CRH Porter's Five Forces Analysis

Don't Miss the Bigger Picture

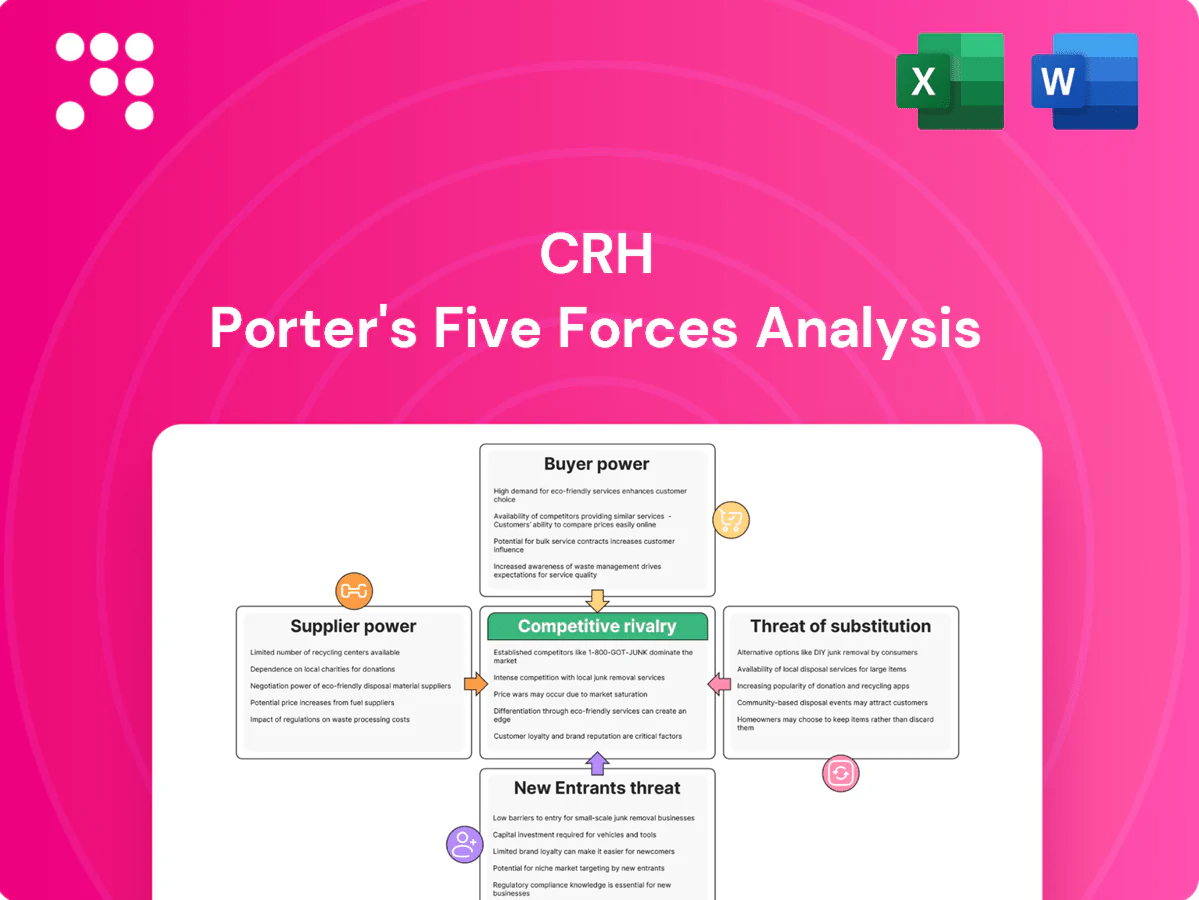

CRH’s Porter's Five Forces snapshot highlights concentrated buyer power, moderate supplier influence, high competitive rivalry, limited substitutes, and barriers that temper new entrants. This brief shows core pressures but skips the force-by-force ratings, visuals and strategic implications. Unlock the full Porter’s Five Forces Analysis to access data-driven insights, actionable recommendations, and presentation-ready Excel/Word deliverables for investment or strategy decisions.

