Criteo Porter's Five Forces Analysis

From Overview to Strategy Blueprint

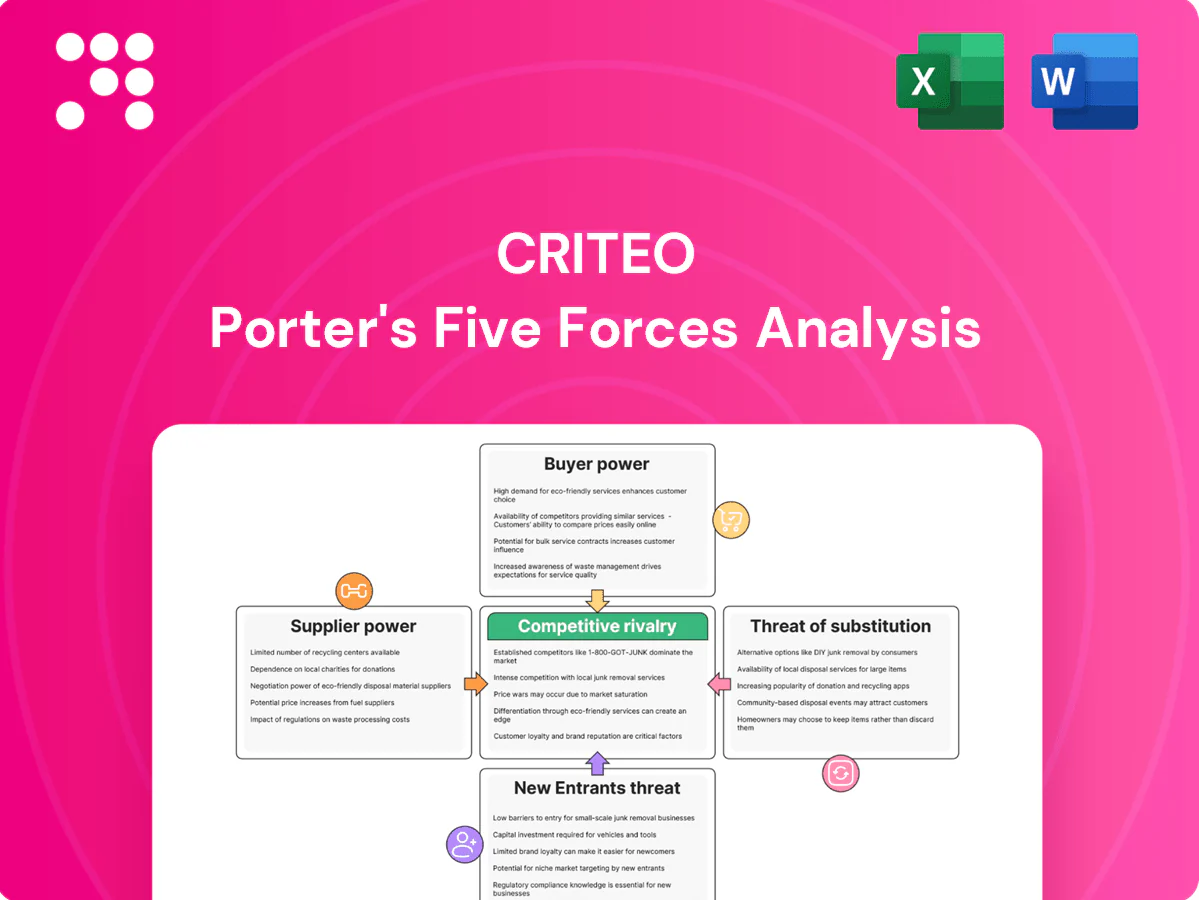

Criteo faces intense rivalry from ad-tech giants and programmatic platforms, moderate buyer power due to large advertiser consolidation, and supplier dependence on publishers and data partners; regulatory and privacy shifts raise the threat of substitutes and barriers to entry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Criteo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated premium publishers

As of 2024, Criteo depends on high-quality inventory from major publishers and SSPs that can demand higher take rates and stricter terms; scarcity of premium supply, especially in commerce-heavy verticals, increases publishers' leverage. Header bidding and supply-path optimization have reduced but not removed concentration risk. Losing exclusive or preferred supply can materially reduce campaign scale and ROAS.

