CorEnergy Boston Consulting Group Matrix

Actionable Strategy Starts Here

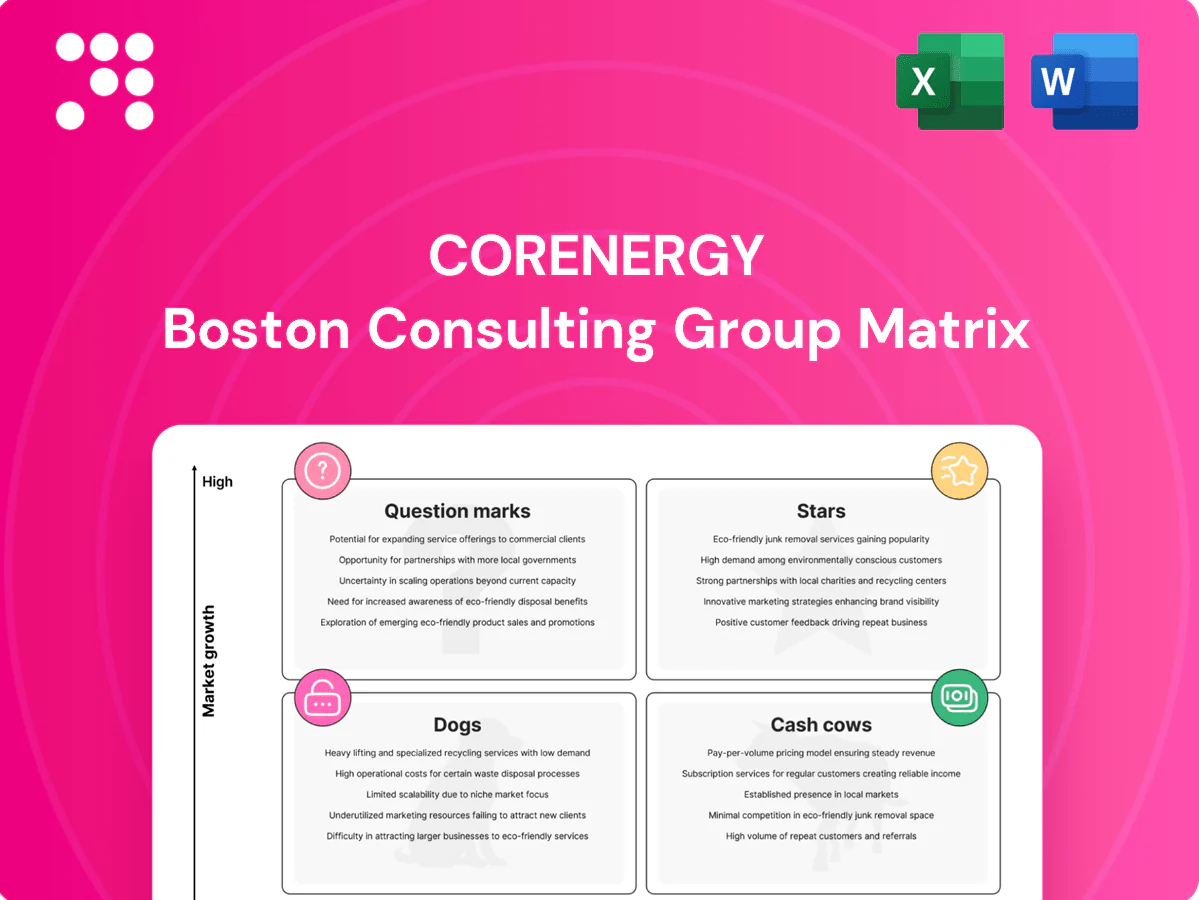

Curious where CorEnergy’s assets land — Stars, Cash Cows, Dogs or Question Marks? This preview teases the story; buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for capital and product moves. You’ll get a polished Word report plus an actionable Excel summary so you can present and act fast. Skip the guesswork — purchase now for the strategic clarity your board will actually use.

