CPFL Energia Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

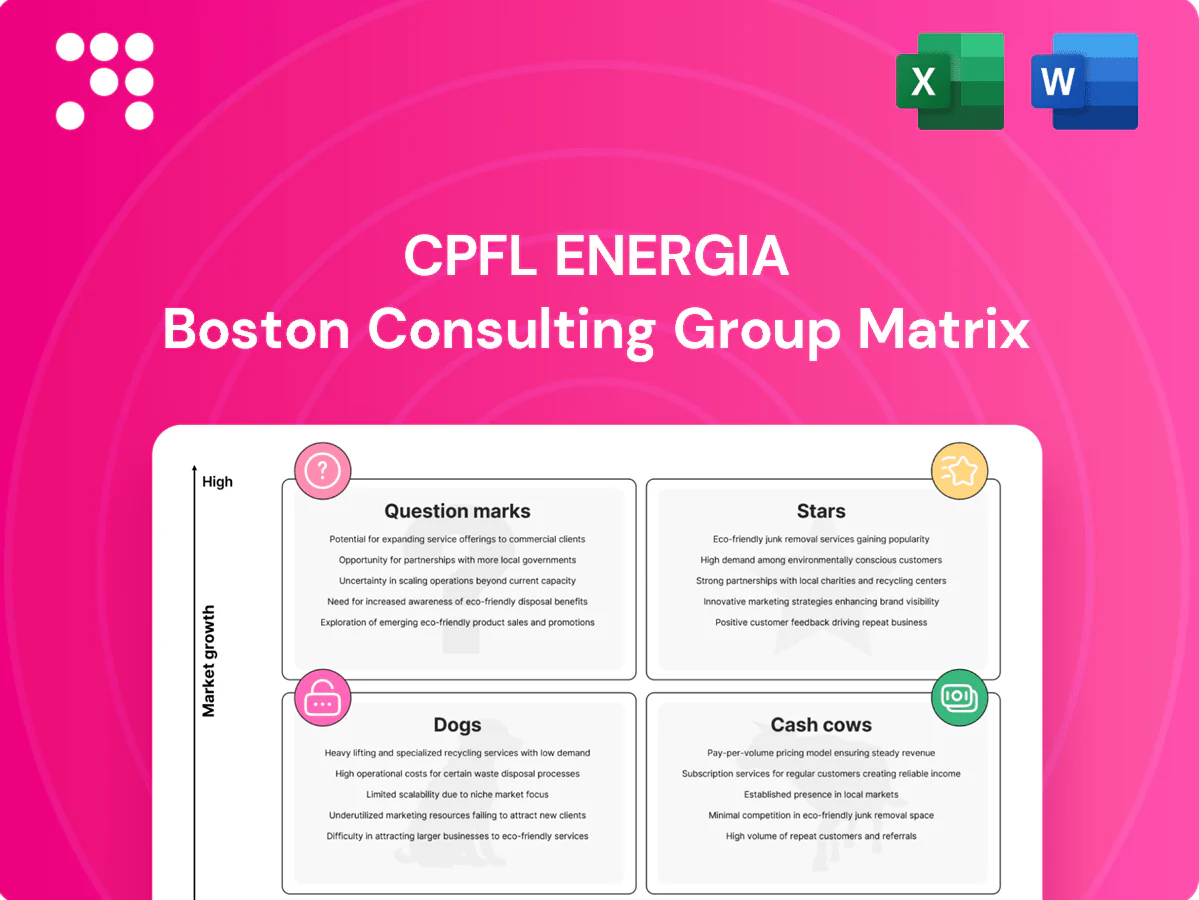

Curious where CPFL Energia’s businesses fall—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at strengths and risks, but the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed recommendations, and a ready-to-use Word report plus an Excel summary. Buy the complete analysis to skip the guesswork and get strategic moves you can act on today.

Stars

Utility-scale wind portfolio

Utility-scale wind in Brazil remains fast-growing, with national installed capacity exceeding 20 GW and sustained annual additions, and CPFL holds meaningful installed capacity plus a visible project pipeline supporting growth.

