Criteo PESTLE Analysis

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Criteo reveals how political regulation, economic shifts, and rapid adtech innovation are reshaping its growth prospects. Actionable insights identify regulatory risks, privacy trends, and technological opportunities for investors and strategists. Purchase the full report to get the complete, editable analysis and strategic recommendations instantly.

Political factors

Data sovereignty and localization

Cross-border ad delivery must respect national localization rules, with the EU GDPR (2018) allowing fines up to €20 million or 4% of global turnover and the US CLOUD Act (2018) altering cross‑border access; China’s PIPL (effective 2021) permits penalties up to RMB 50 million or 5% of revenue. Divergent EU, US and APAC regimes force Criteo to route and store user data regionally. Aligning infrastructure to sovereign requirements raises capex/opex but unlocks market access, while sudden government scrutiny can tighten controls quickly, increasing latency and limiting scale.

Digital taxation and tech levies

Digital services taxes and the OECD Pillar Two global minimum tax (15% adopted by 137 Inclusive Framework jurisdictions) raise effective tax rates and pressure Criteo's margins. Multi-country operations increase compliance complexity and dispute risk across jurisdictions with unilateral DSTs. Pricing and agile financial planning are required to pass through costs amid ongoing policy volatility.

Trade relations and platform access

Geopolitical tensions can curtail partnerships, APIs or cloud vendors—AWS (~32%), Azure (~23%) and GCP (~11%) concentration (2024 IDC) raises platform-access risk if providers face sanctions. US export controls since 2022 restrict high-end AI chips to China, limiting tooling and talent mobility. Market entry hinges on stable trade channels and the EU‑US Data Privacy Framework (adopted 2023) for cross‑border data; diversification reduces concentration risk.

Public policy on online advertising

Governments increasingly set rules on targeting, transparency and political ads; GDPR (2018) and the EU DSA/DMA (in force 2024) sharply raised compliance expectations. Stricter norms limit personalization levers and can reduce targeting effectiveness, while global digital ad spend was about $517 billion in 2023. Criteo must engage in policy dialogue and early adaptation to gain competitive advantage.

- Policy: DSA/DMA 2024

- Risk: reduced personalization

- Opportunity: first-mover compliance

- Market: $517B digital ads 2023

Subsidies and innovation incentives

Grants and tax credits for AI, cloud and R&D (Horizon Europe €95.5bn 2021–27; US CHIPS Act $52.7bn) can cut effective project costs—R&D incentives in many markets lower cash tax by roughly 10–30%—while public‑private programs accelerate Criteo product roadmaps through co‑funding and pilots.

- Local presence & compliance determine eligibility

- Choose hubs (EU, US, Israel) to maximize returns

- Leverage co‑funding to shorten time‑to‑market

Regulation, taxes and concentrated cloud power force cross-border digital strategy shifts

Cross‑border rules force regional data routing: GDPR fines up to €20m/4% turnover, China PIPL penalties up to RMB50m/5%, CLOUD Act affects access; EU‑US Data Privacy Framework adopted 2023.

Tax and levies squeeze margins: OECD Pillar Two 15% (137 jurisdictions), unilateral DSTs; global digital ad spend $517B (2023).

Platform risk high: AWS ~32%, Azure ~23%, GCP ~11% (2024 IDC); US export controls and grants (CHIPS $52.7B, Horizon €95.5B) shape strategy.