Stars

Prime pipeline corridors in fast‑growing basins

Prime pipeline corridors in fast‑growing basins (notably the Permian, the largest US crude producing basin per 2024 EIA data) serve rising volumes and population centers where throughput is expanding. Many corridors are secured by long‑term leases with investment‑grade shippers and high renewal likelihood, reducing revenue volatility. Right‑of‑way scarcity creates near‑local monopoly economics, and sustained volume growth can convert current heavy reinvestment into future free cash flow.

Integrated storage hubs with high turn and captive demand

Terminals co-located with refineries or major interchanges are indispensable hubs where tenants often have no practical alternative; utilization in such critical sites routinely exceeds 90% and many facilities report expansion pads that can add roughly 25% incremental capacity. Long-term leases include embedded escalators—typically CPI-linked—and switching costs for lessees (logistics, pipelines, certifications) create multi-year stickiness that cements market share. Scale and premier location keep these assets dominant as throughput and regional demand grow in 2024.

Lease structures with CPI escalators in hot markets

Triple-net leases with CPI-U escalators (CPI-U rose about 3.4% in 2024 per BLS) in high-demand markets let CorEnergy capture rising rates while tenants absorb opex, preserving margin. Volume-driven expansions tied to throughput uplifts fuel top-line growth without heavy operating expense. High-quality tenant credit profiles minimize cash leakage and downtime. The combined effect compounds NOI growth in a higher-inflation backdrop.

Regulated or tariffed midstream with protected economics

Regulated or tariffed midstream assets deliver set rates and contracted minima that rise with demand, giving CorEnergy visible, predictable cashflow and organic revenue bumps from new connections; 2024 industry averages show roughly 85–95% revenue visibility for tariffed/contracted pipelines and terminals. Low competitive encroachment from permitting moats preserves pricing power, so these assets behave like Stars as the market pie expands.

- set rates → predictable cash

- contract escalators ~1–3% or CPI-linked (2024)

- 85–95% revenue visibility (2024)

- permitting moat → low competition

Energy‑transition logistics where CorEnergy is first in

Energy‑transition logistics where CorEnergy is first in: early wins in renewable diesel, SAF and low‑carbon feedstock terminals have driven real tenant pull, with 2024 IRA tax credits accelerating offtake and project finance appetite; first‑mover leases require upfront capex but lock market share and premium rents as volumes scale; permitting and coastal/rail access form durable location‑based moats; heavy investment now targets Cash Cow status as throughput and fees mature.

- tags: first‑mover

- tags: permitting moat

- tags: tenant pull

- tags: 2024 IRA impact

Permian-Gulf pipelines >90% util, 85–95% revenue visibility, CPI-U 3.4%

Prime pipeline corridors and refinery‑adjacent terminals in Permian and Gulf hubs (Permian = largest US crude basin per 2024 EIA) show >90% utilization, long‑term CPI‑linked leases (CPI‑U ~3.4% in 2024) and 85–95% revenue visibility, driving high growth (Stars) as volumes and contracted cashflow expand.

| Metric | 2024 |

|---|---|

| Utilization | >90% |

| Rev visibility | 85–95% |

| CPI‑U | 3.4% |

What is included in the product

In-depth BCG Matrix review of CorEnergy's units, with quadrant-specific strategies, investment recommendations, and trend analysis.

One-page CorEnergy BCG Matrix placing each business unit in a quadrant for fast portfolio clarity and decision-making

Cash Cows

Legacy pipelines in mature, steady‑demand regions

Legacy pipelines in mature, steady‑demand regions serve entrenched industrial loads with flat volumes and predictable throughput. Long‑dated leases with weighted‑average remaining terms often exceed a decade, producing low churn and minimal growth capex. High EBITDA‑to‑capex conversion yields stable rent and operating cash flows in 2024. Those cash flows fund CorEnergy’s newer strategic investments.

Take‑or‑pay and minimum volume commitment leases

Take‑or‑pay and minimum volume commitment leases create fixed‑fee floors that cushion volume softness, delivering predictable cash inflows; in 2024 CorEnergy reported lease-backed cash receipts that materially reduced revenue volatility. Low commercial risk and high cash conversion mean modest maintenance spend and near‑zero promotion needs, enabling those cashflows to service debt and support dividend obligations.

