CP All Boston Consulting Group Matrix

Download Your Competitive Advantage

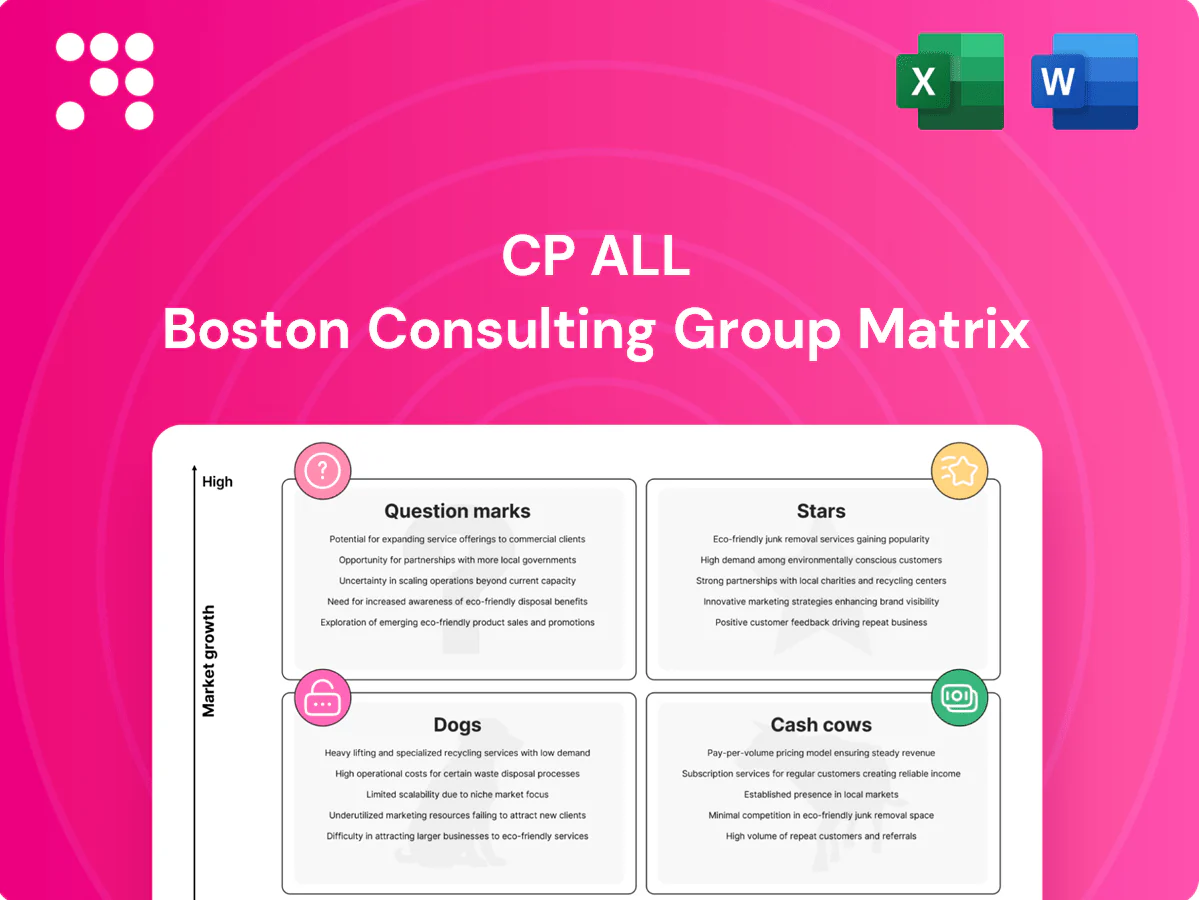

Curious where CP All’s brands sit in the market—Stars, Cash Cows, Dogs or Question Marks? This preview sketches the picture; buy the full BCG Matrix for quadrant-by-quadrant clarity, data-backed recommendations, and a clear playbook to reallocate capital and boost returns. Purchase now for an editable Word report plus a high-level Excel summary—instant access, ready to present and act on.

