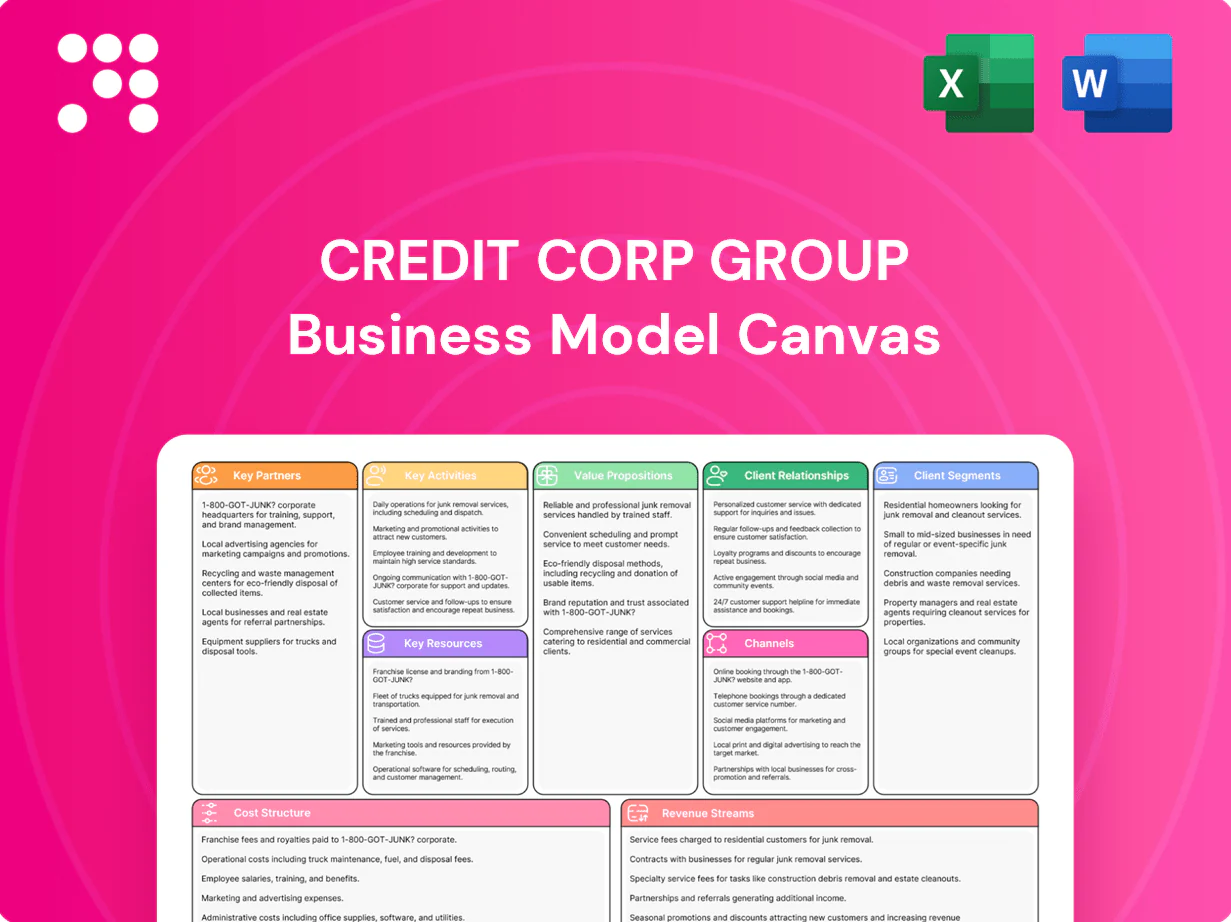

Credit Corp Group Business Model Canvas

Business Model Canvas: Strategic snapshot of a top credit recovery group

Unlock the strategic blueprint behind Credit Corp Group with our concise Business Model Canvas summary—covering customer segments, value propositions, key partners, and revenue streams. This snapshot reveals why the group outperforms peers and where growth opportunities lie. Download the full, editable Canvas for a section-by-section breakdown to use in benchmarking or investor decks. Purchase now to access Word and Excel versions.

