CPI Card Business Model Canvas

Business Model Canvas: Secure payment-card solutions, partnerships, and revenue drivers

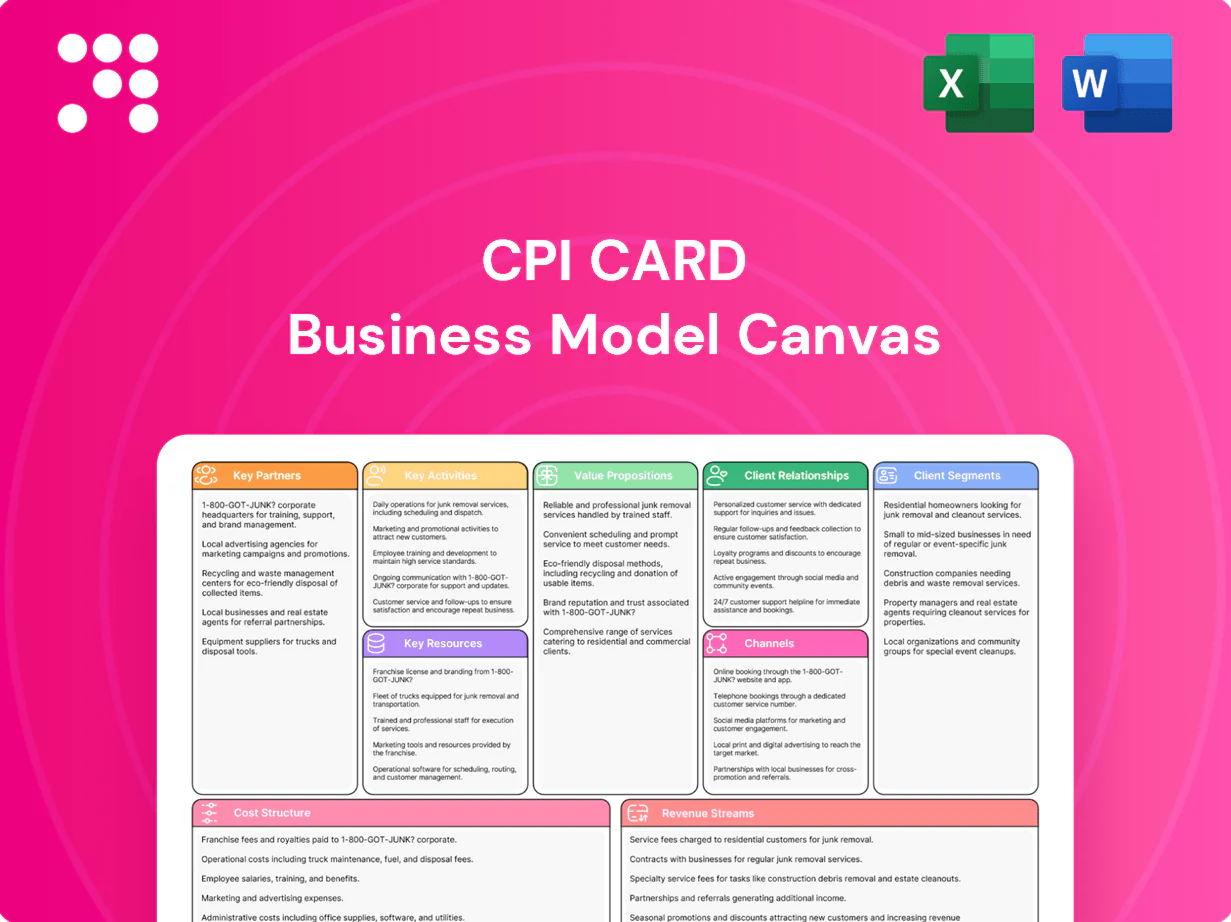

Explore CPI Card’s Business Model Canvas to see how the company creates value through secure payment solutions, strategic partnerships, and diversified revenue streams; this brief snapshot highlights key customer segments and competitive advantages. For a complete, editable breakdown—covering cost structure, revenue drivers, and actionable strategic recommendations—purchase the full Business Model Canvas to inform your analysis or presentation.

