CPP Group SWOT Analysis

Your Strategic Toolkit Starts Here

CPP Group’s SWOT snapshot highlights resilient brand recognition and diversified protection products, balanced against regulatory exposure and competitive pressure; growth hinges on digital transformation and geographic expansion. For investors and strategists, our full SWOT delivers research-backed detail, financial context, and actionable recommendations. Purchase the complete report to access editable Word and Excel files for planning and pitch-ready presentations.

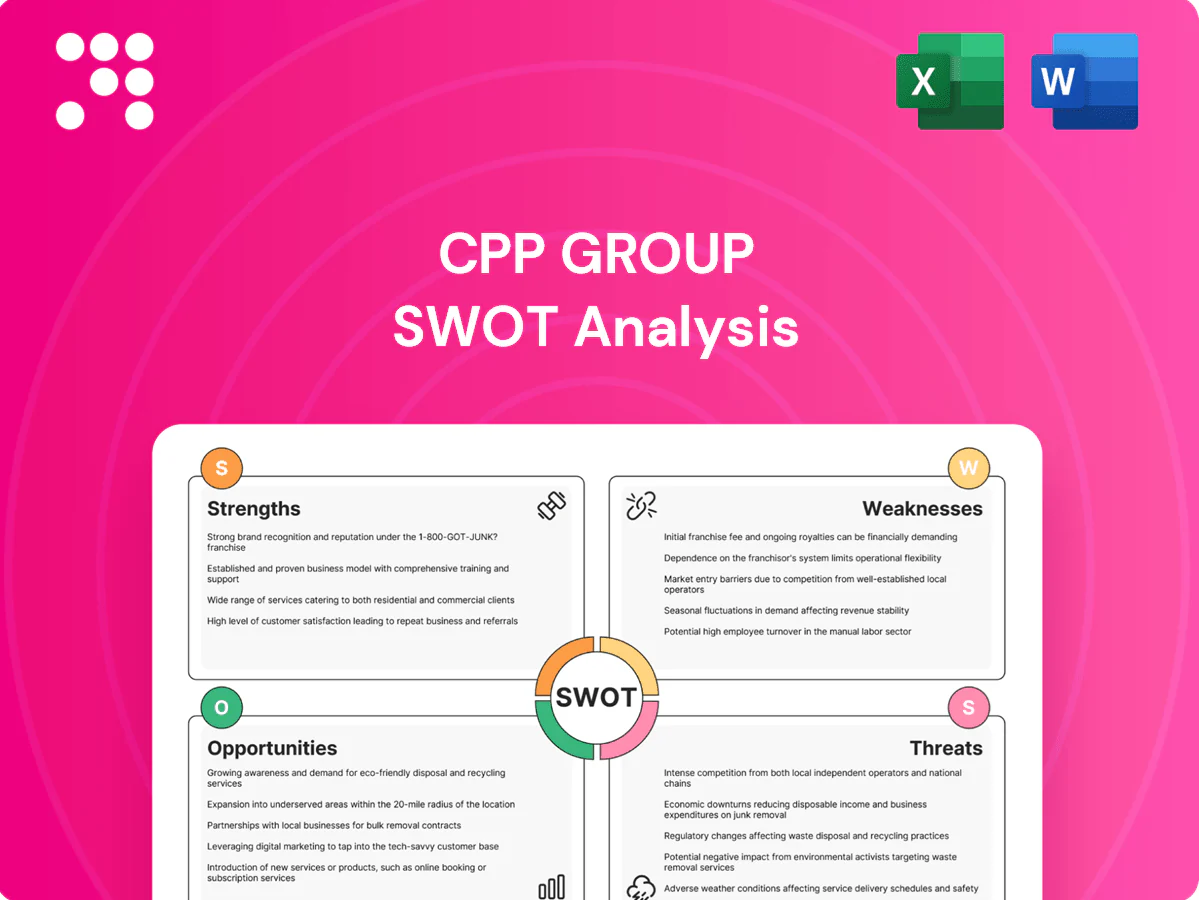

Strengths

Deep B2B partnerships

CPP Group distributes primarily through banks and corporates, giving efficient access to large customer bases and lowering acquisition costs versus direct-to-consumer models; co-branded trust from financial institutions enhances conversion and retention, and the partnership model is inherently scalable across additional partners and markets.

