CrossFirst Bankshares Porter's Five Forces Analysis

Don't Miss the Bigger Picture

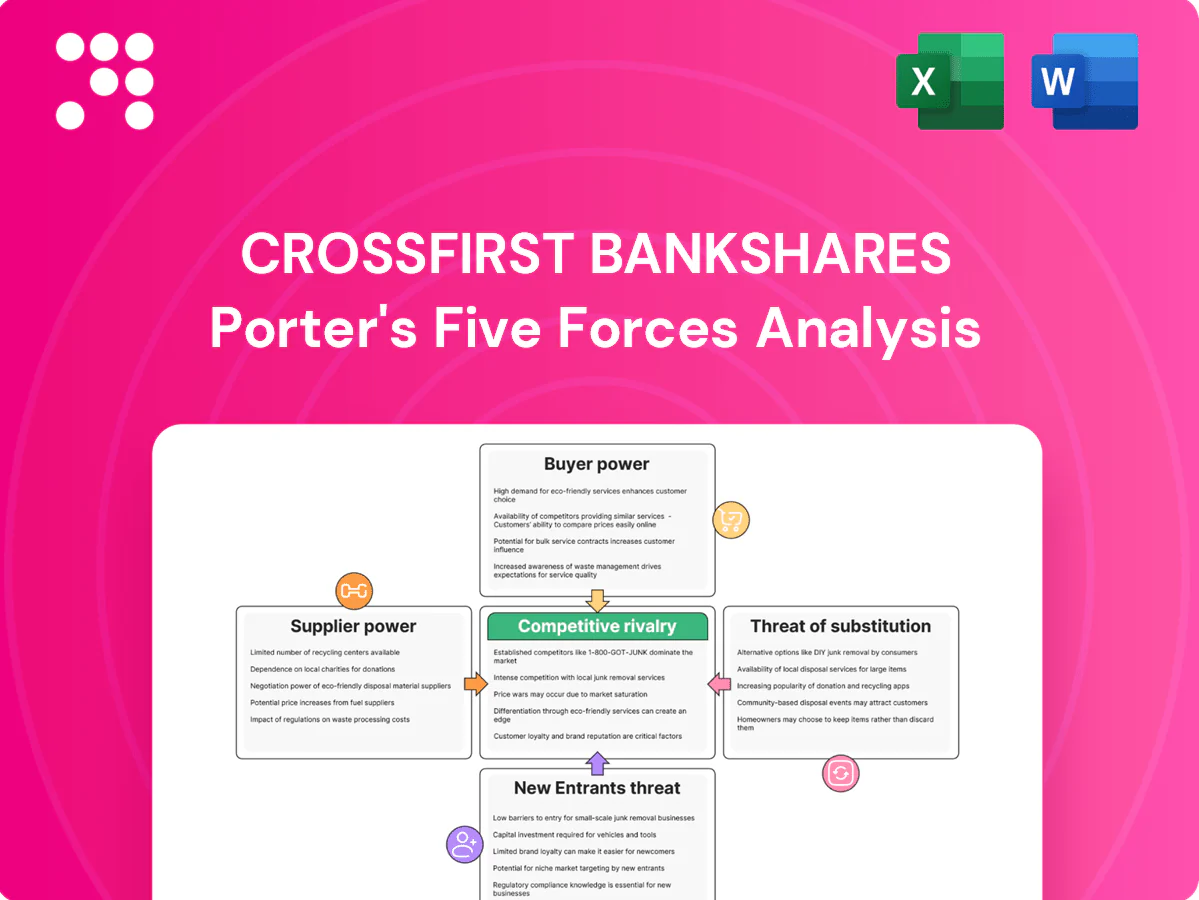

CrossFirst Bankshares faces moderate buyer power, intense regional competition, and rising fintech substitution while regulatory and capital requirements create structural barriers to entry; supplier influence remains limited. This snapshot highlights strategic pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Core funding concentration

Depositors are CrossFirst’s primary suppliers of funding; as of 2024 the bank reported approximately $4.6 billion in core deposits, making concentration in large commercial accounts a notable risk. If a few clients hold sizable balances (top 10 commercial accounts ~15% of deposits in 2024), they can press for higher rates or enhanced services. Diversifying retail and small-business deposits helps dilute supplier power, while CrossFirst’s relationship banking stabilizes core funding but demands competitive pricing.