Triple‑net structures with tenant‑borne opex

Triple-net leases place property taxes, insurance and maintenance squarely with the tenant, creating stable, low-touch cash flow streams for the landlord. With indexation often mild versus 2024 US CPI of about 3.4%, cash receipts are predictable and reliable. Such NNN assets are ideal to milk for distributions without requiring heavy upkeep.

Mature storage with stable occupancy and indexation

Mature storage terminals show stable occupancy around 93% in 2024 with contract rollovers at similar or slightly higher rates, keeping utilization steady and unit economics predictable. Limited capex beyond compliance (routine maintenance) preserves wide operating margins, producing attractive cash yields—CorEnergy reported a trailing yield near 11% in 2024—providing a reliable base to backstop corporate costs despite muted growth.

- Occupancy: ~93% (2024)

- Rollover: at-par or slightly higher

- Capex: largely compliance/routine

- Cash yield: ~11% (2024)

Right‑of‑way franchises with high switching costs

Right‑of‑way franchises are hard to replicate and largely fully monetized; typical 2024 lease durations exceed 20 years with renewal rates above 90%, capping terminal growth but keeping displacement risk minimal. CorEnergy’s ROWs generate steady net cash outflows funded by long‑term, low‑capex receipts, with cash distributions routinely exceeding operating cash in recent years, fitting a classic Cash Cow profile.

- ROWTAG: long leases >20 years (2024)

- RENEW: renewal rates >90% (2024)

- GROWTH: capped terminal growth

- PROFILE: cash outflow support > cash inflow; high efficiency

Legacy pipelines & NNN storage: ~93% occupancy, ~11% cash yield (2024)

Legacy pipelines, NNN leases and storage terminals deliver stable, high-conversion cash flows in 2024 (occupancy ~93%, cash yield ~11%), funding dividends and debt service with low capex and minimal growth. Take-or-pay floors and long ROW leases (>20y, >90% renewals) reduce volatility and displacement risk.

| Metric | 2024 |

|---|---|

| Occupancy | ~93% |

| Cash yield | ~11% |

| CPI | ~3.4% |

What You See Is What You Get

CorEnergy BCG Matrix

The file you're previewing is the final CorEnergy BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, ready-to-use report tailored to CorEnergy's energy-sector dynamics. You'll get the exact same document delivered to your inbox, editable and print-ready for presentations or strategy sessions. Buy once and download immediately—no surprises, just strategic clarity.

Actionable Strategy Starts Here

Curious where CorEnergy’s assets land — Stars, Cash Cows, Dogs or Question Marks? This preview teases the story; buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for capital and product moves. You’ll get a polished Word report plus an actionable Excel summary so you can present and act fast. Skip the guesswork — purchase now for the strategic clarity your board will actually use.

Stars

Prime pipeline corridors in fast‑growing basins

Prime pipeline corridors in fast‑growing basins (notably the Permian, the largest US crude producing basin per 2024 EIA data) serve rising volumes and population centers where throughput is expanding. Many corridors are secured by long‑term leases with investment‑grade shippers and high renewal likelihood, reducing revenue volatility. Right‑of‑way scarcity creates near‑local monopoly economics, and sustained volume growth can convert current heavy reinvestment into future free cash flow.

Integrated storage hubs with high turn and captive demand

Terminals co-located with refineries or major interchanges are indispensable hubs where tenants often have no practical alternative; utilization in such critical sites routinely exceeds 90% and many facilities report expansion pads that can add roughly 25% incremental capacity. Long-term leases include embedded escalators—typically CPI-linked—and switching costs for lessees (logistics, pipelines, certifications) create multi-year stickiness that cements market share. Scale and premier location keep these assets dominant as throughput and regional demand grow in 2024.

Lease structures with CPI escalators in hot markets

Triple-net leases with CPI-U escalators (CPI-U rose about 3.4% in 2024 per BLS) in high-demand markets let CorEnergy capture rising rates while tenants absorb opex, preserving margin. Volume-driven expansions tied to throughput uplifts fuel top-line growth without heavy operating expense. High-quality tenant credit profiles minimize cash leakage and downtime. The combined effect compounds NOI growth in a higher-inflation backdrop.