Partnerships

Card networks

Alliances with Visa, Mastercard, Discover, and AmEx ensure certification, compliance, and acceptance across four major networks.

These relationships enable EMV, contactless, and tokenization standards, driving global interoperability across three core security protocols.

Co-marketing and innovation pilots help speed new product adoption, while ongoing audits and annual recertifications maintain trust and interoperability.

Chip and materials suppliers

Secure chip, inlay, antenna, and eco-substrate providers underpin CPI Card quality and sustainability, with 2024 supplier scorecards averaging 98% on-time delivery and 0.12% defect rates across critical components.

Digital wallets and token service providers

Partnerships with Apple Pay, Google Pay, Samsung Pay and certified TSPs enable CPI Card to deliver native digital issuance tied to the 4.6 billion global digital wallet users in 2024. APIs and SDKs streamline provisioning and lifecycle management, reducing integration cycles. Rigorous compliance and token testing shorten issuer time-to-market, while co-development improves user experience and security.

Core banking and fintech platforms

Integrations with cores, program managers, and neobanks expand CPI Card's reach into ≈4,700 US banks (FDIC, 2024) and 200+ neobanks (2024), enabling volume scale and faster issuer onboarding. Pre-built connectors cut issuer IT effort and time-to-market, while joint go-to-market bundles target SMB banks and fintechs. Data-sharing drives richer personalization and improved analytics.

- reach: ≈4,700 US banks (FDIC, 2024)

- scale: 200+ neobanks (2024)

- benefit: lower IT effort, bundled SMB GTM, enhanced analytics

Logistics and personalization bureaus

Mailing, fulfillment, and personalization bureaus enable CPI Card to scale production surges—2024 industry data show 3PL-enabled peak capacity boosts of 20–40%—while distributed facilities improve SLAs and regional delivery speed by shortening transit times and reducing last-mile costs. Redundant sites enhance business continuity and risk mitigation; co-located services cut cycle times and lower unit costs through reduced handling and transport.

EMV-certified card issuance: 4.6B digital wallets, 4,700 banks reachable

Alliances with Visa, Mastercard, Discover, AmEx and TSPs ensure EMV/contactless/tokenization certification and acceptance, supporting 4.6B digital wallet users (2024).

Supply partners deliver chips, inlays and eco-substrates with 98% on-time and 0.12% defect (2024), while 3PLs boost peak capacity +20–40%.

Integrations reach ≈4,700 US banks and 200+ neobanks (2024), shortening issuer time-to-market.

| Metric | Value (2024) |

|---|---|

| Digital wallets | 4.6B |

| US banks reachable | ≈4,700 |

| Neobanks | 200+ |

| Supplier OT delivery | 98% |

| Critical defect rate | 0.12% |

| 3PL peak capacity | +20–40% |

What is included in the product

A comprehensive pre-written Business Model Canvas for CPI Card outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships; includes SWOT, competitive advantages and actionable insights to support presentations, funding and strategic decisions.

Condenses CPI Card’s payroll and prepaid program complexity into one editable canvas so teams can map value propositions, key partners, revenue streams and compliance risks—saving hours of alignment work and easing cross‑functional decision making.

Activities

Secure card manufacturing

CPI Card manufactures EMV, contactless, metal and eco-focused cards at scale, leveraging EMV standards used across 200+ countries and networks. Facilities maintain PCI DSS and industry quality controls plus strict physical security and chain-of-custody. Operations optimize throughput and yield to meet peak issuer demand and manage high SKU complexity across programs.