Platform gatekeepers’ policies

Platform gatekeepers Apple and Google control IDs, ATT, ITP and browser policies that shrink signal availability and attribution. ATT opt-in rates hovered near 25% in 2024, while Chrome holds roughly 65% global browser share, making cookie deprecation impactful. Changes like ATT, ITP and planned third-party cookie phase-out raise costs, reduce precision, and force engineering work and vendor dependence. These gatekeepers thus exert structural supplier power over identity and measurement rails.

Cloud and adtech infrastructure

Criteo depends on hyperscalers, CDPs and measurement vendors for compute, storage and tooling; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 11% of the cloud market, concentrating supplier power. Pricing changes, egress fees or outages can compress margins and hurt reliability. Long-term contracts and committed-use discounts (commonly 20–40%) reduce unit costs but create switching costs. Regional data residency and performance SLAs add supplier leverage and operational complexity.

Retail and data partnerships

Access to retailers’ first-party data and on-site inventory is foundational to commerce media; in 2024 Criteo, a NASDAQ-listed commerce media provider, relies on retailer partnerships that underpin targeting and closed-loop reporting, and losing a marquee partner can materially reduce match rates and post-click attribution quality.

Large retailers can negotiate revenue shares, data-usage limits and exclusivities, shifting economics—co-innovation roadmaps align product roadmaps but deepen dependency, concentrating supplier leverage.

- Revenue sensitivity: 2023 full-year revenue ~€1.43bn (reported in 2024)

- Concentration risk: marquee partner loss reduces closed-loop reporting and targeting accuracy

- Negotiation levers: revenue share, data constraints, exclusivity, co-innovation roadmaps

Specialized talent and tools

AI/ML talent, measurement scientists and privacy engineers are scarce and costly, with Glassdoor 2024 showing senior ML engineer base pay often above 160,000 USD, driving compensation inflation and boosting labor bargaining power; non-compete limitations and mobility further raise costs. Niche ad-verification and brand-safety vendors wield leverage via certification standards, and tight labor markets or tool deprecations can slow Criteo product velocity.

- AI/ML pay pressure — senior ML >160k (Glassdoor 2024)

- Non-compete limits increase churn and wage bids

- Certification-driven leverage from ad-verification tools

Publisher power, cloud concentration and AI pay threaten scale; rev €1.43bn

Criteo faces strong supplier power: premium publisher inventory, retailer first‑party data and platform gatekeepers (ATT opt‑in ~25%, Chrome ~65% share) can raise costs and constrain targeting; cloud concentration (AWS 32%, Azure 23%, GCP 11%) and costly AI talent (senior ML >160,000 USD) further increase leverage. Loss of marquee partners threatens scale and ROAS; revenue sensitivity remains high (2023 revenue ~€1.43bn).

| Metric | 2024/2023 |

|---|---|

| 2023 Revenue | ~€1.43bn |

| ATT opt‑in | ~25% |

| Chrome share | ~65% |

| AWS/Azure/GCP | 32% / 23% / 11% |

| Senior ML pay | >160,000 USD |

What is included in the product

Concise Porter's Five Forces analysis tailored to Criteo, revealing competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and industry factors shaping its pricing and profitability.

A one-sheet Porter's Five Forces for Criteo—customize pressure levels and instantly visualize strategic pressure with a spider chart for fast, board-ready decision-making.

Customers Bargaining Power

Large advertisers and agencies

Large global brands and holding-company agencies, which collectively manage hundreds of billions in media spend, aggregate buying power to negotiate lower fees and tighter SLAs with Criteo. Their ability to multi-home across publishers and DSPs increases pressure on pricing and demands greater transparency. Outcome-based CPC/CPA models transfer campaign risk onto Criteo, while consolidated RFPs favor scaled vendors and compress Criteo’s pricing power.

Retailers with closed-loop data

Retailers that own closed-loop purchase data wield dual leverage over Criteo by buying media and supplying high-value first-party data; global retail media captured over 100 billion USD in ad spend in 2024, concentrating bargaining power. They demand granular attribution, ROAS guarantees and flexible integrations, and can reallocate budgets to proprietary networks if performance slips. Control of purchase-level data increases switching power and strengthens their negotiating position.