Stars

7‑Eleven Thailand core convenience format

Market leader 7‑Eleven Thailand operates roughly 14,000 stores as of 2024, delivering massive footprint coverage and dominant share in the expanding convenience segment driven by ready‑to‑eat meals, quick trips and O2O ordering. The format benefits from urbanization and lifestyle shifts that keep category volume rising. Defending the lead requires steady capex in store refresh, cold chain and last‑mile logistics. Sustained dominance typically converts into stronger cash generation.

Ready‑to‑eat/private‑label food ecosystem

CP All, operator of 7‑Eleven Thailand with over 14,000 stores in 2024, leverages fresh ready‑to‑eat and private‑label lines to drive volume, margin and loyalty rapidly.

Category growth is strong as consumers favor convenience—especially breakfast and late‑night—while heavy working capital and commissary/kitchen capacity continue to absorb cash.

Ongoing investment in quality, speed and SKU breadth is required to lock habitual purchases and defend share.

Makro B2B wholesale to HoReCa

Makro B2B to HoReCa holds a high share in CP All’s portfolio, benefiting from 2024 tourism rebound and robust SME foodservice demand; Thailand saw markedly higher international arrivals and domestic dining activity versus 2022. The wholesale model scales through deeper assortment, competitive price perception and B2B services—credit, delivery and contracts. Capital intensive in logistics, cold chain and digital B2B platforms, but unit economics and repeat contracts justify investments. Prioritize omnichannel and contract customers to cement leadership.

All Member loyalty + data flywheel

All Member loyalty + data flywheel leverages a large, active base and rising engagement to make promotions smarter and traffic stickier, positioning CP All in the retail-media sweet spot as targeted offers gain share.

Maintaining relevance requires ongoing tech investment and partner integrations; when executed well the flywheel supplies cheaper demand and feeds every business unit, improving ROI across channels.

- Member-driven targeting

- Higher promo efficiency

- Requires continuous tech spend

- Feeds other units with lower CAC

O2O last‑mile (7‑Delivery / click‑and‑collect)

Convenience plus speed is a growing market where CP All already has proximity advantage with over 14,000 7‑Eleven stores in Thailand (2024).

Order density and dark back‑room fulfillment boost viability as adoption rises, but early unit economics can be thin, driving continued burn on ops and promotions.

Scale and higher orders per store tend to shift the model toward cash‑positive territory over time.

- proximity: 14,000+ stores (2024)

- order density: improves fulfillment ROI

- unit economics: early thin, requires promos/ops spend

- scale: key to cash positivity

Market leader with ~14,000 stores: data-driven loyalty, O2O growth, heavy capex

Market leader 7‑Eleven Thailand operates ~14,000 stores in 2024, driving volume via ready‑to‑eat, private‑label and O2O. Strong category growth from urbanization and tourism rebound boosts unit sales, but heavy capex in store refresh, cold chain and last‑mile keeps cash intensity high. All Member data-driven targeting improves promo ROI and loyalty, lowering CAC as scale raises store-level profitability over time.

| Metric | 2024 |

|---|---|

| Stores | ~14,000 |

| Growth drivers | Urbanization, tourism rebound |

| Key costs | Capex: stores/cold chain/logistics |

| Strategic asset | All Member loyalty (data flywheel) |

What is included in the product

Comprehensive BCG Matrix review of CP All’s portfolio with strategic moves per quadrant—invest, hold, or divest—plus trend context.

One-page CP All BCG Matrix that pins each business unit in a quadrant for fast, board-ready strategic decisions.

Cash Cows

Legacy high‑traffic urban 7‑Eleven stores

Legacy high‑traffic urban 7‑Eleven stores occupy prime locations with entrenched routines, stable baskets and predictable footfall, supporting low single‑digit same‑store variability and operational predictability; CP All operates over 13,000 7‑Eleven stores in Thailand (2024). Low incremental investment beyond maintenance and planogram tweaks keeps margins resilient. Strong cash conversion from these cash cows funds newer bets—keep standards high, don’t over‑renovate; milk wisely.

Bill payment and Counter Service at stores

Bill payment and counter services generate high‑margin fee income with minimal incremental capex, leveraging CP All’s 13,000+ 7‑Eleven stores in Thailand (2024) to deliver steady ticket flow across utilities, telco, and services. They sustain regular footfall without heavy promotions by offering essential, repeatable transactions. Focus should be on maintaining uptime and expanding the partner roster at low cost to preserve margins and retail traffic.

