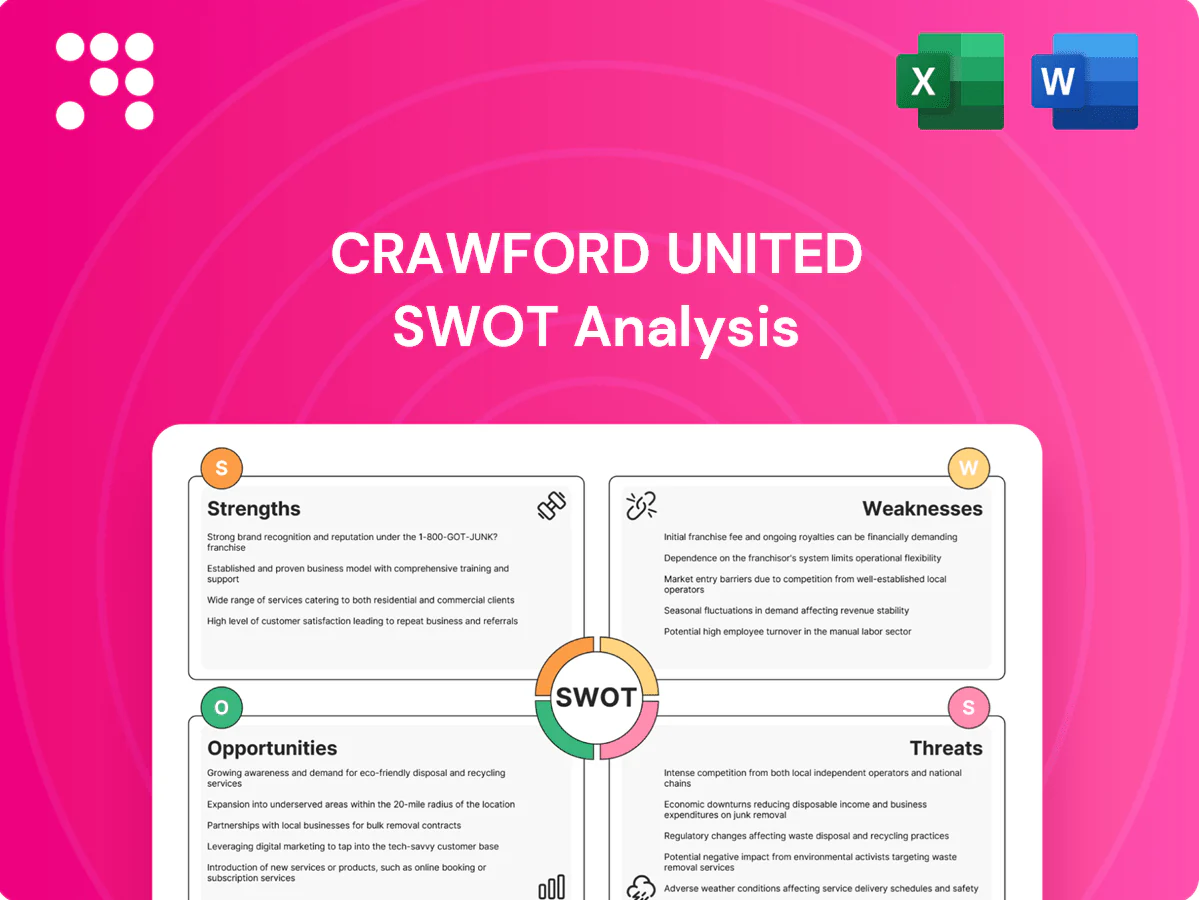

Crawford United SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Crawford United’s SWOT snapshot highlights resilient market footholds, operational efficiencies, and exposure to regulatory and competitive pressures. Our full SWOT unpacks financial context, strategic gaps, and growth levers with research-backed detail. Ideal for investors, advisors, and strategists seeking actionable insights. Purchase the complete, editable report to plan with confidence.

Strengths

Diversified industrial portfolio

Crawford United's three-segment industrial portfolio—air filtration, automation, and precision metrology—reduces dependence on any single end market and smooths revenue across industrial cycles. This diversification creates optionality to prioritize higher-growth or higher-margin niches and enhances resilience. The complementary mix also supports cross-selling and better capacity utilization.