Wholesale and capital market reliance

Access to FHLB advances, brokered CDs and debt markets proved vital during 2024 liquidity cycles, with these wholesale providers able to reprice or tighten terms rapidly, increasing supplier leverage. Maintaining strong liquidity buffers and diversified funding lines reduces dependence on volatile wholesale channels. CrossFirst’s cost and access to these markets are directly tied to its credit ratings and balance sheet strength.

Technology and fintech vendors

Core processors, digital banking platforms and payments rails are highly concentrated—Fiserv, FIS and Jack Henry together account for roughly three-quarters of US core market—giving vendors strong negotiation leverage. Switching cores is costly and risky, often involving multi-year contracts and migration costs that run into millions. Robust vendor risk management, multi-vendor architectures and co-development or scale commitments can reduce dependency and secure better commercial terms.

Talent and relationship bankers

Experienced lenders and private bankers serve as critical suppliers of deal flow and client relationships, and tight 2024 labor markets amplified their bargaining power through higher incentive demands and mobility. CrossFirst relies on culture, equity incentives, and clear career paths to retain producers, but overreliance on star bankers elevates key-person risk and concentration of client revenues.

- Experienced bankers = primary deal-supply

- Tight 2024 labor market increases pay demands

- Culture & equity aid retention

- Star-producer reliance = key-person risk

Data, compliance, and cloud providers

Data, compliance, and cloud providers (regtech, AML/KYC, cloud infra) are necessary and relatively concentrated, with AWS 32%, Azure 22%, GCP 11% of global cloud IaaS in 2024, limiting switching and increasing compliance spend. Long-term contracts and integration costs raise vendor power; internal build and open APIs can rebalance leverage.

- Regtech

- AML/KYC

- Cloud infra

High risk: $4.6B 75% vendor, cloud 32/22/11%

Depositors (core deposits $4.6B in 2024; top-10 commercial ~15%) and wholesale lenders (FHLB, brokered CDs) hold high leverage; core/vendor concentration (Fiserv/FIS/Jack Henry ~75%) and cloud share (AWS 32%, Azure 22%, GCP 11% in 2024) increase supplier power, while tight 2024 labor markets raise retention costs for bankers.

| Supplier | 2024 Metric |

|---|---|

| Core deposits | $4.6B |

| Top-10 commercial | ~15% |

| Core vendors | ~75% |

| AWS/Azure/GCP | 32%/22%/11% |

What is included in the product

Tailored Porter's Five Forces analysis for CrossFirst Bankshares that uncovers competitive dynamics, buyer and supplier power, entry and substitute risks, and identifies disruptive threats and strategic levers to protect market share and profitability.

A concise one-sheet Porter’s Five Forces for CrossFirst Bankshares—clarifies competitive pressures, regulatory risk, and deposit/credit threats for faster, more confident strategic decisions.

Customers Bargaining Power

Rate sensitivity of business clients

Commercial borrowers and depositors actively shop rates and terms; with the federal funds rate at 5.25–5.50% through much of 2024, rate sensitivity intensified and clients demanded sharper pricing and fee concessions. In rising-rate cycles borrowers push hardest on loan spreads while depositors seek higher yields. Treasury-management bundling (cash mgmt, sweeps, ACH) often offsets rate concessions by increasing revenue per relationship. Strong relationship depth reduces pure price shopping and lowers churn.

