Credit Corp Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Credit Corp Group faces evolving buyer and regulatory pressures, rising fintech competition, and moderate supplier leverage—factors that shape profitability and strategic options; this snapshot highlights key tensions but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis for detailed scoring, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated creditor sellers

Major portfolio supply to Credit Corp Group is concentrated among a small number of banks, telcos and utilities, with Australia’s Big Four banks holding roughly 80% of domestic banking assets (APRA 2024), concentrating negotiating power with sellers.

These institutions run competitive auctions and impose strict eligibility and conduct terms, while preferred-supplier lists restrict access and heighten dependence on relationship quality.

The concentration enables sellers to demand higher prices and tighter reps and warranties, compressing buyer margins and increasing execution risk.

Auction-driven portfolio pricing

Portfolios are sold mainly via sealed-bid or brokered auctions, which concentrates supplier leverage and gives sellers control over timing and format. Competitive tension among buyers in these auctions compresses expected returns and transfers portfolio performance risk to purchasers. Limited transparency on account quality forces bidders to adopt conservative discounting, while sellers can time disposals to favorable credit-cycle windows to maximize proceeds.

Regulatory and contractual constraints

Suppliers impose robust compliance, data and consumer-treatment obligations that shift legal and operational risk onto Credit Corp via breach liabilities and repurchase clauses, tightening buyer leverage. Data minimization and privacy rules limit collection strategies and increase integration costs; the IBM Cost of a Data Breach Report 2024 cites a $4.45m average breach cost, raising operational expense and compressing negotiating room.

Funding and cost-of-capital dependency

Access to debt and equity is pivotal for Credit Corp’s bid aggressiveness; with the RBA cash rate around 4.35% in 2024 and corporate borrowing costs up roughly 200–300 basis points since 2021, required returns have risen and can price marginal buyers out, strengthening seller power.

- Committed capital and quick close increase supplier preference

- Higher rates raise hurdle rates and reduce bid capacity

- Funding covenants can ban certain portfolio types, narrowing options

Data and tech vendor reliance

Credit Corp Group's recoveries in FY24 remain heavily dependent on third-party data, dialers, analytics and servicing platforms; switching costs are moderate but integration and compliance testing create meaningful implementation friction. Vendors can pass on price rises or restrict features for risk/compliance reasons, while outages or model drift directly erode bid confidence and recoveries.

- Vendor concentration: operational risk

- Integration/compliance: moderate switching cost

- Outages/model drift: direct recovery impact

Concentrated banks ~80%, higher rates 4.35% and cyber costs compress margins

Supplier concentration is high: Australia’s Big Four hold ~80% of banking assets (APRA 2024), giving sellers pricing and timing control. Auctions and strict reps shift execution and legal risk to Credit Corp; IBM reports average data breach cost $4.45m (2024). RBA cash rate ~4.35% (2024) lifts funding costs and raises bid hurdles, compressing margins.

| Metric | 2024 Value |

|---|---|

| Big Four share of banking assets | ~80% (APRA) |

| RBA cash rate | ~4.35% |

| Avg data breach cost | $4.45m (IBM) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Credit Corp Group, detailing supplier and buyer power, substitute threats, and intensity of rivalry. Identifies disruptive forces and barriers protecting incumbents, providing strategic insights for investors, advisors, and management.

A concise Porter's Five Forces snapshot for Credit Corp Group that highlights competitive pressures, customer bargaining power and regulatory risks—ready to drop into decks for faster, boardroom-ready decision-making.

Customers Bargaining Power

Debtors’ ability to delay or dispute

Individual consumers have limited monetary leverage but frequently delay through disputes and hardship claims, with AFCA recording over 100,000 complaints in 2023–24, increasing resolution timelines.

Time-value erosion and legal/collection costs create bargaining room for discounts and extended payment plans, compressing recoverable value.

Ombudsman rulings and strengthened consumer law in 2024 raise debtor protections and dispute success rates.

