Citic Securities Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

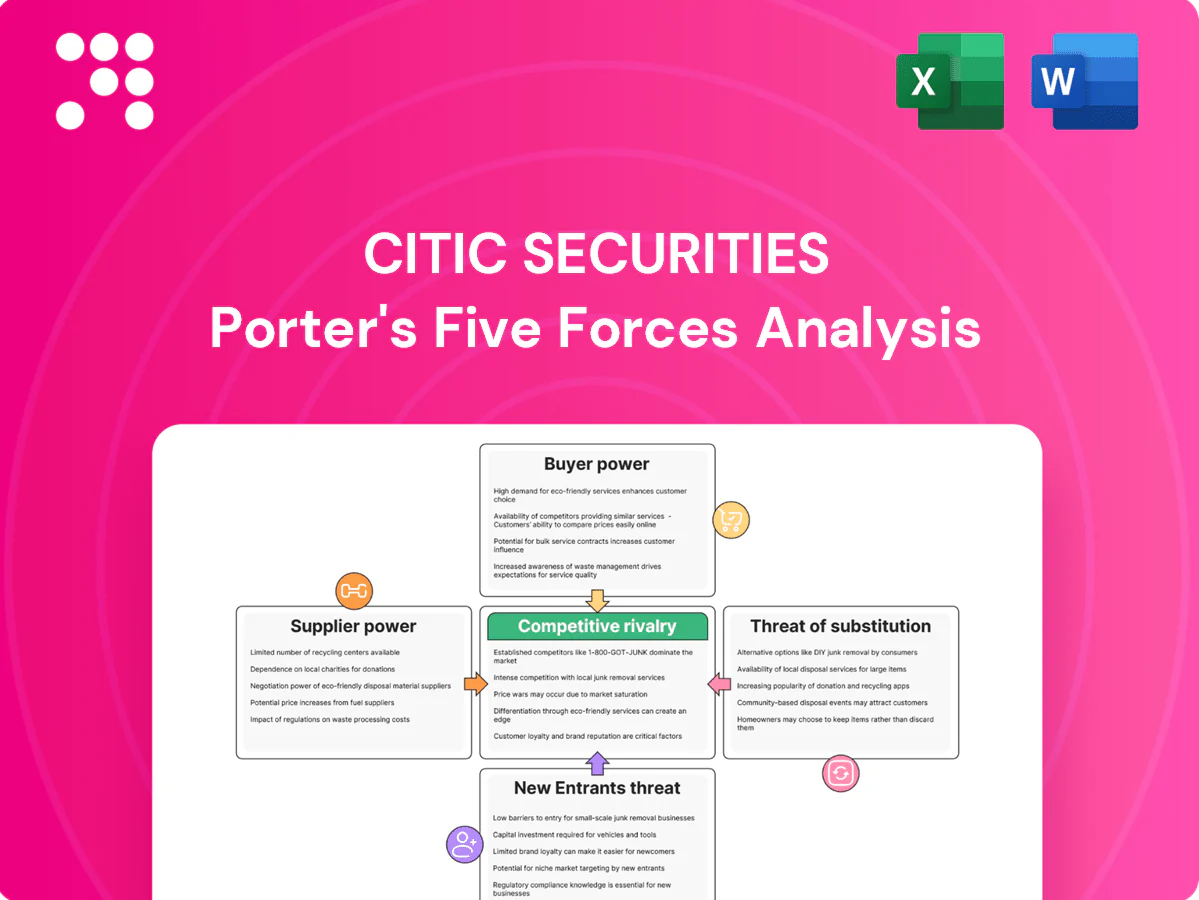

Citic Securities faces evolving competitive pressures across buyer power, supplier influence, and regulatory threats that reshape its brokerage and investment banking margins. This brief highlights key industry tensions and strategic levers leadership can exploit. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on skilled talent

CITIC Securities depends on scarce top bankers, traders, quants and research analysts, driving wage pressure and premium compensation for star performers who can jump to rivals, raising retention costs.

Training pipelines and internal mobility have reduced churn, but talent remains a high-leverage supplier for deal flow and trading profits; China’s 2024 graduate cohort (~11.5 million) eases entry-level supply yet not senior hires.

Government-linked prestige via parent CITIC Group strengthens campus attraction, moderating supplier power despite continued competition for experienced specialists.