Partnerships

Debt sellers

Relationships with banks, fintech lenders, telcos, utilities and retailers deliver a steady pipeline of charged-off and non-performing loan portfolios, often structured via multi-year (typically 3–5 year) forward flow agreements that secure volume and pricing visibility.

Credit bureaus & data providers

Credit bureaus and specialist data providers give Credit Corp access to bureau files, alternative data and skip-trace sources that improve contactability and allow finer segmentation. These partnerships feed pricing engines and propensity-to-pay models while strengthening fraud controls. Real-time enrichment raises right-party contact rates and speeds recoveries. Using compliance-aligned data reduces regulatory and compliance risk.

Legal & compliance partners

Specialist law firms, process servers and external counsel support Credit Corp Group’s litigation strategies, helping reduce cycle times and improve recovery outcomes; in FY2024 the group reported improved operational efficiencies alongside statutory NPAT of AUD 130.8m and revenue growth supporting continued legal spend.

Compliance advisors ensure collections and lending practices align with regulation, reducing regulatory risk and preserving brand reputation while balanced legal escalation maintains consumer fairness and mitigates complaint volumes and potential fines in 2024.

Technology vendors

Technology vendors—dialers, CRM/collections platforms, payment gateways and analytics—enable scalable collections for Credit Corp Group, which operates across Australia, New Zealand and the United States. Cloud infrastructure and security vendors provide resilience and data protection while API integrations streamline omnichannel engagement and straight-through payments. Vendor roadmaps drive continuous automation gains and operational efficiency.

Capital & funding partners

Banks, noteholders and warehouse lenders fund Credit Corp Group’s portfolio buys and consumer lending, with flexible facilities lowering weighted-average capital costs and expanding bidding capacity. Covenants and regular reporting frameworks enforce discipline and transparency across funding lines. Diversified funding sources reduce refinancing and liquidity risk while supporting growth.

- Banks

- Noteholders

- Warehouse lenders

- Flexible facilities

Forward-flow charged-off portfolios; FY2024 NPAT AUD 130.8m

Partnerships with banks, fintechs, telcos, utilities and retailers supply charged-off portfolios via multi-year (3–5yr) forward-flow deals, securing volume and pricing visibility.

Data vendors, credit bureaus and tech vendors (dialers, CRM, cloud, APIs) boost contactability, automation and compliance across Australia, NZ and US; FY2024 NPAT AUD 130.8m.

Banks, noteholders and warehouse lenders provide flexible funding, lowering WACC and expanding bidding capacity.

| Partner | Role | FY2024 metric |

|---|---|---|

| Banks/Noteholders | Funding | Supports portfolio buys; disciplined covenants |

What is included in the product

A comprehensive Business Model Canvas for Credit Corp Group mapping customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks to reflect real-world debt purchasing, collections and analytics operations. Ideal for presentations, investor discussions and strategic planning with linked SWOT and competitive advantage insights.

High-level view of Credit Corp Group’s business model with editable cells that clarify how debt purchasing, end-to-end collections and digital servicing relieve cash-flow shortages and operational inefficiencies for creditors and investors.

Activities

Portfolio sourcing & pricing

Identifying, evaluating and bidding on NPL portfolios via auctions and negotiated sales, Credit Corp deployed targeted buy strategies across Australia and the US, supporting FY2024 NPAT of AU$69.6m. Cashflow models use stratifications by vintage and behavioral cohorts to project recoveries and price portfolios. Target ROIs are set with scenario analysis and sensitivity testing, typically stress-testing recovery rates and discount margins. Due diligence and deal closing are streamlined to capture win-rate efficiencies.

Collections & recoveries

Running compliant, empathetic contact strategies across phone, SMS, email and portals, Credit Corp recorded managed receivables of over A$3.3bn in 2024 while maintaining regulatory and hardship frameworks. Frontline teams negotiate repayment plans, settlements and hardship arrangements, converting accounts through tailored offers. Segmentation and treatment paths drive sustainable recoveries, with cohort monitoring used to optimise contact intensity and timing to lift cure rates.

