Bank of Chongqing Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

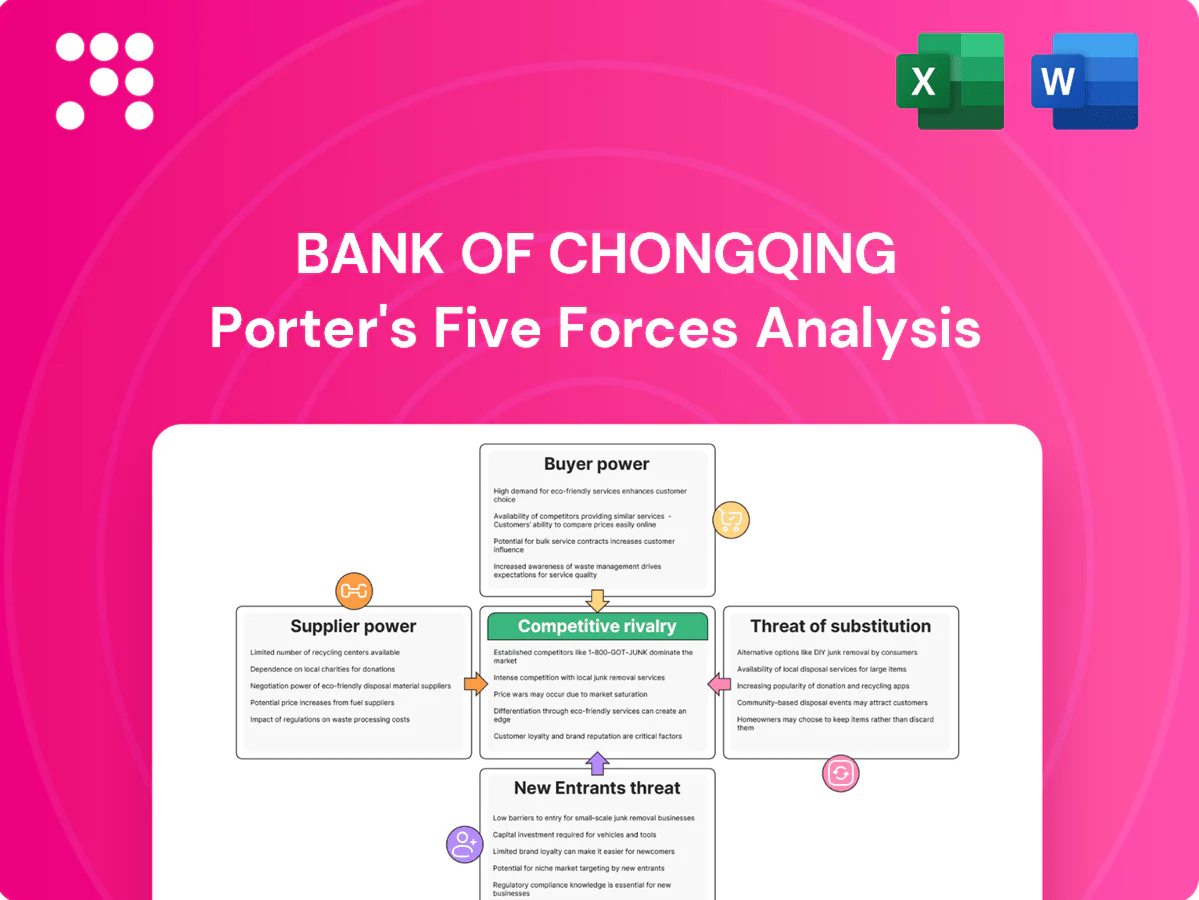

Bank of Chongqing faces moderate buyer power, intense domestic rivalry, and regulatory barriers that limit new entrants, while fintech substitutes and funding costs shape its margins; this snapshot highlights where strategic pressure concentrates. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Concentrated funding base

Bank of Chongqing depends on retail and local corporate deposits for roughly 65% of its funding, so shifts by large depositors or public-sector accounts can quickly force up funding costs. When the top 10 depositors represent over 15% of deposits and more than 75% of balances are Chongqing-based, regional concentration amplifies supplier leverage. Diversifying into stable, low-cost deposits—salary, NIM-friendly retail accounts and small enterprise sticky funds—reduces that pressure.

Wholesale and interbank reliance

In tight liquidity cycles Bank of Chongqing's reliance on interbank and NCD markets allows counterparties to demand higher rates, tighter covenants or shorter tenors, pushing funding costs up and compressing NIMs. In 2024 China’s 1-year LPR hovered around 3.55%, while short-term interbank rates occasionally spiked several hundred basis points, widening funding spreads. Robust liquidity buffers and PBOC facilities reduce this dependency and limit margin pressure.