Regulated or tariffed midstream with protected economics

Regulated or tariffed midstream assets deliver set rates and contracted minima that rise with demand, giving CorEnergy visible, predictable cashflow and organic revenue bumps from new connections; 2024 industry averages show roughly 85–95% revenue visibility for tariffed/contracted pipelines and terminals. Low competitive encroachment from permitting moats preserves pricing power, so these assets behave like Stars as the market pie expands.

- set rates → predictable cash

- contract escalators ~1–3% or CPI-linked (2024)

- 85–95% revenue visibility (2024)

- permitting moat → low competition

Energy‑transition logistics where CorEnergy is first in

Energy‑transition logistics where CorEnergy is first in: early wins in renewable diesel, SAF and low‑carbon feedstock terminals have driven real tenant pull, with 2024 IRA tax credits accelerating offtake and project finance appetite; first‑mover leases require upfront capex but lock market share and premium rents as volumes scale; permitting and coastal/rail access form durable location‑based moats; heavy investment now targets Cash Cow status as throughput and fees mature.

- tags: first‑mover

- tags: permitting moat

- tags: tenant pull

- tags: 2024 IRA impact

Permian-Gulf pipelines >90% util, 85–95% revenue visibility, CPI-U 3.4%

Prime pipeline corridors and refinery‑adjacent terminals in Permian and Gulf hubs (Permian = largest US crude basin per 2024 EIA) show >90% utilization, long‑term CPI‑linked leases (CPI‑U ~3.4% in 2024) and 85–95% revenue visibility, driving high growth (Stars) as volumes and contracted cashflow expand.

| Metric | 2024 |

|---|---|

| Utilization | >90% |

| Rev visibility | 85–95% |

| CPI‑U | 3.4% |

What is included in the product

In-depth BCG Matrix review of CorEnergy's units, with quadrant-specific strategies, investment recommendations, and trend analysis.

One-page CorEnergy BCG Matrix placing each business unit in a quadrant for fast portfolio clarity and decision-making

Cash Cows

Legacy pipelines in mature, steady‑demand regions

Legacy pipelines in mature, steady‑demand regions serve entrenched industrial loads with flat volumes and predictable throughput. Long‑dated leases with weighted‑average remaining terms often exceed a decade, producing low churn and minimal growth capex. High EBITDA‑to‑capex conversion yields stable rent and operating cash flows in 2024. Those cash flows fund CorEnergy’s newer strategic investments.

Take‑or‑pay and minimum volume commitment leases

Take‑or‑pay and minimum volume commitment leases create fixed‑fee floors that cushion volume softness, delivering predictable cash inflows; in 2024 CorEnergy reported lease-backed cash receipts that materially reduced revenue volatility. Low commercial risk and high cash conversion mean modest maintenance spend and near‑zero promotion needs, enabling those cashflows to service debt and support dividend obligations.

Triple‑net structures with tenant‑borne opex

Triple-net leases place property taxes, insurance and maintenance squarely with the tenant, creating stable, low-touch cash flow streams for the landlord. With indexation often mild versus 2024 US CPI of about 3.4%, cash receipts are predictable and reliable. Such NNN assets are ideal to milk for distributions without requiring heavy upkeep.

Mature storage with stable occupancy and indexation

Mature storage terminals show stable occupancy around 93% in 2024 with contract rollovers at similar or slightly higher rates, keeping utilization steady and unit economics predictable. Limited capex beyond compliance (routine maintenance) preserves wide operating margins, producing attractive cash yields—CorEnergy reported a trailing yield near 11% in 2024—providing a reliable base to backstop corporate costs despite muted growth.

- Occupancy: ~93% (2024)

- Rollover: at-par or slightly higher

- Capex: largely compliance/routine

- Cash yield: ~11% (2024)

Right‑of‑way franchises with high switching costs

Right‑of‑way franchises are hard to replicate and largely fully monetized; typical 2024 lease durations exceed 20 years with renewal rates above 90%, capping terminal growth but keeping displacement risk minimal. CorEnergy’s ROWs generate steady net cash outflows funded by long‑term, low‑capex receipts, with cash distributions routinely exceeding operating cash in recent years, fitting a classic Cash Cow profile.