Supplier trade income and retail media

Slotting, displays and data‑driven promos monetize shelf space across CP Alls vast network of over 14,000 7‑Eleven stores, creating predictable, recurring cash with limited working capital needs. Brands continue to pay as long as CP Alls share and footfall remain high; supplier trade and retail media are high‑margin cash cows. Tighten measurement and attribution to sustain premium rates and justify price increases to partners.

Makro mature Thai warehouses

Makro mature Thai warehouses deliver steady cash flow as established stores serving loyal SME customers with efficient ops; about 120 stores nationwide in 2024 sustain repeat B2B purchases. Growth is slower but cash yield remains solid, with reported EBITDA margins near 12% in 2024, requiring only upkeep and category refresh rather than heavy capex. Excess cash is being redeployed into digital platforms and new retail formats to drive future expansion.

- Scale: ~120 stores (2024)

- Profitability: ~12% EBITDA margin (2024)

- Strategy: low capex, fund digital & new formats

Core beverages and tobacco mix

Core beverages and tobacco mix are stable, highly regulated, habit-driven categories that provide steady volume and cash for CP All, delivering consistent margin contribution despite little category growth.

These lines demand compliance and tight inventory discipline rather than heavy marketing spend, forming a dependable earnings base that smooths volatility from other higher-growth segments.

- Stable cash flow

- Low growth, steady margins

- Compliance & inventory focus

- Volatility dampener

Cash engine: 13,000+ stores & ≈120 wholesale sites fund digital bets

Legacy 7‑Eleven stores (13,000+ Thailand, 2024) plus bill‑payment, retail media and Makro (≈120 stores, 2024) generate steady, high‑margin cash with low incremental capex and predictable footfall; focus on maintenance, monetization and measurement to sustain cash conversion. Milk to fund digital and new formats.

| Asset | Scale (2024) | EBITDA |

|---|---|---|

| 7‑Eleven | 13,000+ stores | High |

| Makro | ≈120 stores | ~12% |

What You See Is What You Get

CP All BCG Matrix

The CP All BCG Matrix you're previewing on this page is the exact file you'll receive after purchase—no watermarks, no placeholders. This is the finished, fully formatted report built for strategic clarity and quick presentation. Purchase unlocks the same editable, print-ready document sent straight to your inbox. Use it immediately for planning, investor decks, or client briefings.

Download Your Competitive Advantage

Curious where CP All’s brands sit in the market—Stars, Cash Cows, Dogs or Question Marks? This preview sketches the picture; buy the full BCG Matrix for quadrant-by-quadrant clarity, data-backed recommendations, and a clear playbook to reallocate capital and boost returns. Purchase now for an editable Word report plus a high-level Excel summary—instant access, ready to present and act on.

Stars

7‑Eleven Thailand core convenience format

Market leader 7‑Eleven Thailand operates roughly 14,000 stores as of 2024, delivering massive footprint coverage and dominant share in the expanding convenience segment driven by ready‑to‑eat meals, quick trips and O2O ordering. The format benefits from urbanization and lifestyle shifts that keep category volume rising. Defending the lead requires steady capex in store refresh, cold chain and last‑mile logistics. Sustained dominance typically converts into stronger cash generation.

Ready‑to‑eat/private‑label food ecosystem

CP All, operator of 7‑Eleven Thailand with over 14,000 stores in 2024, leverages fresh ready‑to‑eat and private‑label lines to drive volume, margin and loyalty rapidly.

Category growth is strong as consumers favor convenience—especially breakfast and late‑night—while heavy working capital and commissary/kitchen capacity continue to absorb cash.

Ongoing investment in quality, speed and SKU breadth is required to lock habitual purchases and defend share.

Makro B2B wholesale to HoReCa

Makro B2B to HoReCa holds a high share in CP All’s portfolio, benefiting from 2024 tourism rebound and robust SME foodservice demand; Thailand saw markedly higher international arrivals and domestic dining activity versus 2022. The wholesale model scales through deeper assortment, competitive price perception and B2B services—credit, delivery and contracts. Capital intensive in logistics, cold chain and digital B2B platforms, but unit economics and repeat contracts justify investments. Prioritize omnichannel and contract customers to cement leadership.

