CSL Boston Consulting Group Matrix

See the Bigger Picture

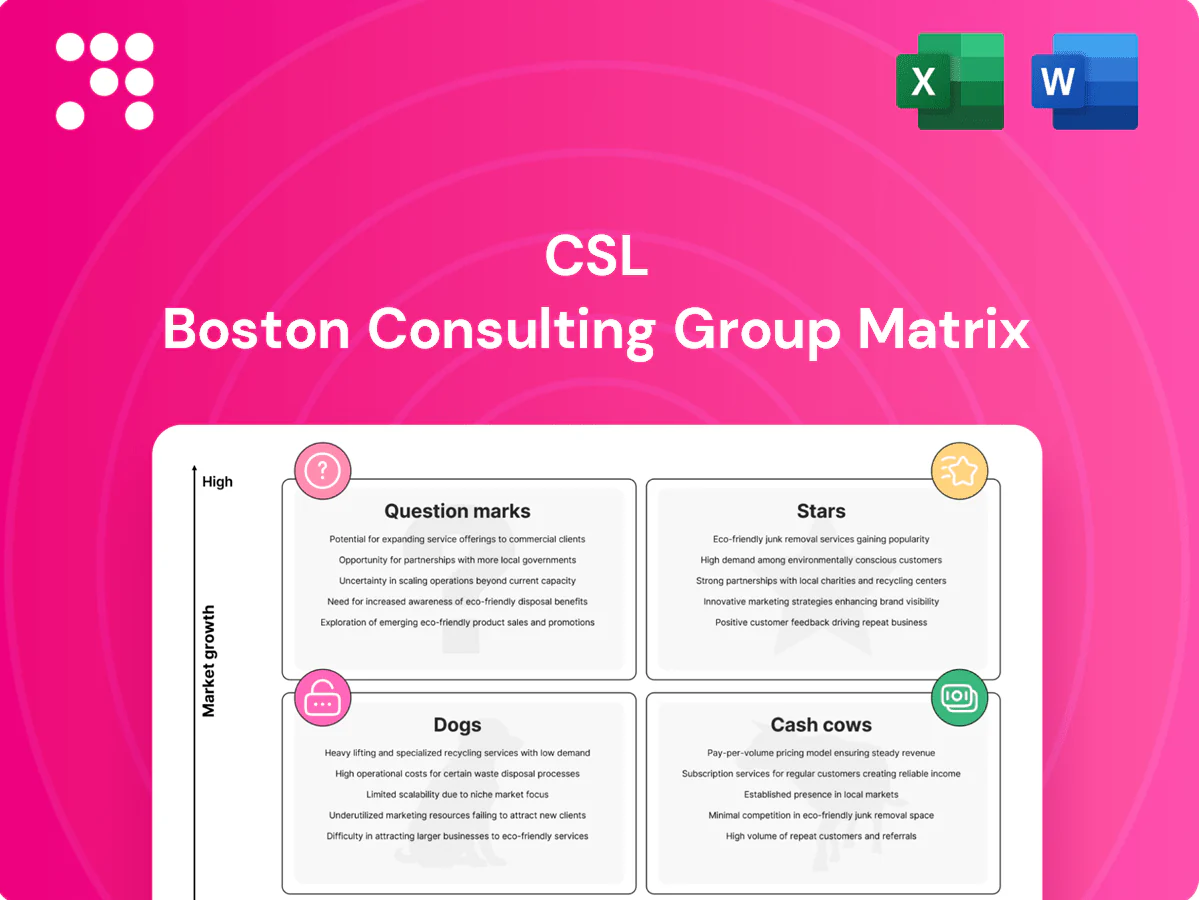

The CSL BCG Matrix snapshot shows which product lines are pulling their weight and which need a new play — a quick read on Stars, Cash Cows, Question Marks, and Dogs within CSL’s portfolio. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word and Excel pack. Skip the guesswork and get strategic clarity now — act where it counts.

