Credit Agricole Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

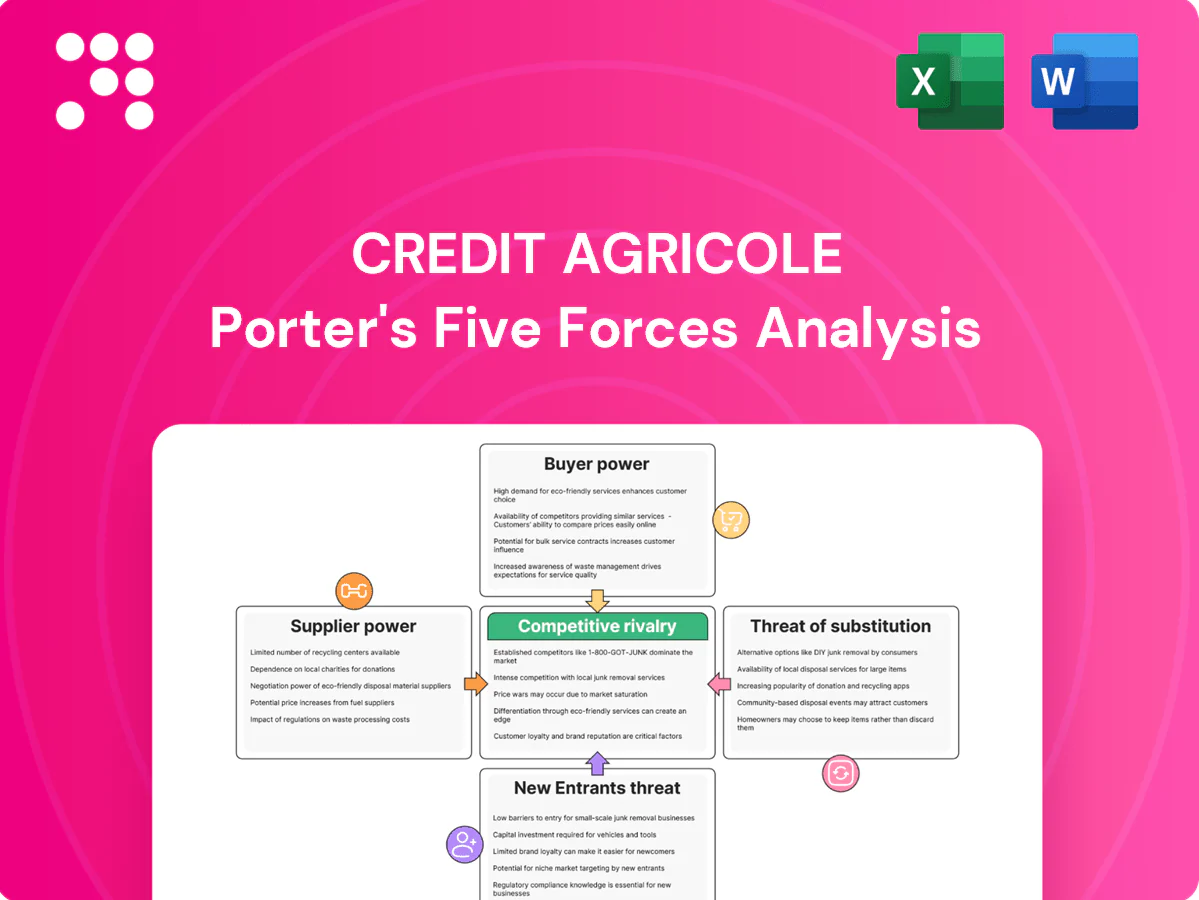

Credit Agricole faces moderate rivalry from large domestic banks, rising digital challengers, strong regulatory constraints, concentrated supplier and funding power, and muted threat from substitutes. This Porter's Five Forces snapshot highlights where strategic pressure and opportunity intersect for the bank. Unlock the full analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or planning decisions.