Aggregated, these factors flatten settlement curves and force higher provisioning and adjusted pricing for Credit Corp Group.

Regulatory protection and hardship

Regulatory protection — hardship rules, vulnerability safeguards and responsible collection codes force Credit Corp Group to offer flexible payment plans and cap effective collection yields, reducing pricing leverage; AFCA registered over 100,000 financial disputes in 2023–24, increasing scrutiny and redress risk; expanded complaints channels strengthen consumers practical bargaining position and constrain aggressive collection tactics.

Alternative payment and credit options

Consumers can refinance, consolidate or use BNPL/payday options to settle or avoid collection, with global BNPL gross merchandise value reaching about US$170bn in 2024, increasing settlement elasticity for Credit Corp Group’s clients. In tighter credit conditions (2024 rate volatility), alternative availability shrinks and customer bargaining power falls. Cross-sell in consumer finance remains highly price sensitive, compressing margins.

Information transparency

Information transparency — driven by easy access to credit reports, debt validation tools and published settlement benchmarks — has increased debtor negotiating confidence; a 2024 consumer study found about 60% of delinquent accounts research options before settlement. Digital outreach and education on rights raise expectations for larger discounts, forcing Credit Corp to use data-driven, segmented offers to close more settlements.

- Access to reports: raises debtor leverage

- Debt validation: reduces disputes, sharpens expectations

- Settlement benchmarks: push higher discount demands

- Response: targeted, data-led offers to protect recovery rates

Low switching costs in consumer finance

For new loans customers can shop online and switch providers easily; in 2024 Finder reported 69% of Australians used comparison sites for financial products. Rate comparison tools heighten price competition and squeeze margins in adjacent lending products. Brand trust and UX aid retention but are replicable, keeping Credit Corp Group margins under pressure.

- Low switching costs

- Comparison-driven pricing

- Replicable brand/UX

Rising AFCA disputes and BNPL growth force deeper settlements and longer recovery timelines

Debtor protections and 100,000+ AFCA complaints (2023–24) raise dispute success and extend resolution timelines, compressing recoverable value. Time erosion, legal costs and 60% of debtors researching options (2024) boost discount demands. BNPL GMV ~US$170bn (2024) and 69% comparison-site use (Finder 2024) increase settlement elasticity and pressure margins.