Stars

CSL Seqirus influenza vaccines

Massive demand cycles and pandemic readiness keep CSL Seqirus on a steep growth curve, supported by the fact seasonal influenza causes an estimated 290,000–650,000 respiratory deaths annually (WHO). Market share is strong across key markets with trusted government and health-system relationships. Continue investing in capacity, next‑gen platforms and distribution to lock in the lead; as uptake stabilizes this can glide into Cash Cow territory.

Plasma-derived immunoglobulins (PID, CIDP)

Clinical need for plasma-derived immunoglobulins is expanding with global IG demand >US$12bn in 2023 and mid-single-digit CAGR as diagnosis rates and access widen; CSL’s scale — operating ~270 plasma collection centres — and integrated fractionation deliver high share and reliable availability (CSL Behring among top global suppliers). It remains cash-intensive for collection, fractionation and network expansion, but defending share now positions CSL to harvest higher returns as demand grows.

Specialty plasma for rare bleeding disorders

High medical urgency and strong clinician trust drive brisk uptake in growth markets for specialty plasma in rare bleeding disorders; hemophilia A affects about 1 in 5,000 male births and hemophilia B about 1 in 25,000, keeping demand steady. CSL’s deep portfolio and relationships with centers of excellence keep it top‑of‑mind. Ongoing medical education and market access muscle are required; sustained execution can compound into durable leadership.

Recombinant hemophilia therapies (selected assets)

In 2024 switch dynamics and longer‑acting profiles continued to drive recombinant hemophilia category growth; where CSL holds strong positions, share gains plus positive clinical data are sustaining momentum. Competitive heat remains high, keeping promo and access spend elevated, so CSL must keep backing winners to outpace class averages.

- 2024 trend: EHL-driven switch fueling market expansion

- CSL advantage: share gains supported by clinical readouts

- Cost: sustained promo/access investment due to competition

- Priority: double down on top assets to beat class growth

CSL Vifor iron therapies in expanding markets

CSL Vifor iron therapies sit in Stars as CKD and iron‑deficiency care pathways scale: ~850 million people have CKD and ~1.8 billion suffer iron deficiency (WHO/GBD 2023), driving rising hospital and outpatient adoption in 2023–24. Continued market education and tender wins are required; push now while the category is breaking out.

- High prevalence: CKD ~850M; ID ~1.8B

- Adoption: hospital + outpatient growth 2023–24

- Needs: education, tender wins

- Priority: accelerate market capture

Biopharma readies for flu, plasma, hemophilia & CKD/ID growth — scale, R&D, access

CSL Stars: Seqirus rides influenza demand (290,000–650,000 deaths/yr WHO) and pandemic readiness; Behring leads plasma (global IG >US$12bn 2023; ~270 plasma centres); recombinant hemophilia growth sustained by 2024 EHL switches; Vifor scales in CKD/ID (CKD ~850M; ID ~1.8B). Priorities: capacity, next‑gen R&D, market access and focused promo to convert growth into cash flow.

| Product | 2023–24 metric | CSL position | Priority |

|---|---|---|---|

| Seqirus | Influenza burden 290k–650k | Strong gov't share | Capacity/capex |

| Behring | IG >US$12bn | Top supplier; ~270 centres | Collection scale |

| Hemophilia | EHL switch 2024 | Share gains | Back winners |

| Vifor | CKD 850M; ID 1.8B | Growing adoption | Education/tenders |

What is included in the product

Comprehensive BCG Matrix review of CSL's units, with clear quadrant insights and recommendations to invest, hold or divest.

One-page CSL BCG Matrix aligning portfolio pain points to strategy — ready to print, present, or drop into slides.

Cash Cows

Albumin for hospital and critical care

Mature hospital/critical-care albumin has steady, sticky institutional contracts delivering predictable cash flow and low incremental promotion needs; scale drives cost efficiency across plasma sourcing and fractionation, keeping per-unit COGS low. Prioritize manufacturing throughput and regional logistics optimization to preserve high margins and free cash for portfolio reinvestment.