Suppliers Bargaining Power

Diverse funding base limits single-source leverage

Crédit Agricole funds itself via retail deposits, covered bonds, senior debt and central bank facilities; retail deposits accounted for over 50% of funding in 2024, limiting dependence on any single supplier class. This diversification moderates pricing pressure from wholesale investors during market stress and reduces rollover risk. The cooperative regional bank structure further anchors stable retail funding and customer loyalty.

Stable cooperative deposits dampen rate pressure

Regional cooperative networks give Crédit Agricole sticky, low‑cost deposits—customer deposits exceeded €1 trillion in 2024—so members’ inertia and deep relationships limit supplier bargaining power. Depositors can press for higher rates, but cross‑selling of insurance and savings raises switching frictions, preserving margin stability versus market‑reliant peers.

Wholesale investors exert cyclical power

Bondholders and money markets can reprice funding within days in risk-off periods, with sector/issuer spreads widening and raising funding costs; European bank senior spreads moved hundreds of basis points in 2024 stress episodes. Credit Agricole’s strong CET1 ratio of 12.9% (end-2024) and transparent asset quality limit supplier leverage. Active liability management—smoothing maturities and rebalancing term vs. short-term funding—reduces repricing spikes.

Technology and cloud vendors hold moderate sway

Core banking, cybersecurity, data and cloud providers are concentrated—Gartner 2024 shows AWS 31.8%, Microsoft Azure 23.6% and Google Cloud 11.4% of the IaaS/PaaS market—so vendor stickiness is reinforced by high switching costs, integration complexity and regulatory constraints for banks like Crédit Agricole.

- Multi-vendor + in-house reduces dependency

- Scale enables stronger price and SLA negotiation

- Concentration: AWS 31.8%, Azure 23.6%, GCP 11.4%

Market infrastructures and schemes shape terms

Card networks, SWIFT/SEPA rails and central clearinghouses set mandatory fees and operating rules that materially shape Credit Agricole’s supplier bargaining: SWIFT connects 11,000+ institutions in 200+ countries, SEPA spans 36 European markets, and Visa/Mastercard account for over 70% of global card volume, giving infrastructures structural influence.

- Mandatory compliance raises switching costs

- Regulated governance caps fee hikes

- Network scale delivers offsetting benefits

Supplier power limited: deposits €1tn+, CET1 12.9%

Supplier power is limited: retail deposits >€1tn in 2024 and CET1 12.9% (end-2024) reduce reliance on volatile wholesale funding. Cloud and fintech vendors show concentration (AWS 31.8%, Azure 23.6%), raising switching costs but scale enables stronger negotiation. Card rails and SWIFT (11,000+ institutions) exert structural fees, but regulation caps unilateral fee hikes.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Deposits | €1trn+ | Low supplier power |

| Capital markets | CET1 12.9% | Lower repricing risk |

| Cloud | AWS 31.8% | High switching cost |

| Card/rails | Visa/MC >70% | Structural fees |

What is included in the product

Tailored Porter's Five Forces analysis for Crédit Agricole uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptive forces that could erode market share and profitability; includes strategic implications to reinforce its incumbent advantages and guide investor or management decisions.

One-sheet Porter’s Five Forces for Credit Agricole—clear, customizable pressure levels and an instant radar view that highlights competitive pain points for swift strategy decisions and board-ready slides.

Customers Bargaining Power

High price transparency intensifies client leverage

Digital comparison tools make rates and fees easily comparable, driving client leverage as corporate treasurers routinely run competitive RFPs across lenders; this transparency compresses margins in commoditized products such as mortgages and cash management, forcing banks to compete on price and service. Expanding relationship breadth across products is now essential to defend pricing and preserve share.

Multi-banking reduces dependence on a single bank

Large corporates and affluent clients increasingly multi-bank to spread counterparty risk and extract better pricing, with industry surveys in 2024 indicating majority adoption among top-tier firms; share-of-wallet is therefore contestable at each renewal. Crédit Agricole must win mandates product-by-product as clients split services across lenders. Bundled solutions and superior service quality remain key levers to retain primacy.