| Metric | Value |

|---|---|

| GDPR fine | €20M / 4% |

| Pillar Two | 15% |

| Cloud share (2024) | AWS32% AZ23% GCP11% |

What is included in the product

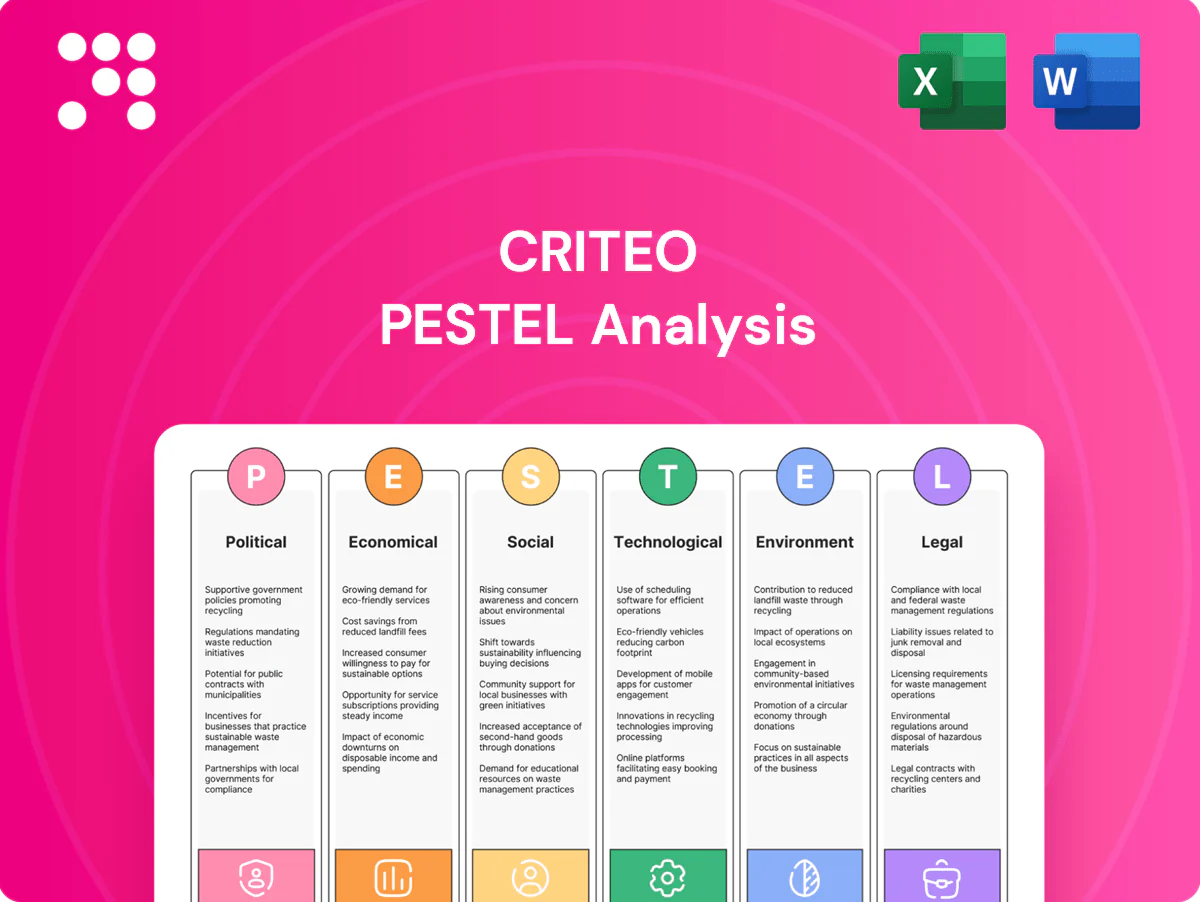

Explores how external macro-environmental factors uniquely affect Criteo across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Each section uses current data and trend-backed subpoints and forward-looking insights to help executives, consultants, and investors identify regulatory, market and tech-driven threats and opportunities.

A concise, visually segmented Criteo PESTLE summary that distills external risks and market drivers for quick reference in meetings, easily shareable and editable for region- or team-specific planning.

Economic factors

Ad spend cyclicality

Advertising budgets track consumer demand and GDP: WARC reported global adspend at about $729bn in 2023 while IMF projected ~3.0% global GDP growth for 2024, linking budgets to macro trends. Downturns shift spend to measurable performance channels where Criteo competes, increasing share for ROI-focused buys. Recovery phases reward measurable incrementality and flexible cross-vertical offerings help smooth cyclical volatility.