Legacy immunoglobulin indications in mature markets

Established prescriber habits and reimbursement in mature markets keep CSL's legacy immunoglobulin volumes broadly stable, supporting steady annual cash flow; the global IVIG market was roughly USD 18.5 billion in 2024. Brand trust and supply reliability favor CSL, underpinning premium uptake and low churn. Growth is minimal (low-single-digit), but cash conversion remains excellent. Maintain service levels and avoid price leaks to preserve margins.

Seasonal flu vaccines in stable geographies

Seasonal flu vaccines in stable geographies provide forecastable demand via annual procurement cycles and repeat tenders, with global production roughly 500–900 million doses per year. Efficient fill‑finish runs and harvested manufacturing learning curves keep unit costs low, making the franchise cash positive despite routine lifecycle management. Milk revenues while reallocating R&D into next‑gen platforms; Seqirus is among the top three global suppliers.

Established nephrology supportive therapies

Established nephrology supportive therapies are embedded in dialysis protocols with predictable utilization and stable demand; the US dialysis population remains ~550,000 patients (2024), anchoring recurring volume. Competitive set is well known and switching is low, enabling solid margins with modest upkeep; keep contracts tight and operations lean to protect cash flow.

- Embedded protocols: predictable utilization

- Market: US dialysis ~550,000 patients (2024)

- Switching: low, known competitors

- Economics: solid margins, modest upkeep

- Playbook: tight contracts, lean operations

Contracted government supply agreements

Contracted government supply agreements act as cash cows for CSL by smoothing volume and capacity planning through long-term buys; CSL reported FY2024 revenue of about A$13.0 billion, with government programs providing a durable, low-volatility cash base. Once agreements are secured, incremental sales costs are limited and cash visibility is high, supporting predictable free cash flow. Maintaining reliability SLAs above contractual targets preserves renewal rates and pricing leverage.

- Long-term buys: smoothes production planning

- Low incremental sales cost: improves margins

- High cash visibility: reduces volatility

- SLAs critical: drives renewals and pricing

Steady cash: high-margin albumin, IVIG, flu vaccines and nephrology fuel A$13.0bn FY2024

Mature albumin, legacy IVIG and Seqirus flu vaccines plus nephrology therapies and long‑term government contracts generate predictable, high‑margin cash for CSL; FY2024 revenue ~A$13.0bn. IVIG market ~USD18.5bn (2024); US dialysis ~550,000 patients (2024); flu supply 500–900M doses/yr. Prioritize throughput, contract retention and tight SLAs to sustain free cash.

| Cash Cow | 2024 metric | Role |

|---|---|---|

| Albumin | Stable institutional contracts | High margin, low promo |

| IVIG | Global market USD18.5bn | Steady cash flow |

| Seqirus | 500–900M doses/yr | Repeat annual revenue |

| Nephrology | US dialysis ~550k | Recurring demand |

| Govt contracts | Contributes to A$13.0bn | Volume visibility |

Preview = Final Product

CSL BCG Matrix

The file you're previewing is the exact CSL BCG Matrix report you'll receive after purchase. No watermarks, no demo text—just the fully formatted, market-tested analysis ready for strategy meetings. After buying, the final document is delivered immediately for editing, printing, or sharing with stakeholders. It's designed for clarity and action, so there are no surprises.

See the Bigger Picture

The CSL BCG Matrix snapshot shows which product lines are pulling their weight and which need a new play — a quick read on Stars, Cash Cows, Question Marks, and Dogs within CSL’s portfolio. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word and Excel pack. Skip the guesswork and get strategic clarity now — act where it counts.

Stars

CSL Seqirus influenza vaccines

Massive demand cycles and pandemic readiness keep CSL Seqirus on a steep growth curve, supported by the fact seasonal influenza causes an estimated 290,000–650,000 respiratory deaths annually (WHO). Market share is strong across key markets with trusted government and health-system relationships. Continue investing in capacity, next‑gen platforms and distribution to lock in the lead; as uptake stabilizes this can glide into Cash Cow territory.

