CrowdStrike Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

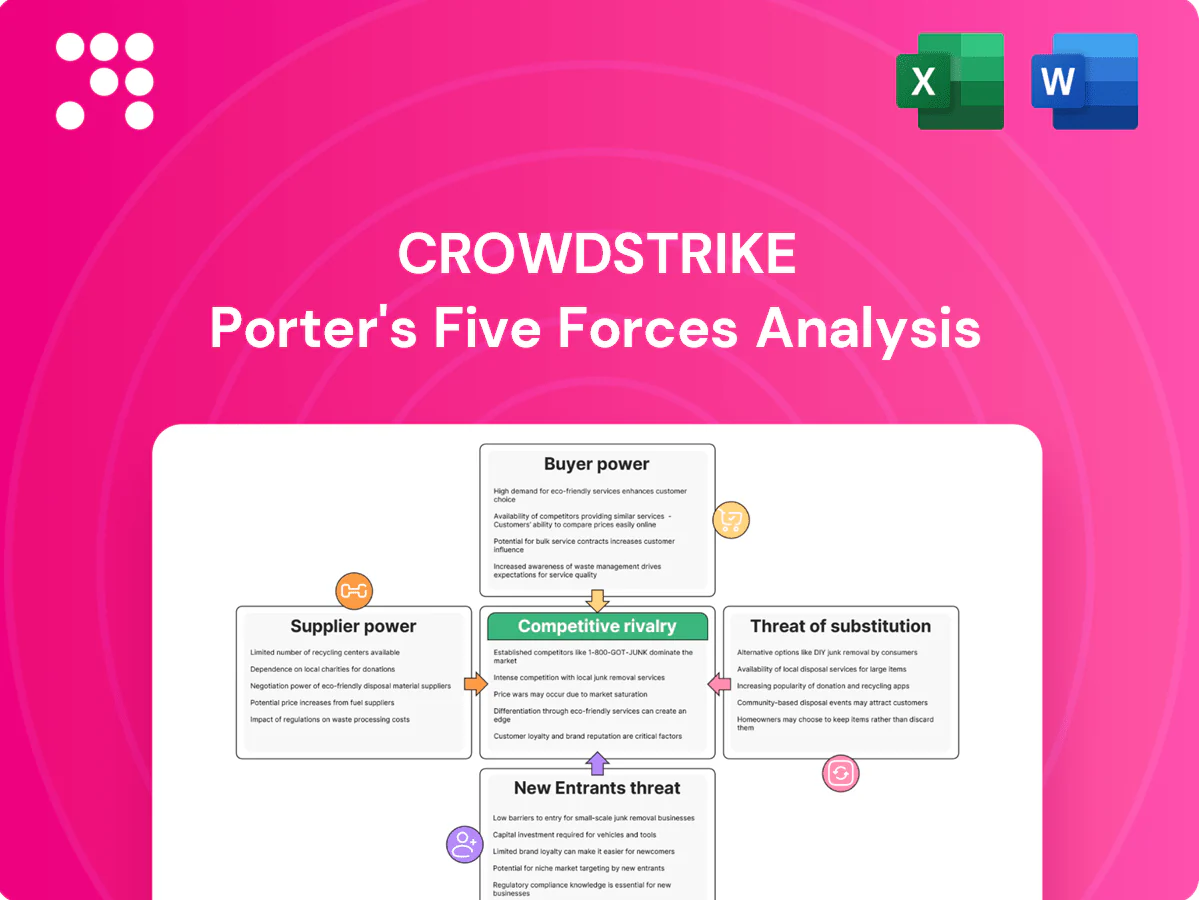

CrowdStrike faces intense competitive rivalry amid rapid innovation and scaling incumbents, while supplier influence is limited and buyer expectations for integrated, cloud-native security raise switching dynamics; barriers to entry are moderate but high R&D and data network effects protect incumbents. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CrowdStrike’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on hyperscale clouds

CrowdStrike depends on public hyperscale clouds for compute, storage and global delivery of Falcon, with FY2024 revenue of about 2.07 billion USD highlighting scale and exposure. Hyperscalers (AWS ~32%, Azure ~24%, GCP ~11% share in 2024 IaaS) can influence pricing, service levels and egress fees, creating supplier leverage. Multi-cloud architectures and long-term contracts mitigate risk, but major outages or policy shifts at a hyperscaler could disrupt continuity and compress margins.