Payment and tech vendors

Payment and tech vendors (core banking, cloud, cybersecurity, UnionPay rails) supply essential infrastructure; UnionPay remained the dominant card-rail in 2024 with over 70% domestic card-network market share. High switching costs for core systems and integrations give vendors pricing and service leverage. Contracting, multi-vendor strategies and increasing in-house tech build-outs in 2024 can rebalance supplier power over time.

Talent and risk expertise

Skilled bankers, risk modelers and compliance professionals are scarce in many regional Chinese markets, raising compensation and retention costs for Bank of Chongqing and increasing supplier power of labor; loss of key teams can disrupt lending and risk control and slow credit deployment. Building internal training pipelines and targeted retention programs mitigates this supplier power and preserves underwriting continuity.

- Scarcity elevates wage pressure

- Key-team loss disrupts lending/risk

- Training pipelines lower supplier power

- Targeted retention improves continuity

Data and analytics providers

Credit bureaus, alternative data and analytics tools underpin Bank of Chongqing underwriting and collections, with China credit reference systems covering roughly 1.2 billion profiles by 2024, while specialist vendors supply localized signals where public datasets are sparse.

Reliance on external providers can raise unit acquisition costs and slow product rollout, but building proprietary data and models reduces supplier leverage and improves pricing and speed to market.

- Credit bureau reach: ~1.2bn Chinese profiles (2024)

- Alternative data: empowers niche scoring where local datasets limited

- Risk: supplier dependence increases costs and rollout constraints

- Mitigation: proprietary data/models lower supplier bargaining power

Supplier power high: 65% deposit funding, >75% Chongqing concentration

Suppliers exert moderate-high power: 65% funding from retail/local corporates with top-10 >15% and >75% Chongqing concentration; interbank/NCD reliance exposes the bank to rate spikes (1yr LPR ~3.55% in 2024). Tech/vendors (UnionPay >70%) and scarce skilled staff raise costs; credit bureaus cover ~1.2bn profiles, while proprietary data reduces dependence.

| Metric | 2024 |

|---|---|

| Funding from deposits | 65% |

| Top-10 deposit share | >15% |

| Chongqing deposit share | >75% |

| 1yr LPR | 3.55% |

| UnionPay share | >70% |

| Credit profiles | ~1.2bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bank of Chongqing, with a detailed assessment of rivalry, buyer and supplier power, substitutes, and barriers to entry, highlighting disruptive threats and strategic levers to protect and grow market share.

A clear one-sheet Porter's Five Forces summary tailored to Bank of Chongqing—perfect for quick strategic, credit-risk or branch expansion decisions.

Customers Bargaining Power

Large corporate and SOE clients

Anchor corporates and SOEs in Chongqing wield strong bargaining power, forcing tighter loan spreads, fee waivers and bundled-service demands; top corporate relationships often represent a double-digit share of corporate deposit and loan balances, so losing one hits balances and cross-sell materially. Relationship banking and tailored solutions are used to defend pricing and preserve wallet share.

SMEs’ price sensitivity

SMEs, which contribute over 60% of China’s GDP and more than 80% of urban employment, actively compare rates and collateral terms across city and joint-stock banks when choosing relationship banks. They increasingly switch to lenders that offer faster approvals and seamless digital onboarding, forcing Bank of Chongqing to streamline credit processes or concede margins. Offering value-added cash management and receivables financing can measurably reduce SME churn.

Retail depositors’ mobility

Digital channels let Chongqing depositors compare rates and transfer funds instantly; China had over 1.0 billion mobile payment users by 2024, accelerating switchability. Proliferation of MMFs and wealth products (retail WMPs expanding double digits) intensifies price competition for savings. Super-apps enable rapid reallocation, while loyalty programs and ecosystem partnerships help the bank retain deposits.

Wealth clients’ product breadth demands

- Product breadth pressure

- Fee/performance-driven mobility

- Advisory quality requirement

- Open-architecture reduces switch risk

Switching costs lowering

eKYC, API-based payroll and digital mortgage pre-approvals cut onboarding from days to minutes and materially lower switching costs, prompting customers to press harder on price and service; banks must compete on UX and speed as friction falls, while deep integration into payroll and lending workflows increases account stickiness.