Low switching costs via APIs

Standardized integrations and widespread APIs let advertisers test alternative DSPs and retail media partners quickly, and global programmatic ad spend—about $225 billion in 2024—raises incentives to optimize allocations. Buyers run A/B budget splits to compare lift and price, driving down CPMs and compressing vendor margins. This fluidity shortens contract durations and increases churn, forcing Criteo to deliver differentiated commerce outcomes to retain share of wallet.

Performance transparency expectations

Buyers now insist on log-level data, incrementality tests, and clean-room measurement, and any opacity around attribution or privacy compliance prompts immediate price concessions and contract renegotiation. Superior reporting is table stakes rather than a premium, raising Criteo’s operational costs while consolidating buyer leverage. These transparency demands materially strengthen customer bargaining power.

- log-level data required

- incrementality & clean-room measurement

- opacity => price concessions

- reporting = table stakes

- higher ops costs, stronger buyer power

Macro budget cyclicality

Ad budgets react swiftly to macro cycles, letting buyers pause or renegotiate spend and pressuring Criteo's pricing and take rates; seasonal peaks heighten rate sensitivity and auction volatility as advertisers optimize for ROI.

Budget fluidity drives shifts toward walled gardens when performance lags, keeping CPMs and margin compression persistent (global digital ad spend ~600B in 2024).

- Buyers leverage: pause/renegotiate

- Seasonality: spikes in rate sensitivity

- Shift risk: walled gardens if ROAS drops

- Result: pricing and take rates under pressure

Buyers scale and data demands squeeze ad platform fees and compress CPMs

Global advertisers/agencies and retailers (retail media >100B USD in 2024) exert strong pricing and data leverage, forcing lower fees and tighter SLAs on Criteo.

Programmatic scale (~225B USD DSP spend) and $600B global digital ad market in 2024 enable multi-homing, short contracts and CPM compression.

Requests for log-level data, incrementality and clean-room measurement raise ops costs and strengthen buyer bargaining power.

| Metric | 2024 |

|---|---|

| Global digital ad spend | ~600B USD |

| Programmatic/DSP spend | ~225B USD |

| Retail media | >100B USD |

Preview the Actual Deliverable

Criteo Porter's Five Forces Analysis

This preview shows the exact Criteo Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups. The file is the complete, professionally formatted document, ready for download and use the moment you buy. You’re viewing the final deliverable; purchase grants instant access to this same document.

From Overview to Strategy Blueprint

Criteo faces intense rivalry from ad-tech giants and programmatic platforms, moderate buyer power due to large advertiser consolidation, and supplier dependence on publishers and data partners; regulatory and privacy shifts raise the threat of substitutes and barriers to entry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Criteo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated premium publishers

As of 2024, Criteo depends on high-quality inventory from major publishers and SSPs that can demand higher take rates and stricter terms; scarcity of premium supply, especially in commerce-heavy verticals, increases publishers' leverage. Header bidding and supply-path optimization have reduced but not removed concentration risk. Losing exclusive or preferred supply can materially reduce campaign scale and ROAS.

Platform gatekeepers’ policies

Platform gatekeepers Apple and Google control IDs, ATT, ITP and browser policies that shrink signal availability and attribution. ATT opt-in rates hovered near 25% in 2024, while Chrome holds roughly 65% global browser share, making cookie deprecation impactful. Changes like ATT, ITP and planned third-party cookie phase-out raise costs, reduce precision, and force engineering work and vendor dependence. These gatekeepers thus exert structural supplier power over identity and measurement rails.

Cloud and adtech infrastructure

Criteo depends on hyperscalers, CDPs and measurement vendors for compute, storage and tooling; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 11% of the cloud market, concentrating supplier power. Pricing changes, egress fees or outages can compress margins and hurt reliability. Long-term contracts and committed-use discounts (commonly 20–40%) reduce unit costs but create switching costs. Regional data residency and performance SLAs add supplier leverage and operational complexity.

Retail and data partnerships

Access to retailers’ first-party data and on-site inventory is foundational to commerce media; in 2024 Criteo, a NASDAQ-listed commerce media provider, relies on retailer partnerships that underpin targeting and closed-loop reporting, and losing a marquee partner can materially reduce match rates and post-click attribution quality.