Scarcity of elite security talent

Advanced threat researchers, data scientists and reverse engineers are critical inputs; ISC2 reported a global cybersecurity workforce shortfall of about 3.4 million in 2024, driving wage inflation and higher retention costs. The labor market and specialized contractors thus hold strong bargaining power. CrowdStrike’s brand and hiring investments improve attraction but do not erase scarcity-driven supplier leverage.

Third-party threat intel and data feeds

Supplemental third-party intelligence and OS/app telemetry partnerships improve detection quality and enrich context; niche feeds with unique indicators can command pricing power. Some providers retain leverage due to differentiated, hard-to-replicate signals. CrowdStrike’s proprietary scale—20,000+ customers and billions of daily telemetry events—reduces dependence on any single feed. Diversified supplier contracts further lower switching risk and supplier power.

Chipsets, device ecosystems, and OS vendors

Endpoint agents must interoperate with CPUs, firmware, and operating systems, with Windows holding ~76% desktop share in 2024 and Android ~71% of mobile—making platform compatibility critical. API access, driver models, and policy shifts by platform owners can materially affect detection and performance, and platform gatekeepers often dictate timelines despite open standards. Close partnerships and early-access programs with OS and chipset vendors reduce integration lag and moderate supplier influence.

- Platform share: Windows ~76% (2024)

- Mobile OS: Android ~71% (2024)

- Risk: API/policy changes can delay features

- Mitigation: early-access/partnerships

Channel and MSSP alliances

Channel and MSSP alliances—value-added resellers, distributors and managed security providers—extend CrowdStrike reach, while top partners can extract favorable terms, marketing funds or deal-registration priority.

- FY2024: over 20,000 customers reduces channel reliance

- Top-channel leverage varies by region and segment

- Direct enterprise sales lower supplier power

Hyperscaler leverage (AWS 32%) and 3.4M cyber talent gap

CrowdStrike faces supplier leverage from hyperscalers (FY2024 revenue ~$2.07B; IaaS: AWS ~32%, Azure ~24%, GCP ~11%), a global cyber workforce shortfall ~3.4M (2024) driving wage pressure, reliance on niche intelligence feeds, and platform gatekeepers (Windows ~76%, Android ~71%, 20,000+ customers reduces single-supplier risk).

| Metric | 2024 |

|---|---|

| Revenue (FY2024) | $2.07B |

| Customers | 20,000+ |

| IaaS share | AWS32%/Azure24%/GCP11% |

| Workforce gap | 3.4M |

| OS share | Windows76%/Android71% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to CrowdStrike, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and disruptive/emerging risks to market share. Provides strategic commentary on pricing power, barriers to entry and defensive advantages to inform investors, strategists and academics.

Clear, one-sheet Porter's Five Forces for CrowdStrike that visualizes competitive pressure with an editable radar chart—perfect for quick, boardroom-ready decisions. No macros, easy integration into decks or broader dashboards.

Customers Bargaining Power

Large enterprise procurement leverage

Global enterprises and governments press hard on price and terms, leveraging scale, multi-year commitments and complex compliance needs to increase bargaining power; competitive bake-offs among top vendors amplify this pressure. CrowdStrike entered FY2024 with 20,000+ customers, $2.18B revenue and ~$2.03B ARR, countering with platform breadth and documented ROI to defend pricing and win multi-year deals.

High switching costs from agent footprint

Deploying and managing CrowdStrike agents across thousands of endpoints creates operational stickiness, given the scale of deployments across over 19,000 customers in 2024 and millions of protected devices. Integration into SOC workflows, SIEMs and automation platforms amplifies lock-in by embedding processes and alerts. Longitudinal telemetry, detection tuning and playbook customizations further raise switching barriers, lowering buyer power post-deployment despite pre-sale leverage; dollar-based net retention remained >120% in 2024.