Switching costs vary by segment

Switching costs vary: everyday retail accounts face moderate frictions from payments, lending and insurance bundles, while SMEs and corporates incur higher integration costs for cash, FX and ERP links. Crédit Agricole, serving over 50 million customers in 2024, can leverage onboarding complexity to stabilize relationships, but accelerating open banking and API adoption in 2024 steadily lowers barriers.

Cooperative loyalty mitigates churn

Member-owners often value local presence and dividends from cooperative shares, with Groupe Crédit Agricole serving about 52 million customers in 2024, creating relational stickiness beyond pure pricing; community engagement and local branch networks strengthen trust and retention and partially offset digital-only challengers’ offers.

- Local branches + dividends = higher retention

- 2024: ~52M customers supporting relational loyalty

- Community engagement reduces churn vs digital challengers

Mass-affluent and institutional clients negotiate hard

Mass-affluent, asset management and CIB clients at Crédit Agricole demand bespoke pricing and negotiate hard; fee compression persisted in 2024 with industry AM fees trending lower and lending spreads remaining thin, while advisory and distribution reach help offset margin pressure. Performance track record and balance-sheet strength are decisive to retain wallet share amid competitive pricing and value-added service expectations.

- 2024 global wealth ~ $463 trillion (Credit Suisse Global Wealth Report 2024)

- AM fee compression notable across Europe in 2024

- Thin lending spreads raise importance of scale and capital

Rising customer bargaining power squeezes bank margins as open banking cuts switching costs

Customer bargaining power is high due to transparent digital rate comparisons and routine RFPs, compressing margins in mortgages and cash management. Large corporates and mass-affluent clients multi-bank, making share-of-wallet contestable despite Crédit Agricole’s ~52M customers in 2024. Open banking and API uptake steadily lower switching costs, raising pressure on price and service.

| Metric | 2024 |

|---|---|

| Crédit Agricole customers | ~52M |

| Global wealth (Credit Suisse) | $463T |

| AM fee trend (EU) | down |

Same Document Delivered

Credit Agricole Porter's Five Forces Analysis

This preview displays the exact Credit Agricole Porter’s Five Forces Analysis you’ll receive upon purchase—no placeholders or samples. The full document is professionally formatted, ready for download and immediate use, and contains the complete strategic assessment, insights, and actionable conclusions included here.

Go Beyond the Preview—Access the Full Strategic Report

Credit Agricole faces moderate rivalry from large domestic banks, rising digital challengers, strong regulatory constraints, concentrated supplier and funding power, and muted threat from substitutes. This Porter's Five Forces snapshot highlights where strategic pressure and opportunity intersect for the bank. Unlock the full analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or planning decisions.

Suppliers Bargaining Power

Diverse funding base limits single-source leverage

Crédit Agricole funds itself via retail deposits, covered bonds, senior debt and central bank facilities; retail deposits accounted for over 50% of funding in 2024, limiting dependence on any single supplier class. This diversification moderates pricing pressure from wholesale investors during market stress and reduces rollover risk. The cooperative regional bank structure further anchors stable retail funding and customer loyalty.

Stable cooperative deposits dampen rate pressure

Regional cooperative networks give Crédit Agricole sticky, low‑cost deposits—customer deposits exceeded €1 trillion in 2024—so members’ inertia and deep relationships limit supplier bargaining power. Depositors can press for higher rates, but cross‑selling of insurance and savings raises switching frictions, preserving margin stability versus market‑reliant peers.

Wholesale investors exert cyclical power

Bondholders and money markets can reprice funding within days in risk-off periods, with sector/issuer spreads widening and raising funding costs; European bank senior spreads moved hundreds of basis points in 2024 stress episodes. Credit Agricole’s strong CET1 ratio of 12.9% (end-2024) and transparent asset quality limit supplier leverage. Active liability management—smoothing maturities and rebalancing term vs. short-term funding—reduces repricing spikes.