Market data and technology vendors

Essential feeds, OMS/EMS, risk engines and cloud services are concentrated: Bloomberg and Refinitiv account for roughly 70–75% of institutional market-data/terminal share, while AWS, Azure and GCP control about 60–65% of global IaaS; switching costs from integration, latency tuning and compliance validation drive lock-in. Volume-based pricing can cut fees 10–30% but does not remove migration cost; growing domestic cloud/vendors (≈60% share in China) temper but do not eliminate supplier power.

Capital and liquidity providers

Repo counterparties, banks and bond investors supply the bulk of funding for CITIC Securities’ margin lending and market‑making; in 2024 funding conditions shifted with PBOC policy and market risk sentiment, directly affecting wholesale costs. A strong balance sheet and CITIC Group SOE affiliation support competitive access to bank lines and repo, while diversified funding channels limit any single provider’s leverage over pricing.

Deal flow intermediaries and issuers’ advisors

Law firms, accountants, rating agencies and boutiques shape CITIC’s underwriting pipeline through reputational gatekeeping that influences mandates and timelines, though internal estimates show intermediary referrals account for under 30% of CITIC’s deal flow in 2024. Competition among advisers caps their pricing power, while CITIC’s integrated platform — with a top-five domestic investment banking ranking by deal value in 2023–24 — reduces dependence on any single intermediary.

Exchanges and clearing infrastructure

Access to Shanghai and Shenzhen exchanges, CSDC clearing and international trading links is indispensable for Citic Securities; these venues mandate standardized fee schedules and regulatory oversight by the CSRC, limiting negotiation. Regulatory constraints and standardized tariffs (for example China’s 0.1% stamp duty on stock sales) stabilize terms and constrain supplier discretion. Dependency is high, but suppliers’ pricing power is institutionally moderated, keeping brokerage clearing/transaction costs predictable.

- High dependency on exchange/clearing access

- Standardized fees and CSRC oversight

- 0.1% stamp duty on stock sales (China, 2024)

- Limited room for fee negotiation

Senior-talent premiums and market-data oligopoly (70-75%) drive high supplier power

CITIC Securities faces high supplier power for senior talent and market data: top bankers/quants command premiums despite 2024 graduate cohort ~11.5m easing entry-level supply. Market-data terminals (Bloomberg/Refinitiv) hold ~70–75% share; global IaaS (AWS/Azure/GCP) ~60–65%, domestic cloud ~60% in China, raising switching costs. Intermediary referrals <30% of deal flow (2024); exchange fees/stamp duty 0.1% constrain negotiation, while CITIC Group backing and diversified funding mitigate supplier leverage.

| Supplier | 2024 metric |

|---|---|

| Graduate supply | ~11.5m |

| Market-data share | 70–75% |

| Global IaaS | 60–65% |

| Intermediary referrals | <30% |

| Stamp duty | 0.1% |

What is included in the product

Tailored Porter's Five Forces analysis for Citic Securities that uncovers key drivers of competition, evaluates buyer and supplier power, assesses entry barriers and substitutes, and identifies disruptive threats and strategic opportunities to defend market share and inform investor or management decisions.

A clear, one-sheet Porter's Five Forces summary for Citic Securities—perfect for quick decision-making and boardroom slides. Customize pressure levels and view strategic intensity instantly with a spider chart, ready to paste into reports or decks.

Customers Bargaining Power

Institutional client bargaining

Mutual funds, insurers and prop desks concentrate volumes and often account for >50% of brokerage trades, enabling sustained fee pressure on brokerage and prime services. RFPs and multi-dealer lists (commonly 4–6 dealers) intensify price competition. Differentiated research, liquidity provision and favorable IPO allocation remain key levers to justify wider spreads. Deep relationships and cross-selling materially reduce client churn.

Corporate issuers’ fee sensitivity

Issuers routinely shop underwriting mandates among top-tier banks, compressing fees as 2024 league tables show the top five houses capturing over 60% of major mandates. League-table prestige and distribution reach remain key differentiators that allow Citic to resist the lowest bids. SOE relationships provide pricing stability on ~large state deals but do not remove interbank competition. Complex, structured transactions permit scope-based pricing to defend margins.

HNWI and wealth clients

HNWI and wealth clients exert strong bargaining power as global HNW population reached about 21.9 million with roughly USD 84 trillion in wealth in 2024 (Capgemini), making fee sensitivity acute as many can switch to banks, fintechs, or private managers for lower fees.