Large retailers can negotiate revenue shares, data-usage limits and exclusivities, shifting economics—co-innovation roadmaps align product roadmaps but deepen dependency, concentrating supplier leverage.

- Revenue sensitivity: 2023 full-year revenue ~€1.43bn (reported in 2024)

- Concentration risk: marquee partner loss reduces closed-loop reporting and targeting accuracy

- Negotiation levers: revenue share, data constraints, exclusivity, co-innovation roadmaps

Specialized talent and tools

AI/ML talent, measurement scientists and privacy engineers are scarce and costly, with Glassdoor 2024 showing senior ML engineer base pay often above 160,000 USD, driving compensation inflation and boosting labor bargaining power; non-compete limitations and mobility further raise costs. Niche ad-verification and brand-safety vendors wield leverage via certification standards, and tight labor markets or tool deprecations can slow Criteo product velocity.

- AI/ML pay pressure — senior ML >160k (Glassdoor 2024)

- Non-compete limits increase churn and wage bids

- Certification-driven leverage from ad-verification tools

Publisher power, cloud concentration and AI pay threaten scale; rev €1.43bn

Criteo faces strong supplier power: premium publisher inventory, retailer first‑party data and platform gatekeepers (ATT opt‑in ~25%, Chrome ~65% share) can raise costs and constrain targeting; cloud concentration (AWS 32%, Azure 23%, GCP 11%) and costly AI talent (senior ML >160,000 USD) further increase leverage. Loss of marquee partners threatens scale and ROAS; revenue sensitivity remains high (2023 revenue ~€1.43bn).

| Metric | 2024/2023 |

|---|---|

| 2023 Revenue | ~€1.43bn |

| ATT opt‑in | ~25% |

| Chrome share | ~65% |

| AWS/Azure/GCP | 32% / 23% / 11% |

| Senior ML pay | >160,000 USD |

What is included in the product

Concise Porter's Five Forces analysis tailored to Criteo, revealing competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and industry factors shaping its pricing and profitability.

A one-sheet Porter's Five Forces for Criteo—customize pressure levels and instantly visualize strategic pressure with a spider chart for fast, board-ready decision-making.

Customers Bargaining Power

Large advertisers and agencies

Large global brands and holding-company agencies, which collectively manage hundreds of billions in media spend, aggregate buying power to negotiate lower fees and tighter SLAs with Criteo. Their ability to multi-home across publishers and DSPs increases pressure on pricing and demands greater transparency. Outcome-based CPC/CPA models transfer campaign risk onto Criteo, while consolidated RFPs favor scaled vendors and compress Criteo’s pricing power.

Retailers with closed-loop data

Retailers that own closed-loop purchase data wield dual leverage over Criteo by buying media and supplying high-value first-party data; global retail media captured over 100 billion USD in ad spend in 2024, concentrating bargaining power. They demand granular attribution, ROAS guarantees and flexible integrations, and can reallocate budgets to proprietary networks if performance slips. Control of purchase-level data increases switching power and strengthens their negotiating position.

Low switching costs via APIs

Standardized integrations and widespread APIs let advertisers test alternative DSPs and retail media partners quickly, and global programmatic ad spend—about $225 billion in 2024—raises incentives to optimize allocations. Buyers run A/B budget splits to compare lift and price, driving down CPMs and compressing vendor margins. This fluidity shortens contract durations and increases churn, forcing Criteo to deliver differentiated commerce outcomes to retain share of wallet.

Performance transparency expectations

Buyers now insist on log-level data, incrementality tests, and clean-room measurement, and any opacity around attribution or privacy compliance prompts immediate price concessions and contract renegotiation. Superior reporting is table stakes rather than a premium, raising Criteo’s operational costs while consolidating buyer leverage. These transparency demands materially strengthen customer bargaining power.

- log-level data required

- incrementality & clean-room measurement

- opacity => price concessions

- reporting = table stakes

- higher ops costs, stronger buyer power

Macro budget cyclicality

Ad budgets react swiftly to macro cycles, letting buyers pause or renegotiate spend and pressuring Criteo's pricing and take rates; seasonal peaks heighten rate sensitivity and auction volatility as advertisers optimize for ROI.