Personalization and fulfillment

Encode, print and package EMV and mag-stripe cards with PIN mailers and inserts, supporting PCI DSS and ISO 9001 controls. Execute same-day and instant issuance workflows—industry-standard instant issuance can be completed in under 5 minutes. Track and audit every unit for compliance with immutable audit trails. Coordinate logistics with SLA-backed, end-to-end traceable delivery.

Digital issuance and tokenization

Provisioning of virtual and mobile wallet cards—serving part of the 3.4 billion mobile wallet users in 2024—includes tokenization and real-time lifecycle management (activation, reissuance, token updates). Provide RESTful APIs for issuer integration, maintain PCI DSS-grade security and 99.99% uptime SLAs to ensure transaction integrity and availability.

Software and services

Offer card management portals, onboarding tools, and analytics with 24/7 customer support and implementation services; integrate fraud, risk, and compliance features aligned to 2024 network rule cycles and updates to EMV/tokenization standards.

- portals & onboarding

- 24/7 support & implementation

- fraud, risk, compliance

- platform updates per 2024 network rules

Quality, compliance, and R&D

Maintain PCI DSS v4.0 and network/regulatory certifications with the March 31, 2024 transition in scope; perform continuous testing and quarterly penetration tests plus annual third-party audits; innovate using sustainable substrates and premium metal/eco‑polymer form factors; pilot biometric sensors and dynamic CVV solutions with issuer partners to capture new issuance demand.

- PCI DSS v4.0 deadline: March 31, 2024

- Quarterly penetration tests

- Annual third‑party audits

- Sustainable substrates & premium form factors

- Biometric & dynamic CVV pilots with issuers

Global EMV and contactless card services: instant issuance under 5 minutes, tokenization, 99.99% uptime

CPI Card runs high-volume EMV, contactless, metal and eco-card manufacturing across PCI DSS v4.0 certified facilities serving 200+ countries, with throughput and SKU management to meet peak issuer demand. Operations provide encoding, printing, instant issuance (<5 minutes), tokenization and 99.99% uptime APIs for provisioning and lifecycle management. Continuous security testing includes quarterly pen tests and annual third‑party audits.

| Metric | 2024 value |

|---|---|

| Mobile wallet users | 3.4 billion |

| PCI DSS v4.0 deadline | Mar 31, 2024 |

| Uptime SLA | 99.99% |

| EMV reach | 200+ countries |

Delivered as Displayed

Business Model Canvas

The document previewed here is the actual CPI Card Business Model Canvas, not a mockup, and reflects the exact layout and content you’ll receive after purchase. When you complete your order, you’ll download this same professional file ready to edit and present. No surprises—what you see is what you get.

Business Model Canvas: Secure payment-card solutions, partnerships, and revenue drivers

Explore CPI Card’s Business Model Canvas to see how the company creates value through secure payment solutions, strategic partnerships, and diversified revenue streams; this brief snapshot highlights key customer segments and competitive advantages. For a complete, editable breakdown—covering cost structure, revenue drivers, and actionable strategic recommendations—purchase the full Business Model Canvas to inform your analysis or presentation.

Partnerships

Card networks

Alliances with Visa, Mastercard, Discover, and AmEx ensure certification, compliance, and acceptance across four major networks.

These relationships enable EMV, contactless, and tokenization standards, driving global interoperability across three core security protocols.

Co-marketing and innovation pilots help speed new product adoption, while ongoing audits and annual recertifications maintain trust and interoperability.

Chip and materials suppliers

Secure chip, inlay, antenna, and eco-substrate providers underpin CPI Card quality and sustainability, with 2024 supplier scorecards averaging 98% on-time delivery and 0.12% defect rates across critical components.

Digital wallets and token service providers

Partnerships with Apple Pay, Google Pay, Samsung Pay and certified TSPs enable CPI Card to deliver native digital issuance tied to the 4.6 billion global digital wallet users in 2024. APIs and SDKs streamline provisioning and lifecycle management, reducing integration cycles. Rigorous compliance and token testing shorten issuer time-to-market, while co-development improves user experience and security.