Technology and cloud vendors hold moderate sway

Core banking, cybersecurity, data and cloud providers are concentrated—Gartner 2024 shows AWS 31.8%, Microsoft Azure 23.6% and Google Cloud 11.4% of the IaaS/PaaS market—so vendor stickiness is reinforced by high switching costs, integration complexity and regulatory constraints for banks like Crédit Agricole.

- Multi-vendor + in-house reduces dependency

- Scale enables stronger price and SLA negotiation

- Concentration: AWS 31.8%, Azure 23.6%, GCP 11.4%

Market infrastructures and schemes shape terms

Card networks, SWIFT/SEPA rails and central clearinghouses set mandatory fees and operating rules that materially shape Credit Agricole’s supplier bargaining: SWIFT connects 11,000+ institutions in 200+ countries, SEPA spans 36 European markets, and Visa/Mastercard account for over 70% of global card volume, giving infrastructures structural influence.

- Mandatory compliance raises switching costs

- Regulated governance caps fee hikes

- Network scale delivers offsetting benefits

Supplier power limited: deposits €1tn+, CET1 12.9%

Supplier power is limited: retail deposits >€1tn in 2024 and CET1 12.9% (end-2024) reduce reliance on volatile wholesale funding. Cloud and fintech vendors show concentration (AWS 31.8%, Azure 23.6%), raising switching costs but scale enables stronger negotiation. Card rails and SWIFT (11,000+ institutions) exert structural fees, but regulation caps unilateral fee hikes.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Deposits | €1trn+ | Low supplier power |

| Capital markets | CET1 12.9% | Lower repricing risk |

| Cloud | AWS 31.8% | High switching cost |

| Card/rails | Visa/MC >70% | Structural fees |

What is included in the product

Tailored Porter's Five Forces analysis for Crédit Agricole uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptive forces that could erode market share and profitability; includes strategic implications to reinforce its incumbent advantages and guide investor or management decisions.

One-sheet Porter’s Five Forces for Credit Agricole—clear, customizable pressure levels and an instant radar view that highlights competitive pain points for swift strategy decisions and board-ready slides.

Customers Bargaining Power

High price transparency intensifies client leverage

Digital comparison tools make rates and fees easily comparable, driving client leverage as corporate treasurers routinely run competitive RFPs across lenders; this transparency compresses margins in commoditized products such as mortgages and cash management, forcing banks to compete on price and service. Expanding relationship breadth across products is now essential to defend pricing and preserve share.

Multi-banking reduces dependence on a single bank

Large corporates and affluent clients increasingly multi-bank to spread counterparty risk and extract better pricing, with industry surveys in 2024 indicating majority adoption among top-tier firms; share-of-wallet is therefore contestable at each renewal. Crédit Agricole must win mandates product-by-product as clients split services across lenders. Bundled solutions and superior service quality remain key levers to retain primacy.

Switching costs vary by segment

Switching costs vary: everyday retail accounts face moderate frictions from payments, lending and insurance bundles, while SMEs and corporates incur higher integration costs for cash, FX and ERP links. Crédit Agricole, serving over 50 million customers in 2024, can leverage onboarding complexity to stabilize relationships, but accelerating open banking and API adoption in 2024 steadily lowers barriers.

Cooperative loyalty mitigates churn

Member-owners often value local presence and dividends from cooperative shares, with Groupe Crédit Agricole serving about 52 million customers in 2024, creating relational stickiness beyond pure pricing; community engagement and local branch networks strengthen trust and retention and partially offset digital-only challengers’ offers.

- Local branches + dividends = higher retention

- 2024: ~52M customers supporting relational loyalty

- Community engagement reduces churn vs digital challengers

Mass-affluent and institutional clients negotiate hard

Mass-affluent, asset management and CIB clients at Crédit Agricole demand bespoke pricing and negotiate hard; fee compression persisted in 2024 with industry AM fees trending lower and lending spreads remaining thin, while advisory and distribution reach help offset margin pressure. Performance track record and balance-sheet strength are decisive to retain wallet share amid competitive pricing and value-added service expectations.