Suppliers Bargaining Power

Input diversification limits leverage

CRH sources energy, raw materials and additives from multiple vendors across c.28 countries, diluting single-supplier influence and enabling local substitution. Its vertical integration in aggregates and cement cuts external exposure, while decentralized procurement allows rapid supplier swaps. Scale purchasing across its global footprint secures volume discounts and stronger contract terms.

Energy and fuel volatility

Power, petcoke and gas suppliers gain leverage during spikes or scarcity, as energy can account for up to 40% of cement production costs; regional fuel price swings in 2022–24 saw occasional doubling in spot gas/petcoke costs. CRH mitigates exposure through hedging programs and rising alternative fuel use, and its shift to long-term energy supply frameworks in 2024 aims to stabilize input pricing.

Logistics and transport constraints

Haulage capacity and limited rail access concentrate supplier power in tight markets, with road freight carrying about 70–80% of aggregates deliveries and typical localized delivery windows of 2–4 hours restricting switching. CRH’s owned fleets and regional carriers, supported by a workforce of roughly 86,000 (2024), help reduce bottlenecks and improve resilience. Proximity of quarries and plants, often within 20–40 km of sites, lowers freight dependency and supplier leverage.

Specialty additives and equipment

Admixtures, spare parts and kiln components are concentrated among specialized suppliers—top global players in 2024 remain BASF, Sika and GCP—creating technical lock-in and pockets of bargaining power for CRH. Multiyear service agreements (commonly 3–5 years) trade reduced unit pricing for guaranteed uptime. Dual-sourcing and growing in-house technical teams limit supplier leverage and disruption risk.

- Supplier concentration: top players dominate

- Service terms: 3–5 years

- Mitigants: dual-source, in-house expertise

Permits and mineral rights

Landowners and permit holders strongly influence access to aggregates and raw feed, with scarce high-quality reserves increasing supplier leverage; CRH reports over 3,500 locations across 30+ countries, which mitigates single-site dependency. CRH’s long-dated permits and sizable reserve footprint reduce short-term exposure, while an active permitting pipeline preserves supply optionality and bargaining flexibility.

- Supplier influence: high where premium reserves are scarce

- CRH scale: over 3,500 locations across 30+ countries

- Risk mitigation: long-dated permits and reserve base

- Ongoing permits: sustain supply optionality

3,500+ sites, ~40% energy, strong freight leverage

CRH limits supplier power via vertical integration, 3,500+ sites across 30+ countries (2024) and scale purchasing; energy can be ~40% of cement costs so 2024 hedging and long-term energy deals reduce volatility. Road freight carries ~70–80% of aggregates, giving local haulage leverage mitigated by owned fleets; specialized admixture suppliers (BASF, Sika, GCP) keep pockets of technical supplier power.

| Metric | 2024 |

|---|---|

| Sites | 3,500+ |

| Workforce | 86,000 |

| Energy share | ~40% |

| Road freight | 70–80% |

| Key suppliers | BASF, Sika, GCP |

What is included in the product

Tailored Porter’s Five Forces analysis for CRH uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and critical disruptive forces—providing data-backed insight on pricing influence, market entry risks, and strategic levers to protect or grow CRH’s market position.

A concise one-sheet Porter's Five Forces for CRH that quantifies supplier, buyer, entrant, substitute and rivalry pressures—ideal for fast strategic decisions and slide-ready summaries. Customize pressure levels or swap in your own data to reflect changing markets and regulatory shifts.

Customers Bargaining Power

Large contractors and DOTs

National contractors and DOTs buy at scale and drive price pressure via competitive tendering; CRH reported full-year 2024 revenue of €26.7bn, reflecting exposure to large public contracts. These buyers demand tight specs, reliability and on-time delivery, shifting penalties and risk onto suppliers. CRH leverages integrated asphalt, aggregates and concrete offerings and long-term framework agreements that trade committed volume for pricing stability.