Retail media monetization

Retailers are pursuing new profit pools from retail media as the channel scales—Amazon ad revenue topped about 46 billion dollars in 2023, underscoring opportunity for others. Criteo’s Commerce Media can capture this shift by activating first-party data across retailer inventories. Revenue potential rises with retailer adoption and shopper traffic; strong measurement and ROI drive repeat advertiser spend and lift lifetime value.

Currency and inflation pressures

Multi-currency revenues expose Criteo to FX volatility across major corridors, pressuring reported top-line when currencies weaken versus the euro. Rising inflation lifts cloud, talent and traffic acquisition costs, squeezing CPA and margin profiles. Contract indexation and dynamic pricing models help preserve margins by passing cost increases to clients. Active hedging programs can dampen short-term earnings swings and stabilize cash flow.

Competition with walled gardens

Large platforms like Google and Meta captured roughly 60% of global digital ad spend in 2024 (eMarketer), creating budget and data advantages that pressure open-internet players; Criteo must demonstrate comparable ROI from its open-web inventory. Criteo offsets concentration via deep publisher and retailer partnerships and differentiated multi-touch attribution to protect and grow share.

- Platforms: ~60% ad share 2024

- Counter: publisher/retailer partnerships

- Edge: differentiated attribution strengthens share

SMB and mid-market dynamics

- turnkey-solutions

- low-touch-onboarding

- self-serve-automation

- payment-risk-management

Regulation, taxes and concentrated cloud power force cross-border digital strategy shifts

Ad budgets track GDP and demand: global adspend ~$729bn (WARC 2023) while ROI channels gain in downturns, favoring Criteo’s performance stack.

Retail media scales—Amazon ads ~$46bn (2023); Criteo can capture retailer-first‑party opportunities via Commerce Media.

FY2023 revenue ~€1.46B; FX, inflation and ~60% platform concentration (eMarketer 2024) pressure margins and pricing power.

| Metric | Value | Source/Year |

|---|---|---|

| Global adspend | $729bn | WARC 2023 |

| Amazon ad revenue | $46bn | 2023 |

| Criteo revenue | €1.46B | FY2023 |

| Platform share | ~60% | eMarketer 2024 |

Full Version Awaits

Criteo PESTLE Analysis

The preview shown here is the exact Criteo PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real snapshot of the product you’re buying, delivered exactly as shown with no placeholders. The layout, content, and structure visible here are the final version available for immediate download after payment.

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Criteo reveals how political regulation, economic shifts, and rapid adtech innovation are reshaping its growth prospects. Actionable insights identify regulatory risks, privacy trends, and technological opportunities for investors and strategists. Purchase the full report to get the complete, editable analysis and strategic recommendations instantly.

Political factors

Data sovereignty and localization

Cross-border ad delivery must respect national localization rules, with the EU GDPR (2018) allowing fines up to €20 million or 4% of global turnover and the US CLOUD Act (2018) altering cross‑border access; China’s PIPL (effective 2021) permits penalties up to RMB 50 million or 5% of revenue. Divergent EU, US and APAC regimes force Criteo to route and store user data regionally. Aligning infrastructure to sovereign requirements raises capex/opex but unlocks market access, while sudden government scrutiny can tighten controls quickly, increasing latency and limiting scale.

Digital taxation and tech levies

Digital services taxes and the OECD Pillar Two global minimum tax (15% adopted by 137 Inclusive Framework jurisdictions) raise effective tax rates and pressure Criteo's margins. Multi-country operations increase compliance complexity and dispute risk across jurisdictions with unilateral DSTs. Pricing and agile financial planning are required to pass through costs amid ongoing policy volatility.

Trade relations and platform access

Geopolitical tensions can curtail partnerships, APIs or cloud vendors—AWS (~32%), Azure (~23%) and GCP (~11%) concentration (2024 IDC) raises platform-access risk if providers face sanctions. US export controls since 2022 restrict high-end AI chips to China, limiting tooling and talent mobility. Market entry hinges on stable trade channels and the EU‑US Data Privacy Framework (adopted 2023) for cross‑border data; diversification reduces concentration risk.