Strong long-term PPAs and declining onshore wind cost curves keep utilization and revenue profiles solid, preserving cash flow visibility for CPFL.

Wind currently soaks up capital, but its share and growth justify continued investment to lock leadership before market maturation.

Utility-scale solar build-out

Utility-scale solar additions accelerated in 2024 and CPFL is winning sites and contracts, with a disclosed pipeline topping 1 GW and several PPAs awarded during the year. Execution speed and strict EPC discipline give CPFL clear heft versus smaller developers, shortening COD timelines. Cash burn is real during construction, but modeled IRRs above low-double digits as assets ramp make returns attractive. Stay on the front foot — scale is the edge.

Free-market retailing (ACL) for C&I

Migration to the free market is expanding fast and CPFL’s strong brand and retail book—about 11 million clients across São Paulo, Paraná and Rio Grande do Sul—positions it to win C&I load. Cross-selling risk management and tailored PPAs has been lifting share in the ACL, while brisk growth requires ongoing sales and hedging muscle. Keep feeding the engine to sustain momentum.

Grid digitalization & smart grid rollouts

Grid digitalization and smart grid rollouts are accelerating in Brazil with clear regulatory support and maturing technologies; CPFL’s deployments cut technical losses and raise reliability, compounding competitive advantage across its concession areas. Capex is front-loaded while efficiency gains and data-driven O&M savings accrue over time, making this a Stars-position asset to press for growth.

- Capex-heavy

- Loss reduction

- Reliability uplift

- Data-driven O&M

Distributed generation for corporates

Corporate and industrial clients increasingly demand predictable green power; CPFL bundles distributed-generation solar with financing and O&M, capturing customers seeking fixed-cost, low-carbon supply. The addressable DG market is expanding amid tariff volatility and rising ESG mandates, with global corporate renewables deals exceeding 30 GW by 2023 and rooftop costs down over 85% since 2010, boosting CPFL share where it bundles energy plus services. Double down while conversion costs continue to fall and customer acquisition costs decline.

- Tag: market_expansion — corporate renewables >30 GW (2023)

- Tag: cost_trend — rooftop solar costs down >85% since 2010

- Tag: CPFL_advantage — bundles: DG + financing + O&M

- Tag: recommendation — scale while conversion costs fall

Brazil: >20 GW wind, ~11m clients

Utility wind: Brazil >20 GW (2024); CPFL has meaningful capacity and pipeline, steady PPAs preserving cash flow. Solar: CPFL disclosed >1 GW pipeline (2024) and strong EPC execution delivering low-double-digit IRRs. Retail/C&I: ~11m clients and ACL wins; DG bundles + financing scale as rooftop costs down >85% since 2010.

| Metric | Figure |

|---|---|

| Brazil wind (2024) | >20 GW |

| CPFL solar pipeline (2024) | >1 GW |

| Retail clients | ~11m |

What is included in the product

In-depth BCG Matrix review of CPFL Energia’s units with strategic moves per quadrant—invest, hold, or divest, plus risks and trends.

One-page CPFL Energia BCG Matrix snapshot that clarifies portfolio pain points for faster executive decisions.

Cash Cows

Regulated distribution concessions

Regulated distribution concessions serve ~8.8 million customers across mature São Paulo and Rio Grande do Sul markets, holding high market share and stable demand. Regulatory tariffs and efficiency gains delivered predictable returns, with 2024 distribution EBITDA margin around 30% and regular ANEEL adjustments supporting cash flow. Low volume growth but strong free cash generation after maintenance capex; milk assets while pursuing selective automation to widen margins.

Legacy small hydro (PCHs)

Legacy small hydro (PCHs) are depreciated assets with deep operational know-how and are defined in Brazil as plants up to 30 MW, delivering stable, low-growth generation. Availability is strong and O&M is efficient, producing reliable cash flows that fund newer bets across CPFL Energia. Focus is on optimizing outages and incremental yield improvements rather than capital-intensive upgrades.