| Metric | Value (2024) |

|---|---|

| AFCA complaints | 100,000+ |

| Debtors researching | 60% |

| BNPL GMV | US$170bn |

| Comparison use (AU) | 69% |

Preview the Actual Deliverable

Credit Corp Group Porter's Five Forces Analysis

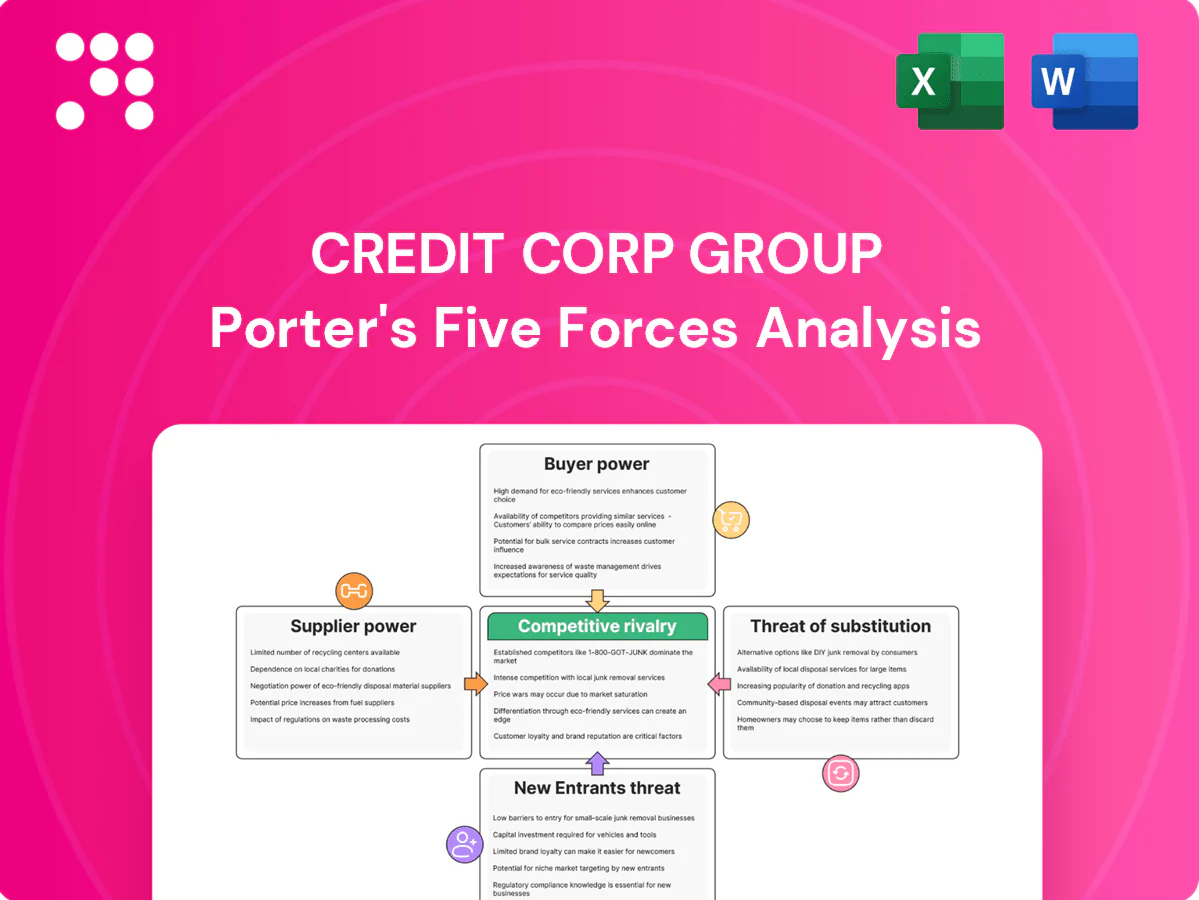

This preview shows the exact Credit Corp Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document presents supplier, buyer, rivalry, threat of new entrants, and substitutes analysis with clear implications for strategy. It's fully formatted and ready for immediate use.

From Overview to Strategy Blueprint

Credit Corp Group faces evolving buyer and regulatory pressures, rising fintech competition, and moderate supplier leverage—factors that shape profitability and strategic options; this snapshot highlights key tensions but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis for detailed scoring, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated creditor sellers

Major portfolio supply to Credit Corp Group is concentrated among a small number of banks, telcos and utilities, with Australia’s Big Four banks holding roughly 80% of domestic banking assets (APRA 2024), concentrating negotiating power with sellers.

These institutions run competitive auctions and impose strict eligibility and conduct terms, while preferred-supplier lists restrict access and heighten dependence on relationship quality.

The concentration enables sellers to demand higher prices and tighter reps and warranties, compressing buyer margins and increasing execution risk.

Auction-driven portfolio pricing

Portfolios are sold mainly via sealed-bid or brokered auctions, which concentrates supplier leverage and gives sellers control over timing and format. Competitive tension among buyers in these auctions compresses expected returns and transfers portfolio performance risk to purchasers. Limited transparency on account quality forces bidders to adopt conservative discounting, while sellers can time disposals to favorable credit-cycle windows to maximize proceeds.

Regulatory and contractual constraints

Suppliers impose robust compliance, data and consumer-treatment obligations that shift legal and operational risk onto Credit Corp via breach liabilities and repurchase clauses, tightening buyer leverage. Data minimization and privacy rules limit collection strategies and increase integration costs; the IBM Cost of a Data Breach Report 2024 cites a $4.45m average breach cost, raising operational expense and compressing negotiating room.