All Member loyalty + data flywheel

All Member loyalty + data flywheel leverages a large, active base and rising engagement to make promotions smarter and traffic stickier, positioning CP All in the retail-media sweet spot as targeted offers gain share.

Maintaining relevance requires ongoing tech investment and partner integrations; when executed well the flywheel supplies cheaper demand and feeds every business unit, improving ROI across channels.

- Member-driven targeting

- Higher promo efficiency

- Requires continuous tech spend

- Feeds other units with lower CAC

O2O last‑mile (7‑Delivery / click‑and‑collect)

Convenience plus speed is a growing market where CP All already has proximity advantage with over 14,000 7‑Eleven stores in Thailand (2024).

Order density and dark back‑room fulfillment boost viability as adoption rises, but early unit economics can be thin, driving continued burn on ops and promotions.

Scale and higher orders per store tend to shift the model toward cash‑positive territory over time.

- proximity: 14,000+ stores (2024)

- order density: improves fulfillment ROI

- unit economics: early thin, requires promos/ops spend

- scale: key to cash positivity

Market leader with ~14,000 stores: data-driven loyalty, O2O growth, heavy capex

Market leader 7‑Eleven Thailand operates ~14,000 stores in 2024, driving volume via ready‑to‑eat, private‑label and O2O. Strong category growth from urbanization and tourism rebound boosts unit sales, but heavy capex in store refresh, cold chain and last‑mile keeps cash intensity high. All Member data-driven targeting improves promo ROI and loyalty, lowering CAC as scale raises store-level profitability over time.

| Metric | 2024 |

|---|---|

| Stores | ~14,000 |

| Growth drivers | Urbanization, tourism rebound |

| Key costs | Capex: stores/cold chain/logistics |

| Strategic asset | All Member loyalty (data flywheel) |

What is included in the product

Comprehensive BCG Matrix review of CP All’s portfolio with strategic moves per quadrant—invest, hold, or divest—plus trend context.

One-page CP All BCG Matrix that pins each business unit in a quadrant for fast, board-ready strategic decisions.

Cash Cows

Legacy high‑traffic urban 7‑Eleven stores

Legacy high‑traffic urban 7‑Eleven stores occupy prime locations with entrenched routines, stable baskets and predictable footfall, supporting low single‑digit same‑store variability and operational predictability; CP All operates over 13,000 7‑Eleven stores in Thailand (2024). Low incremental investment beyond maintenance and planogram tweaks keeps margins resilient. Strong cash conversion from these cash cows funds newer bets—keep standards high, don’t over‑renovate; milk wisely.

Bill payment and Counter Service at stores

Bill payment and counter services generate high‑margin fee income with minimal incremental capex, leveraging CP All’s 13,000+ 7‑Eleven stores in Thailand (2024) to deliver steady ticket flow across utilities, telco, and services. They sustain regular footfall without heavy promotions by offering essential, repeatable transactions. Focus should be on maintaining uptime and expanding the partner roster at low cost to preserve margins and retail traffic.

Supplier trade income and retail media

Slotting, displays and data‑driven promos monetize shelf space across CP Alls vast network of over 14,000 7‑Eleven stores, creating predictable, recurring cash with limited working capital needs. Brands continue to pay as long as CP Alls share and footfall remain high; supplier trade and retail media are high‑margin cash cows. Tighten measurement and attribution to sustain premium rates and justify price increases to partners.

Makro mature Thai warehouses

Makro mature Thai warehouses deliver steady cash flow as established stores serving loyal SME customers with efficient ops; about 120 stores nationwide in 2024 sustain repeat B2B purchases. Growth is slower but cash yield remains solid, with reported EBITDA margins near 12% in 2024, requiring only upkeep and category refresh rather than heavy capex. Excess cash is being redeployed into digital platforms and new retail formats to drive future expansion.

- Scale: ~120 stores (2024)

- Profitability: ~12% EBITDA margin (2024)

- Strategy: low capex, fund digital & new formats

Core beverages and tobacco mix

Core beverages and tobacco mix are stable, highly regulated, habit-driven categories that provide steady volume and cash for CP All, delivering consistent margin contribution despite little category growth.