Low switching costs digitally

Modern API-driven onboarding and open-banking tools make switching faster, and in 2024 roughly 60% of businesses multihome across banks for lending, payments and deposits, raising buyer leverage for basic services. CrossFirst reduces churn with differentiated service levels and specialized credit expertise that increase switching frictions. Superior UX and ERP/accounting integrations can create strong client lock-in despite low digital switching costs.

Client concentration risk

Middle-market portfolios can show meaningful single-client exposures, giving large clients leverage to negotiate covenants, fees, and ancillary services. Proactive portfolio diversification—shifting concentration across industries and geographies—reduces this bargaining power. Cross-selling wealth and private banking deepens client relationships and lowers churn by embedding services beyond lending.

Demand for tailored solutions

Professional and private banking clients increasingly demand bespoke credit structures and white-glove concierge service, which raises per-client servicing costs and can compress margins unless priced appropriately. When premium experiences are delivered consistently, they create pricing power and client stickiness, shifting bargaining power back to the bank. Robust SLAs and enhanced advisory capabilities become key differentiators in retaining high-value customers.

- Higher servicing cost → margin pressure

- Consistent premium delivery → pricing power

- SLAs & advisory = competitive moat

Transparency and comparison tools

Online comparison sites and fintech marketplaces in 2024 give borrowers and depositors clear rate and fee visibility, increasing price sensitivity and intensifying competition for CrossFirst Bankshares on loans and deposits. Educational content and advisory positioning can reframe choices toward service and value, reducing pure price churn. For complex commercial deals, CrossFirst's reputation and fast responsiveness remain decisive.

- Transparency: higher price competition

- Advisory: shifts focus to value

- Reputation: key in complex deals

Higher rates drive multihoming and buyer leverage; treasury bundling restores pricing power

Commercial customers intensified rate shopping with the fed funds rate at 5.25–5.50% in 2024, boosting price sensitivity; roughly 60% of businesses multihome across banks, increasing buyer leverage. Treasury-management bundling and specialized advisory reduce churn and restore pricing power for CrossFirst when consistently delivered. Large single-client exposures raise negotiation leverage unless diversification and cross-sell are executed.

| Metric | 2024 | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Higher price sensitivity |

| Multihoming | ~60% businesses | Increases bargaining power |

| Premium service | — | Restores pricing power |

Full Version Awaits

CrossFirst Bankshares Porter's Five Forces Analysis

This preview is the exact CrossFirst Bankshares Porter's Five Forces analysis you’ll receive after purchase, containing a full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry. The file is professionally written, fully formatted, and ready for immediate download with no placeholders or changes required.

Don't Miss the Bigger Picture

CrossFirst Bankshares faces moderate buyer power, intense regional competition, and rising fintech substitution while regulatory and capital requirements create structural barriers to entry; supplier influence remains limited. This snapshot highlights strategic pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Core funding concentration

Depositors are CrossFirst’s primary suppliers of funding; as of 2024 the bank reported approximately $4.6 billion in core deposits, making concentration in large commercial accounts a notable risk. If a few clients hold sizable balances (top 10 commercial accounts ~15% of deposits in 2024), they can press for higher rates or enhanced services. Diversifying retail and small-business deposits helps dilute supplier power, while CrossFirst’s relationship banking stabilizes core funding but demands competitive pricing.

Wholesale and capital market reliance

Access to FHLB advances, brokered CDs and debt markets proved vital during 2024 liquidity cycles, with these wholesale providers able to reprice or tighten terms rapidly, increasing supplier leverage. Maintaining strong liquidity buffers and diversified funding lines reduces dependence on volatile wholesale channels. CrossFirst’s cost and access to these markets are directly tied to its credit ratings and balance sheet strength.

Technology and fintech vendors

Core processors, digital banking platforms and payments rails are highly concentrated—Fiserv, FIS and Jack Henry together account for roughly three-quarters of US core market—giving vendors strong negotiation leverage. Switching cores is costly and risky, often involving multi-year contracts and migration costs that run into millions. Robust vendor risk management, multi-vendor architectures and co-development or scale commitments can reduce dependency and secure better commercial terms.

