CPP Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

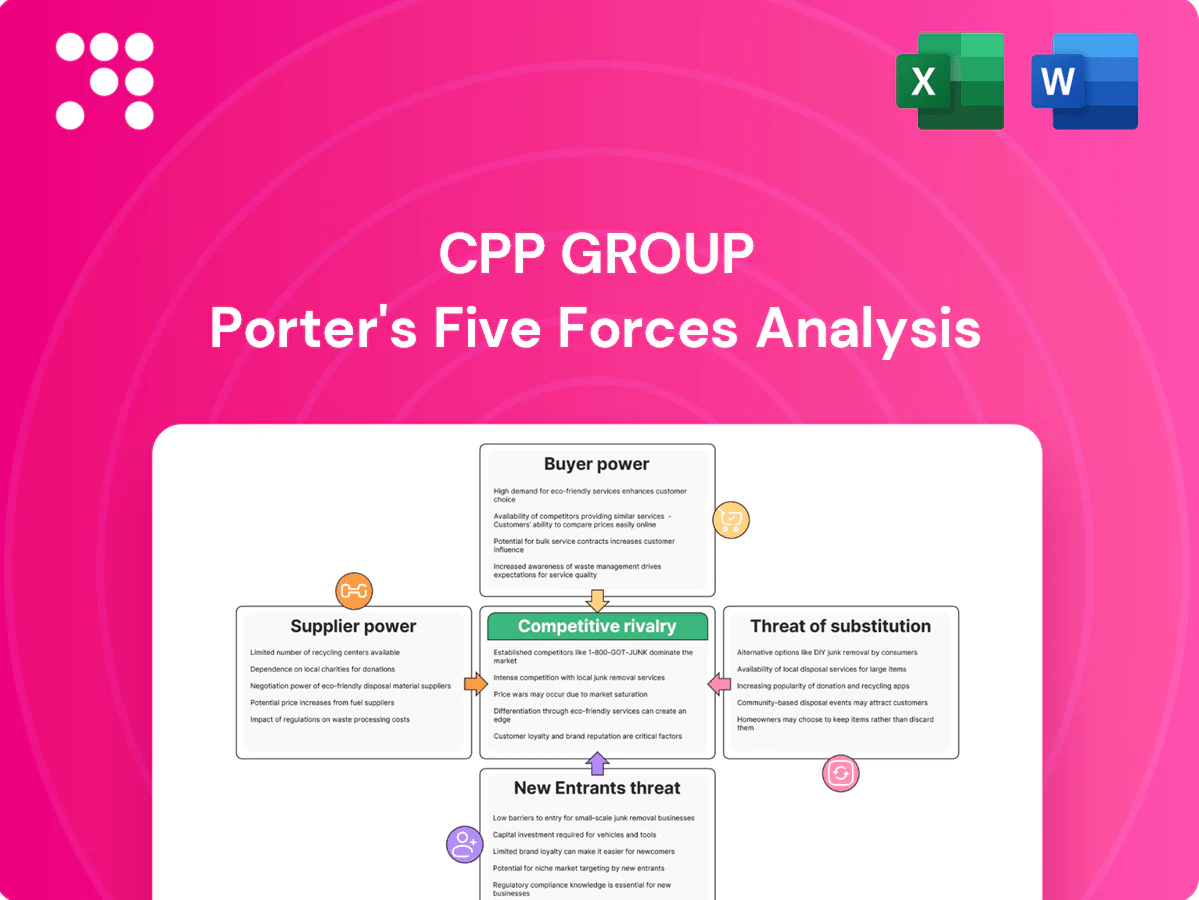

CPP Group faces moderate buyer power and regulatory pressure, while substitute threats and digital entrants shape margins—supplier influence is limited by scale. This snapshot highlights strategic levers in pricing, distribution and product diversification. The full Porter's Five Forces Analysis unpacks force-by-force ratings, visuals and business implications for CPP Group. Unlock the complete report to drive informed investment and strategic decisions.

Suppliers Bargaining Power

Dependence on underwriters

CPP Group relies on insurance carriers and reinsurers to underwrite and price risk, giving well-rated underwriters leverage to demand tighter terms—global reinsurance pricing rose c.11% at 1/1/2024 renewals (Guy Carpenter), squeezing insurer margins in hard markets.

Critical tech and cyber vendors

Core systems, cybersecurity tools and identity-monitoring providers are essential to CPPs product delivery; the three national credit bureaus dominate identity data access in key markets, concentrating supplier power. The global cybersecurity market reached about $218 billion in 2024, increasing supplier leverage on pricing. CPP can mitigate via volume agreements and multi-sourcing, but high integration and switching costs keep vendors influential. SLAs and performance-based fees are used to rebalance power.