Public policy on online advertising

Governments increasingly set rules on targeting, transparency and political ads; GDPR (2018) and the EU DSA/DMA (in force 2024) sharply raised compliance expectations. Stricter norms limit personalization levers and can reduce targeting effectiveness, while global digital ad spend was about $517 billion in 2023. Criteo must engage in policy dialogue and early adaptation to gain competitive advantage.

- Policy: DSA/DMA 2024

- Risk: reduced personalization

- Opportunity: first-mover compliance

- Market: $517B digital ads 2023

Subsidies and innovation incentives

Grants and tax credits for AI, cloud and R&D (Horizon Europe €95.5bn 2021–27; US CHIPS Act $52.7bn) can cut effective project costs—R&D incentives in many markets lower cash tax by roughly 10–30%—while public‑private programs accelerate Criteo product roadmaps through co‑funding and pilots.

- Local presence & compliance determine eligibility

- Choose hubs (EU, US, Israel) to maximize returns

- Leverage co‑funding to shorten time‑to‑market

Regulation, taxes and concentrated cloud power force cross-border digital strategy shifts

Cross‑border rules force regional data routing: GDPR fines up to €20m/4% turnover, China PIPL penalties up to RMB50m/5%, CLOUD Act affects access; EU‑US Data Privacy Framework adopted 2023.

Tax and levies squeeze margins: OECD Pillar Two 15% (137 jurisdictions), unilateral DSTs; global digital ad spend $517B (2023).

Platform risk high: AWS ~32%, Azure ~23%, GCP ~11% (2024 IDC); US export controls and grants (CHIPS $52.7B, Horizon €95.5B) shape strategy.

| Metric | Value |

|---|---|

| GDPR fine | €20M / 4% |

| Pillar Two | 15% |

| Cloud share (2024) | AWS32% AZ23% GCP11% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Criteo across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Each section uses current data and trend-backed subpoints and forward-looking insights to help executives, consultants, and investors identify regulatory, market and tech-driven threats and opportunities.

A concise, visually segmented Criteo PESTLE summary that distills external risks and market drivers for quick reference in meetings, easily shareable and editable for region- or team-specific planning.

Economic factors

Ad spend cyclicality

Advertising budgets track consumer demand and GDP: WARC reported global adspend at about $729bn in 2023 while IMF projected ~3.0% global GDP growth for 2024, linking budgets to macro trends. Downturns shift spend to measurable performance channels where Criteo competes, increasing share for ROI-focused buys. Recovery phases reward measurable incrementality and flexible cross-vertical offerings help smooth cyclical volatility.

Retail media monetization

Retailers are pursuing new profit pools from retail media as the channel scales—Amazon ad revenue topped about 46 billion dollars in 2023, underscoring opportunity for others. Criteo’s Commerce Media can capture this shift by activating first-party data across retailer inventories. Revenue potential rises with retailer adoption and shopper traffic; strong measurement and ROI drive repeat advertiser spend and lift lifetime value.

Currency and inflation pressures

Multi-currency revenues expose Criteo to FX volatility across major corridors, pressuring reported top-line when currencies weaken versus the euro. Rising inflation lifts cloud, talent and traffic acquisition costs, squeezing CPA and margin profiles. Contract indexation and dynamic pricing models help preserve margins by passing cost increases to clients. Active hedging programs can dampen short-term earnings swings and stabilize cash flow.

Competition with walled gardens

Large platforms like Google and Meta captured roughly 60% of global digital ad spend in 2024 (eMarketer), creating budget and data advantages that pressure open-internet players; Criteo must demonstrate comparable ROI from its open-web inventory. Criteo offsets concentration via deep publisher and retailer partnerships and differentiated multi-touch attribution to protect and grow share.