Funding and cost-of-capital dependency

Access to debt and equity is pivotal for Credit Corp’s bid aggressiveness; with the RBA cash rate around 4.35% in 2024 and corporate borrowing costs up roughly 200–300 basis points since 2021, required returns have risen and can price marginal buyers out, strengthening seller power.

- Committed capital and quick close increase supplier preference

- Higher rates raise hurdle rates and reduce bid capacity

- Funding covenants can ban certain portfolio types, narrowing options

Data and tech vendor reliance

Credit Corp Group's recoveries in FY24 remain heavily dependent on third-party data, dialers, analytics and servicing platforms; switching costs are moderate but integration and compliance testing create meaningful implementation friction. Vendors can pass on price rises or restrict features for risk/compliance reasons, while outages or model drift directly erode bid confidence and recoveries.

- Vendor concentration: operational risk

- Integration/compliance: moderate switching cost

- Outages/model drift: direct recovery impact

Concentrated banks ~80%, higher rates 4.35% and cyber costs compress margins

Supplier concentration is high: Australia’s Big Four hold ~80% of banking assets (APRA 2024), giving sellers pricing and timing control. Auctions and strict reps shift execution and legal risk to Credit Corp; IBM reports average data breach cost $4.45m (2024). RBA cash rate ~4.35% (2024) lifts funding costs and raises bid hurdles, compressing margins.

| Metric | 2024 Value |

|---|---|

| Big Four share of banking assets | ~80% (APRA) |

| RBA cash rate | ~4.35% |

| Avg data breach cost | $4.45m (IBM) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Credit Corp Group, detailing supplier and buyer power, substitute threats, and intensity of rivalry. Identifies disruptive forces and barriers protecting incumbents, providing strategic insights for investors, advisors, and management.

A concise Porter's Five Forces snapshot for Credit Corp Group that highlights competitive pressures, customer bargaining power and regulatory risks—ready to drop into decks for faster, boardroom-ready decision-making.

Customers Bargaining Power

Debtors’ ability to delay or dispute

Individual consumers have limited monetary leverage but frequently delay through disputes and hardship claims, with AFCA recording over 100,000 complaints in 2023–24, increasing resolution timelines.

Time-value erosion and legal/collection costs create bargaining room for discounts and extended payment plans, compressing recoverable value.

Ombudsman rulings and strengthened consumer law in 2024 raise debtor protections and dispute success rates.

Aggregated, these factors flatten settlement curves and force higher provisioning and adjusted pricing for Credit Corp Group.

Regulatory protection and hardship

Regulatory protection — hardship rules, vulnerability safeguards and responsible collection codes force Credit Corp Group to offer flexible payment plans and cap effective collection yields, reducing pricing leverage; AFCA registered over 100,000 financial disputes in 2023–24, increasing scrutiny and redress risk; expanded complaints channels strengthen consumers practical bargaining position and constrain aggressive collection tactics.

Alternative payment and credit options

Consumers can refinance, consolidate or use BNPL/payday options to settle or avoid collection, with global BNPL gross merchandise value reaching about US$170bn in 2024, increasing settlement elasticity for Credit Corp Group’s clients. In tighter credit conditions (2024 rate volatility), alternative availability shrinks and customer bargaining power falls. Cross-sell in consumer finance remains highly price sensitive, compressing margins.

Information transparency

Information transparency — driven by easy access to credit reports, debt validation tools and published settlement benchmarks — has increased debtor negotiating confidence; a 2024 consumer study found about 60% of delinquent accounts research options before settlement. Digital outreach and education on rights raise expectations for larger discounts, forcing Credit Corp to use data-driven, segmented offers to close more settlements.

- Access to reports: raises debtor leverage

- Debt validation: reduces disputes, sharpens expectations

- Settlement benchmarks: push higher discount demands

- Response: targeted, data-led offers to protect recovery rates

Low switching costs in consumer finance

For new loans customers can shop online and switch providers easily; in 2024 Finder reported 69% of Australians used comparison sites for financial products. Rate comparison tools heighten price competition and squeeze margins in adjacent lending products. Brand trust and UX aid retention but are replicable, keeping Credit Corp Group margins under pressure.