Data and verification providers

Credit bureaus, KYC/AML and fraud-data suppliers directly shape CPP Group’s product pricing and loss control by determining risk accuracy; in 2024 the top three credit bureaus held an estimated >80% share in major markets, raising supplier leverage. Layering alternative data sources and proprietary models reduces lock-in, but GDPR, FCA AML rules and KYC mandates limit easy substitution.

BPO and assistance networks

BPO call centers, claims TPAs and repair/replacement networks drive CPP Group service levels and cost; the global contact center market reached 379 billion USD in 2024, concentrating operational leverage in suppliers that control capacity and expertise. Regional fragmentation enables competitive bidding, but peak-demand surges and specialized repairs can shift bargaining power to suppliers; pay-for-outcomes and strict KPIs rebalance incentives.

- Call centers: scale and peak capacity

- TPA claims: accuracy and speed

- Repair networks: specialized skills

- Mitigants: competitive bids, KPIs, outcome payments

Regulatory and compliance services

External legal, compliance and audit expertise is required across multiple jurisdictions, and specialist scarcity elevates fees and supplier influence; Big Four advisory revenues totaled roughly USD 200bn in 2024, underscoring concentrated supplier power. Building internal capability reduces dependency and can cut advisory spend over time. Cross-market standardization of policies and platforms lowers advisory hours and supplier leverage.

- Specialist scarcity raises fees and influence

- Big Four ~USD 200bn 2024 revenue highlights concentration

- Internal capability reduces long-term external spend

- Cross-market standardization lowers advisory hours

+11% reinsurance; bureaus >80% dominance

Suppliers (reinsurers, credit bureaus, cybersecurity and BPOs) hold significant leverage for CPP Group: reinsurance pricing rose c.11% at 1/1/2024 and top three credit bureaus hold >80% market share. Cybersecurity market ~USD 218bn and contact center market ~USD 379bn in 2024 increase vendor pricing power. Mitigants: multi-sourcing, SLAs, outcome fees and internal capability build.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +11% price (1/1/2024) | Higher terms |

| Credit bureaus | >80% share | Data lock-in |

| Cybersecurity | USD 218bn | Pricing power |

| Contact centers | USD 379bn | Operational leverage |

| Big Four | ~USD 200bn | Advisory scarcity |

What is included in the product

Tailored Porter’s Five Forces analysis for CPP Group, uncovering competitive pressures, buyer and supplier influence, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

A concise one-sheet Porter's Five Forces for CPP Group that quickly surfaces competitive pressures and recommended strategic moves, ready to drop into pitch decks or boardroom slides. Customize intensity levels as market conditions change to prioritize actions and relieve analysis bottlenecks without complex tools.

Customers Bargaining Power

Large distribution partners

Banks, telcos and retailers bundle CPP products into customer offers, aggregating large volumes and giving distributors substantial leverage. Their scale and low switching costs translate into strong pricing and contract power, with CPP's 2024 channel-concentrated model seeing over 50% of revenues tied to top partners. This revenue concentration raises renegotiation exposure, though co-created products and joint go-to-market models can deepen ties and reduce pure price pressure.

End-consumer price sensitivity

Consumers treat card protection and gadget insurance as semi-commodities, with 2024 Statista data showing about 59% of UK shoppers using comparison sites for small insurances, amplifying price sensitivity. Monthly subscription models and easy cancellations increase bargaining power and churn risk. Clear value proofs — rapid claim turnaround, bundled add-ons — demonstrably lower price elasticity. Transparent terms and fair claims handling sustain willingness to pay.

Alternative partner offerings

Partners can source similar covers from global insurers or insurtech MGAs, with insurtech market investment still in the low billions annual range in 2024, increasing competitive options and buyer leverage in RFPs.

CPP can offset pure price comparisons by demonstrating UX, data-insight-driven underwriting and reported conversion lifts (often cited in the 10–30% range by platform providers).

Deep embedded integration—API, single-sign-on and policy administration links—raises switching costs for partners, making long-term deals and higher-margin bundles more defensible.

Regulatory scrutiny on add-ons

Multi-year renegotiation cycles

Multi-year renegotiation cycles concentrate 100% of contracted volume at discrete renewal points, enabling buyers to extract concessions on price, SLAs and revenue share; CPP’s leverage rises when retention and cross-sell performance remain strong through the cycle.