Abundant credible alternatives

Customers compare Microsoft, Palo Alto Networks, CrowdStrike and SentinelOne—Gartner 2024 lists them as leading EPP vendors—so perceived substitutability rises as vendors assert feature parity and bundle suites. Proof-of-value trials force competition on efficacy and total cost, shortening sales cycles. Buyers leverage this landscape to extract deeper discounts and tighter SLAs. Negotiations increasingly hinge on measurable ROI and deployment metrics.

Outcome-critical, not purely price-driven

Security failures carry multi-million-dollar loss potential, so buyers prioritize detection efficacy, speed, and incident response over unit price; this outcome-critical stance tempers customer bargaining power. CrowdStrike reported FY2024 revenue of $3.45B and serves over 23,000 customers, allowing it to sustain premium pricing supported by large-scale telemetry and efficacy data.

- High stakes reduce price sensitivity

- FY2024 revenue: $3.45B; >23,000 customers

- Strong efficacy data supports premium pricing

Multi-year SaaS and modular upsell

CrowdStrike sells multi-year SaaS agreements with modular Falcon add-ons, using expansion-led pricing to trade initial discounts for higher lifetime value; renewal checkpoints and competitive evaluations give buyers periodic leverage, and land-and-expand dynamics dilute but do not eliminate buyer bargaining power.

- FY2024 revenue about $2.06B

- ARR ~ $3.45B

- Net retention ~121%

Scale, stickiness and ~121% retention curb pricing pressure

Buyers press on price via scale and multi-year deals, but CrowdStrike’s FY2024 scale (revenue $2.18B; ARR ~$2.03B; 20,000+ customers) and documented ROI limit concession. Deployment stickiness, SOC integrations and telemetry raise switching costs; competition (Microsoft, Palo Alto, SentinelOne) increases pre-sale leverage. High breach costs reduce pure price sensitivity; dollar-based net retention ~121% in 2024.

| Metric | FY2024 |

|---|---|

| Revenue | $2.18B |

| ARR | ~$2.03B |

| Customers | 20,000+ |

| Net retention | ~121% |

Preview the Actual Deliverable

CrowdStrike Porter's Five Forces Analysis

This CrowdStrike Porter's Five Forces analysis delivers a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products with clear implications for strategy and valuation. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file. It's fully formatted and ready to use.

A Must-Have Tool for Decision-Makers

CrowdStrike faces intense competitive rivalry amid rapid innovation and scaling incumbents, while supplier influence is limited and buyer expectations for integrated, cloud-native security raise switching dynamics; barriers to entry are moderate but high R&D and data network effects protect incumbents. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CrowdStrike’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on hyperscale clouds

CrowdStrike depends on public hyperscale clouds for compute, storage and global delivery of Falcon, with FY2024 revenue of about 2.07 billion USD highlighting scale and exposure. Hyperscalers (AWS ~32%, Azure ~24%, GCP ~11% share in 2024 IaaS) can influence pricing, service levels and egress fees, creating supplier leverage. Multi-cloud architectures and long-term contracts mitigate risk, but major outages or policy shifts at a hyperscaler could disrupt continuity and compress margins.

Scarcity of elite security talent

Advanced threat researchers, data scientists and reverse engineers are critical inputs; ISC2 reported a global cybersecurity workforce shortfall of about 3.4 million in 2024, driving wage inflation and higher retention costs. The labor market and specialized contractors thus hold strong bargaining power. CrowdStrike’s brand and hiring investments improve attraction but do not erase scarcity-driven supplier leverage.

Third-party threat intel and data feeds

Supplemental third-party intelligence and OS/app telemetry partnerships improve detection quality and enrich context; niche feeds with unique indicators can command pricing power. Some providers retain leverage due to differentiated, hard-to-replicate signals. CrowdStrike’s proprietary scale—20,000+ customers and billions of daily telemetry events—reduces dependence on any single feed. Diversified supplier contracts further lower switching risk and supplier power.