Budget fluidity drives shifts toward walled gardens when performance lags, keeping CPMs and margin compression persistent (global digital ad spend ~600B in 2024).

- Buyers leverage: pause/renegotiate

- Seasonality: spikes in rate sensitivity

- Shift risk: walled gardens if ROAS drops

- Result: pricing and take rates under pressure

Buyers scale and data demands squeeze ad platform fees and compress CPMs

Global advertisers/agencies and retailers (retail media >100B USD in 2024) exert strong pricing and data leverage, forcing lower fees and tighter SLAs on Criteo.

Programmatic scale (~225B USD DSP spend) and $600B global digital ad market in 2024 enable multi-homing, short contracts and CPM compression.

Requests for log-level data, incrementality and clean-room measurement raise ops costs and strengthen buyer bargaining power.

| Metric | 2024 |

|---|---|

| Global digital ad spend | ~600B USD |

| Programmatic/DSP spend | ~225B USD |

| Retail media | >100B USD |

Preview the Actual Deliverable

Criteo Porter's Five Forces Analysis

This preview shows the exact Criteo Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups. The file is the complete, professionally formatted document, ready for download and use the moment you buy. You’re viewing the final deliverable; purchase grants instant access to this same document.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Criteo faces intense rivalry from ad-tech giants and programmatic platforms, moderate buyer power due to large advertiser consolidation, and supplier dependence on publishers and data partners; regulatory and privacy shifts raise the threat of substitutes and barriers to entry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Criteo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated premium publishers

As of 2024, Criteo depends on high-quality inventory from major publishers and SSPs that can demand higher take rates and stricter terms; scarcity of premium supply, especially in commerce-heavy verticals, increases publishers' leverage. Header bidding and supply-path optimization have reduced but not removed concentration risk. Losing exclusive or preferred supply can materially reduce campaign scale and ROAS.

Platform gatekeepers’ policies

Platform gatekeepers Apple and Google control IDs, ATT, ITP and browser policies that shrink signal availability and attribution. ATT opt-in rates hovered near 25% in 2024, while Chrome holds roughly 65% global browser share, making cookie deprecation impactful. Changes like ATT, ITP and planned third-party cookie phase-out raise costs, reduce precision, and force engineering work and vendor dependence. These gatekeepers thus exert structural supplier power over identity and measurement rails.

Cloud and adtech infrastructure

Criteo depends on hyperscalers, CDPs and measurement vendors for compute, storage and tooling; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 11% of the cloud market, concentrating supplier power. Pricing changes, egress fees or outages can compress margins and hurt reliability. Long-term contracts and committed-use discounts (commonly 20–40%) reduce unit costs but create switching costs. Regional data residency and performance SLAs add supplier leverage and operational complexity.

Retail and data partnerships

Access to retailers’ first-party data and on-site inventory is foundational to commerce media; in 2024 Criteo, a NASDAQ-listed commerce media provider, relies on retailer partnerships that underpin targeting and closed-loop reporting, and losing a marquee partner can materially reduce match rates and post-click attribution quality.

Large retailers can negotiate revenue shares, data-usage limits and exclusivities, shifting economics—co-innovation roadmaps align product roadmaps but deepen dependency, concentrating supplier leverage.

- Revenue sensitivity: 2023 full-year revenue ~€1.43bn (reported in 2024)

- Concentration risk: marquee partner loss reduces closed-loop reporting and targeting accuracy

- Negotiation levers: revenue share, data constraints, exclusivity, co-innovation roadmaps

Specialized talent and tools

AI/ML talent, measurement scientists and privacy engineers are scarce and costly, with Glassdoor 2024 showing senior ML engineer base pay often above 160,000 USD, driving compensation inflation and boosting labor bargaining power; non-compete limitations and mobility further raise costs. Niche ad-verification and brand-safety vendors wield leverage via certification standards, and tight labor markets or tool deprecations can slow Criteo product velocity.