Precision-engineering capabilities

High-accuracy design and manufacturing underpin Crawford United’s product quality and performance, enabling consistent delivery within tight tolerances that mission-critical customers demand. The company’s precision know-how forms a meaningful barrier to entry, supporting premium pricing and higher margins. This expertise reinforces brand credibility in aerospace and medical segments where reliability and exact tolerances are prioritized.

Aftermarket and services potential

Aftermarket air filtration and calibration generate recurring consumables and service revenue—filter replacements and scheduled calibrations typically recur quarterly to annually, boosting lifetime customer value. Recurring revenue in industrial-equipment aftermarket often exceeds 30% of service income, improving revenue visibility and margin stability. Regular service deepens customer relationships and enables cross-sell of parts and diagnostics.

Customized automation solutions

Customized automation solutions let Crawford United design equipment that directly matches customers’ workflow and productivity requirements, embedding their systems into daily operations and increasing operational reliance. Tailored installations raise customer switching costs and support premium pricing while creating opportunities for follow-on projects, upgrades, and long-term service revenue.

- Addresses specific workflow and productivity needs

- Deepens integration into customer operations

- Raises switching costs and protects pricing

- Drives follow-on projects and upgrade revenue

Cross-industry applications

Crawford United serves manufacturing, healthcare, electronics and other sectors, widening its sales funnel and reducing sector concentration risk; cross-industry applicability lets the company target emerging high-growth verticals and pivot as demand shifts. This diversification supports revenue resilience and strategic flexibility amid shifting market dynamics.

- Multi-sector reach: manufacturing, healthcare, electronics, others

- Reduced concentration risk; broader sales funnel

- Can reweight toward emerging high-growth verticals

Three-segment portfolio: recurring aftermarket, precision manufacturing, diversified end-markets

Three-segment portfolio (air filtration, automation, precision metrology) diversifies end-market exposure and enables cross-selling; precision manufacturing creates barriers to entry and supports premium pricing; recurring aftermarket services (filters, calibrations) improve revenue visibility—industry benchmark: aftermarket often >30% of service income; customized automation raises switching costs.

| Metric | Value |

|---|---|

| Aftermarket share (industry) | >30% |

| Service cadence | Quarterly–Annually |

What is included in the product

Delivers a strategic overview of Crawford United’s internal strengths and weaknesses and external opportunities and threats, highlighting key growth drivers, operational gaps, competitive positioning, and risks shaping the company’s future.

Provides a concise, editable SWOT matrix for Crawford United that quickly identifies strategic pain points and enables fast corrective action across teams.

Weaknesses

Smaller scale vs. majors

Compared with global industrial leaders, Crawford United likely has less purchasing power and narrower brand reach, which can compress gross margins and reduce supplier discounts. Limited marketing and R&D budgets constrain product development and market expansion. The company’s negotiating leverage is weaker, making cost control harder. Large-scale bids and multinational contracts are more difficult to win.

Capital and labor intensity

Automation and precision manufacturing demand skilled technicians and steady capex for robots, CNCs and metrology, increasing fixed costs and cash needs. Tight labor markets push wage inflation and can delay delivery schedules. Equipment refresh cycles and compliance testing add recurring capital outlays; utilization swings therefore quickly depress margins. World Economic Forum estimated 85 million jobs may be displaced or transformed by 2025, intensifying reskilling needs.

Project-driven revenue volatility

Custom automation revenue at Crawford United is highly project-driven, making results sensitive to timing, scope changes and client approvals, and slippage can shift material revenue between quarters. Large builds can cause working capital to spike as inventory and WIP rise, complicating cash management. This variability increases forecasting complexity for investors and management and raises short-term earnings predictability risks.

Integration complexity across segments

Distinct businesses require different sales cycles and technical expertise, making cross-segment integration complex; aligning processes, ERP and quality systems is difficult and can dilute operational focus while increasing overhead. Misalignment can push synergy capture into the 18–36 month window; McKinsey-style industry analysis notes roughly 60–70% of deals fail to realize expected synergies.

Potential customer concentration

Potential customer concentration: niche industrial suppliers like Crawford United commonly rely on a few large accounts, which heightens revenue risk if a program ends and can force pricing concessions to retain anchor customers; 2024 industry risk reports identify customer concentration as a top supplier vulnerability.