- Low switching costs

- Comparison-driven pricing

- Replicable brand/UX

Rising AFCA disputes and BNPL growth force deeper settlements and longer recovery timelines

Debtor protections and 100,000+ AFCA complaints (2023–24) raise dispute success and extend resolution timelines, compressing recoverable value. Time erosion, legal costs and 60% of debtors researching options (2024) boost discount demands. BNPL GMV ~US$170bn (2024) and 69% comparison-site use (Finder 2024) increase settlement elasticity and pressure margins.

| Metric | Value (2024) |

|---|---|

| AFCA complaints | 100,000+ |

| Debtors researching | 60% |

| BNPL GMV | US$170bn |

| Comparison use (AU) | 69% |

Preview the Actual Deliverable

Credit Corp Group Porter's Five Forces Analysis

This preview shows the exact Credit Corp Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document presents supplier, buyer, rivalry, threat of new entrants, and substitutes analysis with clear implications for strategy. It's fully formatted and ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Credit Corp Group faces evolving buyer and regulatory pressures, rising fintech competition, and moderate supplier leverage—factors that shape profitability and strategic options; this snapshot highlights key tensions but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis for detailed scoring, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated creditor sellers

Major portfolio supply to Credit Corp Group is concentrated among a small number of banks, telcos and utilities, with Australia’s Big Four banks holding roughly 80% of domestic banking assets (APRA 2024), concentrating negotiating power with sellers.

These institutions run competitive auctions and impose strict eligibility and conduct terms, while preferred-supplier lists restrict access and heighten dependence on relationship quality.

The concentration enables sellers to demand higher prices and tighter reps and warranties, compressing buyer margins and increasing execution risk.

Auction-driven portfolio pricing

Portfolios are sold mainly via sealed-bid or brokered auctions, which concentrates supplier leverage and gives sellers control over timing and format. Competitive tension among buyers in these auctions compresses expected returns and transfers portfolio performance risk to purchasers. Limited transparency on account quality forces bidders to adopt conservative discounting, while sellers can time disposals to favorable credit-cycle windows to maximize proceeds.

Regulatory and contractual constraints

Suppliers impose robust compliance, data and consumer-treatment obligations that shift legal and operational risk onto Credit Corp via breach liabilities and repurchase clauses, tightening buyer leverage. Data minimization and privacy rules limit collection strategies and increase integration costs; the IBM Cost of a Data Breach Report 2024 cites a $4.45m average breach cost, raising operational expense and compressing negotiating room.

Funding and cost-of-capital dependency

Access to debt and equity is pivotal for Credit Corp’s bid aggressiveness; with the RBA cash rate around 4.35% in 2024 and corporate borrowing costs up roughly 200–300 basis points since 2021, required returns have risen and can price marginal buyers out, strengthening seller power.

- Committed capital and quick close increase supplier preference

- Higher rates raise hurdle rates and reduce bid capacity

- Funding covenants can ban certain portfolio types, narrowing options

Data and tech vendor reliance

Credit Corp Group's recoveries in FY24 remain heavily dependent on third-party data, dialers, analytics and servicing platforms; switching costs are moderate but integration and compliance testing create meaningful implementation friction. Vendors can pass on price rises or restrict features for risk/compliance reasons, while outages or model drift directly erode bid confidence and recoveries.