Chipsets, device ecosystems, and OS vendors

Endpoint agents must interoperate with CPUs, firmware, and operating systems, with Windows holding ~76% desktop share in 2024 and Android ~71% of mobile—making platform compatibility critical. API access, driver models, and policy shifts by platform owners can materially affect detection and performance, and platform gatekeepers often dictate timelines despite open standards. Close partnerships and early-access programs with OS and chipset vendors reduce integration lag and moderate supplier influence.

- Platform share: Windows ~76% (2024)

- Mobile OS: Android ~71% (2024)

- Risk: API/policy changes can delay features

- Mitigation: early-access/partnerships

Channel and MSSP alliances

Channel and MSSP alliances—value-added resellers, distributors and managed security providers—extend CrowdStrike reach, while top partners can extract favorable terms, marketing funds or deal-registration priority.

- FY2024: over 20,000 customers reduces channel reliance

- Top-channel leverage varies by region and segment

- Direct enterprise sales lower supplier power

Hyperscaler leverage (AWS 32%) and 3.4M cyber talent gap

CrowdStrike faces supplier leverage from hyperscalers (FY2024 revenue ~$2.07B; IaaS: AWS ~32%, Azure ~24%, GCP ~11%), a global cyber workforce shortfall ~3.4M (2024) driving wage pressure, reliance on niche intelligence feeds, and platform gatekeepers (Windows ~76%, Android ~71%, 20,000+ customers reduces single-supplier risk).

| Metric | 2024 |

|---|---|

| Revenue (FY2024) | $2.07B |

| Customers | 20,000+ |

| IaaS share | AWS32%/Azure24%/GCP11% |

| Workforce gap | 3.4M |

| OS share | Windows76%/Android71% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to CrowdStrike, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and disruptive/emerging risks to market share. Provides strategic commentary on pricing power, barriers to entry and defensive advantages to inform investors, strategists and academics.

Clear, one-sheet Porter's Five Forces for CrowdStrike that visualizes competitive pressure with an editable radar chart—perfect for quick, boardroom-ready decisions. No macros, easy integration into decks or broader dashboards.

Customers Bargaining Power

Large enterprise procurement leverage

Global enterprises and governments press hard on price and terms, leveraging scale, multi-year commitments and complex compliance needs to increase bargaining power; competitive bake-offs among top vendors amplify this pressure. CrowdStrike entered FY2024 with 20,000+ customers, $2.18B revenue and ~$2.03B ARR, countering with platform breadth and documented ROI to defend pricing and win multi-year deals.

High switching costs from agent footprint

Deploying and managing CrowdStrike agents across thousands of endpoints creates operational stickiness, given the scale of deployments across over 19,000 customers in 2024 and millions of protected devices. Integration into SOC workflows, SIEMs and automation platforms amplifies lock-in by embedding processes and alerts. Longitudinal telemetry, detection tuning and playbook customizations further raise switching barriers, lowering buyer power post-deployment despite pre-sale leverage; dollar-based net retention remained >120% in 2024.

Abundant credible alternatives

Customers compare Microsoft, Palo Alto Networks, CrowdStrike and SentinelOne—Gartner 2024 lists them as leading EPP vendors—so perceived substitutability rises as vendors assert feature parity and bundle suites. Proof-of-value trials force competition on efficacy and total cost, shortening sales cycles. Buyers leverage this landscape to extract deeper discounts and tighter SLAs. Negotiations increasingly hinge on measurable ROI and deployment metrics.

Outcome-critical, not purely price-driven

Security failures carry multi-million-dollar loss potential, so buyers prioritize detection efficacy, speed, and incident response over unit price; this outcome-critical stance tempers customer bargaining power. CrowdStrike reported FY2024 revenue of $3.45B and serves over 23,000 customers, allowing it to sustain premium pricing supported by large-scale telemetry and efficacy data.

- High stakes reduce price sensitivity

- FY2024 revenue: $3.45B; >23,000 customers

- Strong efficacy data supports premium pricing

Multi-year SaaS and modular upsell

CrowdStrike sells multi-year SaaS agreements with modular Falcon add-ons, using expansion-led pricing to trade initial discounts for higher lifetime value; renewal checkpoints and competitive evaluations give buyers periodic leverage, and land-and-expand dynamics dilute but do not eliminate buyer bargaining power.