High-quality advisory and exclusive product access raise switching costs, while superior digital experience and transparency—used by over 60% of HNW in 2024—drive retention.

Bundled lending, brokerage and asset management services markedly improve stickiness by deepening wallet share and raising exit costs.

Global investors accessing China

Global investors accessing China demand best execution, research and connectivity via QFII/Stock Connect, with foreign ownership of A-shares rising to about 5.4% by end-2023, forcing fee benchmarking against global peers and pressuring margins. Compliance, custody and RMB liquidity solutions can command premiums; currency and policy risks emphasize service reliability over pure price.

- Demands: execution, research, connectivity

- Pressure: global fee benchmarking

- Differentiators: compliance, custody, RMB solutions

- Risk factor: currency/policy drives reliability focus

Data-driven performance scrutiny

Clients in 2024 deploy analytics to scrutinize execution quality and alpha contribution, driving tougher fee negotiations; measurable benchmarks like VWAP and slippage metrics intensify pricing pressure. Citic defends fees by offering value-added research and bespoke solutions, while multi-year mandates and advisory retainers mitigate short-term repricing.

- 2024: analytics-led scrutiny

- benchmarks: VWAP/slippage

- defense: bespoke insights

- stability: long-term mandates

Institutions and HNWI squeeze fees; Top5 banks win >60% underwriting mandates

Large institutional clients (mutual funds, insurers, prop desks) concentrate volumes (>50% of brokerage) and force fee competition; top five banks capture >60% of underwriting mandates, pressuring spreads. HNWI fee sensitivity is high (21.9m HNW, USD84tn wealth in 2024), while foreign investors (A-share ownership ~5.4% end-2023) benchmark fees globally. Citic defends with research, exclusives, bundled services and multi-year mandates.

| Client | Bargaining power | Key metric |

|---|---|---|

| Institutions | High | >50% trades |

| Issuers | High | Top5>60% mandates |

| HNWI | High | 21.9m / USD84tn (2024) |

| Foreign | Medium | A-shares 5.4% (2023) |

Same Document Delivered

Citic Securities Porter's Five Forces Analysis

This preview shows the exact Citic Securities Porter’s Five Forces analysis you’ll receive—fully formatted, accurate, and ready to download immediately after purchase. No samples or placeholders: the content, charts, and conclusions here are the final deliverable for your use.

Go Beyond the Preview—Access the Full Strategic Report

Citic Securities faces evolving competitive pressures across buyer power, supplier influence, and regulatory threats that reshape its brokerage and investment banking margins. This brief highlights key industry tensions and strategic levers leadership can exploit. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on skilled talent

CITIC Securities depends on scarce top bankers, traders, quants and research analysts, driving wage pressure and premium compensation for star performers who can jump to rivals, raising retention costs.

Training pipelines and internal mobility have reduced churn, but talent remains a high-leverage supplier for deal flow and trading profits; China’s 2024 graduate cohort (~11.5 million) eases entry-level supply yet not senior hires.

Government-linked prestige via parent CITIC Group strengthens campus attraction, moderating supplier power despite continued competition for experienced specialists.

Market data and technology vendors

Essential feeds, OMS/EMS, risk engines and cloud services are concentrated: Bloomberg and Refinitiv account for roughly 70–75% of institutional market-data/terminal share, while AWS, Azure and GCP control about 60–65% of global IaaS; switching costs from integration, latency tuning and compliance validation drive lock-in. Volume-based pricing can cut fees 10–30% but does not remove migration cost; growing domestic cloud/vendors (≈60% share in China) temper but do not eliminate supplier power.

Capital and liquidity providers

Repo counterparties, banks and bond investors supply the bulk of funding for CITIC Securities’ margin lending and market‑making; in 2024 funding conditions shifted with PBOC policy and market risk sentiment, directly affecting wholesale costs. A strong balance sheet and CITIC Group SOE affiliation support competitive access to bank lines and repo, while diversified funding channels limit any single provider’s leverage over pricing.

Deal flow intermediaries and issuers’ advisors

Law firms, accountants, rating agencies and boutiques shape CITIC’s underwriting pipeline through reputational gatekeeping that influences mandates and timelines, though internal estimates show intermediary referrals account for under 30% of CITIC’s deal flow in 2024. Competition among advisers caps their pricing power, while CITIC’s integrated platform — with a top-five domestic investment banking ranking by deal value in 2023–24 — reduces dependence on any single intermediary.