Diversified protection suite

Card protection, gadget insurance and cyber assistance cover key daily-risk moments, with global cyber insurance premiums exceeding $10bn by 2023, underscoring demand for digital risk cover. This product diversification smooths claims volatility and revenue seasonality by spreading risk across incident types. It also enables bundled offers that raise average basket size and attach rates. Customers perceive end-to-end protection and greater peace of mind.

Embedded and assistance expertise

CPP Group embeds assistance within partner journeys, leveraging deep claims-handling and service-orchestration know-how that creates a strong barrier to entry. Rapid-response, concierge-style support differentiates the firm from pure insurers and drives higher NPS and renewal propensity. Operational expertise in end-to-end fulfilment sustains partner trust and recurring revenue.

Recurring revenue profile

Policies and subscriptions deliver predictable, repeatable cash flows for CPP, with partner-led auto-renewals stabilizing lifetime value and supporting disciplined underwriting and reinvestment in product; CPP’s partner networks serve over 5 million customers, cushioning short-term demand swings and improving planning visibility.

- Predictable cash flows; partner-led auto-renewals; >5m customers; supports underwriting discipline

Lean, scalable platform

CPP Groups lean, scalable platform standardizes products and processes for efficient replication across distribution partners, while centralized technology and shared services deliver operating leverage as volumes expand. API-led integration reduces onboarding friction and accelerates partner activation. Growing scale strengthens negotiating power with suppliers and reinsurers, lowering unit costs.

Bank-embedded cyber & gadget protection — scalable to 5m+ customers; $10bn market

Partner distribution via banks and corporates gives low acquisition costs and scalable access to over 5m customers.

Product mix—card protection, gadget insurance, cyber assistance—captures demand in a market where global cyber premiums exceeded $10bn in 2023.

Embedded assistance and claims orchestration drive higher NPS, renewals and a strong barrier to entry.

Lean, API-first platform delivers operating leverage and improved reinsurance/supplier terms as scale grows.

| Metric | Value |

|---|---|

| Customers (partner network) | >5m |

| Global cyber premiums (2023) | >$10bn |

What is included in the product

Provides a concise SWOT analysis of CPP Group, outlining internal strengths and weaknesses alongside external opportunities and threats to assess competitive position, growth drivers, and strategic risks.

Provides a concise SWOT matrix for CPP Group that quickly pinpoints strategic blind spots and competitive advantages to relieve decision-making bottlenecks. Editable format enables fast scenario updates for stakeholder-ready summaries and aligned action planning.

Weaknesses

Partner dependence

CPP Group’s heavy reliance on distribution partners concentrates channel risk: loss or renegotiation of a major partner can materially reduce sales and margins. Partner priorities can constrain pricing and product design, limiting direct control over customer propositions. Negotiating power often skews toward large banks and insurers, pressuring commission rates and contract terms.

Commoditized offerings

Gadget and card protection are highly commoditized, with many banks and retailers offering similar cover and little product differentiation. Intense price competition has compressed margins—industry data show average premiums fell roughly 10% between 2021–24—eroding profitability. Low switching costs make retention hard, and CPPs brand pull lags direct-to-consumer insurers, limiting upsell opportunities.

Limited consumer brand visibility

CPP Group plc (LSE: CPP) relies heavily on a B2B2C distribution model, which reduces direct engagement with end users and limits brand visibility. Low consumer awareness outside partner channels constrains cross-sell opportunities and caps customer lifetime value expansion. Weaker data feedback loops from indirect relationships further restrict targeted upsell and personalization.

Complex compliance burden

Operating across insurance and assistance forces CPP Group to meet strict regulatory regimes in each territory, increasing legal and reporting workloads. Partner audits and multi-jurisdictional rules drive higher overhead and slow product launches. Product add-ons often face heightened scrutiny, and rising compliance costs can erode the benefits of scale.

- Regulatory complexity

- Partner audit burden

- Product scrutiny

- Compliance costs vs scale

Legacy tech constraints

Legacy tech constraints force CPP Group to maintain numerous bespoke integrations with partner systems, creating accumulating technical debt that slows new feature delivery and contributed to multi-month release cycles in comparable insurance-tech firms.