- Vendor concentration: operational risk

- Integration/compliance: moderate switching cost

- Outages/model drift: direct recovery impact

Concentrated banks ~80%, higher rates 4.35% and cyber costs compress margins

Supplier concentration is high: Australia’s Big Four hold ~80% of banking assets (APRA 2024), giving sellers pricing and timing control. Auctions and strict reps shift execution and legal risk to Credit Corp; IBM reports average data breach cost $4.45m (2024). RBA cash rate ~4.35% (2024) lifts funding costs and raises bid hurdles, compressing margins.

| Metric | 2024 Value |

|---|---|

| Big Four share of banking assets | ~80% (APRA) |

| RBA cash rate | ~4.35% |

| Avg data breach cost | $4.45m (IBM) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Credit Corp Group, detailing supplier and buyer power, substitute threats, and intensity of rivalry. Identifies disruptive forces and barriers protecting incumbents, providing strategic insights for investors, advisors, and management.

A concise Porter's Five Forces snapshot for Credit Corp Group that highlights competitive pressures, customer bargaining power and regulatory risks—ready to drop into decks for faster, boardroom-ready decision-making.

Customers Bargaining Power

Debtors’ ability to delay or dispute

Individual consumers have limited monetary leverage but frequently delay through disputes and hardship claims, with AFCA recording over 100,000 complaints in 2023–24, increasing resolution timelines.

Time-value erosion and legal/collection costs create bargaining room for discounts and extended payment plans, compressing recoverable value.

Ombudsman rulings and strengthened consumer law in 2024 raise debtor protections and dispute success rates.

Aggregated, these factors flatten settlement curves and force higher provisioning and adjusted pricing for Credit Corp Group.

Regulatory protection and hardship

Regulatory protection — hardship rules, vulnerability safeguards and responsible collection codes force Credit Corp Group to offer flexible payment plans and cap effective collection yields, reducing pricing leverage; AFCA registered over 100,000 financial disputes in 2023–24, increasing scrutiny and redress risk; expanded complaints channels strengthen consumers practical bargaining position and constrain aggressive collection tactics.

Alternative payment and credit options

Consumers can refinance, consolidate or use BNPL/payday options to settle or avoid collection, with global BNPL gross merchandise value reaching about US$170bn in 2024, increasing settlement elasticity for Credit Corp Group’s clients. In tighter credit conditions (2024 rate volatility), alternative availability shrinks and customer bargaining power falls. Cross-sell in consumer finance remains highly price sensitive, compressing margins.

Information transparency

Information transparency — driven by easy access to credit reports, debt validation tools and published settlement benchmarks — has increased debtor negotiating confidence; a 2024 consumer study found about 60% of delinquent accounts research options before settlement. Digital outreach and education on rights raise expectations for larger discounts, forcing Credit Corp to use data-driven, segmented offers to close more settlements.

- Access to reports: raises debtor leverage

- Debt validation: reduces disputes, sharpens expectations

- Settlement benchmarks: push higher discount demands

- Response: targeted, data-led offers to protect recovery rates

Low switching costs in consumer finance

For new loans customers can shop online and switch providers easily; in 2024 Finder reported 69% of Australians used comparison sites for financial products. Rate comparison tools heighten price competition and squeeze margins in adjacent lending products. Brand trust and UX aid retention but are replicable, keeping Credit Corp Group margins under pressure.

- Low switching costs

- Comparison-driven pricing

- Replicable brand/UX

Rising AFCA disputes and BNPL growth force deeper settlements and longer recovery timelines

Debtor protections and 100,000+ AFCA complaints (2023–24) raise dispute success and extend resolution timelines, compressing recoverable value. Time erosion, legal costs and 60% of debtors researching options (2024) boost discount demands. BNPL GMV ~US$170bn (2024) and 69% comparison-site use (Finder 2024) increase settlement elasticity and pressure margins.

| Metric | Value (2024) |

|---|---|

| AFCA complaints | 100,000+ |

| Debtors researching | 60% |

| BNPL GMV | US$170bn |

| Comparison use (AU) | 69% |

Preview the Actual Deliverable

Credit Corp Group Porter's Five Forces Analysis

This preview shows the exact Credit Corp Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document presents supplier, buyer, rivalry, threat of new entrants, and substitutes analysis with clear implications for strategy. It's fully formatted and ready for immediate use.