Project-based bidding

Construction is bid-driven, with buyers routinely comparing suppliers across projects; local aggregates markets typically constrain viable alternatives to providers within roughly 50–100 km. Switching costs are moderate, largely logistical and spec-related, so buyers rebid frequently. Strong QA/QC and performance history can justify modest premiums of around 3–7% on unit pricing.

Spec and standards stickiness

DOT and engineering specifications create approved-material lists for IIJA-funded projects (the 2021 Infrastructure Investment and Jobs Act authorized $1.2 trillion), making supplier qualification a gateway to repeat business and less price-only competition. CRH leverages certifications and consistent quality to reduce churn, while technical support teams embed CRH early in project design to lock in specs and long-term supply relationships.

Sustainability requirements

Buyers increasingly demand EPDs, recycled content and low-carbon mixes, driven by ESG mandates that push for greener options at comparable cost; cement and concrete account for about 7% of global CO2 emissions, raising procurement scrutiny. CRH’s decarbonization roadmap and alternative binders create differentiation, tempering pure price bargaining and enabling value-based sales.

- EPDs & low‑carbon mixes demanded; sector ≈7% of CO2

Local market fragmentation

Local market fragmentation leaves many small and mid-sized buyers with limited leverage, and proximity economics often constrain supplier choice; in 2024 CRH reported group revenue of €32.5bn and c.3,000 local operations which underpin delivery density. Service reliability and credit terms carry heavy weight for buyers and raise switching costs. High local reach helps CRH sustain price realization across fragmented markets.

- 2024 revenue: €32.5bn

- Local operations: ≈3,000 sites

- Delivery density increases switching friction

Tender-driven price pressure from large contractors; local network (~3,000) and ESG shift buying

Large national contractors and DOTs exert strong price pressure via tendering; CRH reported 2024 revenue €32.5bn, exposing it to big public contracts. Switching costs are moderate and local proximity limits alternatives, with c.3,000 sites boosting delivery density. ESG specs (cement ≈7% of CO2) raise value-based buying, reducing pure price bargaining.

| Metric | 2024 |

|---|---|

| Revenue | €32.5bn |

| Local sites | ≈3,000 |

| Cement CO2 share | ≈7% |

Full Version Awaits

CRH Porter's Five Forces Analysis

This preview shows the exact CRH Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes, providing actionable implications for CRH's market position and strategy. It's the final, fully formatted file available for instant download upon payment.

Don't Miss the Bigger Picture

CRH’s Porter's Five Forces snapshot highlights concentrated buyer power, moderate supplier influence, high competitive rivalry, limited substitutes, and barriers that temper new entrants. This brief shows core pressures but skips the force-by-force ratings, visuals and strategic implications. Unlock the full Porter’s Five Forces Analysis to access data-driven insights, actionable recommendations, and presentation-ready Excel/Word deliverables for investment or strategy decisions.

Suppliers Bargaining Power

Input diversification limits leverage

CRH sources energy, raw materials and additives from multiple vendors across c.28 countries, diluting single-supplier influence and enabling local substitution. Its vertical integration in aggregates and cement cuts external exposure, while decentralized procurement allows rapid supplier swaps. Scale purchasing across its global footprint secures volume discounts and stronger contract terms.

Energy and fuel volatility

Power, petcoke and gas suppliers gain leverage during spikes or scarcity, as energy can account for up to 40% of cement production costs; regional fuel price swings in 2022–24 saw occasional doubling in spot gas/petcoke costs. CRH mitigates exposure through hedging programs and rising alternative fuel use, and its shift to long-term energy supply frameworks in 2024 aims to stabilize input pricing.

Logistics and transport constraints

Haulage capacity and limited rail access concentrate supplier power in tight markets, with road freight carrying about 70–80% of aggregates deliveries and typical localized delivery windows of 2–4 hours restricting switching. CRH’s owned fleets and regional carriers, supported by a workforce of roughly 86,000 (2024), help reduce bottlenecks and improve resilience. Proximity of quarries and plants, often within 20–40 km of sites, lowers freight dependency and supplier leverage.