Core banking and fintech platforms

Integrations with cores, program managers, and neobanks expand CPI Card's reach into ≈4,700 US banks (FDIC, 2024) and 200+ neobanks (2024), enabling volume scale and faster issuer onboarding. Pre-built connectors cut issuer IT effort and time-to-market, while joint go-to-market bundles target SMB banks and fintechs. Data-sharing drives richer personalization and improved analytics.

- reach: ≈4,700 US banks (FDIC, 2024)

- scale: 200+ neobanks (2024)

- benefit: lower IT effort, bundled SMB GTM, enhanced analytics

Logistics and personalization bureaus

Mailing, fulfillment, and personalization bureaus enable CPI Card to scale production surges—2024 industry data show 3PL-enabled peak capacity boosts of 20–40%—while distributed facilities improve SLAs and regional delivery speed by shortening transit times and reducing last-mile costs. Redundant sites enhance business continuity and risk mitigation; co-located services cut cycle times and lower unit costs through reduced handling and transport.

EMV-certified card issuance: 4.6B digital wallets, 4,700 banks reachable

Alliances with Visa, Mastercard, Discover, AmEx and TSPs ensure EMV/contactless/tokenization certification and acceptance, supporting 4.6B digital wallet users (2024).

Supply partners deliver chips, inlays and eco-substrates with 98% on-time and 0.12% defect (2024), while 3PLs boost peak capacity +20–40%.

Integrations reach ≈4,700 US banks and 200+ neobanks (2024), shortening issuer time-to-market.

| Metric | Value (2024) |

|---|---|

| Digital wallets | 4.6B |

| US banks reachable | ≈4,700 |

| Neobanks | 200+ |

| Supplier OT delivery | 98% |

| Critical defect rate | 0.12% |

| 3PL peak capacity | +20–40% |

What is included in the product

A comprehensive pre-written Business Model Canvas for CPI Card outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships; includes SWOT, competitive advantages and actionable insights to support presentations, funding and strategic decisions.

Condenses CPI Card’s payroll and prepaid program complexity into one editable canvas so teams can map value propositions, key partners, revenue streams and compliance risks—saving hours of alignment work and easing cross‑functional decision making.

Activities

Secure card manufacturing

CPI Card manufactures EMV, contactless, metal and eco-focused cards at scale, leveraging EMV standards used across 200+ countries and networks. Facilities maintain PCI DSS and industry quality controls plus strict physical security and chain-of-custody. Operations optimize throughput and yield to meet peak issuer demand and manage high SKU complexity across programs.

Personalization and fulfillment

Encode, print and package EMV and mag-stripe cards with PIN mailers and inserts, supporting PCI DSS and ISO 9001 controls. Execute same-day and instant issuance workflows—industry-standard instant issuance can be completed in under 5 minutes. Track and audit every unit for compliance with immutable audit trails. Coordinate logistics with SLA-backed, end-to-end traceable delivery.

Digital issuance and tokenization

Provisioning of virtual and mobile wallet cards—serving part of the 3.4 billion mobile wallet users in 2024—includes tokenization and real-time lifecycle management (activation, reissuance, token updates). Provide RESTful APIs for issuer integration, maintain PCI DSS-grade security and 99.99% uptime SLAs to ensure transaction integrity and availability.

Software and services

Offer card management portals, onboarding tools, and analytics with 24/7 customer support and implementation services; integrate fraud, risk, and compliance features aligned to 2024 network rule cycles and updates to EMV/tokenization standards.

- portals & onboarding

- 24/7 support & implementation

- fraud, risk, compliance

- platform updates per 2024 network rules

Quality, compliance, and R&D

Maintain PCI DSS v4.0 and network/regulatory certifications with the March 31, 2024 transition in scope; perform continuous testing and quarterly penetration tests plus annual third-party audits; innovate using sustainable substrates and premium metal/eco‑polymer form factors; pilot biometric sensors and dynamic CVV solutions with issuer partners to capture new issuance demand.

