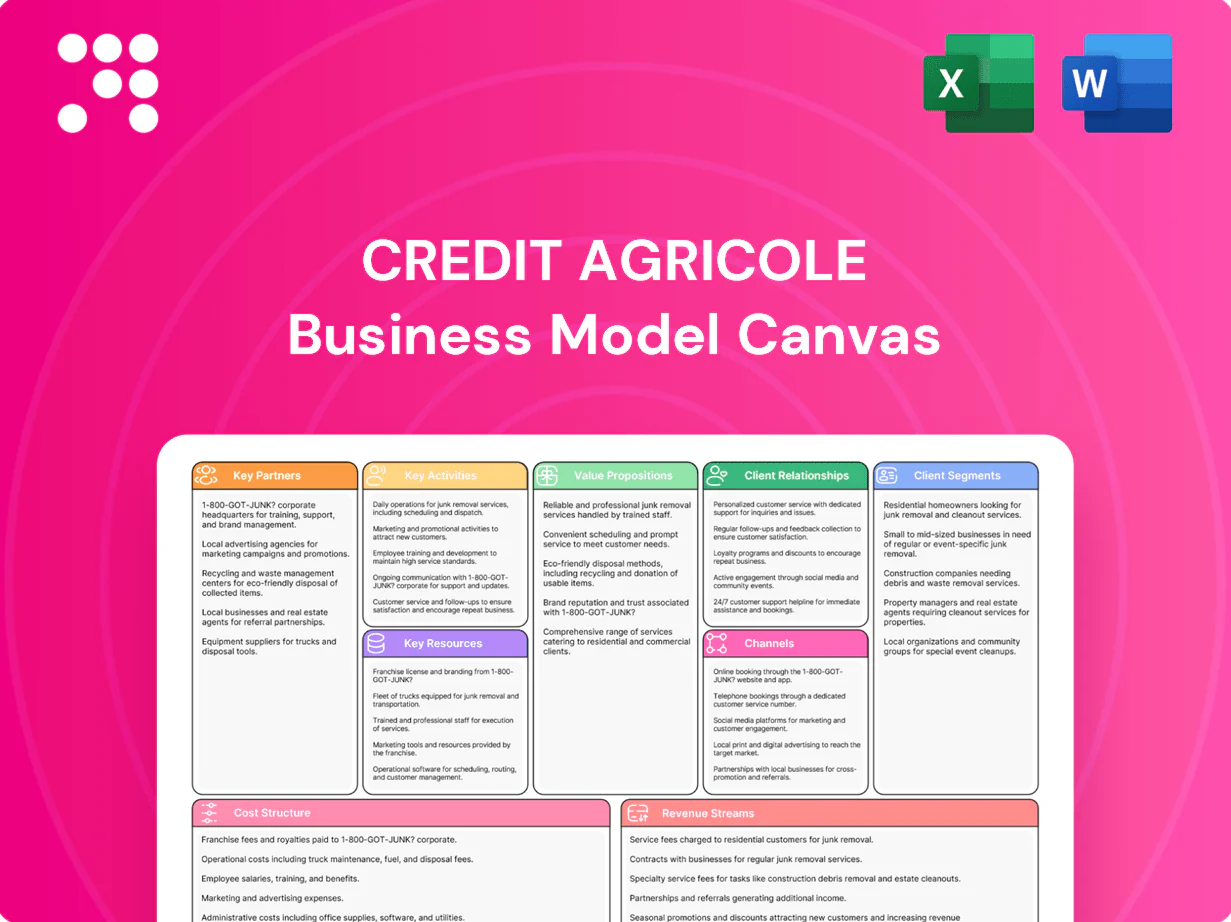

Credit Agricole Business Model Canvas

Concise Business Model Canvas for a leading bank: strategic blueprint for investors

Unlock the full strategic blueprint behind Crédit Agricole’s business model with our in-depth Business Model Canvas. This concise, company-specific analysis uncovers value propositions, revenue streams, partnerships and cost drivers to inform better decisions. Purchase the full editable Word & Excel canvas to benchmark strategies, build investor decks, or accelerate your strategic planning.