- eKYC: faster onboarding

- API payroll: continuous integration

- Pre-approvals: quicker lending decisions

Corporate concentration and 1.0bn mobile users squeeze spreads; SMEs boost switchability

Corporate and SOE clients hold strong leverage—top corporates can account for double-digit shares of deposits/loans—forcing tighter spreads and bundled-service demands. SMEs (≈60% of GDP; >80% urban employment) and 1.0bn+ mobile payment users (2024) increase switchability, pressuring pricing and speed. Retail/MMF/WMP growth (double-digit) and HNW fee sensitivity raise product-access and advisory demands.

| Metric | 2024 |

|---|---|

| Mobile pay users | 1.0bn+ |

| SME GDP share | ≈60% |

| Urban employment by SMEs | >80% |

Preview the Actual Deliverable

Bank of Chongqing Porter's Five Forces Analysis

This preview shows the Bank of Chongqing Porter’s Five Forces analysis exactly as delivered—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download upon purchase. You’ll receive this same file instantly after payment, complete and ready to use for strategic or investment decisions.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bank of Chongqing faces moderate buyer power, intense domestic rivalry, and regulatory barriers that limit new entrants, while fintech substitutes and funding costs shape its margins; this snapshot highlights where strategic pressure concentrates. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Concentrated funding base

Bank of Chongqing depends on retail and local corporate deposits for roughly 65% of its funding, so shifts by large depositors or public-sector accounts can quickly force up funding costs. When the top 10 depositors represent over 15% of deposits and more than 75% of balances are Chongqing-based, regional concentration amplifies supplier leverage. Diversifying into stable, low-cost deposits—salary, NIM-friendly retail accounts and small enterprise sticky funds—reduces that pressure.

Wholesale and interbank reliance

In tight liquidity cycles Bank of Chongqing's reliance on interbank and NCD markets allows counterparties to demand higher rates, tighter covenants or shorter tenors, pushing funding costs up and compressing NIMs. In 2024 China’s 1-year LPR hovered around 3.55%, while short-term interbank rates occasionally spiked several hundred basis points, widening funding spreads. Robust liquidity buffers and PBOC facilities reduce this dependency and limit margin pressure.

Payment and tech vendors

Payment and tech vendors (core banking, cloud, cybersecurity, UnionPay rails) supply essential infrastructure; UnionPay remained the dominant card-rail in 2024 with over 70% domestic card-network market share. High switching costs for core systems and integrations give vendors pricing and service leverage. Contracting, multi-vendor strategies and increasing in-house tech build-outs in 2024 can rebalance supplier power over time.

Talent and risk expertise

Skilled bankers, risk modelers and compliance professionals are scarce in many regional Chinese markets, raising compensation and retention costs for Bank of Chongqing and increasing supplier power of labor; loss of key teams can disrupt lending and risk control and slow credit deployment. Building internal training pipelines and targeted retention programs mitigates this supplier power and preserves underwriting continuity.

- Scarcity elevates wage pressure

- Key-team loss disrupts lending/risk

- Training pipelines lower supplier power

- Targeted retention improves continuity

Data and analytics providers

Credit bureaus, alternative data and analytics tools underpin Bank of Chongqing underwriting and collections, with China credit reference systems covering roughly 1.2 billion profiles by 2024, while specialist vendors supply localized signals where public datasets are sparse.

Reliance on external providers can raise unit acquisition costs and slow product rollout, but building proprietary data and models reduces supplier leverage and improves pricing and speed to market.

- Credit bureau reach: ~1.2bn Chinese profiles (2024)

- Alternative data: empowers niche scoring where local datasets limited

- Risk: supplier dependence increases costs and rollout constraints

- Mitigation: proprietary data/models lower supplier bargaining power

Supplier power high: 65% deposit funding, >75% Chongqing concentration

Suppliers exert moderate-high power: 65% funding from retail/local corporates with top-10 >15% and >75% Chongqing concentration; interbank/NCD reliance exposes the bank to rate spikes (1yr LPR ~3.55% in 2024). Tech/vendors (UnionPay >70%) and scarce skilled staff raise costs; credit bureaus cover ~1.2bn profiles, while proprietary data reduces dependence.

| Metric | 2024 |

|---|---|

| Funding from deposits | 65% |

| Top-10 deposit share | >15% |

| Chongqing deposit share | >75% |

| 1yr LPR | 3.55% |

| UnionPay share | >70% |

| Credit profiles | ~1.2bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bank of Chongqing, with a detailed assessment of rivalry, buyer and supplier power, substitutes, and barriers to entry, highlighting disruptive threats and strategic levers to protect and grow market share.

A clear one-sheet Porter's Five Forces summary tailored to Bank of Chongqing—perfect for quick strategic, credit-risk or branch expansion decisions.