- AI/ML pay pressure — senior ML >160k (Glassdoor 2024)

- Non-compete limits increase churn and wage bids

- Certification-driven leverage from ad-verification tools

Publisher power, cloud concentration and AI pay threaten scale; rev €1.43bn

Criteo faces strong supplier power: premium publisher inventory, retailer first‑party data and platform gatekeepers (ATT opt‑in ~25%, Chrome ~65% share) can raise costs and constrain targeting; cloud concentration (AWS 32%, Azure 23%, GCP 11%) and costly AI talent (senior ML >160,000 USD) further increase leverage. Loss of marquee partners threatens scale and ROAS; revenue sensitivity remains high (2023 revenue ~€1.43bn).

| Metric | 2024/2023 |

|---|---|

| 2023 Revenue | ~€1.43bn |

| ATT opt‑in | ~25% |

| Chrome share | ~65% |

| AWS/Azure/GCP | 32% / 23% / 11% |

| Senior ML pay | >160,000 USD |

What is included in the product

Concise Porter's Five Forces analysis tailored to Criteo, revealing competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and industry factors shaping its pricing and profitability.

A one-sheet Porter's Five Forces for Criteo—customize pressure levels and instantly visualize strategic pressure with a spider chart for fast, board-ready decision-making.

Customers Bargaining Power

Large advertisers and agencies

Large global brands and holding-company agencies, which collectively manage hundreds of billions in media spend, aggregate buying power to negotiate lower fees and tighter SLAs with Criteo. Their ability to multi-home across publishers and DSPs increases pressure on pricing and demands greater transparency. Outcome-based CPC/CPA models transfer campaign risk onto Criteo, while consolidated RFPs favor scaled vendors and compress Criteo’s pricing power.

Retailers with closed-loop data

Retailers that own closed-loop purchase data wield dual leverage over Criteo by buying media and supplying high-value first-party data; global retail media captured over 100 billion USD in ad spend in 2024, concentrating bargaining power. They demand granular attribution, ROAS guarantees and flexible integrations, and can reallocate budgets to proprietary networks if performance slips. Control of purchase-level data increases switching power and strengthens their negotiating position.

Low switching costs via APIs

Standardized integrations and widespread APIs let advertisers test alternative DSPs and retail media partners quickly, and global programmatic ad spend—about $225 billion in 2024—raises incentives to optimize allocations. Buyers run A/B budget splits to compare lift and price, driving down CPMs and compressing vendor margins. This fluidity shortens contract durations and increases churn, forcing Criteo to deliver differentiated commerce outcomes to retain share of wallet.

Performance transparency expectations

Buyers now insist on log-level data, incrementality tests, and clean-room measurement, and any opacity around attribution or privacy compliance prompts immediate price concessions and contract renegotiation. Superior reporting is table stakes rather than a premium, raising Criteo’s operational costs while consolidating buyer leverage. These transparency demands materially strengthen customer bargaining power.

- log-level data required

- incrementality & clean-room measurement

- opacity => price concessions

- reporting = table stakes

- higher ops costs, stronger buyer power

Macro budget cyclicality

Ad budgets react swiftly to macro cycles, letting buyers pause or renegotiate spend and pressuring Criteo's pricing and take rates; seasonal peaks heighten rate sensitivity and auction volatility as advertisers optimize for ROI.

Budget fluidity drives shifts toward walled gardens when performance lags, keeping CPMs and margin compression persistent (global digital ad spend ~600B in 2024).

- Buyers leverage: pause/renegotiate

- Seasonality: spikes in rate sensitivity

- Shift risk: walled gardens if ROAS drops

- Result: pricing and take rates under pressure

Buyers scale and data demands squeeze ad platform fees and compress CPMs

Global advertisers/agencies and retailers (retail media >100B USD in 2024) exert strong pricing and data leverage, forcing lower fees and tighter SLAs on Criteo.

Programmatic scale (~225B USD DSP spend) and $600B global digital ad market in 2024 enable multi-homing, short contracts and CPM compression.

Requests for log-level data, incrementality and clean-room measurement raise ops costs and strengthen buyer bargaining power.

| Metric | 2024 |

|---|---|

| Global digital ad spend | ~600B USD |

| Programmatic/DSP spend | ~225B USD |

| Retail media | >100B USD |

Preview the Actual Deliverable

Criteo Porter's Five Forces Analysis

This preview shows the exact Criteo Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups. The file is the complete, professionally formatted document, ready for download and use the moment you buy. You’re viewing the final deliverable; purchase grants instant access to this same document.