Captive residential & small business sales (ACR)

Captive residential and small-business sales (ACR) show mature demand with CPFL Energia serving roughly 9 million concession customers in 2024, yielding stable volume and high retention within the concession. Tariff pass-through to consumers stabilizes margins against wholesale cost swings, reducing margin volatility. Low marketing needs and steady receivables enable cash harvest strategies while keeping losses and delinquency tightly controlled.

Centralized O&M services for owned fleet

Centralized O&M for CPFL Energia’s owned fleet drives lower per-MW operating cost through shared crews, spares and scheduling; the standardized “factory” approach yields repeatable processes and stable margins, producing steady free cash flow rather than rapid growth.

Incremental digitization—remote monitoring, predictive maintenance—can lift O&M efficiency by a few percentage points and further reinforce cash generation without changing the cash-cow profile.

- Shared services reduce per-MW costs

- Standardized operations keep margins stable

- Low-growth, steady cash drip

- Digitization adds modest efficiency gains (a few percentage points)

Billing, metering, and collection backbone

Billing, metering, and collection backbone is largely amortized after prior capex waves, delivering steady contribution per billed kWh and supporting distribution EBITDA margins near 30% in 2024; market volume growth is muted but cash generation remains predictable, so focus on maintenance, targeted automation, and capturing float.

- Amortized backbone

- Predictable contribution per kWh

- 2024 distribution EBITDA ~30%

- Maintain, automate, bank the float

Distribution (~8.8–9.0M) and PCHs (≤30 MW) deliver steady cash, ~30% EBITDA

Regulated distribution concessions (~8.8–9.0M customers) deliver stable demand and predictable cash with 2024 distribution EBITDA ~30%. Depreciated PCHs (≤30 MW) provide low‑growth, high‑availability generation funding new investments. Centralized O&M, amortized billing systems and modest digitization lift margins slightly while preserving strong free cash generation.

| Metric | 2024 |

|---|---|

| Concession customers | ~8.8–9.0M |

| Distribution EBITDA margin | ~30% |

| PCH size | ≤30 MW |

What You’re Viewing Is Included

CPFL Energia BCG Matrix

The file you're previewing on this page is the exact BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just the finished, fully formatted analysis built for strategic clarity. It's crafted by strategy experts and ready to edit, print, or present to your team. After buying you'll get the same document delivered straight to your inbox—no surprises, no extra steps.

Visual. Strategic. Downloadable.

Curious where CPFL Energia’s businesses fall—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at strengths and risks, but the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed recommendations, and a ready-to-use Word report plus an Excel summary. Buy the complete analysis to skip the guesswork and get strategic moves you can act on today.

Stars

Utility-scale wind portfolio

Utility-scale wind in Brazil remains fast-growing, with national installed capacity exceeding 20 GW and sustained annual additions, and CPFL holds meaningful installed capacity plus a visible project pipeline supporting growth.

Strong long-term PPAs and declining onshore wind cost curves keep utilization and revenue profiles solid, preserving cash flow visibility for CPFL.

Wind currently soaks up capital, but its share and growth justify continued investment to lock leadership before market maturation.

Utility-scale solar build-out

Utility-scale solar additions accelerated in 2024 and CPFL is winning sites and contracts, with a disclosed pipeline topping 1 GW and several PPAs awarded during the year. Execution speed and strict EPC discipline give CPFL clear heft versus smaller developers, shortening COD timelines. Cash burn is real during construction, but modeled IRRs above low-double digits as assets ramp make returns attractive. Stay on the front foot — scale is the edge.

Free-market retailing (ACL) for C&I

Migration to the free market is expanding fast and CPFL’s strong brand and retail book—about 11 million clients across São Paulo, Paraná and Rio Grande do Sul—positions it to win C&I load. Cross-selling risk management and tailored PPAs has been lifting share in the ACL, while brisk growth requires ongoing sales and hedging muscle. Keep feeding the engine to sustain momentum.