Consumer lending operations

Credit Corp Group originates near-prime consumer loans with responsible underwriting and affordability checks, refining scorecard-based pricing to align returns with credit risk. Servicing covers repayments, hardship support and arrears strategies to minimise loss and support performance. In FY2024 the business maintained transparent product design and clear disclosures to meet regulatory and consumer expectations.

Analytics & decisioning

Analytics & decisioning develops valuation, contact-prioritisation and payment-propensity models for Credit Corp Group (ASX: CCP). Champion–challenger testing refines strategies and scripts while forecasts of cash collections and provisioning are calibrated to AASB 9. Real-time dashboards deliver performance management across Australia, New Zealand, US, UK and the Philippines.

- Models: valuation, contact prioritisation, payment propensity

- Testing: champion–challenger for scripts and strategies

- Forecasting: cash collections and provisioning (AASB 9 aligned)

- Dashboards: real-time performance management

Risk, compliance & governance

Risk, compliance & governance frameworks at Credit Corp Group (ASX: CCP) are maintained to align with credit, collections, privacy and consumer protection laws across Australia and the United States (2024). Ongoing training, QA, call monitoring and structured complaint resolution support regulatory reporting and audit readiness. Third-party oversight and conduct risk management are integrated into vendor contracts and monitoring programs.

- ASX ticker: CCP

- Jurisdictions: Australia and United States (2024)

- Key controls: training, QA, call monitoring, complaints handling

- Focus: regulatory reporting, audit readiness, third-party oversight

Cross-jurisdictional NPL acquisition and near-prime lending drove AU$69.6m NPAT

Identifying and acquiring NPLs across AU/US with cashflow models and target ROIs supported FY2024 NPAT AU$69.6m. Managing receivables A$3.3bn via multichannel contact, hardship frameworks and segmentation. Originating near‑prime loans with responsible underwriting, AASB9 provisioning and analytics across AU, NZ, US, UK, PH.

| Metric | 2024 |

|---|---|

| NPAT | AU$69.6m |

| Managed receivables | A$3.3bn |

| Jurisdictions | AU, NZ, US, UK, PH |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Credit Corp Group Business Model Canvas—not a mockup—and it’s the same file you’ll receive after purchase. When you complete your order you’ll get the full, editable deliverable formatted exactly as shown, ready for analysis, presentation, or editing. No placeholders or omissions: what you see here is what you’ll download in full.

Business Model Canvas: Strategic snapshot of a top credit recovery group

Unlock the strategic blueprint behind Credit Corp Group with our concise Business Model Canvas summary—covering customer segments, value propositions, key partners, and revenue streams. This snapshot reveals why the group outperforms peers and where growth opportunities lie. Download the full, editable Canvas for a section-by-section breakdown to use in benchmarking or investor decks. Purchase now to access Word and Excel versions.

Partnerships

Debt sellers

Relationships with banks, fintech lenders, telcos, utilities and retailers deliver a steady pipeline of charged-off and non-performing loan portfolios, often structured via multi-year (typically 3–5 year) forward flow agreements that secure volume and pricing visibility.

Credit bureaus & data providers

Credit bureaus and specialist data providers give Credit Corp access to bureau files, alternative data and skip-trace sources that improve contactability and allow finer segmentation. These partnerships feed pricing engines and propensity-to-pay models while strengthening fraud controls. Real-time enrichment raises right-party contact rates and speeds recoveries. Using compliance-aligned data reduces regulatory and compliance risk.

Legal & compliance partners

Specialist law firms, process servers and external counsel support Credit Corp Group’s litigation strategies, helping reduce cycle times and improve recovery outcomes; in FY2024 the group reported improved operational efficiencies alongside statutory NPAT of AUD 130.8m and revenue growth supporting continued legal spend.

Compliance advisors ensure collections and lending practices align with regulation, reducing regulatory risk and preserving brand reputation while balanced legal escalation maintains consumer fairness and mitigates complaint volumes and potential fines in 2024.