- PCI DSS v4.0 deadline: March 31, 2024

- Quarterly penetration tests

- Annual third‑party audits

- Sustainable substrates & premium form factors

- Biometric & dynamic CVV pilots with issuers

Global EMV and contactless card services: instant issuance under 5 minutes, tokenization, 99.99% uptime

CPI Card runs high-volume EMV, contactless, metal and eco-card manufacturing across PCI DSS v4.0 certified facilities serving 200+ countries, with throughput and SKU management to meet peak issuer demand. Operations provide encoding, printing, instant issuance (<5 minutes), tokenization and 99.99% uptime APIs for provisioning and lifecycle management. Continuous security testing includes quarterly pen tests and annual third‑party audits.

| Metric | 2024 value |

|---|---|

| Mobile wallet users | 3.4 billion |

| PCI DSS v4.0 deadline | Mar 31, 2024 |

| Uptime SLA | 99.99% |

| EMV reach | 200+ countries |

Delivered as Displayed

Business Model Canvas

The document previewed here is the actual CPI Card Business Model Canvas, not a mockup, and reflects the exact layout and content you’ll receive after purchase. When you complete your order, you’ll download this same professional file ready to edit and present. No surprises—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: Secure payment-card solutions, partnerships, and revenue drivers

Explore CPI Card’s Business Model Canvas to see how the company creates value through secure payment solutions, strategic partnerships, and diversified revenue streams; this brief snapshot highlights key customer segments and competitive advantages. For a complete, editable breakdown—covering cost structure, revenue drivers, and actionable strategic recommendations—purchase the full Business Model Canvas to inform your analysis or presentation.

Partnerships

Card networks

Alliances with Visa, Mastercard, Discover, and AmEx ensure certification, compliance, and acceptance across four major networks.

These relationships enable EMV, contactless, and tokenization standards, driving global interoperability across three core security protocols.

Co-marketing and innovation pilots help speed new product adoption, while ongoing audits and annual recertifications maintain trust and interoperability.

Chip and materials suppliers

Secure chip, inlay, antenna, and eco-substrate providers underpin CPI Card quality and sustainability, with 2024 supplier scorecards averaging 98% on-time delivery and 0.12% defect rates across critical components.

Digital wallets and token service providers

Partnerships with Apple Pay, Google Pay, Samsung Pay and certified TSPs enable CPI Card to deliver native digital issuance tied to the 4.6 billion global digital wallet users in 2024. APIs and SDKs streamline provisioning and lifecycle management, reducing integration cycles. Rigorous compliance and token testing shorten issuer time-to-market, while co-development improves user experience and security.

Core banking and fintech platforms

Integrations with cores, program managers, and neobanks expand CPI Card's reach into ≈4,700 US banks (FDIC, 2024) and 200+ neobanks (2024), enabling volume scale and faster issuer onboarding. Pre-built connectors cut issuer IT effort and time-to-market, while joint go-to-market bundles target SMB banks and fintechs. Data-sharing drives richer personalization and improved analytics.

- reach: ≈4,700 US banks (FDIC, 2024)

- scale: 200+ neobanks (2024)

- benefit: lower IT effort, bundled SMB GTM, enhanced analytics

Logistics and personalization bureaus

Mailing, fulfillment, and personalization bureaus enable CPI Card to scale production surges—2024 industry data show 3PL-enabled peak capacity boosts of 20–40%—while distributed facilities improve SLAs and regional delivery speed by shortening transit times and reducing last-mile costs. Redundant sites enhance business continuity and risk mitigation; co-located services cut cycle times and lower unit costs through reduced handling and transport.

EMV-certified card issuance: 4.6B digital wallets, 4,700 banks reachable

Alliances with Visa, Mastercard, Discover, AmEx and TSPs ensure EMV/contactless/tokenization certification and acceptance, supporting 4.6B digital wallet users (2024).