- Top-customer dependency

- Program termination risk

- Pricing pressure from anchors

- Urgent need to diversify

Smaller manufacturer faces margin squeeze, high automation capex and delayed cross-segment synergies

Compared with global leaders Crawford United has weaker scale, limited R&D/marketing budgets and tighter negotiating leverage, compressing margins and making large multinational bids harder. High capex for automation, tight labor markets and project-driven revenue increase cash volatility; WEF estimated 85 million jobs may be transformed by 2025. Cross-segment integration raises overhead and delays synergies (often 18–36 months; 60–70% fail).

| Metric | Data |

|---|---|

| Jobs transformed (WEF) | 85 million by 2025 |

| Synergy realization | 18–36 months; 60–70% fail |

| 2024 industry risk | Customer concentration top supplier vulnerability |

Full Version Awaits

Crawford United SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live excerpt of the complete, editable file; the full document becomes available immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Crawford United’s SWOT snapshot highlights resilient market footholds, operational efficiencies, and exposure to regulatory and competitive pressures. Our full SWOT unpacks financial context, strategic gaps, and growth levers with research-backed detail. Ideal for investors, advisors, and strategists seeking actionable insights. Purchase the complete, editable report to plan with confidence.

Strengths

Diversified industrial portfolio

Crawford United's three-segment industrial portfolio—air filtration, automation, and precision metrology—reduces dependence on any single end market and smooths revenue across industrial cycles. This diversification creates optionality to prioritize higher-growth or higher-margin niches and enhances resilience. The complementary mix also supports cross-selling and better capacity utilization.

Precision-engineering capabilities

High-accuracy design and manufacturing underpin Crawford United’s product quality and performance, enabling consistent delivery within tight tolerances that mission-critical customers demand. The company’s precision know-how forms a meaningful barrier to entry, supporting premium pricing and higher margins. This expertise reinforces brand credibility in aerospace and medical segments where reliability and exact tolerances are prioritized.

Aftermarket and services potential

Aftermarket air filtration and calibration generate recurring consumables and service revenue—filter replacements and scheduled calibrations typically recur quarterly to annually, boosting lifetime customer value. Recurring revenue in industrial-equipment aftermarket often exceeds 30% of service income, improving revenue visibility and margin stability. Regular service deepens customer relationships and enables cross-sell of parts and diagnostics.

Customized automation solutions

Customized automation solutions let Crawford United design equipment that directly matches customers’ workflow and productivity requirements, embedding their systems into daily operations and increasing operational reliance. Tailored installations raise customer switching costs and support premium pricing while creating opportunities for follow-on projects, upgrades, and long-term service revenue.

- Addresses specific workflow and productivity needs

- Deepens integration into customer operations

- Raises switching costs and protects pricing

- Drives follow-on projects and upgrade revenue

Cross-industry applications

Crawford United serves manufacturing, healthcare, electronics and other sectors, widening its sales funnel and reducing sector concentration risk; cross-industry applicability lets the company target emerging high-growth verticals and pivot as demand shifts. This diversification supports revenue resilience and strategic flexibility amid shifting market dynamics.

- Multi-sector reach: manufacturing, healthcare, electronics, others

- Reduced concentration risk; broader sales funnel

- Can reweight toward emerging high-growth verticals

Three-segment portfolio: recurring aftermarket, precision manufacturing, diversified end-markets

Three-segment portfolio (air filtration, automation, precision metrology) diversifies end-market exposure and enables cross-selling; precision manufacturing creates barriers to entry and supports premium pricing; recurring aftermarket services (filters, calibrations) improve revenue visibility—industry benchmark: aftermarket often >30% of service income; customized automation raises switching costs.

| Metric | Value |

|---|---|

| Aftermarket share (industry) | >30% |

| Service cadence | Quarterly–Annually |

What is included in the product

Delivers a strategic overview of Crawford United’s internal strengths and weaknesses and external opportunities and threats, highlighting key growth drivers, operational gaps, competitive positioning, and risks shaping the company’s future.

Provides a concise, editable SWOT matrix for Crawford United that quickly identifies strategic pain points and enables fast corrective action across teams.

