 2024 industry surveys found integration benefits cited as a primary barrier to rapid switching. Performance warranties and joint tooling investments further bind relationships.

- DFM-led stickiness

- Premium justification

- Benchmarking persists

- Warranties bind

OEM concentration boosts buyer leverage — US Class 8 ≈250,000, dual-sourcing ~40%

OEM concentration gives buyers strong leverage—US Class 8 ≈250,000 units in 2024—driving RFQ price-downs and should-cost tactics. Dual-sourcing (~40% of programs) and resin/glass indexing sustain pressure despite mid-program switching frictions. Tooling $0.5–2.0M/cavity and PPAP 3–12 months raise costs; US light-vehicle ≈13.5M units in 2024 amplifies cyclic leverage.

| Metric | 2024 Value |

|---|---|

| US Class 8 | ~250,000 units |

| US light-vehicle | ~13.5M units |

| Dual-sourcing rate | ~40% |

| Tooling cost | $0.5–2.0M/cavity |

Full Version Awaits

Core Molding Technologies Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Core Molding Technologies you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis ready for download and use the moment you buy. You're looking at the actual deliverable; instant access is granted upon payment.