Specialty additives and equipment

Admixtures, spare parts and kiln components are concentrated among specialized suppliers—top global players in 2024 remain BASF, Sika and GCP—creating technical lock-in and pockets of bargaining power for CRH. Multiyear service agreements (commonly 3–5 years) trade reduced unit pricing for guaranteed uptime. Dual-sourcing and growing in-house technical teams limit supplier leverage and disruption risk.

- Supplier concentration: top players dominate

- Service terms: 3–5 years

- Mitigants: dual-source, in-house expertise

Permits and mineral rights

Landowners and permit holders strongly influence access to aggregates and raw feed, with scarce high-quality reserves increasing supplier leverage; CRH reports over 3,500 locations across 30+ countries, which mitigates single-site dependency. CRH’s long-dated permits and sizable reserve footprint reduce short-term exposure, while an active permitting pipeline preserves supply optionality and bargaining flexibility.

- Supplier influence: high where premium reserves are scarce

- CRH scale: over 3,500 locations across 30+ countries

- Risk mitigation: long-dated permits and reserve base

- Ongoing permits: sustain supply optionality

3,500+ sites, ~40% energy, strong freight leverage

CRH limits supplier power via vertical integration, 3,500+ sites across 30+ countries (2024) and scale purchasing; energy can be ~40% of cement costs so 2024 hedging and long-term energy deals reduce volatility. Road freight carries ~70–80% of aggregates, giving local haulage leverage mitigated by owned fleets; specialized admixture suppliers (BASF, Sika, GCP) keep pockets of technical supplier power.

| Metric | 2024 |

|---|---|

| Sites | 3,500+ |

| Workforce | 86,000 |

| Energy share | ~40% |

| Road freight | 70–80% |

| Key suppliers | BASF, Sika, GCP |

What is included in the product

Tailored Porter’s Five Forces analysis for CRH uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and critical disruptive forces—providing data-backed insight on pricing influence, market entry risks, and strategic levers to protect or grow CRH’s market position.

A concise one-sheet Porter's Five Forces for CRH that quantifies supplier, buyer, entrant, substitute and rivalry pressures—ideal for fast strategic decisions and slide-ready summaries. Customize pressure levels or swap in your own data to reflect changing markets and regulatory shifts.

Customers Bargaining Power

Large contractors and DOTs

National contractors and DOTs buy at scale and drive price pressure via competitive tendering; CRH reported full-year 2024 revenue of €26.7bn, reflecting exposure to large public contracts. These buyers demand tight specs, reliability and on-time delivery, shifting penalties and risk onto suppliers. CRH leverages integrated asphalt, aggregates and concrete offerings and long-term framework agreements that trade committed volume for pricing stability.

Project-based bidding

Construction is bid-driven, with buyers routinely comparing suppliers across projects; local aggregates markets typically constrain viable alternatives to providers within roughly 50–100 km. Switching costs are moderate, largely logistical and spec-related, so buyers rebid frequently. Strong QA/QC and performance history can justify modest premiums of around 3–7% on unit pricing.

Spec and standards stickiness

DOT and engineering specifications create approved-material lists for IIJA-funded projects (the 2021 Infrastructure Investment and Jobs Act authorized $1.2 trillion), making supplier qualification a gateway to repeat business and less price-only competition. CRH leverages certifications and consistent quality to reduce churn, while technical support teams embed CRH early in project design to lock in specs and long-term supply relationships.

Sustainability requirements

Buyers increasingly demand EPDs, recycled content and low-carbon mixes, driven by ESG mandates that push for greener options at comparable cost; cement and concrete account for about 7% of global CO2 emissions, raising procurement scrutiny. CRH’s decarbonization roadmap and alternative binders create differentiation, tempering pure price bargaining and enabling value-based sales.