Grid digitalization & smart grid rollouts

Grid digitalization and smart grid rollouts are accelerating in Brazil with clear regulatory support and maturing technologies; CPFL’s deployments cut technical losses and raise reliability, compounding competitive advantage across its concession areas. Capex is front-loaded while efficiency gains and data-driven O&M savings accrue over time, making this a Stars-position asset to press for growth.

- Capex-heavy

- Loss reduction

- Reliability uplift

- Data-driven O&M

Distributed generation for corporates

Corporate and industrial clients increasingly demand predictable green power; CPFL bundles distributed-generation solar with financing and O&M, capturing customers seeking fixed-cost, low-carbon supply. The addressable DG market is expanding amid tariff volatility and rising ESG mandates, with global corporate renewables deals exceeding 30 GW by 2023 and rooftop costs down over 85% since 2010, boosting CPFL share where it bundles energy plus services. Double down while conversion costs continue to fall and customer acquisition costs decline.

- Tag: market_expansion — corporate renewables >30 GW (2023)

- Tag: cost_trend — rooftop solar costs down >85% since 2010

- Tag: CPFL_advantage — bundles: DG + financing + O&M

- Tag: recommendation — scale while conversion costs fall

Brazil: >20 GW wind, ~11m clients

Utility wind: Brazil >20 GW (2024); CPFL has meaningful capacity and pipeline, steady PPAs preserving cash flow. Solar: CPFL disclosed >1 GW pipeline (2024) and strong EPC execution delivering low-double-digit IRRs. Retail/C&I: ~11m clients and ACL wins; DG bundles + financing scale as rooftop costs down >85% since 2010.

| Metric | Figure |

|---|---|

| Brazil wind (2024) | >20 GW |

| CPFL solar pipeline (2024) | >1 GW |

| Retail clients | ~11m |

What is included in the product

In-depth BCG Matrix review of CPFL Energia’s units with strategic moves per quadrant—invest, hold, or divest, plus risks and trends.

One-page CPFL Energia BCG Matrix snapshot that clarifies portfolio pain points for faster executive decisions.

Cash Cows

Regulated distribution concessions

Regulated distribution concessions serve ~8.8 million customers across mature São Paulo and Rio Grande do Sul markets, holding high market share and stable demand. Regulatory tariffs and efficiency gains delivered predictable returns, with 2024 distribution EBITDA margin around 30% and regular ANEEL adjustments supporting cash flow. Low volume growth but strong free cash generation after maintenance capex; milk assets while pursuing selective automation to widen margins.

Legacy small hydro (PCHs)

Legacy small hydro (PCHs) are depreciated assets with deep operational know-how and are defined in Brazil as plants up to 30 MW, delivering stable, low-growth generation. Availability is strong and O&M is efficient, producing reliable cash flows that fund newer bets across CPFL Energia. Focus is on optimizing outages and incremental yield improvements rather than capital-intensive upgrades.

Captive residential & small business sales (ACR)

Captive residential and small-business sales (ACR) show mature demand with CPFL Energia serving roughly 9 million concession customers in 2024, yielding stable volume and high retention within the concession. Tariff pass-through to consumers stabilizes margins against wholesale cost swings, reducing margin volatility. Low marketing needs and steady receivables enable cash harvest strategies while keeping losses and delinquency tightly controlled.

Centralized O&M services for owned fleet

Centralized O&M for CPFL Energia’s owned fleet drives lower per-MW operating cost through shared crews, spares and scheduling; the standardized “factory” approach yields repeatable processes and stable margins, producing steady free cash flow rather than rapid growth.

Incremental digitization—remote monitoring, predictive maintenance—can lift O&M efficiency by a few percentage points and further reinforce cash generation without changing the cash-cow profile.

- Shared services reduce per-MW costs

- Standardized operations keep margins stable

- Low-growth, steady cash drip

- Digitization adds modest efficiency gains (a few percentage points)

Billing, metering, and collection backbone

Billing, metering, and collection backbone is largely amortized after prior capex waves, delivering steady contribution per billed kWh and supporting distribution EBITDA margins near 30% in 2024; market volume growth is muted but cash generation remains predictable, so focus on maintenance, targeted automation, and capturing float.