- FY2024 revenue about $2.06B

- ARR ~ $3.45B

- Net retention ~121%

Scale, stickiness and ~121% retention curb pricing pressure

Buyers press on price via scale and multi-year deals, but CrowdStrike’s FY2024 scale (revenue $2.18B; ARR ~$2.03B; 20,000+ customers) and documented ROI limit concession. Deployment stickiness, SOC integrations and telemetry raise switching costs; competition (Microsoft, Palo Alto, SentinelOne) increases pre-sale leverage. High breach costs reduce pure price sensitivity; dollar-based net retention ~121% in 2024.

| Metric | FY2024 |

|---|---|

| Revenue | $2.18B |

| ARR | ~$2.03B |

| Customers | 20,000+ |

| Net retention | ~121% |

Preview the Actual Deliverable

CrowdStrike Porter's Five Forces Analysis

This CrowdStrike Porter's Five Forces analysis delivers a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products with clear implications for strategy and valuation. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file. It's fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

CrowdStrike faces intense competitive rivalry amid rapid innovation and scaling incumbents, while supplier influence is limited and buyer expectations for integrated, cloud-native security raise switching dynamics; barriers to entry are moderate but high R&D and data network effects protect incumbents. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CrowdStrike’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on hyperscale clouds

CrowdStrike depends on public hyperscale clouds for compute, storage and global delivery of Falcon, with FY2024 revenue of about 2.07 billion USD highlighting scale and exposure. Hyperscalers (AWS ~32%, Azure ~24%, GCP ~11% share in 2024 IaaS) can influence pricing, service levels and egress fees, creating supplier leverage. Multi-cloud architectures and long-term contracts mitigate risk, but major outages or policy shifts at a hyperscaler could disrupt continuity and compress margins.

Scarcity of elite security talent

Advanced threat researchers, data scientists and reverse engineers are critical inputs; ISC2 reported a global cybersecurity workforce shortfall of about 3.4 million in 2024, driving wage inflation and higher retention costs. The labor market and specialized contractors thus hold strong bargaining power. CrowdStrike’s brand and hiring investments improve attraction but do not erase scarcity-driven supplier leverage.

Third-party threat intel and data feeds

Supplemental third-party intelligence and OS/app telemetry partnerships improve detection quality and enrich context; niche feeds with unique indicators can command pricing power. Some providers retain leverage due to differentiated, hard-to-replicate signals. CrowdStrike’s proprietary scale—20,000+ customers and billions of daily telemetry events—reduces dependence on any single feed. Diversified supplier contracts further lower switching risk and supplier power.

Chipsets, device ecosystems, and OS vendors

Endpoint agents must interoperate with CPUs, firmware, and operating systems, with Windows holding ~76% desktop share in 2024 and Android ~71% of mobile—making platform compatibility critical. API access, driver models, and policy shifts by platform owners can materially affect detection and performance, and platform gatekeepers often dictate timelines despite open standards. Close partnerships and early-access programs with OS and chipset vendors reduce integration lag and moderate supplier influence.

- Platform share: Windows ~76% (2024)

- Mobile OS: Android ~71% (2024)

- Risk: API/policy changes can delay features

- Mitigation: early-access/partnerships

Channel and MSSP alliances

Channel and MSSP alliances—value-added resellers, distributors and managed security providers—extend CrowdStrike reach, while top partners can extract favorable terms, marketing funds or deal-registration priority.