Weaknesses

Smaller scale vs. majors

Compared with global industrial leaders, Crawford United likely has less purchasing power and narrower brand reach, which can compress gross margins and reduce supplier discounts. Limited marketing and R&D budgets constrain product development and market expansion. The company’s negotiating leverage is weaker, making cost control harder. Large-scale bids and multinational contracts are more difficult to win.

Capital and labor intensity

Automation and precision manufacturing demand skilled technicians and steady capex for robots, CNCs and metrology, increasing fixed costs and cash needs. Tight labor markets push wage inflation and can delay delivery schedules. Equipment refresh cycles and compliance testing add recurring capital outlays; utilization swings therefore quickly depress margins. World Economic Forum estimated 85 million jobs may be displaced or transformed by 2025, intensifying reskilling needs.

Project-driven revenue volatility

Custom automation revenue at Crawford United is highly project-driven, making results sensitive to timing, scope changes and client approvals, and slippage can shift material revenue between quarters. Large builds can cause working capital to spike as inventory and WIP rise, complicating cash management. This variability increases forecasting complexity for investors and management and raises short-term earnings predictability risks.

Integration complexity across segments

Distinct businesses require different sales cycles and technical expertise, making cross-segment integration complex; aligning processes, ERP and quality systems is difficult and can dilute operational focus while increasing overhead. Misalignment can push synergy capture into the 18–36 month window; McKinsey-style industry analysis notes roughly 60–70% of deals fail to realize expected synergies.

Potential customer concentration

Potential customer concentration: niche industrial suppliers like Crawford United commonly rely on a few large accounts, which heightens revenue risk if a program ends and can force pricing concessions to retain anchor customers; 2024 industry risk reports identify customer concentration as a top supplier vulnerability.

- Top-customer dependency

- Program termination risk

- Pricing pressure from anchors

- Urgent need to diversify

Smaller manufacturer faces margin squeeze, high automation capex and delayed cross-segment synergies

Compared with global leaders Crawford United has weaker scale, limited R&D/marketing budgets and tighter negotiating leverage, compressing margins and making large multinational bids harder. High capex for automation, tight labor markets and project-driven revenue increase cash volatility; WEF estimated 85 million jobs may be transformed by 2025. Cross-segment integration raises overhead and delays synergies (often 18–36 months; 60–70% fail).

| Metric | Data |

|---|---|

| Jobs transformed (WEF) | 85 million by 2025 |

| Synergy realization | 18–36 months; 60–70% fail |

| 2024 industry risk | Customer concentration top supplier vulnerability |

Full Version Awaits

Crawford United SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live excerpt of the complete, editable file; the full document becomes available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Crawford United’s SWOT snapshot highlights resilient market footholds, operational efficiencies, and exposure to regulatory and competitive pressures. Our full SWOT unpacks financial context, strategic gaps, and growth levers with research-backed detail. Ideal for investors, advisors, and strategists seeking actionable insights. Purchase the complete, editable report to plan with confidence.

Strengths

Diversified industrial portfolio

Crawford United's three-segment industrial portfolio—air filtration, automation, and precision metrology—reduces dependence on any single end market and smooths revenue across industrial cycles. This diversification creates optionality to prioritize higher-growth or higher-margin niches and enhances resilience. The complementary mix also supports cross-selling and better capacity utilization.

Precision-engineering capabilities

High-accuracy design and manufacturing underpin Crawford United’s product quality and performance, enabling consistent delivery within tight tolerances that mission-critical customers demand. The company’s precision know-how forms a meaningful barrier to entry, supporting premium pricing and higher margins. This expertise reinforces brand credibility in aerospace and medical segments where reliability and exact tolerances are prioritized.

Aftermarket and services potential

Aftermarket air filtration and calibration generate recurring consumables and service revenue—filter replacements and scheduled calibrations typically recur quarterly to annually, boosting lifetime customer value. Recurring revenue in industrial-equipment aftermarket often exceeds 30% of service income, improving revenue visibility and margin stability. Regular service deepens customer relationships and enables cross-sell of parts and diagnostics.

Customized automation solutions

Customized automation solutions let Crawford United design equipment that directly matches customers’ workflow and productivity requirements, embedding their systems into daily operations and increasing operational reliance. Tailored installations raise customer switching costs and support premium pricing while creating opportunities for follow-on projects, upgrades, and long-term service revenue.