Plasma-derived immunoglobulins (PID, CIDP)

Clinical need for plasma-derived immunoglobulins is expanding with global IG demand >US$12bn in 2023 and mid-single-digit CAGR as diagnosis rates and access widen; CSL’s scale — operating ~270 plasma collection centres — and integrated fractionation deliver high share and reliable availability (CSL Behring among top global suppliers). It remains cash-intensive for collection, fractionation and network expansion, but defending share now positions CSL to harvest higher returns as demand grows.

Specialty plasma for rare bleeding disorders

High medical urgency and strong clinician trust drive brisk uptake in growth markets for specialty plasma in rare bleeding disorders; hemophilia A affects about 1 in 5,000 male births and hemophilia B about 1 in 25,000, keeping demand steady. CSL’s deep portfolio and relationships with centers of excellence keep it top‑of‑mind. Ongoing medical education and market access muscle are required; sustained execution can compound into durable leadership.

Recombinant hemophilia therapies (selected assets)

In 2024 switch dynamics and longer‑acting profiles continued to drive recombinant hemophilia category growth; where CSL holds strong positions, share gains plus positive clinical data are sustaining momentum. Competitive heat remains high, keeping promo and access spend elevated, so CSL must keep backing winners to outpace class averages.

- 2024 trend: EHL-driven switch fueling market expansion

- CSL advantage: share gains supported by clinical readouts

- Cost: sustained promo/access investment due to competition

- Priority: double down on top assets to beat class growth

CSL Vifor iron therapies in expanding markets

CSL Vifor iron therapies sit in Stars as CKD and iron‑deficiency care pathways scale: ~850 million people have CKD and ~1.8 billion suffer iron deficiency (WHO/GBD 2023), driving rising hospital and outpatient adoption in 2023–24. Continued market education and tender wins are required; push now while the category is breaking out.

- High prevalence: CKD ~850M; ID ~1.8B

- Adoption: hospital + outpatient growth 2023–24

- Needs: education, tender wins

- Priority: accelerate market capture

Biopharma readies for flu, plasma, hemophilia & CKD/ID growth — scale, R&D, access

CSL Stars: Seqirus rides influenza demand (290,000–650,000 deaths/yr WHO) and pandemic readiness; Behring leads plasma (global IG >US$12bn 2023; ~270 plasma centres); recombinant hemophilia growth sustained by 2024 EHL switches; Vifor scales in CKD/ID (CKD ~850M; ID ~1.8B). Priorities: capacity, next‑gen R&D, market access and focused promo to convert growth into cash flow.

| Product | 2023–24 metric | CSL position | Priority |

|---|---|---|---|

| Seqirus | Influenza burden 290k–650k | Strong gov't share | Capacity/capex |

| Behring | IG >US$12bn | Top supplier; ~270 centres | Collection scale |

| Hemophilia | EHL switch 2024 | Share gains | Back winners |

| Vifor | CKD 850M; ID 1.8B | Growing adoption | Education/tenders |

What is included in the product

Comprehensive BCG Matrix review of CSL's units, with clear quadrant insights and recommendations to invest, hold or divest.

One-page CSL BCG Matrix aligning portfolio pain points to strategy — ready to print, present, or drop into slides.

Cash Cows

Albumin for hospital and critical care

Mature hospital/critical-care albumin has steady, sticky institutional contracts delivering predictable cash flow and low incremental promotion needs; scale drives cost efficiency across plasma sourcing and fractionation, keeping per-unit COGS low. Prioritize manufacturing throughput and regional logistics optimization to preserve high margins and free cash for portfolio reinvestment.