Technology vendors

Technology vendors—dialers, CRM/collections platforms, payment gateways and analytics—enable scalable collections for Credit Corp Group, which operates across Australia, New Zealand and the United States. Cloud infrastructure and security vendors provide resilience and data protection while API integrations streamline omnichannel engagement and straight-through payments. Vendor roadmaps drive continuous automation gains and operational efficiency.

Capital & funding partners

Banks, noteholders and warehouse lenders fund Credit Corp Group’s portfolio buys and consumer lending, with flexible facilities lowering weighted-average capital costs and expanding bidding capacity. Covenants and regular reporting frameworks enforce discipline and transparency across funding lines. Diversified funding sources reduce refinancing and liquidity risk while supporting growth.

- Banks

- Noteholders

- Warehouse lenders

- Flexible facilities

Forward-flow charged-off portfolios; FY2024 NPAT AUD 130.8m

Partnerships with banks, fintechs, telcos, utilities and retailers supply charged-off portfolios via multi-year (3–5yr) forward-flow deals, securing volume and pricing visibility.

Data vendors, credit bureaus and tech vendors (dialers, CRM, cloud, APIs) boost contactability, automation and compliance across Australia, NZ and US; FY2024 NPAT AUD 130.8m.

Banks, noteholders and warehouse lenders provide flexible funding, lowering WACC and expanding bidding capacity.

| Partner | Role | FY2024 metric |

|---|---|---|

| Banks/Noteholders | Funding | Supports portfolio buys; disciplined covenants |

What is included in the product

A comprehensive Business Model Canvas for Credit Corp Group mapping customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks to reflect real-world debt purchasing, collections and analytics operations. Ideal for presentations, investor discussions and strategic planning with linked SWOT and competitive advantage insights.

High-level view of Credit Corp Group’s business model with editable cells that clarify how debt purchasing, end-to-end collections and digital servicing relieve cash-flow shortages and operational inefficiencies for creditors and investors.

Activities

Portfolio sourcing & pricing

Identifying, evaluating and bidding on NPL portfolios via auctions and negotiated sales, Credit Corp deployed targeted buy strategies across Australia and the US, supporting FY2024 NPAT of AU$69.6m. Cashflow models use stratifications by vintage and behavioral cohorts to project recoveries and price portfolios. Target ROIs are set with scenario analysis and sensitivity testing, typically stress-testing recovery rates and discount margins. Due diligence and deal closing are streamlined to capture win-rate efficiencies.

Collections & recoveries

Running compliant, empathetic contact strategies across phone, SMS, email and portals, Credit Corp recorded managed receivables of over A$3.3bn in 2024 while maintaining regulatory and hardship frameworks. Frontline teams negotiate repayment plans, settlements and hardship arrangements, converting accounts through tailored offers. Segmentation and treatment paths drive sustainable recoveries, with cohort monitoring used to optimise contact intensity and timing to lift cure rates.

Consumer lending operations

Credit Corp Group originates near-prime consumer loans with responsible underwriting and affordability checks, refining scorecard-based pricing to align returns with credit risk. Servicing covers repayments, hardship support and arrears strategies to minimise loss and support performance. In FY2024 the business maintained transparent product design and clear disclosures to meet regulatory and consumer expectations.

Analytics & decisioning

Analytics & decisioning develops valuation, contact-prioritisation and payment-propensity models for Credit Corp Group (ASX: CCP). Champion–challenger testing refines strategies and scripts while forecasts of cash collections and provisioning are calibrated to AASB 9. Real-time dashboards deliver performance management across Australia, New Zealand, US, UK and the Philippines.

- Models: valuation, contact prioritisation, payment propensity

- Testing: champion–challenger for scripts and strategies

- Forecasting: cash collections and provisioning (AASB 9 aligned)

- Dashboards: real-time performance management

Risk, compliance & governance

Risk, compliance & governance frameworks at Credit Corp Group (ASX: CCP) are maintained to align with credit, collections, privacy and consumer protection laws across Australia and the United States (2024). Ongoing training, QA, call monitoring and structured complaint resolution support regulatory reporting and audit readiness. Third-party oversight and conduct risk management are integrated into vendor contracts and monitoring programs.