Partnerships

Regional cooperative banks and local mutuals

The network of 39 regional cooperative banks underpins Crédit Agricole's distribution, funding and customer acquisition across France, supporting a group with over EUR 2 trillion in assets (2023). Local mutuals provide governance input and member engagement aligned with cooperative values, ensuring proximity to clients and granular risk knowledge. This model captures scale benefits while preserving local decision-making and credit discretion.

Fintechs and technology vendors

Alliances with fintechs accelerate digital onboarding, payments innovation and analytics, feeding services to Crédit Agricole's network of about 52 million customers. Core vendors underpin cloud, cybersecurity and core-banking modernization, enabling scalable deployments. Co-development via APIs shortens time-to-market for new services and helps balance legacy stability with agile innovation.

Payment networks and processors

Ties with Visa, Mastercard and domestic schemes operating in over 200 countries and territories enable Crédit Agricole to issue cards, acquire payments and broaden acceptance. Processors deliver near-real-time settlement, fraud controls and value-added services that improve authorization rates. These partnerships expand merchant reach, enhance customer payment experiences and generate fee income and interchange efficiencies for the group.

Institutional investors and funding partners

Relationships with institutional investors, supranationals and wholesale markets underpin Crédit Agricole’s liquidity and capital optimization, supporting diversified issuance across covered bonds, senior debt and securitisations; the group reported ~€2.3tn total assets and a CET1 ratio near 12.9% in 2024, reinforcing resilience through rate and credit cycles. Strategic co-lending and syndications expand balance-sheet capacity and risk-sharing across portfolios.

- Institutional funding: wholesale markets and supranationals

- Instruments: covered bonds, senior debt, securitisations

- Structuring: co-lending and syndications

- Outcome: liquidity, capital diversification, cycle resilience

Regulators and industry bodies

Constructive engagement with European and national regulators ensures compliance and operational continuity across 27 EU member states and the UK, supporting Crédit Agricole’s cross-border operations; industry associations like the European Banking Federation enable best-practice sharing and standard-setting; these partnerships shape prudential, ESG and open-banking frameworks affecting ~450 million EU/EEA consumers and reduce regulatory friction and reputational risk.

- Regulatory footprint: 27 EU member states + UK

- Consumer scope: ~450 million EU/EEA population

- Focus areas: prudential capital, ESG, open-banking

39-region network, ~52m customers and €2.3tn assets fuel global payments

Crédit Agricole leverages 39 regional banks, ~52m customers and ~€2.3tn assets (2024) to scale distribution; fintech and card partnerships boost digital services and payments across 200+ countries. Wholesale investors and covered bonds support liquidity; CET1 ~12.9% (2024) underpins resilience. Regulatory ties across 27 EU states + UK harmonize compliance and open-banking efforts.

| Partnership | KPI | 2024 |

|---|---|---|

| Regional network | Banks | 39 |

| Retail reach | Customers | ~52m |

| Balance sheet | Total assets | €2.3tn |

| Capital | CET1 | ~12.9% |

| Payments | Coverage | 200+ countries |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Crédit Agricole that maps customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks, with competitive analysis and SWOT insights to support presentations, funding discussions, and strategic decision-making.

High-level, editable Business Model Canvas for Crédit Agricole that condenses the bank’s strategy into a one-page snapshot, quickly revealing revenue drivers, cost centers, and customer segments to relieve analysis bottlenecks. Shareable and adaptable for teams, it saves hours of structuring and enables fast comparisons or executive summaries.

Activities

Retail and commercial banking

Retail and commercial banking anchors Crédit Agricole with about 50 million customers; deposit gathering and payments foster core relationships while driving roughly €1.8 trillion in household and corporate deposits. Mortgage, consumer and SME lending—anchoring local economies—represent the bulk of the loan book, supporting regional growth. Daily banking services deliver engagement and data insights; pricing and risk calibration adapt to macro shifts and a CET1 ratio around 13%.

Corporate and investment banking

Origination, advisory and markets activities serve large corporates and institutions, structuring M&A, derivatives and bespoke financing across sectors. Trade finance, cash management and structured finance are core pillars delivering working capital and project solutions. Risk intermediation in rates, FX and credit supports client hedging while syndication and DCM/ECM provide capital access; Credit Agricole Group reported about €2.1tn total assets in 2023.