Legacy immunoglobulin indications in mature markets

Established prescriber habits and reimbursement in mature markets keep CSL's legacy immunoglobulin volumes broadly stable, supporting steady annual cash flow; the global IVIG market was roughly USD 18.5 billion in 2024. Brand trust and supply reliability favor CSL, underpinning premium uptake and low churn. Growth is minimal (low-single-digit), but cash conversion remains excellent. Maintain service levels and avoid price leaks to preserve margins.

Seasonal flu vaccines in stable geographies

Seasonal flu vaccines in stable geographies provide forecastable demand via annual procurement cycles and repeat tenders, with global production roughly 500–900 million doses per year. Efficient fill‑finish runs and harvested manufacturing learning curves keep unit costs low, making the franchise cash positive despite routine lifecycle management. Milk revenues while reallocating R&D into next‑gen platforms; Seqirus is among the top three global suppliers.

Established nephrology supportive therapies

Established nephrology supportive therapies are embedded in dialysis protocols with predictable utilization and stable demand; the US dialysis population remains ~550,000 patients (2024), anchoring recurring volume. Competitive set is well known and switching is low, enabling solid margins with modest upkeep; keep contracts tight and operations lean to protect cash flow.

- Embedded protocols: predictable utilization

- Market: US dialysis ~550,000 patients (2024)

- Switching: low, known competitors

- Economics: solid margins, modest upkeep

- Playbook: tight contracts, lean operations

Contracted government supply agreements

Contracted government supply agreements act as cash cows for CSL by smoothing volume and capacity planning through long-term buys; CSL reported FY2024 revenue of about A$13.0 billion, with government programs providing a durable, low-volatility cash base. Once agreements are secured, incremental sales costs are limited and cash visibility is high, supporting predictable free cash flow. Maintaining reliability SLAs above contractual targets preserves renewal rates and pricing leverage.

- Long-term buys: smoothes production planning

- Low incremental sales cost: improves margins

- High cash visibility: reduces volatility

- SLAs critical: drives renewals and pricing

Steady cash: high-margin albumin, IVIG, flu vaccines and nephrology fuel A$13.0bn FY2024

Mature albumin, legacy IVIG and Seqirus flu vaccines plus nephrology therapies and long‑term government contracts generate predictable, high‑margin cash for CSL; FY2024 revenue ~A$13.0bn. IVIG market ~USD18.5bn (2024); US dialysis ~550,000 patients (2024); flu supply 500–900M doses/yr. Prioritize throughput, contract retention and tight SLAs to sustain free cash.

| Cash Cow | 2024 metric | Role |

|---|---|---|

| Albumin | Stable institutional contracts | High margin, low promo |

| IVIG | Global market USD18.5bn | Steady cash flow |

| Seqirus | 500–900M doses/yr | Repeat annual revenue |

| Nephrology | US dialysis ~550k | Recurring demand |

| Govt contracts | Contributes to A$13.0bn | Volume visibility |

Preview = Final Product

CSL BCG Matrix

The file you're previewing is the exact CSL BCG Matrix report you'll receive after purchase. No watermarks, no demo text—just the fully formatted, market-tested analysis ready for strategy meetings. After buying, the final document is delivered immediately for editing, printing, or sharing with stakeholders. It's designed for clarity and action, so there are no surprises.

Description

See the Bigger Picture

The CSL BCG Matrix snapshot shows which product lines are pulling their weight and which need a new play — a quick read on Stars, Cash Cows, Question Marks, and Dogs within CSL’s portfolio. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word and Excel pack. Skip the guesswork and get strategic clarity now — act where it counts.

Stars

CSL Seqirus influenza vaccines

Massive demand cycles and pandemic readiness keep CSL Seqirus on a steep growth curve, supported by the fact seasonal influenza causes an estimated 290,000–650,000 respiratory deaths annually (WHO). Market share is strong across key markets with trusted government and health-system relationships. Continue investing in capacity, next‑gen platforms and distribution to lock in the lead; as uptake stabilizes this can glide into Cash Cow territory.