- FY2024: over 20,000 customers reduces channel reliance

- Top-channel leverage varies by region and segment

- Direct enterprise sales lower supplier power

Hyperscaler leverage (AWS 32%) and 3.4M cyber talent gap

CrowdStrike faces supplier leverage from hyperscalers (FY2024 revenue ~$2.07B; IaaS: AWS ~32%, Azure ~24%, GCP ~11%), a global cyber workforce shortfall ~3.4M (2024) driving wage pressure, reliance on niche intelligence feeds, and platform gatekeepers (Windows ~76%, Android ~71%, 20,000+ customers reduces single-supplier risk).

| Metric | 2024 |

|---|---|

| Revenue (FY2024) | $2.07B |

| Customers | 20,000+ |

| IaaS share | AWS32%/Azure24%/GCP11% |

| Workforce gap | 3.4M |

| OS share | Windows76%/Android71% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to CrowdStrike, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and disruptive/emerging risks to market share. Provides strategic commentary on pricing power, barriers to entry and defensive advantages to inform investors, strategists and academics.

Clear, one-sheet Porter's Five Forces for CrowdStrike that visualizes competitive pressure with an editable radar chart—perfect for quick, boardroom-ready decisions. No macros, easy integration into decks or broader dashboards.

Customers Bargaining Power

Large enterprise procurement leverage

Global enterprises and governments press hard on price and terms, leveraging scale, multi-year commitments and complex compliance needs to increase bargaining power; competitive bake-offs among top vendors amplify this pressure. CrowdStrike entered FY2024 with 20,000+ customers, $2.18B revenue and ~$2.03B ARR, countering with platform breadth and documented ROI to defend pricing and win multi-year deals.

High switching costs from agent footprint

Deploying and managing CrowdStrike agents across thousands of endpoints creates operational stickiness, given the scale of deployments across over 19,000 customers in 2024 and millions of protected devices. Integration into SOC workflows, SIEMs and automation platforms amplifies lock-in by embedding processes and alerts. Longitudinal telemetry, detection tuning and playbook customizations further raise switching barriers, lowering buyer power post-deployment despite pre-sale leverage; dollar-based net retention remained >120% in 2024.

Abundant credible alternatives

Customers compare Microsoft, Palo Alto Networks, CrowdStrike and SentinelOne—Gartner 2024 lists them as leading EPP vendors—so perceived substitutability rises as vendors assert feature parity and bundle suites. Proof-of-value trials force competition on efficacy and total cost, shortening sales cycles. Buyers leverage this landscape to extract deeper discounts and tighter SLAs. Negotiations increasingly hinge on measurable ROI and deployment metrics.

Outcome-critical, not purely price-driven

Security failures carry multi-million-dollar loss potential, so buyers prioritize detection efficacy, speed, and incident response over unit price; this outcome-critical stance tempers customer bargaining power. CrowdStrike reported FY2024 revenue of $3.45B and serves over 23,000 customers, allowing it to sustain premium pricing supported by large-scale telemetry and efficacy data.

- High stakes reduce price sensitivity

- FY2024 revenue: $3.45B; >23,000 customers

- Strong efficacy data supports premium pricing

Multi-year SaaS and modular upsell

CrowdStrike sells multi-year SaaS agreements with modular Falcon add-ons, using expansion-led pricing to trade initial discounts for higher lifetime value; renewal checkpoints and competitive evaluations give buyers periodic leverage, and land-and-expand dynamics dilute but do not eliminate buyer bargaining power.

- FY2024 revenue about $2.06B

- ARR ~ $3.45B

- Net retention ~121%

Scale, stickiness and ~121% retention curb pricing pressure

Buyers press on price via scale and multi-year deals, but CrowdStrike’s FY2024 scale (revenue $2.18B; ARR ~$2.03B; 20,000+ customers) and documented ROI limit concession. Deployment stickiness, SOC integrations and telemetry raise switching costs; competition (Microsoft, Palo Alto, SentinelOne) increases pre-sale leverage. High breach costs reduce pure price sensitivity; dollar-based net retention ~121% in 2024.

| Metric | FY2024 |

|---|---|

| Revenue | $2.18B |

| ARR | ~$2.03B |

| Customers | 20,000+ |

| Net retention | ~121% |

Preview the Actual Deliverable

CrowdStrike Porter's Five Forces Analysis

This CrowdStrike Porter's Five Forces analysis delivers a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products with clear implications for strategy and valuation. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file. It's fully formatted and ready to use.