Asset management and insurance operations

Manufacturing and distribution of funds, savings and protection solutions broaden share of wallet, supported by Amundi which managed about €2.3 trillion AUM in 2024. Underwriting, claims handling and actuarial management balance growth and risk through centralized reserving and stress testing. Bancassurance synergies leverage 50+ million group customers via branches and digital channels. Product innovation targets regulatory compliance and ESG integration across offerings.

Risk management and compliance

Risk management and compliance at Crédit Agricole safeguard capital through credit, market, liquidity and operational risk frameworks, with a reported CET1 ratio of 12.9% and group total assets ~€1.9tn in 2024. AML/KYC, sanctions and conduct controls protect clients and reputation; stress testing and conservative provisioning manage cycle volatility. Data governance and model risk oversight improve decision quality and model reliability.

- Credit risk controls

- Market & liquidity frameworks

- AML/KYC & sanctions

- Stress testing & provisioning

- Data governance & model oversight

Digital transformation and data analytics

Digital transformation at Crédit Agricole modernizes core systems, APIs and cloud to speed time-to-market and improve reliability; in 2024 the group accelerated cloud migration and platform consolidation. Advanced analytics and AI personalize offers and strengthen fraud detection, while UX optimization lifts acquisition and retention. Automation cuts cost-to-serve and operational errors across retail and corporate channels.

- 2024 focus: cloud-first core modernization

- AI/analytics: personalization + fraud detection

- UX: improved acquisition & retention

- Automation: lower cost-to-serve, fewer errors

50m customers, €1.8tn deposits

Retail/commercial: 50m customers, €1.8tn deposits; mortgages, consumer and SME lending core. Corporates/markets: DCM/ECM, trade finance; group assets ~€1.9tn (2024). Asset management/bancassurance: Amundi AUM €2.3tn (2024). Risk/compliance: CET1 12.9%, AML/KYC, stress testing.

| Metric | 2024 |

|---|---|

| Customers | 50m |

| Deposits | €1.8tn |

| Total assets | €1.9tn |

| Amundi AUM | €2.3tn |

| CET1 | 12.9% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Credit Agricole Business Model Canvas you will receive after purchase. It's not a mockup—this view shows the live file with the same structure, content and layout. After purchase you'll download the identical, editable document in Word and Excel, ready to present or customize.

Concise Business Model Canvas for a leading bank: strategic blueprint for investors

Unlock the full strategic blueprint behind Crédit Agricole’s business model with our in-depth Business Model Canvas. This concise, company-specific analysis uncovers value propositions, revenue streams, partnerships and cost drivers to inform better decisions. Purchase the full editable Word & Excel canvas to benchmark strategies, build investor decks, or accelerate your strategic planning.

Partnerships

Regional cooperative banks and local mutuals

The network of 39 regional cooperative banks underpins Crédit Agricole's distribution, funding and customer acquisition across France, supporting a group with over EUR 2 trillion in assets (2023). Local mutuals provide governance input and member engagement aligned with cooperative values, ensuring proximity to clients and granular risk knowledge. This model captures scale benefits while preserving local decision-making and credit discretion.

Fintechs and technology vendors

Alliances with fintechs accelerate digital onboarding, payments innovation and analytics, feeding services to Crédit Agricole's network of about 52 million customers. Core vendors underpin cloud, cybersecurity and core-banking modernization, enabling scalable deployments. Co-development via APIs shortens time-to-market for new services and helps balance legacy stability with agile innovation.

Payment networks and processors

Ties with Visa, Mastercard and domestic schemes operating in over 200 countries and territories enable Crédit Agricole to issue cards, acquire payments and broaden acceptance. Processors deliver near-real-time settlement, fraud controls and value-added services that improve authorization rates. These partnerships expand merchant reach, enhance customer payment experiences and generate fee income and interchange efficiencies for the group.