- Renewal risk: 100% of volume at renegotiation

- Buyer tactics: price, SLA, revenue-share concessions

- Leverage drivers: high retention, cross-sell

- Mitigation: pilots and rapid rollouts to secure renewals at acceptable margins

Bargaining power: >50% revenue tied; 59% compare-site use

Bargaining power high: >50% revenues tied to top partners (2024), enabling buyer leverage at renewals; 59% UK shoppers use comparison sites for small insurances (Statista 2024), raising price sensitivity. Deep integration and compliance (FCA Consumer Duty Jul 2023) raise switching costs and can mitigate price pressure.

| Metric | Value (2024) |

|---|---|

| Revenue concentration | >50% |

| Comparison-site use | 59% |

| Regulator | FCA Consumer Duty Jul 2023 |

Same Document Delivered

CPP Group Porter's Five Forces Analysis

This preview shows the exact CPP Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the final, professionally formatted analysis, ready for download and immediate use. You’re viewing the same deliverable that will be available to you instantly upon payment.

From Overview to Strategy Blueprint

CPP Group faces moderate buyer power and regulatory pressure, while substitute threats and digital entrants shape margins—supplier influence is limited by scale. This snapshot highlights strategic levers in pricing, distribution and product diversification. The full Porter's Five Forces Analysis unpacks force-by-force ratings, visuals and business implications for CPP Group. Unlock the complete report to drive informed investment and strategic decisions.

Suppliers Bargaining Power

Dependence on underwriters

CPP Group relies on insurance carriers and reinsurers to underwrite and price risk, giving well-rated underwriters leverage to demand tighter terms—global reinsurance pricing rose c.11% at 1/1/2024 renewals (Guy Carpenter), squeezing insurer margins in hard markets.

Critical tech and cyber vendors

Core systems, cybersecurity tools and identity-monitoring providers are essential to CPPs product delivery; the three national credit bureaus dominate identity data access in key markets, concentrating supplier power. The global cybersecurity market reached about $218 billion in 2024, increasing supplier leverage on pricing. CPP can mitigate via volume agreements and multi-sourcing, but high integration and switching costs keep vendors influential. SLAs and performance-based fees are used to rebalance power.

Data and verification providers

Credit bureaus, KYC/AML and fraud-data suppliers directly shape CPP Group’s product pricing and loss control by determining risk accuracy; in 2024 the top three credit bureaus held an estimated >80% share in major markets, raising supplier leverage. Layering alternative data sources and proprietary models reduces lock-in, but GDPR, FCA AML rules and KYC mandates limit easy substitution.

BPO and assistance networks

BPO call centers, claims TPAs and repair/replacement networks drive CPP Group service levels and cost; the global contact center market reached 379 billion USD in 2024, concentrating operational leverage in suppliers that control capacity and expertise. Regional fragmentation enables competitive bidding, but peak-demand surges and specialized repairs can shift bargaining power to suppliers; pay-for-outcomes and strict KPIs rebalance incentives.

- Call centers: scale and peak capacity

- TPA claims: accuracy and speed

- Repair networks: specialized skills

- Mitigants: competitive bids, KPIs, outcome payments

Regulatory and compliance services

External legal, compliance and audit expertise is required across multiple jurisdictions, and specialist scarcity elevates fees and supplier influence; Big Four advisory revenues totaled roughly USD 200bn in 2024, underscoring concentrated supplier power. Building internal capability reduces dependency and can cut advisory spend over time. Cross-market standardization of policies and platforms lowers advisory hours and supplier leverage.

- Specialist scarcity raises fees and influence

- Big Four ~USD 200bn 2024 revenue highlights concentration

- Internal capability reduces long-term external spend

- Cross-market standardization lowers advisory hours

+11% reinsurance; bureaus >80% dominance

Suppliers (reinsurers, credit bureaus, cybersecurity and BPOs) hold significant leverage for CPP Group: reinsurance pricing rose c.11% at 1/1/2024 and top three credit bureaus hold >80% market share. Cybersecurity market ~USD 218bn and contact center market ~USD 379bn in 2024 increase vendor pricing power. Mitigants: multi-sourcing, SLAs, outcome fees and internal capability build.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +11% price (1/1/2024) | Higher terms |

| Credit bureaus | >80% share | Data lock-in |

| Cybersecurity | USD 218bn | Pricing power |

| Contact centers | USD 379bn | Operational leverage |

| Big Four | ~USD 200bn | Advisory scarcity |

What is included in the product

Tailored Porter’s Five Forces analysis for CPP Group, uncovering competitive pressures, buyer and supplier influence, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

A concise one-sheet Porter's Five Forces for CPP Group that quickly surfaces competitive pressures and recommended strategic moves, ready to drop into pitch decks or boardroom slides. Customize intensity levels as market conditions change to prioritize actions and relieve analysis bottlenecks without complex tools.