Slow change cycles hinder rapid product iteration, data silos between claims, distribution and CRM reduce advanced analytics effectiveness and personalization, and modernization will require sustained, multi-year investment to migrate platforms and unify data.

- Integration-driven technical debt

- Prolonged release cycles

- Data silos limit analytics

- High modernization cost over time

Channel concentration, premium compression and legacy tech squeeze margins

Concentrated dependence on distribution partners creates material channel risk and weakens negotiation leverage. Product commoditization and intense price competition drove average premiums down ~10% between 2021–24, compressing margins. B2B2C model limits brand visibility, data feedback and cross-sell. Legacy integrations cause 3–6 month release cycles, data silos and high modernization costs.

| Metric | Recent figure/impact |

|---|---|

| Premium compression | -10% (2021–24) |

| Release cycle | 3–6 months |

| Distribution dependence | High channel concentration risk |

| Compliance | Multi-jurisdiction overhead |

Preview Before You Purchase

CPP Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable version ready for download.

Your Strategic Toolkit Starts Here

CPP Group’s SWOT snapshot highlights resilient brand recognition and diversified protection products, balanced against regulatory exposure and competitive pressure; growth hinges on digital transformation and geographic expansion. For investors and strategists, our full SWOT delivers research-backed detail, financial context, and actionable recommendations. Purchase the complete report to access editable Word and Excel files for planning and pitch-ready presentations.

Strengths

Deep B2B partnerships

CPP Group distributes primarily through banks and corporates, giving efficient access to large customer bases and lowering acquisition costs versus direct-to-consumer models; co-branded trust from financial institutions enhances conversion and retention, and the partnership model is inherently scalable across additional partners and markets.

Diversified protection suite

Card protection, gadget insurance and cyber assistance cover key daily-risk moments, with global cyber insurance premiums exceeding $10bn by 2023, underscoring demand for digital risk cover. This product diversification smooths claims volatility and revenue seasonality by spreading risk across incident types. It also enables bundled offers that raise average basket size and attach rates. Customers perceive end-to-end protection and greater peace of mind.

Embedded and assistance expertise

CPP Group embeds assistance within partner journeys, leveraging deep claims-handling and service-orchestration know-how that creates a strong barrier to entry. Rapid-response, concierge-style support differentiates the firm from pure insurers and drives higher NPS and renewal propensity. Operational expertise in end-to-end fulfilment sustains partner trust and recurring revenue.

Recurring revenue profile

Policies and subscriptions deliver predictable, repeatable cash flows for CPP, with partner-led auto-renewals stabilizing lifetime value and supporting disciplined underwriting and reinvestment in product; CPP’s partner networks serve over 5 million customers, cushioning short-term demand swings and improving planning visibility.

- Predictable cash flows; partner-led auto-renewals; >5m customers; supports underwriting discipline

Lean, scalable platform

CPP Groups lean, scalable platform standardizes products and processes for efficient replication across distribution partners, while centralized technology and shared services deliver operating leverage as volumes expand. API-led integration reduces onboarding friction and accelerates partner activation. Growing scale strengthens negotiating power with suppliers and reinsurers, lowering unit costs.

Bank-embedded cyber & gadget protection — scalable to 5m+ customers; $10bn market

Partner distribution via banks and corporates gives low acquisition costs and scalable access to over 5m customers.

Product mix—card protection, gadget insurance, cyber assistance—captures demand in a market where global cyber premiums exceeded $10bn in 2023.

Embedded assistance and claims orchestration drive higher NPS, renewals and a strong barrier to entry.

Lean, API-first platform delivers operating leverage and improved reinsurance/supplier terms as scale grows.

| Metric | Value |

|---|---|

| Customers (partner network) | >5m |

| Global cyber premiums (2023) | >$10bn |

What is included in the product

Provides a concise SWOT analysis of CPP Group, outlining internal strengths and weaknesses alongside external opportunities and threats to assess competitive position, growth drivers, and strategic risks.

Provides a concise SWOT matrix for CPP Group that quickly pinpoints strategic blind spots and competitive advantages to relieve decision-making bottlenecks. Editable format enables fast scenario updates for stakeholder-ready summaries and aligned action planning.