Institutional investors and funding partners

Relationships with institutional investors, supranationals and wholesale markets underpin Crédit Agricole’s liquidity and capital optimization, supporting diversified issuance across covered bonds, senior debt and securitisations; the group reported ~€2.3tn total assets and a CET1 ratio near 12.9% in 2024, reinforcing resilience through rate and credit cycles. Strategic co-lending and syndications expand balance-sheet capacity and risk-sharing across portfolios.

- Institutional funding: wholesale markets and supranationals

- Instruments: covered bonds, senior debt, securitisations

- Structuring: co-lending and syndications

- Outcome: liquidity, capital diversification, cycle resilience

Regulators and industry bodies

Constructive engagement with European and national regulators ensures compliance and operational continuity across 27 EU member states and the UK, supporting Crédit Agricole’s cross-border operations; industry associations like the European Banking Federation enable best-practice sharing and standard-setting; these partnerships shape prudential, ESG and open-banking frameworks affecting ~450 million EU/EEA consumers and reduce regulatory friction and reputational risk.

- Regulatory footprint: 27 EU member states + UK

- Consumer scope: ~450 million EU/EEA population

- Focus areas: prudential capital, ESG, open-banking

39-region network, ~52m customers and €2.3tn assets fuel global payments

Crédit Agricole leverages 39 regional banks, ~52m customers and ~€2.3tn assets (2024) to scale distribution; fintech and card partnerships boost digital services and payments across 200+ countries. Wholesale investors and covered bonds support liquidity; CET1 ~12.9% (2024) underpins resilience. Regulatory ties across 27 EU states + UK harmonize compliance and open-banking efforts.

| Partnership | KPI | 2024 |

|---|---|---|

| Regional network | Banks | 39 |

| Retail reach | Customers | ~52m |

| Balance sheet | Total assets | €2.3tn |

| Capital | CET1 | ~12.9% |

| Payments | Coverage | 200+ countries |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Crédit Agricole that maps customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks, with competitive analysis and SWOT insights to support presentations, funding discussions, and strategic decision-making.

High-level, editable Business Model Canvas for Crédit Agricole that condenses the bank’s strategy into a one-page snapshot, quickly revealing revenue drivers, cost centers, and customer segments to relieve analysis bottlenecks. Shareable and adaptable for teams, it saves hours of structuring and enables fast comparisons or executive summaries.

Activities

Retail and commercial banking

Retail and commercial banking anchors Crédit Agricole with about 50 million customers; deposit gathering and payments foster core relationships while driving roughly €1.8 trillion in household and corporate deposits. Mortgage, consumer and SME lending—anchoring local economies—represent the bulk of the loan book, supporting regional growth. Daily banking services deliver engagement and data insights; pricing and risk calibration adapt to macro shifts and a CET1 ratio around 13%.

Corporate and investment banking

Origination, advisory and markets activities serve large corporates and institutions, structuring M&A, derivatives and bespoke financing across sectors. Trade finance, cash management and structured finance are core pillars delivering working capital and project solutions. Risk intermediation in rates, FX and credit supports client hedging while syndication and DCM/ECM provide capital access; Credit Agricole Group reported about €2.1tn total assets in 2023.

Asset management and insurance operations

Manufacturing and distribution of funds, savings and protection solutions broaden share of wallet, supported by Amundi which managed about €2.3 trillion AUM in 2024. Underwriting, claims handling and actuarial management balance growth and risk through centralized reserving and stress testing. Bancassurance synergies leverage 50+ million group customers via branches and digital channels. Product innovation targets regulatory compliance and ESG integration across offerings.

Risk management and compliance

Risk management and compliance at Crédit Agricole safeguard capital through credit, market, liquidity and operational risk frameworks, with a reported CET1 ratio of 12.9% and group total assets ~€1.9tn in 2024. AML/KYC, sanctions and conduct controls protect clients and reputation; stress testing and conservative provisioning manage cycle volatility. Data governance and model risk oversight improve decision quality and model reliability.

- Credit risk controls

- Market & liquidity frameworks

- AML/KYC & sanctions

- Stress testing & provisioning

- Data governance & model oversight

Digital transformation and data analytics

Digital transformation at Crédit Agricole modernizes core systems, APIs and cloud to speed time-to-market and improve reliability; in 2024 the group accelerated cloud migration and platform consolidation. Advanced analytics and AI personalize offers and strengthen fraud detection, while UX optimization lifts acquisition and retention. Automation cuts cost-to-serve and operational errors across retail and corporate channels.