Customers Bargaining Power

Large distribution partners

Banks, telcos and retailers bundle CPP products into customer offers, aggregating large volumes and giving distributors substantial leverage. Their scale and low switching costs translate into strong pricing and contract power, with CPP's 2024 channel-concentrated model seeing over 50% of revenues tied to top partners. This revenue concentration raises renegotiation exposure, though co-created products and joint go-to-market models can deepen ties and reduce pure price pressure.

End-consumer price sensitivity

Consumers treat card protection and gadget insurance as semi-commodities, with 2024 Statista data showing about 59% of UK shoppers using comparison sites for small insurances, amplifying price sensitivity. Monthly subscription models and easy cancellations increase bargaining power and churn risk. Clear value proofs — rapid claim turnaround, bundled add-ons — demonstrably lower price elasticity. Transparent terms and fair claims handling sustain willingness to pay.

Alternative partner offerings

Partners can source similar covers from global insurers or insurtech MGAs, with insurtech market investment still in the low billions annual range in 2024, increasing competitive options and buyer leverage in RFPs.

CPP can offset pure price comparisons by demonstrating UX, data-insight-driven underwriting and reported conversion lifts (often cited in the 10–30% range by platform providers).

Deep embedded integration—API, single-sign-on and policy administration links—raises switching costs for partners, making long-term deals and higher-margin bundles more defensible.

Regulatory scrutiny on add-ons

Multi-year renegotiation cycles

Multi-year renegotiation cycles concentrate 100% of contracted volume at discrete renewal points, enabling buyers to extract concessions on price, SLAs and revenue share; CPP’s leverage rises when retention and cross-sell performance remain strong through the cycle.

- Renewal risk: 100% of volume at renegotiation

- Buyer tactics: price, SLA, revenue-share concessions

- Leverage drivers: high retention, cross-sell

- Mitigation: pilots and rapid rollouts to secure renewals at acceptable margins

Bargaining power: >50% revenue tied; 59% compare-site use

Bargaining power high: >50% revenues tied to top partners (2024), enabling buyer leverage at renewals; 59% UK shoppers use comparison sites for small insurances (Statista 2024), raising price sensitivity. Deep integration and compliance (FCA Consumer Duty Jul 2023) raise switching costs and can mitigate price pressure.

| Metric | Value (2024) |

|---|---|

| Revenue concentration | >50% |

| Comparison-site use | 59% |

| Regulator | FCA Consumer Duty Jul 2023 |

Same Document Delivered

CPP Group Porter's Five Forces Analysis

This preview shows the exact CPP Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the final, professionally formatted analysis, ready for download and immediate use. You’re viewing the same deliverable that will be available to you instantly upon payment.

Description

From Overview to Strategy Blueprint

CPP Group faces moderate buyer power and regulatory pressure, while substitute threats and digital entrants shape margins—supplier influence is limited by scale. This snapshot highlights strategic levers in pricing, distribution and product diversification. The full Porter's Five Forces Analysis unpacks force-by-force ratings, visuals and business implications for CPP Group. Unlock the complete report to drive informed investment and strategic decisions.

Suppliers Bargaining Power

Dependence on underwriters

CPP Group relies on insurance carriers and reinsurers to underwrite and price risk, giving well-rated underwriters leverage to demand tighter terms—global reinsurance pricing rose c.11% at 1/1/2024 renewals (Guy Carpenter), squeezing insurer margins in hard markets.

Critical tech and cyber vendors

Core systems, cybersecurity tools and identity-monitoring providers are essential to CPPs product delivery; the three national credit bureaus dominate identity data access in key markets, concentrating supplier power. The global cybersecurity market reached about $218 billion in 2024, increasing supplier leverage on pricing. CPP can mitigate via volume agreements and multi-sourcing, but high integration and switching costs keep vendors influential. SLAs and performance-based fees are used to rebalance power.

Data and verification providers

Credit bureaus, KYC/AML and fraud-data suppliers directly shape CPP Group’s product pricing and loss control by determining risk accuracy; in 2024 the top three credit bureaus held an estimated >80% share in major markets, raising supplier leverage. Layering alternative data sources and proprietary models reduces lock-in, but GDPR, FCA AML rules and KYC mandates limit easy substitution.

BPO and assistance networks

BPO call centers, claims TPAs and repair/replacement networks drive CPP Group service levels and cost; the global contact center market reached 379 billion USD in 2024, concentrating operational leverage in suppliers that control capacity and expertise. Regional fragmentation enables competitive bidding, but peak-demand surges and specialized repairs can shift bargaining power to suppliers; pay-for-outcomes and strict KPIs rebalance incentives.