- EPDs & low‑carbon mixes demanded; sector ≈7% of CO2

Local market fragmentation

Local market fragmentation leaves many small and mid-sized buyers with limited leverage, and proximity economics often constrain supplier choice; in 2024 CRH reported group revenue of €32.5bn and c.3,000 local operations which underpin delivery density. Service reliability and credit terms carry heavy weight for buyers and raise switching costs. High local reach helps CRH sustain price realization across fragmented markets.

- 2024 revenue: €32.5bn

- Local operations: ≈3,000 sites

- Delivery density increases switching friction

Tender-driven price pressure from large contractors; local network (~3,000) and ESG shift buying

Large national contractors and DOTs exert strong price pressure via tendering; CRH reported 2024 revenue €32.5bn, exposing it to big public contracts. Switching costs are moderate and local proximity limits alternatives, with c.3,000 sites boosting delivery density. ESG specs (cement ≈7% of CO2) raise value-based buying, reducing pure price bargaining.

| Metric | 2024 |

|---|---|

| Revenue | €32.5bn |

| Local sites | ≈3,000 |

| Cement CO2 share | ≈7% |

Full Version Awaits

CRH Porter's Five Forces Analysis

This preview shows the exact CRH Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes, providing actionable implications for CRH's market position and strategy. It's the final, fully formatted file available for instant download upon payment.

Description

Don't Miss the Bigger Picture

CRH’s Porter's Five Forces snapshot highlights concentrated buyer power, moderate supplier influence, high competitive rivalry, limited substitutes, and barriers that temper new entrants. This brief shows core pressures but skips the force-by-force ratings, visuals and strategic implications. Unlock the full Porter’s Five Forces Analysis to access data-driven insights, actionable recommendations, and presentation-ready Excel/Word deliverables for investment or strategy decisions.

Suppliers Bargaining Power

Input diversification limits leverage

CRH sources energy, raw materials and additives from multiple vendors across c.28 countries, diluting single-supplier influence and enabling local substitution. Its vertical integration in aggregates and cement cuts external exposure, while decentralized procurement allows rapid supplier swaps. Scale purchasing across its global footprint secures volume discounts and stronger contract terms.

Energy and fuel volatility

Power, petcoke and gas suppliers gain leverage during spikes or scarcity, as energy can account for up to 40% of cement production costs; regional fuel price swings in 2022–24 saw occasional doubling in spot gas/petcoke costs. CRH mitigates exposure through hedging programs and rising alternative fuel use, and its shift to long-term energy supply frameworks in 2024 aims to stabilize input pricing.

Logistics and transport constraints

Haulage capacity and limited rail access concentrate supplier power in tight markets, with road freight carrying about 70–80% of aggregates deliveries and typical localized delivery windows of 2–4 hours restricting switching. CRH’s owned fleets and regional carriers, supported by a workforce of roughly 86,000 (2024), help reduce bottlenecks and improve resilience. Proximity of quarries and plants, often within 20–40 km of sites, lowers freight dependency and supplier leverage.

Specialty additives and equipment

Admixtures, spare parts and kiln components are concentrated among specialized suppliers—top global players in 2024 remain BASF, Sika and GCP—creating technical lock-in and pockets of bargaining power for CRH. Multiyear service agreements (commonly 3–5 years) trade reduced unit pricing for guaranteed uptime. Dual-sourcing and growing in-house technical teams limit supplier leverage and disruption risk.

- Supplier concentration: top players dominate

- Service terms: 3–5 years

- Mitigants: dual-source, in-house expertise

Permits and mineral rights

Landowners and permit holders strongly influence access to aggregates and raw feed, with scarce high-quality reserves increasing supplier leverage; CRH reports over 3,500 locations across 30+ countries, which mitigates single-site dependency. CRH’s long-dated permits and sizable reserve footprint reduce short-term exposure, while an active permitting pipeline preserves supply optionality and bargaining flexibility.