Weaknesses

Partner dependence

CPP Group’s heavy reliance on distribution partners concentrates channel risk: loss or renegotiation of a major partner can materially reduce sales and margins. Partner priorities can constrain pricing and product design, limiting direct control over customer propositions. Negotiating power often skews toward large banks and insurers, pressuring commission rates and contract terms.

Commoditized offerings

Gadget and card protection are highly commoditized, with many banks and retailers offering similar cover and little product differentiation. Intense price competition has compressed margins—industry data show average premiums fell roughly 10% between 2021–24—eroding profitability. Low switching costs make retention hard, and CPPs brand pull lags direct-to-consumer insurers, limiting upsell opportunities.

Limited consumer brand visibility

CPP Group plc (LSE: CPP) relies heavily on a B2B2C distribution model, which reduces direct engagement with end users and limits brand visibility. Low consumer awareness outside partner channels constrains cross-sell opportunities and caps customer lifetime value expansion. Weaker data feedback loops from indirect relationships further restrict targeted upsell and personalization.

Complex compliance burden

Operating across insurance and assistance forces CPP Group to meet strict regulatory regimes in each territory, increasing legal and reporting workloads. Partner audits and multi-jurisdictional rules drive higher overhead and slow product launches. Product add-ons often face heightened scrutiny, and rising compliance costs can erode the benefits of scale.

- Regulatory complexity

- Partner audit burden

- Product scrutiny

- Compliance costs vs scale

Legacy tech constraints

Legacy tech constraints force CPP Group to maintain numerous bespoke integrations with partner systems, creating accumulating technical debt that slows new feature delivery and contributed to multi-month release cycles in comparable insurance-tech firms.

Slow change cycles hinder rapid product iteration, data silos between claims, distribution and CRM reduce advanced analytics effectiveness and personalization, and modernization will require sustained, multi-year investment to migrate platforms and unify data.

- Integration-driven technical debt

- Prolonged release cycles

- Data silos limit analytics

- High modernization cost over time

Channel concentration, premium compression and legacy tech squeeze margins

Concentrated dependence on distribution partners creates material channel risk and weakens negotiation leverage. Product commoditization and intense price competition drove average premiums down ~10% between 2021–24, compressing margins. B2B2C model limits brand visibility, data feedback and cross-sell. Legacy integrations cause 3–6 month release cycles, data silos and high modernization costs.

| Metric | Recent figure/impact |

|---|---|

| Premium compression | -10% (2021–24) |

| Release cycle | 3–6 months |

| Distribution dependence | High channel concentration risk |

| Compliance | Multi-jurisdiction overhead |

Preview Before You Purchase

CPP Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable version ready for download.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

CPP Group’s SWOT snapshot highlights resilient brand recognition and diversified protection products, balanced against regulatory exposure and competitive pressure; growth hinges on digital transformation and geographic expansion. For investors and strategists, our full SWOT delivers research-backed detail, financial context, and actionable recommendations. Purchase the complete report to access editable Word and Excel files for planning and pitch-ready presentations.

Strengths

Deep B2B partnerships

CPP Group distributes primarily through banks and corporates, giving efficient access to large customer bases and lowering acquisition costs versus direct-to-consumer models; co-branded trust from financial institutions enhances conversion and retention, and the partnership model is inherently scalable across additional partners and markets.

Diversified protection suite

Card protection, gadget insurance and cyber assistance cover key daily-risk moments, with global cyber insurance premiums exceeding $10bn by 2023, underscoring demand for digital risk cover. This product diversification smooths claims volatility and revenue seasonality by spreading risk across incident types. It also enables bundled offers that raise average basket size and attach rates. Customers perceive end-to-end protection and greater peace of mind.

Embedded and assistance expertise

CPP Group embeds assistance within partner journeys, leveraging deep claims-handling and service-orchestration know-how that creates a strong barrier to entry. Rapid-response, concierge-style support differentiates the firm from pure insurers and drives higher NPS and renewal propensity. Operational expertise in end-to-end fulfilment sustains partner trust and recurring revenue.

Recurring revenue profile

Policies and subscriptions deliver predictable, repeatable cash flows for CPP, with partner-led auto-renewals stabilizing lifetime value and supporting disciplined underwriting and reinvestment in product; CPP’s partner networks serve over 5 million customers, cushioning short-term demand swings and improving planning visibility.