- Call centers: scale and peak capacity

- TPA claims: accuracy and speed

- Repair networks: specialized skills

- Mitigants: competitive bids, KPIs, outcome payments

Regulatory and compliance services

External legal, compliance and audit expertise is required across multiple jurisdictions, and specialist scarcity elevates fees and supplier influence; Big Four advisory revenues totaled roughly USD 200bn in 2024, underscoring concentrated supplier power. Building internal capability reduces dependency and can cut advisory spend over time. Cross-market standardization of policies and platforms lowers advisory hours and supplier leverage.

- Specialist scarcity raises fees and influence

- Big Four ~USD 200bn 2024 revenue highlights concentration

- Internal capability reduces long-term external spend

- Cross-market standardization lowers advisory hours

+11% reinsurance; bureaus >80% dominance

Suppliers (reinsurers, credit bureaus, cybersecurity and BPOs) hold significant leverage for CPP Group: reinsurance pricing rose c.11% at 1/1/2024 and top three credit bureaus hold >80% market share. Cybersecurity market ~USD 218bn and contact center market ~USD 379bn in 2024 increase vendor pricing power. Mitigants: multi-sourcing, SLAs, outcome fees and internal capability build.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +11% price (1/1/2024) | Higher terms |

| Credit bureaus | >80% share | Data lock-in |

| Cybersecurity | USD 218bn | Pricing power |

| Contact centers | USD 379bn | Operational leverage |

| Big Four | ~USD 200bn | Advisory scarcity |

What is included in the product

Tailored Porter’s Five Forces analysis for CPP Group, uncovering competitive pressures, buyer and supplier influence, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

A concise one-sheet Porter's Five Forces for CPP Group that quickly surfaces competitive pressures and recommended strategic moves, ready to drop into pitch decks or boardroom slides. Customize intensity levels as market conditions change to prioritize actions and relieve analysis bottlenecks without complex tools.

Customers Bargaining Power

Large distribution partners

Banks, telcos and retailers bundle CPP products into customer offers, aggregating large volumes and giving distributors substantial leverage. Their scale and low switching costs translate into strong pricing and contract power, with CPP's 2024 channel-concentrated model seeing over 50% of revenues tied to top partners. This revenue concentration raises renegotiation exposure, though co-created products and joint go-to-market models can deepen ties and reduce pure price pressure.

End-consumer price sensitivity

Consumers treat card protection and gadget insurance as semi-commodities, with 2024 Statista data showing about 59% of UK shoppers using comparison sites for small insurances, amplifying price sensitivity. Monthly subscription models and easy cancellations increase bargaining power and churn risk. Clear value proofs — rapid claim turnaround, bundled add-ons — demonstrably lower price elasticity. Transparent terms and fair claims handling sustain willingness to pay.

Alternative partner offerings

Partners can source similar covers from global insurers or insurtech MGAs, with insurtech market investment still in the low billions annual range in 2024, increasing competitive options and buyer leverage in RFPs.

CPP can offset pure price comparisons by demonstrating UX, data-insight-driven underwriting and reported conversion lifts (often cited in the 10–30% range by platform providers).

Deep embedded integration—API, single-sign-on and policy administration links—raises switching costs for partners, making long-term deals and higher-margin bundles more defensible.

Regulatory scrutiny on add-ons

Multi-year renegotiation cycles

Multi-year renegotiation cycles concentrate 100% of contracted volume at discrete renewal points, enabling buyers to extract concessions on price, SLAs and revenue share; CPP’s leverage rises when retention and cross-sell performance remain strong through the cycle.

- Renewal risk: 100% of volume at renegotiation

- Buyer tactics: price, SLA, revenue-share concessions

- Leverage drivers: high retention, cross-sell

- Mitigation: pilots and rapid rollouts to secure renewals at acceptable margins

Bargaining power: >50% revenue tied; 59% compare-site use

Bargaining power high: >50% revenues tied to top partners (2024), enabling buyer leverage at renewals; 59% UK shoppers use comparison sites for small insurances (Statista 2024), raising price sensitivity. Deep integration and compliance (FCA Consumer Duty Jul 2023) raise switching costs and can mitigate price pressure.

| Metric | Value (2024) |

|---|---|

| Revenue concentration | >50% |

| Comparison-site use | 59% |

| Regulator | FCA Consumer Duty Jul 2023 |

Same Document Delivered

CPP Group Porter's Five Forces Analysis

This preview shows the exact CPP Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the final, professionally formatted analysis, ready for download and immediate use. You’re viewing the same deliverable that will be available to you instantly upon payment.