- Supplier influence: high where premium reserves are scarce

- CRH scale: over 3,500 locations across 30+ countries

- Risk mitigation: long-dated permits and reserve base

- Ongoing permits: sustain supply optionality

3,500+ sites, ~40% energy, strong freight leverage

CRH limits supplier power via vertical integration, 3,500+ sites across 30+ countries (2024) and scale purchasing; energy can be ~40% of cement costs so 2024 hedging and long-term energy deals reduce volatility. Road freight carries ~70–80% of aggregates, giving local haulage leverage mitigated by owned fleets; specialized admixture suppliers (BASF, Sika, GCP) keep pockets of technical supplier power.

| Metric | 2024 |

|---|---|

| Sites | 3,500+ |

| Workforce | 86,000 |

| Energy share | ~40% |

| Road freight | 70–80% |

| Key suppliers | BASF, Sika, GCP |

What is included in the product

Tailored Porter’s Five Forces analysis for CRH uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and critical disruptive forces—providing data-backed insight on pricing influence, market entry risks, and strategic levers to protect or grow CRH’s market position.

A concise one-sheet Porter's Five Forces for CRH that quantifies supplier, buyer, entrant, substitute and rivalry pressures—ideal for fast strategic decisions and slide-ready summaries. Customize pressure levels or swap in your own data to reflect changing markets and regulatory shifts.

Customers Bargaining Power

Large contractors and DOTs

National contractors and DOTs buy at scale and drive price pressure via competitive tendering; CRH reported full-year 2024 revenue of €26.7bn, reflecting exposure to large public contracts. These buyers demand tight specs, reliability and on-time delivery, shifting penalties and risk onto suppliers. CRH leverages integrated asphalt, aggregates and concrete offerings and long-term framework agreements that trade committed volume for pricing stability.

Project-based bidding

Construction is bid-driven, with buyers routinely comparing suppliers across projects; local aggregates markets typically constrain viable alternatives to providers within roughly 50–100 km. Switching costs are moderate, largely logistical and spec-related, so buyers rebid frequently. Strong QA/QC and performance history can justify modest premiums of around 3–7% on unit pricing.

Spec and standards stickiness

DOT and engineering specifications create approved-material lists for IIJA-funded projects (the 2021 Infrastructure Investment and Jobs Act authorized $1.2 trillion), making supplier qualification a gateway to repeat business and less price-only competition. CRH leverages certifications and consistent quality to reduce churn, while technical support teams embed CRH early in project design to lock in specs and long-term supply relationships.

Sustainability requirements

Buyers increasingly demand EPDs, recycled content and low-carbon mixes, driven by ESG mandates that push for greener options at comparable cost; cement and concrete account for about 7% of global CO2 emissions, raising procurement scrutiny. CRH’s decarbonization roadmap and alternative binders create differentiation, tempering pure price bargaining and enabling value-based sales.

- EPDs & low‑carbon mixes demanded; sector ≈7% of CO2

Local market fragmentation

Local market fragmentation leaves many small and mid-sized buyers with limited leverage, and proximity economics often constrain supplier choice; in 2024 CRH reported group revenue of €32.5bn and c.3,000 local operations which underpin delivery density. Service reliability and credit terms carry heavy weight for buyers and raise switching costs. High local reach helps CRH sustain price realization across fragmented markets.

- 2024 revenue: €32.5bn

- Local operations: ≈3,000 sites

- Delivery density increases switching friction

Tender-driven price pressure from large contractors; local network (~3,000) and ESG shift buying

Large national contractors and DOTs exert strong price pressure via tendering; CRH reported 2024 revenue €32.5bn, exposing it to big public contracts. Switching costs are moderate and local proximity limits alternatives, with c.3,000 sites boosting delivery density. ESG specs (cement ≈7% of CO2) raise value-based buying, reducing pure price bargaining.

| Metric | 2024 |

|---|---|

| Revenue | €32.5bn |

| Local sites | ≈3,000 |

| Cement CO2 share | ≈7% |

Full Version Awaits

CRH Porter's Five Forces Analysis

This preview shows the exact CRH Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes, providing actionable implications for CRH's market position and strategy. It's the final, fully formatted file available for instant download upon payment.