- 2024 focus: cloud-first core modernization

- AI/analytics: personalization + fraud detection

- UX: improved acquisition & retention

- Automation: lower cost-to-serve, fewer errors

50m customers, €1.8tn deposits

Retail/commercial: 50m customers, €1.8tn deposits; mortgages, consumer and SME lending core. Corporates/markets: DCM/ECM, trade finance; group assets ~€1.9tn (2024). Asset management/bancassurance: Amundi AUM €2.3tn (2024). Risk/compliance: CET1 12.9%, AML/KYC, stress testing.

| Metric | 2024 |

|---|---|

| Customers | 50m |

| Deposits | €1.8tn |

| Total assets | €1.9tn |

| Amundi AUM | €2.3tn |

| CET1 | 12.9% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Credit Agricole Business Model Canvas you will receive after purchase. It's not a mockup—this view shows the live file with the same structure, content and layout. After purchase you'll download the identical, editable document in Word and Excel, ready to present or customize.

Original: $10.00

-65%$10.00

$3.50Description

Concise Business Model Canvas for a leading bank: strategic blueprint for investors

Unlock the full strategic blueprint behind Crédit Agricole’s business model with our in-depth Business Model Canvas. This concise, company-specific analysis uncovers value propositions, revenue streams, partnerships and cost drivers to inform better decisions. Purchase the full editable Word & Excel canvas to benchmark strategies, build investor decks, or accelerate your strategic planning.

Partnerships

Regional cooperative banks and local mutuals

The network of 39 regional cooperative banks underpins Crédit Agricole's distribution, funding and customer acquisition across France, supporting a group with over EUR 2 trillion in assets (2023). Local mutuals provide governance input and member engagement aligned with cooperative values, ensuring proximity to clients and granular risk knowledge. This model captures scale benefits while preserving local decision-making and credit discretion.

Fintechs and technology vendors

Alliances with fintechs accelerate digital onboarding, payments innovation and analytics, feeding services to Crédit Agricole's network of about 52 million customers. Core vendors underpin cloud, cybersecurity and core-banking modernization, enabling scalable deployments. Co-development via APIs shortens time-to-market for new services and helps balance legacy stability with agile innovation.

Payment networks and processors

Ties with Visa, Mastercard and domestic schemes operating in over 200 countries and territories enable Crédit Agricole to issue cards, acquire payments and broaden acceptance. Processors deliver near-real-time settlement, fraud controls and value-added services that improve authorization rates. These partnerships expand merchant reach, enhance customer payment experiences and generate fee income and interchange efficiencies for the group.

Institutional investors and funding partners

Relationships with institutional investors, supranationals and wholesale markets underpin Crédit Agricole’s liquidity and capital optimization, supporting diversified issuance across covered bonds, senior debt and securitisations; the group reported ~€2.3tn total assets and a CET1 ratio near 12.9% in 2024, reinforcing resilience through rate and credit cycles. Strategic co-lending and syndications expand balance-sheet capacity and risk-sharing across portfolios.

- Institutional funding: wholesale markets and supranationals

- Instruments: covered bonds, senior debt, securitisations

- Structuring: co-lending and syndications

- Outcome: liquidity, capital diversification, cycle resilience

Regulators and industry bodies

Constructive engagement with European and national regulators ensures compliance and operational continuity across 27 EU member states and the UK, supporting Crédit Agricole’s cross-border operations; industry associations like the European Banking Federation enable best-practice sharing and standard-setting; these partnerships shape prudential, ESG and open-banking frameworks affecting ~450 million EU/EEA consumers and reduce regulatory friction and reputational risk.