Talent and relationship bankers

Experienced lenders and private bankers serve as critical suppliers of deal flow and client relationships, and tight 2024 labor markets amplified their bargaining power through higher incentive demands and mobility. CrossFirst relies on culture, equity incentives, and clear career paths to retain producers, but overreliance on star bankers elevates key-person risk and concentration of client revenues.

- Experienced bankers = primary deal-supply

- Tight 2024 labor market increases pay demands

- Culture & equity aid retention

- Star-producer reliance = key-person risk

Data, compliance, and cloud providers

Data, compliance, and cloud providers (regtech, AML/KYC, cloud infra) are necessary and relatively concentrated, with AWS 32%, Azure 22%, GCP 11% of global cloud IaaS in 2024, limiting switching and increasing compliance spend. Long-term contracts and integration costs raise vendor power; internal build and open APIs can rebalance leverage.

- Regtech

- AML/KYC

- Cloud infra

High risk: $4.6B 75% vendor, cloud 32/22/11%

Depositors (core deposits $4.6B in 2024; top-10 commercial ~15%) and wholesale lenders (FHLB, brokered CDs) hold high leverage; core/vendor concentration (Fiserv/FIS/Jack Henry ~75%) and cloud share (AWS 32%, Azure 22%, GCP 11% in 2024) increase supplier power, while tight 2024 labor markets raise retention costs for bankers.

| Supplier | 2024 Metric |

|---|---|

| Core deposits | $4.6B |

| Top-10 commercial | ~15% |

| Core vendors | ~75% |

| AWS/Azure/GCP | 32%/22%/11% |

What is included in the product

Tailored Porter's Five Forces analysis for CrossFirst Bankshares that uncovers competitive dynamics, buyer and supplier power, entry and substitute risks, and identifies disruptive threats and strategic levers to protect market share and profitability.

A concise one-sheet Porter’s Five Forces for CrossFirst Bankshares—clarifies competitive pressures, regulatory risk, and deposit/credit threats for faster, more confident strategic decisions.

Customers Bargaining Power

Rate sensitivity of business clients

Commercial borrowers and depositors actively shop rates and terms; with the federal funds rate at 5.25–5.50% through much of 2024, rate sensitivity intensified and clients demanded sharper pricing and fee concessions. In rising-rate cycles borrowers push hardest on loan spreads while depositors seek higher yields. Treasury-management bundling (cash mgmt, sweeps, ACH) often offsets rate concessions by increasing revenue per relationship. Strong relationship depth reduces pure price shopping and lowers churn.

Low switching costs digitally

Modern API-driven onboarding and open-banking tools make switching faster, and in 2024 roughly 60% of businesses multihome across banks for lending, payments and deposits, raising buyer leverage for basic services. CrossFirst reduces churn with differentiated service levels and specialized credit expertise that increase switching frictions. Superior UX and ERP/accounting integrations can create strong client lock-in despite low digital switching costs.

Client concentration risk

Middle-market portfolios can show meaningful single-client exposures, giving large clients leverage to negotiate covenants, fees, and ancillary services. Proactive portfolio diversification—shifting concentration across industries and geographies—reduces this bargaining power. Cross-selling wealth and private banking deepens client relationships and lowers churn by embedding services beyond lending.

Demand for tailored solutions

Professional and private banking clients increasingly demand bespoke credit structures and white-glove concierge service, which raises per-client servicing costs and can compress margins unless priced appropriately. When premium experiences are delivered consistently, they create pricing power and client stickiness, shifting bargaining power back to the bank. Robust SLAs and enhanced advisory capabilities become key differentiators in retaining high-value customers.

- Higher servicing cost → margin pressure

- Consistent premium delivery → pricing power

- SLAs & advisory = competitive moat

Transparency and comparison tools

Online comparison sites and fintech marketplaces in 2024 give borrowers and depositors clear rate and fee visibility, increasing price sensitivity and intensifying competition for CrossFirst Bankshares on loans and deposits. Educational content and advisory positioning can reframe choices toward service and value, reducing pure price churn. For complex commercial deals, CrossFirst's reputation and fast responsiveness remain decisive.