These lines demand compliance and tight inventory discipline rather than heavy marketing spend, forming a dependable earnings base that smooths volatility from other higher-growth segments.

- Stable cash flow

- Low growth, steady margins

- Compliance & inventory focus

- Volatility dampener

Cash engine: 13,000+ stores & ≈120 wholesale sites fund digital bets

Legacy 7‑Eleven stores (13,000+ Thailand, 2024) plus bill‑payment, retail media and Makro (≈120 stores, 2024) generate steady, high‑margin cash with low incremental capex and predictable footfall; focus on maintenance, monetization and measurement to sustain cash conversion. Milk to fund digital and new formats.

| Asset | Scale (2024) | EBITDA |

|---|---|---|

| 7‑Eleven | 13,000+ stores | High |

| Makro | ≈120 stores | ~12% |

What You See Is What You Get

CP All BCG Matrix

The CP All BCG Matrix you're previewing on this page is the exact file you'll receive after purchase—no watermarks, no placeholders. This is the finished, fully formatted report built for strategic clarity and quick presentation. Purchase unlocks the same editable, print-ready document sent straight to your inbox. Use it immediately for planning, investor decks, or client briefings.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

Curious where CP All’s brands sit in the market—Stars, Cash Cows, Dogs or Question Marks? This preview sketches the picture; buy the full BCG Matrix for quadrant-by-quadrant clarity, data-backed recommendations, and a clear playbook to reallocate capital and boost returns. Purchase now for an editable Word report plus a high-level Excel summary—instant access, ready to present and act on.

Stars

7‑Eleven Thailand core convenience format

Market leader 7‑Eleven Thailand operates roughly 14,000 stores as of 2024, delivering massive footprint coverage and dominant share in the expanding convenience segment driven by ready‑to‑eat meals, quick trips and O2O ordering. The format benefits from urbanization and lifestyle shifts that keep category volume rising. Defending the lead requires steady capex in store refresh, cold chain and last‑mile logistics. Sustained dominance typically converts into stronger cash generation.

Ready‑to‑eat/private‑label food ecosystem

CP All, operator of 7‑Eleven Thailand with over 14,000 stores in 2024, leverages fresh ready‑to‑eat and private‑label lines to drive volume, margin and loyalty rapidly.

Category growth is strong as consumers favor convenience—especially breakfast and late‑night—while heavy working capital and commissary/kitchen capacity continue to absorb cash.

Ongoing investment in quality, speed and SKU breadth is required to lock habitual purchases and defend share.

Makro B2B wholesale to HoReCa

Makro B2B to HoReCa holds a high share in CP All’s portfolio, benefiting from 2024 tourism rebound and robust SME foodservice demand; Thailand saw markedly higher international arrivals and domestic dining activity versus 2022. The wholesale model scales through deeper assortment, competitive price perception and B2B services—credit, delivery and contracts. Capital intensive in logistics, cold chain and digital B2B platforms, but unit economics and repeat contracts justify investments. Prioritize omnichannel and contract customers to cement leadership.

All Member loyalty + data flywheel

All Member loyalty + data flywheel leverages a large, active base and rising engagement to make promotions smarter and traffic stickier, positioning CP All in the retail-media sweet spot as targeted offers gain share.

Maintaining relevance requires ongoing tech investment and partner integrations; when executed well the flywheel supplies cheaper demand and feeds every business unit, improving ROI across channels.

- Member-driven targeting

- Higher promo efficiency

- Requires continuous tech spend

- Feeds other units with lower CAC

O2O last‑mile (7‑Delivery / click‑and‑collect)

Convenience plus speed is a growing market where CP All already has proximity advantage with over 14,000 7‑Eleven stores in Thailand (2024).

Order density and dark back‑room fulfillment boost viability as adoption rises, but early unit economics can be thin, driving continued burn on ops and promotions.

Scale and higher orders per store tend to shift the model toward cash‑positive territory over time.