Customers Bargaining Power

Large corporate and SOE clients

Anchor corporates and SOEs in Chongqing wield strong bargaining power, forcing tighter loan spreads, fee waivers and bundled-service demands; top corporate relationships often represent a double-digit share of corporate deposit and loan balances, so losing one hits balances and cross-sell materially. Relationship banking and tailored solutions are used to defend pricing and preserve wallet share.

SMEs’ price sensitivity

SMEs, which contribute over 60% of China’s GDP and more than 80% of urban employment, actively compare rates and collateral terms across city and joint-stock banks when choosing relationship banks. They increasingly switch to lenders that offer faster approvals and seamless digital onboarding, forcing Bank of Chongqing to streamline credit processes or concede margins. Offering value-added cash management and receivables financing can measurably reduce SME churn.

Retail depositors’ mobility

Digital channels let Chongqing depositors compare rates and transfer funds instantly; China had over 1.0 billion mobile payment users by 2024, accelerating switchability. Proliferation of MMFs and wealth products (retail WMPs expanding double digits) intensifies price competition for savings. Super-apps enable rapid reallocation, while loyalty programs and ecosystem partnerships help the bank retain deposits.

Wealth clients’ product breadth demands

- Product breadth pressure

- Fee/performance-driven mobility

- Advisory quality requirement

- Open-architecture reduces switch risk

Switching costs lowering

eKYC, API-based payroll and digital mortgage pre-approvals cut onboarding from days to minutes and materially lower switching costs, prompting customers to press harder on price and service; banks must compete on UX and speed as friction falls, while deep integration into payroll and lending workflows increases account stickiness.

- eKYC: faster onboarding

- API payroll: continuous integration

- Pre-approvals: quicker lending decisions

Corporate concentration and 1.0bn mobile users squeeze spreads; SMEs boost switchability

Corporate and SOE clients hold strong leverage—top corporates can account for double-digit shares of deposits/loans—forcing tighter spreads and bundled-service demands. SMEs (≈60% of GDP; >80% urban employment) and 1.0bn+ mobile payment users (2024) increase switchability, pressuring pricing and speed. Retail/MMF/WMP growth (double-digit) and HNW fee sensitivity raise product-access and advisory demands.

| Metric | 2024 |

|---|---|

| Mobile pay users | 1.0bn+ |

| SME GDP share | ≈60% |

| Urban employment by SMEs | >80% |

Preview the Actual Deliverable

Bank of Chongqing Porter's Five Forces Analysis

This preview shows the Bank of Chongqing Porter’s Five Forces analysis exactly as delivered—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download upon purchase. You’ll receive this same file instantly after payment, complete and ready to use for strategic or investment decisions.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Bank of Chongqing faces moderate buyer power, intense domestic rivalry, and regulatory barriers that limit new entrants, while fintech substitutes and funding costs shape its margins; this snapshot highlights where strategic pressure concentrates. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Concentrated funding base

Bank of Chongqing depends on retail and local corporate deposits for roughly 65% of its funding, so shifts by large depositors or public-sector accounts can quickly force up funding costs. When the top 10 depositors represent over 15% of deposits and more than 75% of balances are Chongqing-based, regional concentration amplifies supplier leverage. Diversifying into stable, low-cost deposits—salary, NIM-friendly retail accounts and small enterprise sticky funds—reduces that pressure.

Wholesale and interbank reliance

In tight liquidity cycles Bank of Chongqing's reliance on interbank and NCD markets allows counterparties to demand higher rates, tighter covenants or shorter tenors, pushing funding costs up and compressing NIMs. In 2024 China’s 1-year LPR hovered around 3.55%, while short-term interbank rates occasionally spiked several hundred basis points, widening funding spreads. Robust liquidity buffers and PBOC facilities reduce this dependency and limit margin pressure.

Payment and tech vendors

Payment and tech vendors (core banking, cloud, cybersecurity, UnionPay rails) supply essential infrastructure; UnionPay remained the dominant card-rail in 2024 with over 70% domestic card-network market share. High switching costs for core systems and integrations give vendors pricing and service leverage. Contracting, multi-vendor strategies and increasing in-house tech build-outs in 2024 can rebalance supplier power over time.

Talent and risk expertise

Skilled bankers, risk modelers and compliance professionals are scarce in many regional Chinese markets, raising compensation and retention costs for Bank of Chongqing and increasing supplier power of labor; loss of key teams can disrupt lending and risk control and slow credit deployment. Building internal training pipelines and targeted retention programs mitigates this supplier power and preserves underwriting continuity.