- Regulatory footprint: 27 EU member states + UK

- Consumer scope: ~450 million EU/EEA population

- Focus areas: prudential capital, ESG, open-banking

39-region network, ~52m customers and €2.3tn assets fuel global payments

Crédit Agricole leverages 39 regional banks, ~52m customers and ~€2.3tn assets (2024) to scale distribution; fintech and card partnerships boost digital services and payments across 200+ countries. Wholesale investors and covered bonds support liquidity; CET1 ~12.9% (2024) underpins resilience. Regulatory ties across 27 EU states + UK harmonize compliance and open-banking efforts.

| Partnership | KPI | 2024 |

|---|---|---|

| Regional network | Banks | 39 |

| Retail reach | Customers | ~52m |

| Balance sheet | Total assets | €2.3tn |

| Capital | CET1 | ~12.9% |

| Payments | Coverage | 200+ countries |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Crédit Agricole that maps customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks, with competitive analysis and SWOT insights to support presentations, funding discussions, and strategic decision-making.

High-level, editable Business Model Canvas for Crédit Agricole that condenses the bank’s strategy into a one-page snapshot, quickly revealing revenue drivers, cost centers, and customer segments to relieve analysis bottlenecks. Shareable and adaptable for teams, it saves hours of structuring and enables fast comparisons or executive summaries.

Activities

Retail and commercial banking

Retail and commercial banking anchors Crédit Agricole with about 50 million customers; deposit gathering and payments foster core relationships while driving roughly €1.8 trillion in household and corporate deposits. Mortgage, consumer and SME lending—anchoring local economies—represent the bulk of the loan book, supporting regional growth. Daily banking services deliver engagement and data insights; pricing and risk calibration adapt to macro shifts and a CET1 ratio around 13%.

Corporate and investment banking

Origination, advisory and markets activities serve large corporates and institutions, structuring M&A, derivatives and bespoke financing across sectors. Trade finance, cash management and structured finance are core pillars delivering working capital and project solutions. Risk intermediation in rates, FX and credit supports client hedging while syndication and DCM/ECM provide capital access; Credit Agricole Group reported about €2.1tn total assets in 2023.

Asset management and insurance operations

Manufacturing and distribution of funds, savings and protection solutions broaden share of wallet, supported by Amundi which managed about €2.3 trillion AUM in 2024. Underwriting, claims handling and actuarial management balance growth and risk through centralized reserving and stress testing. Bancassurance synergies leverage 50+ million group customers via branches and digital channels. Product innovation targets regulatory compliance and ESG integration across offerings.

Risk management and compliance

Risk management and compliance at Crédit Agricole safeguard capital through credit, market, liquidity and operational risk frameworks, with a reported CET1 ratio of 12.9% and group total assets ~€1.9tn in 2024. AML/KYC, sanctions and conduct controls protect clients and reputation; stress testing and conservative provisioning manage cycle volatility. Data governance and model risk oversight improve decision quality and model reliability.

- Credit risk controls

- Market & liquidity frameworks

- AML/KYC & sanctions

- Stress testing & provisioning

- Data governance & model oversight

Digital transformation and data analytics

Digital transformation at Crédit Agricole modernizes core systems, APIs and cloud to speed time-to-market and improve reliability; in 2024 the group accelerated cloud migration and platform consolidation. Advanced analytics and AI personalize offers and strengthen fraud detection, while UX optimization lifts acquisition and retention. Automation cuts cost-to-serve and operational errors across retail and corporate channels.

- 2024 focus: cloud-first core modernization

- AI/analytics: personalization + fraud detection

- UX: improved acquisition & retention

- Automation: lower cost-to-serve, fewer errors

50m customers, €1.8tn deposits

Retail/commercial: 50m customers, €1.8tn deposits; mortgages, consumer and SME lending core. Corporates/markets: DCM/ECM, trade finance; group assets ~€1.9tn (2024). Asset management/bancassurance: Amundi AUM €2.3tn (2024). Risk/compliance: CET1 12.9%, AML/KYC, stress testing.

| Metric | 2024 |

|---|---|

| Customers | 50m |

| Deposits | €1.8tn |

| Total assets | €1.9tn |

| Amundi AUM | €2.3tn |

| CET1 | 12.9% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Credit Agricole Business Model Canvas you will receive after purchase. It's not a mockup—this view shows the live file with the same structure, content and layout. After purchase you'll download the identical, editable document in Word and Excel, ready to present or customize.