Exchanges and clearing infrastructure

Access to Shanghai and Shenzhen exchanges, CSDC clearing and international trading links is indispensable for Citic Securities; these venues mandate standardized fee schedules and regulatory oversight by the CSRC, limiting negotiation. Regulatory constraints and standardized tariffs (for example China’s 0.1% stamp duty on stock sales) stabilize terms and constrain supplier discretion. Dependency is high, but suppliers’ pricing power is institutionally moderated, keeping brokerage clearing/transaction costs predictable.

- High dependency on exchange/clearing access

- Standardized fees and CSRC oversight

- 0.1% stamp duty on stock sales (China, 2024)

- Limited room for fee negotiation

Senior-talent premiums and market-data oligopoly (70-75%) drive high supplier power

CITIC Securities faces high supplier power for senior talent and market data: top bankers/quants command premiums despite 2024 graduate cohort ~11.5m easing entry-level supply. Market-data terminals (Bloomberg/Refinitiv) hold ~70–75% share; global IaaS (AWS/Azure/GCP) ~60–65%, domestic cloud ~60% in China, raising switching costs. Intermediary referrals <30% of deal flow (2024); exchange fees/stamp duty 0.1% constrain negotiation, while CITIC Group backing and diversified funding mitigate supplier leverage.

| Supplier | 2024 metric |

|---|---|

| Graduate supply | ~11.5m |

| Market-data share | 70–75% |

| Global IaaS | 60–65% |

| Intermediary referrals | <30% |

| Stamp duty | 0.1% |

What is included in the product

Tailored Porter's Five Forces analysis for Citic Securities that uncovers key drivers of competition, evaluates buyer and supplier power, assesses entry barriers and substitutes, and identifies disruptive threats and strategic opportunities to defend market share and inform investor or management decisions.

A clear, one-sheet Porter's Five Forces summary for Citic Securities—perfect for quick decision-making and boardroom slides. Customize pressure levels and view strategic intensity instantly with a spider chart, ready to paste into reports or decks.

Customers Bargaining Power

Institutional client bargaining

Mutual funds, insurers and prop desks concentrate volumes and often account for >50% of brokerage trades, enabling sustained fee pressure on brokerage and prime services. RFPs and multi-dealer lists (commonly 4–6 dealers) intensify price competition. Differentiated research, liquidity provision and favorable IPO allocation remain key levers to justify wider spreads. Deep relationships and cross-selling materially reduce client churn.

Corporate issuers’ fee sensitivity

Issuers routinely shop underwriting mandates among top-tier banks, compressing fees as 2024 league tables show the top five houses capturing over 60% of major mandates. League-table prestige and distribution reach remain key differentiators that allow Citic to resist the lowest bids. SOE relationships provide pricing stability on ~large state deals but do not remove interbank competition. Complex, structured transactions permit scope-based pricing to defend margins.

HNWI and wealth clients

HNWI and wealth clients exert strong bargaining power as global HNW population reached about 21.9 million with roughly USD 84 trillion in wealth in 2024 (Capgemini), making fee sensitivity acute as many can switch to banks, fintechs, or private managers for lower fees.

High-quality advisory and exclusive product access raise switching costs, while superior digital experience and transparency—used by over 60% of HNW in 2024—drive retention.

Bundled lending, brokerage and asset management services markedly improve stickiness by deepening wallet share and raising exit costs.

Global investors accessing China

Global investors accessing China demand best execution, research and connectivity via QFII/Stock Connect, with foreign ownership of A-shares rising to about 5.4% by end-2023, forcing fee benchmarking against global peers and pressuring margins. Compliance, custody and RMB liquidity solutions can command premiums; currency and policy risks emphasize service reliability over pure price.

- Demands: execution, research, connectivity

- Pressure: global fee benchmarking

- Differentiators: compliance, custody, RMB solutions

- Risk factor: currency/policy drives reliability focus

Data-driven performance scrutiny

Clients in 2024 deploy analytics to scrutinize execution quality and alpha contribution, driving tougher fee negotiations; measurable benchmarks like VWAP and slippage metrics intensify pricing pressure. Citic defends fees by offering value-added research and bespoke solutions, while multi-year mandates and advisory retainers mitigate short-term repricing.