- Platforms: ~60% ad share 2024

- Counter: publisher/retailer partnerships

- Edge: differentiated attribution strengthens share

SMB and mid-market dynamics

- turnkey-solutions

- low-touch-onboarding

- self-serve-automation

- payment-risk-management

Regulation, taxes and concentrated cloud power force cross-border digital strategy shifts

Ad budgets track GDP and demand: global adspend ~$729bn (WARC 2023) while ROI channels gain in downturns, favoring Criteo’s performance stack.

Retail media scales—Amazon ads ~$46bn (2023); Criteo can capture retailer-first‑party opportunities via Commerce Media.

FY2023 revenue ~€1.46B; FX, inflation and ~60% platform concentration (eMarketer 2024) pressure margins and pricing power.

| Metric | Value | Source/Year |

|---|---|---|

| Global adspend | $729bn | WARC 2023 |

| Amazon ad revenue | $46bn | 2023 |

| Criteo revenue | €1.46B | FY2023 |

| Platform share | ~60% | eMarketer 2024 |

Full Version Awaits

Criteo PESTLE Analysis

The preview shown here is the exact Criteo PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real snapshot of the product you’re buying, delivered exactly as shown with no placeholders. The layout, content, and structure visible here are the final version available for immediate download after payment.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Criteo reveals how political regulation, economic shifts, and rapid adtech innovation are reshaping its growth prospects. Actionable insights identify regulatory risks, privacy trends, and technological opportunities for investors and strategists. Purchase the full report to get the complete, editable analysis and strategic recommendations instantly.

Political factors

Data sovereignty and localization

Cross-border ad delivery must respect national localization rules, with the EU GDPR (2018) allowing fines up to €20 million or 4% of global turnover and the US CLOUD Act (2018) altering cross‑border access; China’s PIPL (effective 2021) permits penalties up to RMB 50 million or 5% of revenue. Divergent EU, US and APAC regimes force Criteo to route and store user data regionally. Aligning infrastructure to sovereign requirements raises capex/opex but unlocks market access, while sudden government scrutiny can tighten controls quickly, increasing latency and limiting scale.

Digital taxation and tech levies

Digital services taxes and the OECD Pillar Two global minimum tax (15% adopted by 137 Inclusive Framework jurisdictions) raise effective tax rates and pressure Criteo's margins. Multi-country operations increase compliance complexity and dispute risk across jurisdictions with unilateral DSTs. Pricing and agile financial planning are required to pass through costs amid ongoing policy volatility.

Trade relations and platform access

Geopolitical tensions can curtail partnerships, APIs or cloud vendors—AWS (~32%), Azure (~23%) and GCP (~11%) concentration (2024 IDC) raises platform-access risk if providers face sanctions. US export controls since 2022 restrict high-end AI chips to China, limiting tooling and talent mobility. Market entry hinges on stable trade channels and the EU‑US Data Privacy Framework (adopted 2023) for cross‑border data; diversification reduces concentration risk.

Public policy on online advertising

Governments increasingly set rules on targeting, transparency and political ads; GDPR (2018) and the EU DSA/DMA (in force 2024) sharply raised compliance expectations. Stricter norms limit personalization levers and can reduce targeting effectiveness, while global digital ad spend was about $517 billion in 2023. Criteo must engage in policy dialogue and early adaptation to gain competitive advantage.

- Policy: DSA/DMA 2024

- Risk: reduced personalization

- Opportunity: first-mover compliance

- Market: $517B digital ads 2023

Subsidies and innovation incentives

Grants and tax credits for AI, cloud and R&D (Horizon Europe €95.5bn 2021–27; US CHIPS Act $52.7bn) can cut effective project costs—R&D incentives in many markets lower cash tax by roughly 10–30%—while public‑private programs accelerate Criteo product roadmaps through co‑funding and pilots.