- Amortized backbone

- Predictable contribution per kWh

- 2024 distribution EBITDA ~30%

- Maintain, automate, bank the float

Distribution (~8.8–9.0M) and PCHs (≤30 MW) deliver steady cash, ~30% EBITDA

Regulated distribution concessions (~8.8–9.0M customers) deliver stable demand and predictable cash with 2024 distribution EBITDA ~30%. Depreciated PCHs (≤30 MW) provide low‑growth, high‑availability generation funding new investments. Centralized O&M, amortized billing systems and modest digitization lift margins slightly while preserving strong free cash generation.

| Metric | 2024 |

|---|---|

| Concession customers | ~8.8–9.0M |

| Distribution EBITDA margin | ~30% |

| PCH size | ≤30 MW |

What You’re Viewing Is Included

CPFL Energia BCG Matrix

The file you're previewing on this page is the exact BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just the finished, fully formatted analysis built for strategic clarity. It's crafted by strategy experts and ready to edit, print, or present to your team. After buying you'll get the same document delivered straight to your inbox—no surprises, no extra steps.

Original: $10.00

-65%$10.00

$3.50Description

Visual. Strategic. Downloadable.

Curious where CPFL Energia’s businesses fall—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at strengths and risks, but the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed recommendations, and a ready-to-use Word report plus an Excel summary. Buy the complete analysis to skip the guesswork and get strategic moves you can act on today.

Stars

Utility-scale wind portfolio

Utility-scale wind in Brazil remains fast-growing, with national installed capacity exceeding 20 GW and sustained annual additions, and CPFL holds meaningful installed capacity plus a visible project pipeline supporting growth.

Strong long-term PPAs and declining onshore wind cost curves keep utilization and revenue profiles solid, preserving cash flow visibility for CPFL.

Wind currently soaks up capital, but its share and growth justify continued investment to lock leadership before market maturation.

Utility-scale solar build-out

Utility-scale solar additions accelerated in 2024 and CPFL is winning sites and contracts, with a disclosed pipeline topping 1 GW and several PPAs awarded during the year. Execution speed and strict EPC discipline give CPFL clear heft versus smaller developers, shortening COD timelines. Cash burn is real during construction, but modeled IRRs above low-double digits as assets ramp make returns attractive. Stay on the front foot — scale is the edge.

Free-market retailing (ACL) for C&I

Migration to the free market is expanding fast and CPFL’s strong brand and retail book—about 11 million clients across São Paulo, Paraná and Rio Grande do Sul—positions it to win C&I load. Cross-selling risk management and tailored PPAs has been lifting share in the ACL, while brisk growth requires ongoing sales and hedging muscle. Keep feeding the engine to sustain momentum.

Grid digitalization & smart grid rollouts

Grid digitalization and smart grid rollouts are accelerating in Brazil with clear regulatory support and maturing technologies; CPFL’s deployments cut technical losses and raise reliability, compounding competitive advantage across its concession areas. Capex is front-loaded while efficiency gains and data-driven O&M savings accrue over time, making this a Stars-position asset to press for growth.

- Capex-heavy

- Loss reduction

- Reliability uplift

- Data-driven O&M

Distributed generation for corporates

Corporate and industrial clients increasingly demand predictable green power; CPFL bundles distributed-generation solar with financing and O&M, capturing customers seeking fixed-cost, low-carbon supply. The addressable DG market is expanding amid tariff volatility and rising ESG mandates, with global corporate renewables deals exceeding 30 GW by 2023 and rooftop costs down over 85% since 2010, boosting CPFL share where it bundles energy plus services. Double down while conversion costs continue to fall and customer acquisition costs decline.