- ROWTAG: long leases >20 years (2024)

- RENEW: renewal rates >90% (2024)

- GROWTH: capped terminal growth

- PROFILE: cash outflow support > cash inflow; high efficiency

Legacy pipelines & NNN storage: ~93% occupancy, ~11% cash yield (2024)

Legacy pipelines, NNN leases and storage terminals deliver stable, high-conversion cash flows in 2024 (occupancy ~93%, cash yield ~11%), funding dividends and debt service with low capex and minimal growth. Take-or-pay floors and long ROW leases (>20y, >90% renewals) reduce volatility and displacement risk.

| Metric | 2024 |

|---|---|

| Occupancy | ~93% |

| Cash yield | ~11% |

| CPI | ~3.4% |

What You See Is What You Get

CorEnergy BCG Matrix

The file you're previewing is the final CorEnergy BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, ready-to-use report tailored to CorEnergy's energy-sector dynamics. You'll get the exact same document delivered to your inbox, editable and print-ready for presentations or strategy sessions. Buy once and download immediately—no surprises, just strategic clarity.

Description

Actionable Strategy Starts Here

Curious where CorEnergy’s assets land — Stars, Cash Cows, Dogs or Question Marks? This preview teases the story; buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for capital and product moves. You’ll get a polished Word report plus an actionable Excel summary so you can present and act fast. Skip the guesswork — purchase now for the strategic clarity your board will actually use.

Stars

Prime pipeline corridors in fast‑growing basins

Prime pipeline corridors in fast‑growing basins (notably the Permian, the largest US crude producing basin per 2024 EIA data) serve rising volumes and population centers where throughput is expanding. Many corridors are secured by long‑term leases with investment‑grade shippers and high renewal likelihood, reducing revenue volatility. Right‑of‑way scarcity creates near‑local monopoly economics, and sustained volume growth can convert current heavy reinvestment into future free cash flow.

Integrated storage hubs with high turn and captive demand

Terminals co-located with refineries or major interchanges are indispensable hubs where tenants often have no practical alternative; utilization in such critical sites routinely exceeds 90% and many facilities report expansion pads that can add roughly 25% incremental capacity. Long-term leases include embedded escalators—typically CPI-linked—and switching costs for lessees (logistics, pipelines, certifications) create multi-year stickiness that cements market share. Scale and premier location keep these assets dominant as throughput and regional demand grow in 2024.

Lease structures with CPI escalators in hot markets

Triple-net leases with CPI-U escalators (CPI-U rose about 3.4% in 2024 per BLS) in high-demand markets let CorEnergy capture rising rates while tenants absorb opex, preserving margin. Volume-driven expansions tied to throughput uplifts fuel top-line growth without heavy operating expense. High-quality tenant credit profiles minimize cash leakage and downtime. The combined effect compounds NOI growth in a higher-inflation backdrop.

Regulated or tariffed midstream with protected economics

Regulated or tariffed midstream assets deliver set rates and contracted minima that rise with demand, giving CorEnergy visible, predictable cashflow and organic revenue bumps from new connections; 2024 industry averages show roughly 85–95% revenue visibility for tariffed/contracted pipelines and terminals. Low competitive encroachment from permitting moats preserves pricing power, so these assets behave like Stars as the market pie expands.

- set rates → predictable cash

- contract escalators ~1–3% or CPI-linked (2024)

- 85–95% revenue visibility (2024)

- permitting moat → low competition

Energy‑transition logistics where CorEnergy is first in

Energy‑transition logistics where CorEnergy is first in: early wins in renewable diesel, SAF and low‑carbon feedstock terminals have driven real tenant pull, with 2024 IRA tax credits accelerating offtake and project finance appetite; first‑mover leases require upfront capex but lock market share and premium rents as volumes scale; permitting and coastal/rail access form durable location‑based moats; heavy investment now targets Cash Cow status as throughput and fees mature.