- ASX ticker: CCP

- Jurisdictions: Australia and United States (2024)

- Key controls: training, QA, call monitoring, complaints handling

- Focus: regulatory reporting, audit readiness, third-party oversight

Cross-jurisdictional NPL acquisition and near-prime lending drove AU$69.6m NPAT

Identifying and acquiring NPLs across AU/US with cashflow models and target ROIs supported FY2024 NPAT AU$69.6m. Managing receivables A$3.3bn via multichannel contact, hardship frameworks and segmentation. Originating near‑prime loans with responsible underwriting, AASB9 provisioning and analytics across AU, NZ, US, UK, PH.

| Metric | 2024 |

|---|---|

| NPAT | AU$69.6m |

| Managed receivables | A$3.3bn |

| Jurisdictions | AU, NZ, US, UK, PH |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Credit Corp Group Business Model Canvas—not a mockup—and it’s the same file you’ll receive after purchase. When you complete your order you’ll get the full, editable deliverable formatted exactly as shown, ready for analysis, presentation, or editing. No placeholders or omissions: what you see here is what you’ll download in full.

Description

Business Model Canvas: Strategic snapshot of a top credit recovery group

Unlock the strategic blueprint behind Credit Corp Group with our concise Business Model Canvas summary—covering customer segments, value propositions, key partners, and revenue streams. This snapshot reveals why the group outperforms peers and where growth opportunities lie. Download the full, editable Canvas for a section-by-section breakdown to use in benchmarking or investor decks. Purchase now to access Word and Excel versions.

Partnerships

Debt sellers

Relationships with banks, fintech lenders, telcos, utilities and retailers deliver a steady pipeline of charged-off and non-performing loan portfolios, often structured via multi-year (typically 3–5 year) forward flow agreements that secure volume and pricing visibility.

Credit bureaus & data providers

Credit bureaus and specialist data providers give Credit Corp access to bureau files, alternative data and skip-trace sources that improve contactability and allow finer segmentation. These partnerships feed pricing engines and propensity-to-pay models while strengthening fraud controls. Real-time enrichment raises right-party contact rates and speeds recoveries. Using compliance-aligned data reduces regulatory and compliance risk.

Legal & compliance partners

Specialist law firms, process servers and external counsel support Credit Corp Group’s litigation strategies, helping reduce cycle times and improve recovery outcomes; in FY2024 the group reported improved operational efficiencies alongside statutory NPAT of AUD 130.8m and revenue growth supporting continued legal spend.

Compliance advisors ensure collections and lending practices align with regulation, reducing regulatory risk and preserving brand reputation while balanced legal escalation maintains consumer fairness and mitigates complaint volumes and potential fines in 2024.

Technology vendors

Technology vendors—dialers, CRM/collections platforms, payment gateways and analytics—enable scalable collections for Credit Corp Group, which operates across Australia, New Zealand and the United States. Cloud infrastructure and security vendors provide resilience and data protection while API integrations streamline omnichannel engagement and straight-through payments. Vendor roadmaps drive continuous automation gains and operational efficiency.

Capital & funding partners

Banks, noteholders and warehouse lenders fund Credit Corp Group’s portfolio buys and consumer lending, with flexible facilities lowering weighted-average capital costs and expanding bidding capacity. Covenants and regular reporting frameworks enforce discipline and transparency across funding lines. Diversified funding sources reduce refinancing and liquidity risk while supporting growth.

- Banks

- Noteholders

- Warehouse lenders

- Flexible facilities

Forward-flow charged-off portfolios; FY2024 NPAT AUD 130.8m

Partnerships with banks, fintechs, telcos, utilities and retailers supply charged-off portfolios via multi-year (3–5yr) forward-flow deals, securing volume and pricing visibility.

Data vendors, credit bureaus and tech vendors (dialers, CRM, cloud, APIs) boost contactability, automation and compliance across Australia, NZ and US; FY2024 NPAT AUD 130.8m.