- proximity: 14,000+ stores (2024)

- order density: improves fulfillment ROI

- unit economics: early thin, requires promos/ops spend

- scale: key to cash positivity

Market leader with ~14,000 stores: data-driven loyalty, O2O growth, heavy capex

Market leader 7‑Eleven Thailand operates ~14,000 stores in 2024, driving volume via ready‑to‑eat, private‑label and O2O. Strong category growth from urbanization and tourism rebound boosts unit sales, but heavy capex in store refresh, cold chain and last‑mile keeps cash intensity high. All Member data-driven targeting improves promo ROI and loyalty, lowering CAC as scale raises store-level profitability over time.

| Metric | 2024 |

|---|---|

| Stores | ~14,000 |

| Growth drivers | Urbanization, tourism rebound |

| Key costs | Capex: stores/cold chain/logistics |

| Strategic asset | All Member loyalty (data flywheel) |

What is included in the product

Comprehensive BCG Matrix review of CP All’s portfolio with strategic moves per quadrant—invest, hold, or divest—plus trend context.

One-page CP All BCG Matrix that pins each business unit in a quadrant for fast, board-ready strategic decisions.

Cash Cows

Legacy high‑traffic urban 7‑Eleven stores

Legacy high‑traffic urban 7‑Eleven stores occupy prime locations with entrenched routines, stable baskets and predictable footfall, supporting low single‑digit same‑store variability and operational predictability; CP All operates over 13,000 7‑Eleven stores in Thailand (2024). Low incremental investment beyond maintenance and planogram tweaks keeps margins resilient. Strong cash conversion from these cash cows funds newer bets—keep standards high, don’t over‑renovate; milk wisely.

Bill payment and Counter Service at stores

Bill payment and counter services generate high‑margin fee income with minimal incremental capex, leveraging CP All’s 13,000+ 7‑Eleven stores in Thailand (2024) to deliver steady ticket flow across utilities, telco, and services. They sustain regular footfall without heavy promotions by offering essential, repeatable transactions. Focus should be on maintaining uptime and expanding the partner roster at low cost to preserve margins and retail traffic.

Supplier trade income and retail media

Slotting, displays and data‑driven promos monetize shelf space across CP Alls vast network of over 14,000 7‑Eleven stores, creating predictable, recurring cash with limited working capital needs. Brands continue to pay as long as CP Alls share and footfall remain high; supplier trade and retail media are high‑margin cash cows. Tighten measurement and attribution to sustain premium rates and justify price increases to partners.

Makro mature Thai warehouses

Makro mature Thai warehouses deliver steady cash flow as established stores serving loyal SME customers with efficient ops; about 120 stores nationwide in 2024 sustain repeat B2B purchases. Growth is slower but cash yield remains solid, with reported EBITDA margins near 12% in 2024, requiring only upkeep and category refresh rather than heavy capex. Excess cash is being redeployed into digital platforms and new retail formats to drive future expansion.

- Scale: ~120 stores (2024)

- Profitability: ~12% EBITDA margin (2024)

- Strategy: low capex, fund digital & new formats

Core beverages and tobacco mix

Core beverages and tobacco mix are stable, highly regulated, habit-driven categories that provide steady volume and cash for CP All, delivering consistent margin contribution despite little category growth.

These lines demand compliance and tight inventory discipline rather than heavy marketing spend, forming a dependable earnings base that smooths volatility from other higher-growth segments.

- Stable cash flow

- Low growth, steady margins

- Compliance & inventory focus

- Volatility dampener

Cash engine: 13,000+ stores & ≈120 wholesale sites fund digital bets

Legacy 7‑Eleven stores (13,000+ Thailand, 2024) plus bill‑payment, retail media and Makro (≈120 stores, 2024) generate steady, high‑margin cash with low incremental capex and predictable footfall; focus on maintenance, monetization and measurement to sustain cash conversion. Milk to fund digital and new formats.

| Asset | Scale (2024) | EBITDA |

|---|---|---|

| 7‑Eleven | 13,000+ stores | High |

| Makro | ≈120 stores | ~12% |

What You See Is What You Get

CP All BCG Matrix

The CP All BCG Matrix you're previewing on this page is the exact file you'll receive after purchase—no watermarks, no placeholders. This is the finished, fully formatted report built for strategic clarity and quick presentation. Purchase unlocks the same editable, print-ready document sent straight to your inbox. Use it immediately for planning, investor decks, or client briefings.