- Predictable cash flows; partner-led auto-renewals; >5m customers; supports underwriting discipline

Lean, scalable platform

CPP Groups lean, scalable platform standardizes products and processes for efficient replication across distribution partners, while centralized technology and shared services deliver operating leverage as volumes expand. API-led integration reduces onboarding friction and accelerates partner activation. Growing scale strengthens negotiating power with suppliers and reinsurers, lowering unit costs.

Bank-embedded cyber & gadget protection — scalable to 5m+ customers; $10bn market

Partner distribution via banks and corporates gives low acquisition costs and scalable access to over 5m customers.

Product mix—card protection, gadget insurance, cyber assistance—captures demand in a market where global cyber premiums exceeded $10bn in 2023.

Embedded assistance and claims orchestration drive higher NPS, renewals and a strong barrier to entry.

Lean, API-first platform delivers operating leverage and improved reinsurance/supplier terms as scale grows.

| Metric | Value |

|---|---|

| Customers (partner network) | >5m |

| Global cyber premiums (2023) | >$10bn |

What is included in the product

Provides a concise SWOT analysis of CPP Group, outlining internal strengths and weaknesses alongside external opportunities and threats to assess competitive position, growth drivers, and strategic risks.

Provides a concise SWOT matrix for CPP Group that quickly pinpoints strategic blind spots and competitive advantages to relieve decision-making bottlenecks. Editable format enables fast scenario updates for stakeholder-ready summaries and aligned action planning.

Weaknesses

Partner dependence

CPP Group’s heavy reliance on distribution partners concentrates channel risk: loss or renegotiation of a major partner can materially reduce sales and margins. Partner priorities can constrain pricing and product design, limiting direct control over customer propositions. Negotiating power often skews toward large banks and insurers, pressuring commission rates and contract terms.

Commoditized offerings

Gadget and card protection are highly commoditized, with many banks and retailers offering similar cover and little product differentiation. Intense price competition has compressed margins—industry data show average premiums fell roughly 10% between 2021–24—eroding profitability. Low switching costs make retention hard, and CPPs brand pull lags direct-to-consumer insurers, limiting upsell opportunities.

Limited consumer brand visibility

CPP Group plc (LSE: CPP) relies heavily on a B2B2C distribution model, which reduces direct engagement with end users and limits brand visibility. Low consumer awareness outside partner channels constrains cross-sell opportunities and caps customer lifetime value expansion. Weaker data feedback loops from indirect relationships further restrict targeted upsell and personalization.

Complex compliance burden

Operating across insurance and assistance forces CPP Group to meet strict regulatory regimes in each territory, increasing legal and reporting workloads. Partner audits and multi-jurisdictional rules drive higher overhead and slow product launches. Product add-ons often face heightened scrutiny, and rising compliance costs can erode the benefits of scale.

- Regulatory complexity

- Partner audit burden

- Product scrutiny

- Compliance costs vs scale

Legacy tech constraints

Legacy tech constraints force CPP Group to maintain numerous bespoke integrations with partner systems, creating accumulating technical debt that slows new feature delivery and contributed to multi-month release cycles in comparable insurance-tech firms.

Slow change cycles hinder rapid product iteration, data silos between claims, distribution and CRM reduce advanced analytics effectiveness and personalization, and modernization will require sustained, multi-year investment to migrate platforms and unify data.

- Integration-driven technical debt

- Prolonged release cycles

- Data silos limit analytics

- High modernization cost over time

Channel concentration, premium compression and legacy tech squeeze margins

Concentrated dependence on distribution partners creates material channel risk and weakens negotiation leverage. Product commoditization and intense price competition drove average premiums down ~10% between 2021–24, compressing margins. B2B2C model limits brand visibility, data feedback and cross-sell. Legacy integrations cause 3–6 month release cycles, data silos and high modernization costs.

| Metric | Recent figure/impact |

|---|---|

| Premium compression | -10% (2021–24) |

| Release cycle | 3–6 months |

| Distribution dependence | High channel concentration risk |

| Compliance | Multi-jurisdiction overhead |

Preview Before You Purchase

CPP Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable version ready for download.