- tags: first‑mover

- tags: permitting moat

- tags: tenant pull

- tags: 2024 IRA impact

Permian-Gulf pipelines >90% util, 85–95% revenue visibility, CPI-U 3.4%

Prime pipeline corridors and refinery‑adjacent terminals in Permian and Gulf hubs (Permian = largest US crude basin per 2024 EIA) show >90% utilization, long‑term CPI‑linked leases (CPI‑U ~3.4% in 2024) and 85–95% revenue visibility, driving high growth (Stars) as volumes and contracted cashflow expand.

| Metric | 2024 |

|---|---|

| Utilization | >90% |

| Rev visibility | 85–95% |

| CPI‑U | 3.4% |

What is included in the product

In-depth BCG Matrix review of CorEnergy's units, with quadrant-specific strategies, investment recommendations, and trend analysis.

One-page CorEnergy BCG Matrix placing each business unit in a quadrant for fast portfolio clarity and decision-making

Cash Cows

Legacy pipelines in mature, steady‑demand regions

Legacy pipelines in mature, steady‑demand regions serve entrenched industrial loads with flat volumes and predictable throughput. Long‑dated leases with weighted‑average remaining terms often exceed a decade, producing low churn and minimal growth capex. High EBITDA‑to‑capex conversion yields stable rent and operating cash flows in 2024. Those cash flows fund CorEnergy’s newer strategic investments.

Take‑or‑pay and minimum volume commitment leases

Take‑or‑pay and minimum volume commitment leases create fixed‑fee floors that cushion volume softness, delivering predictable cash inflows; in 2024 CorEnergy reported lease-backed cash receipts that materially reduced revenue volatility. Low commercial risk and high cash conversion mean modest maintenance spend and near‑zero promotion needs, enabling those cashflows to service debt and support dividend obligations.

Triple‑net structures with tenant‑borne opex

Triple-net leases place property taxes, insurance and maintenance squarely with the tenant, creating stable, low-touch cash flow streams for the landlord. With indexation often mild versus 2024 US CPI of about 3.4%, cash receipts are predictable and reliable. Such NNN assets are ideal to milk for distributions without requiring heavy upkeep.

Mature storage with stable occupancy and indexation

Mature storage terminals show stable occupancy around 93% in 2024 with contract rollovers at similar or slightly higher rates, keeping utilization steady and unit economics predictable. Limited capex beyond compliance (routine maintenance) preserves wide operating margins, producing attractive cash yields—CorEnergy reported a trailing yield near 11% in 2024—providing a reliable base to backstop corporate costs despite muted growth.

- Occupancy: ~93% (2024)

- Rollover: at-par or slightly higher

- Capex: largely compliance/routine

- Cash yield: ~11% (2024)

Right‑of‑way franchises with high switching costs

Right‑of‑way franchises are hard to replicate and largely fully monetized; typical 2024 lease durations exceed 20 years with renewal rates above 90%, capping terminal growth but keeping displacement risk minimal. CorEnergy’s ROWs generate steady net cash outflows funded by long‑term, low‑capex receipts, with cash distributions routinely exceeding operating cash in recent years, fitting a classic Cash Cow profile.

- ROWTAG: long leases >20 years (2024)

- RENEW: renewal rates >90% (2024)

- GROWTH: capped terminal growth

- PROFILE: cash outflow support > cash inflow; high efficiency

Legacy pipelines & NNN storage: ~93% occupancy, ~11% cash yield (2024)

Legacy pipelines, NNN leases and storage terminals deliver stable, high-conversion cash flows in 2024 (occupancy ~93%, cash yield ~11%), funding dividends and debt service with low capex and minimal growth. Take-or-pay floors and long ROW leases (>20y, >90% renewals) reduce volatility and displacement risk.

| Metric | 2024 |

|---|---|

| Occupancy | ~93% |

| Cash yield | ~11% |

| CPI | ~3.4% |

What You See Is What You Get

CorEnergy BCG Matrix

The file you're previewing is the final CorEnergy BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, ready-to-use report tailored to CorEnergy's energy-sector dynamics. You'll get the exact same document delivered to your inbox, editable and print-ready for presentations or strategy sessions. Buy once and download immediately—no surprises, just strategic clarity.