- Transparency: higher price competition

- Advisory: shifts focus to value

- Reputation: key in complex deals

Higher rates drive multihoming and buyer leverage; treasury bundling restores pricing power

Commercial customers intensified rate shopping with the fed funds rate at 5.25–5.50% in 2024, boosting price sensitivity; roughly 60% of businesses multihome across banks, increasing buyer leverage. Treasury-management bundling and specialized advisory reduce churn and restore pricing power for CrossFirst when consistently delivered. Large single-client exposures raise negotiation leverage unless diversification and cross-sell are executed.

| Metric | 2024 | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Higher price sensitivity |

| Multihoming | ~60% businesses | Increases bargaining power |

| Premium service | — | Restores pricing power |

Full Version Awaits

CrossFirst Bankshares Porter's Five Forces Analysis

This preview is the exact CrossFirst Bankshares Porter's Five Forces analysis you’ll receive after purchase, containing a full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry. The file is professionally written, fully formatted, and ready for immediate download with no placeholders or changes required.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

CrossFirst Bankshares faces moderate buyer power, intense regional competition, and rising fintech substitution while regulatory and capital requirements create structural barriers to entry; supplier influence remains limited. This snapshot highlights strategic pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Core funding concentration

Depositors are CrossFirst’s primary suppliers of funding; as of 2024 the bank reported approximately $4.6 billion in core deposits, making concentration in large commercial accounts a notable risk. If a few clients hold sizable balances (top 10 commercial accounts ~15% of deposits in 2024), they can press for higher rates or enhanced services. Diversifying retail and small-business deposits helps dilute supplier power, while CrossFirst’s relationship banking stabilizes core funding but demands competitive pricing.

Wholesale and capital market reliance

Access to FHLB advances, brokered CDs and debt markets proved vital during 2024 liquidity cycles, with these wholesale providers able to reprice or tighten terms rapidly, increasing supplier leverage. Maintaining strong liquidity buffers and diversified funding lines reduces dependence on volatile wholesale channels. CrossFirst’s cost and access to these markets are directly tied to its credit ratings and balance sheet strength.

Technology and fintech vendors

Core processors, digital banking platforms and payments rails are highly concentrated—Fiserv, FIS and Jack Henry together account for roughly three-quarters of US core market—giving vendors strong negotiation leverage. Switching cores is costly and risky, often involving multi-year contracts and migration costs that run into millions. Robust vendor risk management, multi-vendor architectures and co-development or scale commitments can reduce dependency and secure better commercial terms.

Talent and relationship bankers

Experienced lenders and private bankers serve as critical suppliers of deal flow and client relationships, and tight 2024 labor markets amplified their bargaining power through higher incentive demands and mobility. CrossFirst relies on culture, equity incentives, and clear career paths to retain producers, but overreliance on star bankers elevates key-person risk and concentration of client revenues.

- Experienced bankers = primary deal-supply

- Tight 2024 labor market increases pay demands

- Culture & equity aid retention

- Star-producer reliance = key-person risk

Data, compliance, and cloud providers

Data, compliance, and cloud providers (regtech, AML/KYC, cloud infra) are necessary and relatively concentrated, with AWS 32%, Azure 22%, GCP 11% of global cloud IaaS in 2024, limiting switching and increasing compliance spend. Long-term contracts and integration costs raise vendor power; internal build and open APIs can rebalance leverage.