- Addresses specific workflow and productivity needs

- Deepens integration into customer operations

- Raises switching costs and protects pricing

- Drives follow-on projects and upgrade revenue

Cross-industry applications

Crawford United serves manufacturing, healthcare, electronics and other sectors, widening its sales funnel and reducing sector concentration risk; cross-industry applicability lets the company target emerging high-growth verticals and pivot as demand shifts. This diversification supports revenue resilience and strategic flexibility amid shifting market dynamics.

- Multi-sector reach: manufacturing, healthcare, electronics, others

- Reduced concentration risk; broader sales funnel

- Can reweight toward emerging high-growth verticals

Three-segment portfolio: recurring aftermarket, precision manufacturing, diversified end-markets

Three-segment portfolio (air filtration, automation, precision metrology) diversifies end-market exposure and enables cross-selling; precision manufacturing creates barriers to entry and supports premium pricing; recurring aftermarket services (filters, calibrations) improve revenue visibility—industry benchmark: aftermarket often >30% of service income; customized automation raises switching costs.

| Metric | Value |

|---|---|

| Aftermarket share (industry) | >30% |

| Service cadence | Quarterly–Annually |

What is included in the product

Delivers a strategic overview of Crawford United’s internal strengths and weaknesses and external opportunities and threats, highlighting key growth drivers, operational gaps, competitive positioning, and risks shaping the company’s future.

Provides a concise, editable SWOT matrix for Crawford United that quickly identifies strategic pain points and enables fast corrective action across teams.

Weaknesses

Smaller scale vs. majors

Compared with global industrial leaders, Crawford United likely has less purchasing power and narrower brand reach, which can compress gross margins and reduce supplier discounts. Limited marketing and R&D budgets constrain product development and market expansion. The company’s negotiating leverage is weaker, making cost control harder. Large-scale bids and multinational contracts are more difficult to win.

Capital and labor intensity

Automation and precision manufacturing demand skilled technicians and steady capex for robots, CNCs and metrology, increasing fixed costs and cash needs. Tight labor markets push wage inflation and can delay delivery schedules. Equipment refresh cycles and compliance testing add recurring capital outlays; utilization swings therefore quickly depress margins. World Economic Forum estimated 85 million jobs may be displaced or transformed by 2025, intensifying reskilling needs.

Project-driven revenue volatility

Custom automation revenue at Crawford United is highly project-driven, making results sensitive to timing, scope changes and client approvals, and slippage can shift material revenue between quarters. Large builds can cause working capital to spike as inventory and WIP rise, complicating cash management. This variability increases forecasting complexity for investors and management and raises short-term earnings predictability risks.

Integration complexity across segments

Distinct businesses require different sales cycles and technical expertise, making cross-segment integration complex; aligning processes, ERP and quality systems is difficult and can dilute operational focus while increasing overhead. Misalignment can push synergy capture into the 18–36 month window; McKinsey-style industry analysis notes roughly 60–70% of deals fail to realize expected synergies.

Potential customer concentration

Potential customer concentration: niche industrial suppliers like Crawford United commonly rely on a few large accounts, which heightens revenue risk if a program ends and can force pricing concessions to retain anchor customers; 2024 industry risk reports identify customer concentration as a top supplier vulnerability.

- Top-customer dependency

- Program termination risk

- Pricing pressure from anchors

- Urgent need to diversify

Smaller manufacturer faces margin squeeze, high automation capex and delayed cross-segment synergies

Compared with global leaders Crawford United has weaker scale, limited R&D/marketing budgets and tighter negotiating leverage, compressing margins and making large multinational bids harder. High capex for automation, tight labor markets and project-driven revenue increase cash volatility; WEF estimated 85 million jobs may be transformed by 2025. Cross-segment integration raises overhead and delays synergies (often 18–36 months; 60–70% fail).

| Metric | Data |

|---|---|

| Jobs transformed (WEF) | 85 million by 2025 |

| Synergy realization | 18–36 months; 60–70% fail |

| 2024 industry risk | Customer concentration top supplier vulnerability |

Full Version Awaits

Crawford United SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live excerpt of the complete, editable file; the full document becomes available immediately after checkout.