Supply partners deliver chips, inlays and eco-substrates with 98% on-time and 0.12% defect (2024), while 3PLs boost peak capacity +20–40%.

Integrations reach ≈4,700 US banks and 200+ neobanks (2024), shortening issuer time-to-market.

| Metric | Value (2024) |

|---|---|

| Digital wallets | 4.6B |

| US banks reachable | ≈4,700 |

| Neobanks | 200+ |

| Supplier OT delivery | 98% |

| Critical defect rate | 0.12% |

| 3PL peak capacity | +20–40% |

What is included in the product

A comprehensive pre-written Business Model Canvas for CPI Card outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships; includes SWOT, competitive advantages and actionable insights to support presentations, funding and strategic decisions.

Condenses CPI Card’s payroll and prepaid program complexity into one editable canvas so teams can map value propositions, key partners, revenue streams and compliance risks—saving hours of alignment work and easing cross‑functional decision making.

Activities

Secure card manufacturing

CPI Card manufactures EMV, contactless, metal and eco-focused cards at scale, leveraging EMV standards used across 200+ countries and networks. Facilities maintain PCI DSS and industry quality controls plus strict physical security and chain-of-custody. Operations optimize throughput and yield to meet peak issuer demand and manage high SKU complexity across programs.

Personalization and fulfillment

Encode, print and package EMV and mag-stripe cards with PIN mailers and inserts, supporting PCI DSS and ISO 9001 controls. Execute same-day and instant issuance workflows—industry-standard instant issuance can be completed in under 5 minutes. Track and audit every unit for compliance with immutable audit trails. Coordinate logistics with SLA-backed, end-to-end traceable delivery.

Digital issuance and tokenization

Provisioning of virtual and mobile wallet cards—serving part of the 3.4 billion mobile wallet users in 2024—includes tokenization and real-time lifecycle management (activation, reissuance, token updates). Provide RESTful APIs for issuer integration, maintain PCI DSS-grade security and 99.99% uptime SLAs to ensure transaction integrity and availability.

Software and services

Offer card management portals, onboarding tools, and analytics with 24/7 customer support and implementation services; integrate fraud, risk, and compliance features aligned to 2024 network rule cycles and updates to EMV/tokenization standards.

- portals & onboarding

- 24/7 support & implementation

- fraud, risk, compliance

- platform updates per 2024 network rules

Quality, compliance, and R&D

Maintain PCI DSS v4.0 and network/regulatory certifications with the March 31, 2024 transition in scope; perform continuous testing and quarterly penetration tests plus annual third-party audits; innovate using sustainable substrates and premium metal/eco‑polymer form factors; pilot biometric sensors and dynamic CVV solutions with issuer partners to capture new issuance demand.

- PCI DSS v4.0 deadline: March 31, 2024

- Quarterly penetration tests

- Annual third‑party audits

- Sustainable substrates & premium form factors

- Biometric & dynamic CVV pilots with issuers

Global EMV and contactless card services: instant issuance under 5 minutes, tokenization, 99.99% uptime

CPI Card runs high-volume EMV, contactless, metal and eco-card manufacturing across PCI DSS v4.0 certified facilities serving 200+ countries, with throughput and SKU management to meet peak issuer demand. Operations provide encoding, printing, instant issuance (<5 minutes), tokenization and 99.99% uptime APIs for provisioning and lifecycle management. Continuous security testing includes quarterly pen tests and annual third‑party audits.

| Metric | 2024 value |

|---|---|

| Mobile wallet users | 3.4 billion |

| PCI DSS v4.0 deadline | Mar 31, 2024 |

| Uptime SLA | 99.99% |

| EMV reach | 200+ countries |

Delivered as Displayed

Business Model Canvas

The document previewed here is the actual CPI Card Business Model Canvas, not a mockup, and reflects the exact layout and content you’ll receive after purchase. When you complete your order, you’ll download this same professional file ready to edit and present. No surprises—what you see is what you get.