- 2024: analytics-led scrutiny

- benchmarks: VWAP/slippage

- defense: bespoke insights

- stability: long-term mandates

Institutions and HNWI squeeze fees; Top5 banks win >60% underwriting mandates

Large institutional clients (mutual funds, insurers, prop desks) concentrate volumes (>50% of brokerage) and force fee competition; top five banks capture >60% of underwriting mandates, pressuring spreads. HNWI fee sensitivity is high (21.9m HNW, USD84tn wealth in 2024), while foreign investors (A-share ownership ~5.4% end-2023) benchmark fees globally. Citic defends with research, exclusives, bundled services and multi-year mandates.

| Client | Bargaining power | Key metric |

|---|---|---|

| Institutions | High | >50% trades |

| Issuers | High | Top5>60% mandates |

| HNWI | High | 21.9m / USD84tn (2024) |

| Foreign | Medium | A-shares 5.4% (2023) |

Same Document Delivered

Citic Securities Porter's Five Forces Analysis

This preview shows the exact Citic Securities Porter’s Five Forces analysis you’ll receive—fully formatted, accurate, and ready to download immediately after purchase. No samples or placeholders: the content, charts, and conclusions here are the final deliverable for your use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Citic Securities faces evolving competitive pressures across buyer power, supplier influence, and regulatory threats that reshape its brokerage and investment banking margins. This brief highlights key industry tensions and strategic levers leadership can exploit. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on skilled talent

CITIC Securities depends on scarce top bankers, traders, quants and research analysts, driving wage pressure and premium compensation for star performers who can jump to rivals, raising retention costs.

Training pipelines and internal mobility have reduced churn, but talent remains a high-leverage supplier for deal flow and trading profits; China’s 2024 graduate cohort (~11.5 million) eases entry-level supply yet not senior hires.

Government-linked prestige via parent CITIC Group strengthens campus attraction, moderating supplier power despite continued competition for experienced specialists.

Market data and technology vendors

Essential feeds, OMS/EMS, risk engines and cloud services are concentrated: Bloomberg and Refinitiv account for roughly 70–75% of institutional market-data/terminal share, while AWS, Azure and GCP control about 60–65% of global IaaS; switching costs from integration, latency tuning and compliance validation drive lock-in. Volume-based pricing can cut fees 10–30% but does not remove migration cost; growing domestic cloud/vendors (≈60% share in China) temper but do not eliminate supplier power.

Capital and liquidity providers

Repo counterparties, banks and bond investors supply the bulk of funding for CITIC Securities’ margin lending and market‑making; in 2024 funding conditions shifted with PBOC policy and market risk sentiment, directly affecting wholesale costs. A strong balance sheet and CITIC Group SOE affiliation support competitive access to bank lines and repo, while diversified funding channels limit any single provider’s leverage over pricing.

Deal flow intermediaries and issuers’ advisors

Law firms, accountants, rating agencies and boutiques shape CITIC’s underwriting pipeline through reputational gatekeeping that influences mandates and timelines, though internal estimates show intermediary referrals account for under 30% of CITIC’s deal flow in 2024. Competition among advisers caps their pricing power, while CITIC’s integrated platform — with a top-five domestic investment banking ranking by deal value in 2023–24 — reduces dependence on any single intermediary.

Exchanges and clearing infrastructure

Access to Shanghai and Shenzhen exchanges, CSDC clearing and international trading links is indispensable for Citic Securities; these venues mandate standardized fee schedules and regulatory oversight by the CSRC, limiting negotiation. Regulatory constraints and standardized tariffs (for example China’s 0.1% stamp duty on stock sales) stabilize terms and constrain supplier discretion. Dependency is high, but suppliers’ pricing power is institutionally moderated, keeping brokerage clearing/transaction costs predictable.