- 2024 global wealth ~ $463 trillion (Credit Suisse Global Wealth Report 2024)

- AM fee compression notable across Europe in 2024

- Thin lending spreads raise importance of scale and capital

Rising customer bargaining power squeezes bank margins as open banking cuts switching costs

Customer bargaining power is high due to transparent digital rate comparisons and routine RFPs, compressing margins in mortgages and cash management. Large corporates and mass-affluent clients multi-bank, making share-of-wallet contestable despite Crédit Agricole’s ~52M customers in 2024. Open banking and API uptake steadily lower switching costs, raising pressure on price and service.

| Metric | 2024 |

|---|---|

| Crédit Agricole customers | ~52M |

| Global wealth (Credit Suisse) | $463T |

| AM fee trend (EU) | down |

Same Document Delivered

Credit Agricole Porter's Five Forces Analysis

This preview displays the exact Credit Agricole Porter’s Five Forces Analysis you’ll receive upon purchase—no placeholders or samples. The full document is professionally formatted, ready for download and immediate use, and contains the complete strategic assessment, insights, and actionable conclusions included here.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Credit Agricole faces moderate rivalry from large domestic banks, rising digital challengers, strong regulatory constraints, concentrated supplier and funding power, and muted threat from substitutes. This Porter's Five Forces snapshot highlights where strategic pressure and opportunity intersect for the bank. Unlock the full analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or planning decisions.

Suppliers Bargaining Power

Diverse funding base limits single-source leverage

Crédit Agricole funds itself via retail deposits, covered bonds, senior debt and central bank facilities; retail deposits accounted for over 50% of funding in 2024, limiting dependence on any single supplier class. This diversification moderates pricing pressure from wholesale investors during market stress and reduces rollover risk. The cooperative regional bank structure further anchors stable retail funding and customer loyalty.

Stable cooperative deposits dampen rate pressure

Regional cooperative networks give Crédit Agricole sticky, low‑cost deposits—customer deposits exceeded €1 trillion in 2024—so members’ inertia and deep relationships limit supplier bargaining power. Depositors can press for higher rates, but cross‑selling of insurance and savings raises switching frictions, preserving margin stability versus market‑reliant peers.

Wholesale investors exert cyclical power

Bondholders and money markets can reprice funding within days in risk-off periods, with sector/issuer spreads widening and raising funding costs; European bank senior spreads moved hundreds of basis points in 2024 stress episodes. Credit Agricole’s strong CET1 ratio of 12.9% (end-2024) and transparent asset quality limit supplier leverage. Active liability management—smoothing maturities and rebalancing term vs. short-term funding—reduces repricing spikes.

Technology and cloud vendors hold moderate sway

Core banking, cybersecurity, data and cloud providers are concentrated—Gartner 2024 shows AWS 31.8%, Microsoft Azure 23.6% and Google Cloud 11.4% of the IaaS/PaaS market—so vendor stickiness is reinforced by high switching costs, integration complexity and regulatory constraints for banks like Crédit Agricole.

- Multi-vendor + in-house reduces dependency

- Scale enables stronger price and SLA negotiation

- Concentration: AWS 31.8%, Azure 23.6%, GCP 11.4%

Market infrastructures and schemes shape terms

Card networks, SWIFT/SEPA rails and central clearinghouses set mandatory fees and operating rules that materially shape Credit Agricole’s supplier bargaining: SWIFT connects 11,000+ institutions in 200+ countries, SEPA spans 36 European markets, and Visa/Mastercard account for over 70% of global card volume, giving infrastructures structural influence.