- Tag: market_expansion — corporate renewables >30 GW (2023)

- Tag: cost_trend — rooftop solar costs down >85% since 2010

- Tag: CPFL_advantage — bundles: DG + financing + O&M

- Tag: recommendation — scale while conversion costs fall

Brazil: >20 GW wind, ~11m clients

Utility wind: Brazil >20 GW (2024); CPFL has meaningful capacity and pipeline, steady PPAs preserving cash flow. Solar: CPFL disclosed >1 GW pipeline (2024) and strong EPC execution delivering low-double-digit IRRs. Retail/C&I: ~11m clients and ACL wins; DG bundles + financing scale as rooftop costs down >85% since 2010.

| Metric | Figure |

|---|---|

| Brazil wind (2024) | >20 GW |

| CPFL solar pipeline (2024) | >1 GW |

| Retail clients | ~11m |

What is included in the product

In-depth BCG Matrix review of CPFL Energia’s units with strategic moves per quadrant—invest, hold, or divest, plus risks and trends.

One-page CPFL Energia BCG Matrix snapshot that clarifies portfolio pain points for faster executive decisions.

Cash Cows

Regulated distribution concessions

Regulated distribution concessions serve ~8.8 million customers across mature São Paulo and Rio Grande do Sul markets, holding high market share and stable demand. Regulatory tariffs and efficiency gains delivered predictable returns, with 2024 distribution EBITDA margin around 30% and regular ANEEL adjustments supporting cash flow. Low volume growth but strong free cash generation after maintenance capex; milk assets while pursuing selective automation to widen margins.

Legacy small hydro (PCHs)

Legacy small hydro (PCHs) are depreciated assets with deep operational know-how and are defined in Brazil as plants up to 30 MW, delivering stable, low-growth generation. Availability is strong and O&M is efficient, producing reliable cash flows that fund newer bets across CPFL Energia. Focus is on optimizing outages and incremental yield improvements rather than capital-intensive upgrades.

Captive residential & small business sales (ACR)

Captive residential and small-business sales (ACR) show mature demand with CPFL Energia serving roughly 9 million concession customers in 2024, yielding stable volume and high retention within the concession. Tariff pass-through to consumers stabilizes margins against wholesale cost swings, reducing margin volatility. Low marketing needs and steady receivables enable cash harvest strategies while keeping losses and delinquency tightly controlled.

Centralized O&M services for owned fleet

Centralized O&M for CPFL Energia’s owned fleet drives lower per-MW operating cost through shared crews, spares and scheduling; the standardized “factory” approach yields repeatable processes and stable margins, producing steady free cash flow rather than rapid growth.

Incremental digitization—remote monitoring, predictive maintenance—can lift O&M efficiency by a few percentage points and further reinforce cash generation without changing the cash-cow profile.

- Shared services reduce per-MW costs

- Standardized operations keep margins stable

- Low-growth, steady cash drip

- Digitization adds modest efficiency gains (a few percentage points)

Billing, metering, and collection backbone

Billing, metering, and collection backbone is largely amortized after prior capex waves, delivering steady contribution per billed kWh and supporting distribution EBITDA margins near 30% in 2024; market volume growth is muted but cash generation remains predictable, so focus on maintenance, targeted automation, and capturing float.

- Amortized backbone

- Predictable contribution per kWh

- 2024 distribution EBITDA ~30%

- Maintain, automate, bank the float

Distribution (~8.8–9.0M) and PCHs (≤30 MW) deliver steady cash, ~30% EBITDA

Regulated distribution concessions (~8.8–9.0M customers) deliver stable demand and predictable cash with 2024 distribution EBITDA ~30%. Depreciated PCHs (≤30 MW) provide low‑growth, high‑availability generation funding new investments. Centralized O&M, amortized billing systems and modest digitization lift margins slightly while preserving strong free cash generation.

| Metric | 2024 |

|---|---|

| Concession customers | ~8.8–9.0M |

| Distribution EBITDA margin | ~30% |

| PCH size | ≤30 MW |

What You’re Viewing Is Included

CPFL Energia BCG Matrix

The file you're previewing on this page is the exact BCG Matrix report you'll receive after purchase. No watermarks, no demo content—just the finished, fully formatted analysis built for strategic clarity. It's crafted by strategy experts and ready to edit, print, or present to your team. After buying you'll get the same document delivered straight to your inbox—no surprises, no extra steps.