Banks, noteholders and warehouse lenders provide flexible funding, lowering WACC and expanding bidding capacity.

| Partner | Role | FY2024 metric |

|---|---|---|

| Banks/Noteholders | Funding | Supports portfolio buys; disciplined covenants |

What is included in the product

A comprehensive Business Model Canvas for Credit Corp Group mapping customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks to reflect real-world debt purchasing, collections and analytics operations. Ideal for presentations, investor discussions and strategic planning with linked SWOT and competitive advantage insights.

High-level view of Credit Corp Group’s business model with editable cells that clarify how debt purchasing, end-to-end collections and digital servicing relieve cash-flow shortages and operational inefficiencies for creditors and investors.

Activities

Portfolio sourcing & pricing

Identifying, evaluating and bidding on NPL portfolios via auctions and negotiated sales, Credit Corp deployed targeted buy strategies across Australia and the US, supporting FY2024 NPAT of AU$69.6m. Cashflow models use stratifications by vintage and behavioral cohorts to project recoveries and price portfolios. Target ROIs are set with scenario analysis and sensitivity testing, typically stress-testing recovery rates and discount margins. Due diligence and deal closing are streamlined to capture win-rate efficiencies.

Collections & recoveries

Running compliant, empathetic contact strategies across phone, SMS, email and portals, Credit Corp recorded managed receivables of over A$3.3bn in 2024 while maintaining regulatory and hardship frameworks. Frontline teams negotiate repayment plans, settlements and hardship arrangements, converting accounts through tailored offers. Segmentation and treatment paths drive sustainable recoveries, with cohort monitoring used to optimise contact intensity and timing to lift cure rates.

Consumer lending operations

Credit Corp Group originates near-prime consumer loans with responsible underwriting and affordability checks, refining scorecard-based pricing to align returns with credit risk. Servicing covers repayments, hardship support and arrears strategies to minimise loss and support performance. In FY2024 the business maintained transparent product design and clear disclosures to meet regulatory and consumer expectations.

Analytics & decisioning

Analytics & decisioning develops valuation, contact-prioritisation and payment-propensity models for Credit Corp Group (ASX: CCP). Champion–challenger testing refines strategies and scripts while forecasts of cash collections and provisioning are calibrated to AASB 9. Real-time dashboards deliver performance management across Australia, New Zealand, US, UK and the Philippines.

- Models: valuation, contact prioritisation, payment propensity

- Testing: champion–challenger for scripts and strategies

- Forecasting: cash collections and provisioning (AASB 9 aligned)

- Dashboards: real-time performance management

Risk, compliance & governance

Risk, compliance & governance frameworks at Credit Corp Group (ASX: CCP) are maintained to align with credit, collections, privacy and consumer protection laws across Australia and the United States (2024). Ongoing training, QA, call monitoring and structured complaint resolution support regulatory reporting and audit readiness. Third-party oversight and conduct risk management are integrated into vendor contracts and monitoring programs.

- ASX ticker: CCP

- Jurisdictions: Australia and United States (2024)

- Key controls: training, QA, call monitoring, complaints handling

- Focus: regulatory reporting, audit readiness, third-party oversight

Cross-jurisdictional NPL acquisition and near-prime lending drove AU$69.6m NPAT

Identifying and acquiring NPLs across AU/US with cashflow models and target ROIs supported FY2024 NPAT AU$69.6m. Managing receivables A$3.3bn via multichannel contact, hardship frameworks and segmentation. Originating near‑prime loans with responsible underwriting, AASB9 provisioning and analytics across AU, NZ, US, UK, PH.

| Metric | 2024 |

|---|---|

| NPAT | AU$69.6m |

| Managed receivables | A$3.3bn |

| Jurisdictions | AU, NZ, US, UK, PH |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Credit Corp Group Business Model Canvas—not a mockup—and it’s the same file you’ll receive after purchase. When you complete your order you’ll get the full, editable deliverable formatted exactly as shown, ready for analysis, presentation, or editing. No placeholders or omissions: what you see here is what you’ll download in full.