- High dependency on exchange/clearing access

- Standardized fees and CSRC oversight

- 0.1% stamp duty on stock sales (China, 2024)

- Limited room for fee negotiation

Senior-talent premiums and market-data oligopoly (70-75%) drive high supplier power

CITIC Securities faces high supplier power for senior talent and market data: top bankers/quants command premiums despite 2024 graduate cohort ~11.5m easing entry-level supply. Market-data terminals (Bloomberg/Refinitiv) hold ~70–75% share; global IaaS (AWS/Azure/GCP) ~60–65%, domestic cloud ~60% in China, raising switching costs. Intermediary referrals <30% of deal flow (2024); exchange fees/stamp duty 0.1% constrain negotiation, while CITIC Group backing and diversified funding mitigate supplier leverage.

| Supplier | 2024 metric |

|---|---|

| Graduate supply | ~11.5m |

| Market-data share | 70–75% |

| Global IaaS | 60–65% |

| Intermediary referrals | <30% |

| Stamp duty | 0.1% |

What is included in the product

Tailored Porter's Five Forces analysis for Citic Securities that uncovers key drivers of competition, evaluates buyer and supplier power, assesses entry barriers and substitutes, and identifies disruptive threats and strategic opportunities to defend market share and inform investor or management decisions.

A clear, one-sheet Porter's Five Forces summary for Citic Securities—perfect for quick decision-making and boardroom slides. Customize pressure levels and view strategic intensity instantly with a spider chart, ready to paste into reports or decks.

Customers Bargaining Power

Institutional client bargaining

Mutual funds, insurers and prop desks concentrate volumes and often account for >50% of brokerage trades, enabling sustained fee pressure on brokerage and prime services. RFPs and multi-dealer lists (commonly 4–6 dealers) intensify price competition. Differentiated research, liquidity provision and favorable IPO allocation remain key levers to justify wider spreads. Deep relationships and cross-selling materially reduce client churn.

Corporate issuers’ fee sensitivity

Issuers routinely shop underwriting mandates among top-tier banks, compressing fees as 2024 league tables show the top five houses capturing over 60% of major mandates. League-table prestige and distribution reach remain key differentiators that allow Citic to resist the lowest bids. SOE relationships provide pricing stability on ~large state deals but do not remove interbank competition. Complex, structured transactions permit scope-based pricing to defend margins.

HNWI and wealth clients

HNWI and wealth clients exert strong bargaining power as global HNW population reached about 21.9 million with roughly USD 84 trillion in wealth in 2024 (Capgemini), making fee sensitivity acute as many can switch to banks, fintechs, or private managers for lower fees.

High-quality advisory and exclusive product access raise switching costs, while superior digital experience and transparency—used by over 60% of HNW in 2024—drive retention.

Bundled lending, brokerage and asset management services markedly improve stickiness by deepening wallet share and raising exit costs.

Global investors accessing China

Global investors accessing China demand best execution, research and connectivity via QFII/Stock Connect, with foreign ownership of A-shares rising to about 5.4% by end-2023, forcing fee benchmarking against global peers and pressuring margins. Compliance, custody and RMB liquidity solutions can command premiums; currency and policy risks emphasize service reliability over pure price.

- Demands: execution, research, connectivity

- Pressure: global fee benchmarking

- Differentiators: compliance, custody, RMB solutions

- Risk factor: currency/policy drives reliability focus

Data-driven performance scrutiny

Clients in 2024 deploy analytics to scrutinize execution quality and alpha contribution, driving tougher fee negotiations; measurable benchmarks like VWAP and slippage metrics intensify pricing pressure. Citic defends fees by offering value-added research and bespoke solutions, while multi-year mandates and advisory retainers mitigate short-term repricing.

- 2024: analytics-led scrutiny

- benchmarks: VWAP/slippage

- defense: bespoke insights

- stability: long-term mandates

Institutions and HNWI squeeze fees; Top5 banks win >60% underwriting mandates

Large institutional clients (mutual funds, insurers, prop desks) concentrate volumes (>50% of brokerage) and force fee competition; top five banks capture >60% of underwriting mandates, pressuring spreads. HNWI fee sensitivity is high (21.9m HNW, USD84tn wealth in 2024), while foreign investors (A-share ownership ~5.4% end-2023) benchmark fees globally. Citic defends with research, exclusives, bundled services and multi-year mandates.

| Client | Bargaining power | Key metric |

|---|---|---|

| Institutions | High | >50% trades |

| Issuers | High | Top5>60% mandates |

| HNWI | High | 21.9m / USD84tn (2024) |

| Foreign | Medium | A-shares 5.4% (2023) |

Same Document Delivered

Citic Securities Porter's Five Forces Analysis

This preview shows the exact Citic Securities Porter’s Five Forces analysis you’ll receive—fully formatted, accurate, and ready to download immediately after purchase. No samples or placeholders: the content, charts, and conclusions here are the final deliverable for your use.