- Local presence & compliance determine eligibility

- Choose hubs (EU, US, Israel) to maximize returns

- Leverage co‑funding to shorten time‑to‑market

Regulation, taxes and concentrated cloud power force cross-border digital strategy shifts

Cross‑border rules force regional data routing: GDPR fines up to €20m/4% turnover, China PIPL penalties up to RMB50m/5%, CLOUD Act affects access; EU‑US Data Privacy Framework adopted 2023.

Tax and levies squeeze margins: OECD Pillar Two 15% (137 jurisdictions), unilateral DSTs; global digital ad spend $517B (2023).

Platform risk high: AWS ~32%, Azure ~23%, GCP ~11% (2024 IDC); US export controls and grants (CHIPS $52.7B, Horizon €95.5B) shape strategy.

| Metric | Value |

|---|---|

| GDPR fine | €20M / 4% |

| Pillar Two | 15% |

| Cloud share (2024) | AWS32% AZ23% GCP11% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Criteo across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Each section uses current data and trend-backed subpoints and forward-looking insights to help executives, consultants, and investors identify regulatory, market and tech-driven threats and opportunities.

A concise, visually segmented Criteo PESTLE summary that distills external risks and market drivers for quick reference in meetings, easily shareable and editable for region- or team-specific planning.

Economic factors

Ad spend cyclicality

Advertising budgets track consumer demand and GDP: WARC reported global adspend at about $729bn in 2023 while IMF projected ~3.0% global GDP growth for 2024, linking budgets to macro trends. Downturns shift spend to measurable performance channels where Criteo competes, increasing share for ROI-focused buys. Recovery phases reward measurable incrementality and flexible cross-vertical offerings help smooth cyclical volatility.

Retail media monetization

Retailers are pursuing new profit pools from retail media as the channel scales—Amazon ad revenue topped about 46 billion dollars in 2023, underscoring opportunity for others. Criteo’s Commerce Media can capture this shift by activating first-party data across retailer inventories. Revenue potential rises with retailer adoption and shopper traffic; strong measurement and ROI drive repeat advertiser spend and lift lifetime value.

Currency and inflation pressures

Multi-currency revenues expose Criteo to FX volatility across major corridors, pressuring reported top-line when currencies weaken versus the euro. Rising inflation lifts cloud, talent and traffic acquisition costs, squeezing CPA and margin profiles. Contract indexation and dynamic pricing models help preserve margins by passing cost increases to clients. Active hedging programs can dampen short-term earnings swings and stabilize cash flow.

Competition with walled gardens

Large platforms like Google and Meta captured roughly 60% of global digital ad spend in 2024 (eMarketer), creating budget and data advantages that pressure open-internet players; Criteo must demonstrate comparable ROI from its open-web inventory. Criteo offsets concentration via deep publisher and retailer partnerships and differentiated multi-touch attribution to protect and grow share.

- Platforms: ~60% ad share 2024

- Counter: publisher/retailer partnerships

- Edge: differentiated attribution strengthens share

SMB and mid-market dynamics

- turnkey-solutions

- low-touch-onboarding

- self-serve-automation

- payment-risk-management

Regulation, taxes and concentrated cloud power force cross-border digital strategy shifts

Ad budgets track GDP and demand: global adspend ~$729bn (WARC 2023) while ROI channels gain in downturns, favoring Criteo’s performance stack.

Retail media scales—Amazon ads ~$46bn (2023); Criteo can capture retailer-first‑party opportunities via Commerce Media.

FY2023 revenue ~€1.46B; FX, inflation and ~60% platform concentration (eMarketer 2024) pressure margins and pricing power.

| Metric | Value | Source/Year |

|---|---|---|

| Global adspend | $729bn | WARC 2023 |

| Amazon ad revenue | $46bn | 2023 |

| Criteo revenue | €1.46B | FY2023 |

| Platform share | ~60% | eMarketer 2024 |

Full Version Awaits

Criteo PESTLE Analysis

The preview shown here is the exact Criteo PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real snapshot of the product you’re buying, delivered exactly as shown with no placeholders. The layout, content, and structure visible here are the final version available for immediate download after payment.