- Mandatory compliance raises switching costs

- Regulated governance caps fee hikes

- Network scale delivers offsetting benefits

Supplier power limited: deposits €1tn+, CET1 12.9%

Supplier power is limited: retail deposits >€1tn in 2024 and CET1 12.9% (end-2024) reduce reliance on volatile wholesale funding. Cloud and fintech vendors show concentration (AWS 31.8%, Azure 23.6%), raising switching costs but scale enables stronger negotiation. Card rails and SWIFT (11,000+ institutions) exert structural fees, but regulation caps unilateral fee hikes.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Deposits | €1trn+ | Low supplier power |

| Capital markets | CET1 12.9% | Lower repricing risk |

| Cloud | AWS 31.8% | High switching cost |

| Card/rails | Visa/MC >70% | Structural fees |

What is included in the product

Tailored Porter's Five Forces analysis for Crédit Agricole uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptive forces that could erode market share and profitability; includes strategic implications to reinforce its incumbent advantages and guide investor or management decisions.

One-sheet Porter’s Five Forces for Credit Agricole—clear, customizable pressure levels and an instant radar view that highlights competitive pain points for swift strategy decisions and board-ready slides.

Customers Bargaining Power

High price transparency intensifies client leverage

Digital comparison tools make rates and fees easily comparable, driving client leverage as corporate treasurers routinely run competitive RFPs across lenders; this transparency compresses margins in commoditized products such as mortgages and cash management, forcing banks to compete on price and service. Expanding relationship breadth across products is now essential to defend pricing and preserve share.

Multi-banking reduces dependence on a single bank

Large corporates and affluent clients increasingly multi-bank to spread counterparty risk and extract better pricing, with industry surveys in 2024 indicating majority adoption among top-tier firms; share-of-wallet is therefore contestable at each renewal. Crédit Agricole must win mandates product-by-product as clients split services across lenders. Bundled solutions and superior service quality remain key levers to retain primacy.

Switching costs vary by segment

Switching costs vary: everyday retail accounts face moderate frictions from payments, lending and insurance bundles, while SMEs and corporates incur higher integration costs for cash, FX and ERP links. Crédit Agricole, serving over 50 million customers in 2024, can leverage onboarding complexity to stabilize relationships, but accelerating open banking and API adoption in 2024 steadily lowers barriers.

Cooperative loyalty mitigates churn

Member-owners often value local presence and dividends from cooperative shares, with Groupe Crédit Agricole serving about 52 million customers in 2024, creating relational stickiness beyond pure pricing; community engagement and local branch networks strengthen trust and retention and partially offset digital-only challengers’ offers.

- Local branches + dividends = higher retention

- 2024: ~52M customers supporting relational loyalty

- Community engagement reduces churn vs digital challengers

Mass-affluent and institutional clients negotiate hard

Mass-affluent, asset management and CIB clients at Crédit Agricole demand bespoke pricing and negotiate hard; fee compression persisted in 2024 with industry AM fees trending lower and lending spreads remaining thin, while advisory and distribution reach help offset margin pressure. Performance track record and balance-sheet strength are decisive to retain wallet share amid competitive pricing and value-added service expectations.

- 2024 global wealth ~ $463 trillion (Credit Suisse Global Wealth Report 2024)

- AM fee compression notable across Europe in 2024

- Thin lending spreads raise importance of scale and capital

Rising customer bargaining power squeezes bank margins as open banking cuts switching costs

Customer bargaining power is high due to transparent digital rate comparisons and routine RFPs, compressing margins in mortgages and cash management. Large corporates and mass-affluent clients multi-bank, making share-of-wallet contestable despite Crédit Agricole’s ~52M customers in 2024. Open banking and API uptake steadily lower switching costs, raising pressure on price and service.

| Metric | 2024 |

|---|---|

| Crédit Agricole customers | ~52M |

| Global wealth (Credit Suisse) | $463T |

| AM fee trend (EU) | down |

Same Document Delivered

Credit Agricole Porter's Five Forces Analysis

This preview displays the exact Credit Agricole Porter’s Five Forces Analysis you’ll receive upon purchase—no placeholders or samples. The full document is professionally formatted, ready for download and immediate use, and contains the complete strategic assessment, insights, and actionable conclusions included here.