- Regtech

- AML/KYC

- Cloud infra

High risk: $4.6B 75% vendor, cloud 32/22/11%

Depositors (core deposits $4.6B in 2024; top-10 commercial ~15%) and wholesale lenders (FHLB, brokered CDs) hold high leverage; core/vendor concentration (Fiserv/FIS/Jack Henry ~75%) and cloud share (AWS 32%, Azure 22%, GCP 11% in 2024) increase supplier power, while tight 2024 labor markets raise retention costs for bankers.

| Supplier | 2024 Metric |

|---|---|

| Core deposits | $4.6B |

| Top-10 commercial | ~15% |

| Core vendors | ~75% |

| AWS/Azure/GCP | 32%/22%/11% |

What is included in the product

Tailored Porter's Five Forces analysis for CrossFirst Bankshares that uncovers competitive dynamics, buyer and supplier power, entry and substitute risks, and identifies disruptive threats and strategic levers to protect market share and profitability.

A concise one-sheet Porter’s Five Forces for CrossFirst Bankshares—clarifies competitive pressures, regulatory risk, and deposit/credit threats for faster, more confident strategic decisions.

Customers Bargaining Power

Rate sensitivity of business clients

Commercial borrowers and depositors actively shop rates and terms; with the federal funds rate at 5.25–5.50% through much of 2024, rate sensitivity intensified and clients demanded sharper pricing and fee concessions. In rising-rate cycles borrowers push hardest on loan spreads while depositors seek higher yields. Treasury-management bundling (cash mgmt, sweeps, ACH) often offsets rate concessions by increasing revenue per relationship. Strong relationship depth reduces pure price shopping and lowers churn.

Low switching costs digitally

Modern API-driven onboarding and open-banking tools make switching faster, and in 2024 roughly 60% of businesses multihome across banks for lending, payments and deposits, raising buyer leverage for basic services. CrossFirst reduces churn with differentiated service levels and specialized credit expertise that increase switching frictions. Superior UX and ERP/accounting integrations can create strong client lock-in despite low digital switching costs.

Client concentration risk

Middle-market portfolios can show meaningful single-client exposures, giving large clients leverage to negotiate covenants, fees, and ancillary services. Proactive portfolio diversification—shifting concentration across industries and geographies—reduces this bargaining power. Cross-selling wealth and private banking deepens client relationships and lowers churn by embedding services beyond lending.

Demand for tailored solutions

Professional and private banking clients increasingly demand bespoke credit structures and white-glove concierge service, which raises per-client servicing costs and can compress margins unless priced appropriately. When premium experiences are delivered consistently, they create pricing power and client stickiness, shifting bargaining power back to the bank. Robust SLAs and enhanced advisory capabilities become key differentiators in retaining high-value customers.

- Higher servicing cost → margin pressure

- Consistent premium delivery → pricing power

- SLAs & advisory = competitive moat

Transparency and comparison tools

Online comparison sites and fintech marketplaces in 2024 give borrowers and depositors clear rate and fee visibility, increasing price sensitivity and intensifying competition for CrossFirst Bankshares on loans and deposits. Educational content and advisory positioning can reframe choices toward service and value, reducing pure price churn. For complex commercial deals, CrossFirst's reputation and fast responsiveness remain decisive.

- Transparency: higher price competition

- Advisory: shifts focus to value

- Reputation: key in complex deals

Higher rates drive multihoming and buyer leverage; treasury bundling restores pricing power

Commercial customers intensified rate shopping with the fed funds rate at 5.25–5.50% in 2024, boosting price sensitivity; roughly 60% of businesses multihome across banks, increasing buyer leverage. Treasury-management bundling and specialized advisory reduce churn and restore pricing power for CrossFirst when consistently delivered. Large single-client exposures raise negotiation leverage unless diversification and cross-sell are executed.

| Metric | 2024 | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Higher price sensitivity |

| Multihoming | ~60% businesses | Increases bargaining power |

| Premium service | — | Restores pricing power |

Full Version Awaits

CrossFirst Bankshares Porter's Five Forces Analysis

This preview is the exact CrossFirst Bankshares Porter's Five Forces analysis you’ll receive after purchase, containing a full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry. The file is professionally written, fully formatted, and ready for immediate download with no placeholders or changes required.