- Scarcity elevates wage pressure

- Key-team loss disrupts lending/risk

- Training pipelines lower supplier power

- Targeted retention improves continuity

Data and analytics providers

Credit bureaus, alternative data and analytics tools underpin Bank of Chongqing underwriting and collections, with China credit reference systems covering roughly 1.2 billion profiles by 2024, while specialist vendors supply localized signals where public datasets are sparse.

Reliance on external providers can raise unit acquisition costs and slow product rollout, but building proprietary data and models reduces supplier leverage and improves pricing and speed to market.

- Credit bureau reach: ~1.2bn Chinese profiles (2024)

- Alternative data: empowers niche scoring where local datasets limited

- Risk: supplier dependence increases costs and rollout constraints

- Mitigation: proprietary data/models lower supplier bargaining power

Supplier power high: 65% deposit funding, >75% Chongqing concentration

Suppliers exert moderate-high power: 65% funding from retail/local corporates with top-10 >15% and >75% Chongqing concentration; interbank/NCD reliance exposes the bank to rate spikes (1yr LPR ~3.55% in 2024). Tech/vendors (UnionPay >70%) and scarce skilled staff raise costs; credit bureaus cover ~1.2bn profiles, while proprietary data reduces dependence.

| Metric | 2024 |

|---|---|

| Funding from deposits | 65% |

| Top-10 deposit share | >15% |

| Chongqing deposit share | >75% |

| 1yr LPR | 3.55% |

| UnionPay share | >70% |

| Credit profiles | ~1.2bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bank of Chongqing, with a detailed assessment of rivalry, buyer and supplier power, substitutes, and barriers to entry, highlighting disruptive threats and strategic levers to protect and grow market share.

A clear one-sheet Porter's Five Forces summary tailored to Bank of Chongqing—perfect for quick strategic, credit-risk or branch expansion decisions.

Customers Bargaining Power

Large corporate and SOE clients

Anchor corporates and SOEs in Chongqing wield strong bargaining power, forcing tighter loan spreads, fee waivers and bundled-service demands; top corporate relationships often represent a double-digit share of corporate deposit and loan balances, so losing one hits balances and cross-sell materially. Relationship banking and tailored solutions are used to defend pricing and preserve wallet share.

SMEs’ price sensitivity

SMEs, which contribute over 60% of China’s GDP and more than 80% of urban employment, actively compare rates and collateral terms across city and joint-stock banks when choosing relationship banks. They increasingly switch to lenders that offer faster approvals and seamless digital onboarding, forcing Bank of Chongqing to streamline credit processes or concede margins. Offering value-added cash management and receivables financing can measurably reduce SME churn.

Retail depositors’ mobility

Digital channels let Chongqing depositors compare rates and transfer funds instantly; China had over 1.0 billion mobile payment users by 2024, accelerating switchability. Proliferation of MMFs and wealth products (retail WMPs expanding double digits) intensifies price competition for savings. Super-apps enable rapid reallocation, while loyalty programs and ecosystem partnerships help the bank retain deposits.

Wealth clients’ product breadth demands

- Product breadth pressure

- Fee/performance-driven mobility

- Advisory quality requirement

- Open-architecture reduces switch risk

Switching costs lowering

eKYC, API-based payroll and digital mortgage pre-approvals cut onboarding from days to minutes and materially lower switching costs, prompting customers to press harder on price and service; banks must compete on UX and speed as friction falls, while deep integration into payroll and lending workflows increases account stickiness.

- eKYC: faster onboarding

- API payroll: continuous integration

- Pre-approvals: quicker lending decisions

Corporate concentration and 1.0bn mobile users squeeze spreads; SMEs boost switchability

Corporate and SOE clients hold strong leverage—top corporates can account for double-digit shares of deposits/loans—forcing tighter spreads and bundled-service demands. SMEs (≈60% of GDP; >80% urban employment) and 1.0bn+ mobile payment users (2024) increase switchability, pressuring pricing and speed. Retail/MMF/WMP growth (double-digit) and HNW fee sensitivity raise product-access and advisory demands.

| Metric | 2024 |

|---|---|

| Mobile pay users | 1.0bn+ |

| SME GDP share | ≈60% |

| Urban employment by SMEs | >80% |

Preview the Actual Deliverable

Bank of Chongqing Porter's Five Forces Analysis

This preview shows the Bank of Chongqing Porter’s Five Forces analysis exactly as delivered—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download upon purchase. You’ll receive this same file instantly after payment, complete and ready to use for strategic or investment decisions.