Plasma-derived immunoglobulins (PID, CIDP)

Clinical need for plasma-derived immunoglobulins is expanding with global IG demand >US$12bn in 2023 and mid-single-digit CAGR as diagnosis rates and access widen; CSL’s scale — operating ~270 plasma collection centres — and integrated fractionation deliver high share and reliable availability (CSL Behring among top global suppliers). It remains cash-intensive for collection, fractionation and network expansion, but defending share now positions CSL to harvest higher returns as demand grows.

Specialty plasma for rare bleeding disorders

High medical urgency and strong clinician trust drive brisk uptake in growth markets for specialty plasma in rare bleeding disorders; hemophilia A affects about 1 in 5,000 male births and hemophilia B about 1 in 25,000, keeping demand steady. CSL’s deep portfolio and relationships with centers of excellence keep it top‑of‑mind. Ongoing medical education and market access muscle are required; sustained execution can compound into durable leadership.

Recombinant hemophilia therapies (selected assets)

In 2024 switch dynamics and longer‑acting profiles continued to drive recombinant hemophilia category growth; where CSL holds strong positions, share gains plus positive clinical data are sustaining momentum. Competitive heat remains high, keeping promo and access spend elevated, so CSL must keep backing winners to outpace class averages.

- 2024 trend: EHL-driven switch fueling market expansion

- CSL advantage: share gains supported by clinical readouts

- Cost: sustained promo/access investment due to competition

- Priority: double down on top assets to beat class growth

CSL Vifor iron therapies in expanding markets

CSL Vifor iron therapies sit in Stars as CKD and iron‑deficiency care pathways scale: ~850 million people have CKD and ~1.8 billion suffer iron deficiency (WHO/GBD 2023), driving rising hospital and outpatient adoption in 2023–24. Continued market education and tender wins are required; push now while the category is breaking out.

- High prevalence: CKD ~850M; ID ~1.8B

- Adoption: hospital + outpatient growth 2023–24

- Needs: education, tender wins

- Priority: accelerate market capture

Biopharma readies for flu, plasma, hemophilia & CKD/ID growth — scale, R&D, access

CSL Stars: Seqirus rides influenza demand (290,000–650,000 deaths/yr WHO) and pandemic readiness; Behring leads plasma (global IG >US$12bn 2023; ~270 plasma centres); recombinant hemophilia growth sustained by 2024 EHL switches; Vifor scales in CKD/ID (CKD ~850M; ID ~1.8B). Priorities: capacity, next‑gen R&D, market access and focused promo to convert growth into cash flow.

| Product | 2023–24 metric | CSL position | Priority |

|---|---|---|---|

| Seqirus | Influenza burden 290k–650k | Strong gov't share | Capacity/capex |

| Behring | IG >US$12bn | Top supplier; ~270 centres | Collection scale |

| Hemophilia | EHL switch 2024 | Share gains | Back winners |

| Vifor | CKD 850M; ID 1.8B | Growing adoption | Education/tenders |

What is included in the product

Comprehensive BCG Matrix review of CSL's units, with clear quadrant insights and recommendations to invest, hold or divest.

One-page CSL BCG Matrix aligning portfolio pain points to strategy — ready to print, present, or drop into slides.

Cash Cows

Albumin for hospital and critical care

Mature hospital/critical-care albumin has steady, sticky institutional contracts delivering predictable cash flow and low incremental promotion needs; scale drives cost efficiency across plasma sourcing and fractionation, keeping per-unit COGS low. Prioritize manufacturing throughput and regional logistics optimization to preserve high margins and free cash for portfolio reinvestment.

Legacy immunoglobulin indications in mature markets

Established prescriber habits and reimbursement in mature markets keep CSL's legacy immunoglobulin volumes broadly stable, supporting steady annual cash flow; the global IVIG market was roughly USD 18.5 billion in 2024. Brand trust and supply reliability favor CSL, underpinning premium uptake and low churn. Growth is minimal (low-single-digit), but cash conversion remains excellent. Maintain service levels and avoid price leaks to preserve margins.

Seasonal flu vaccines in stable geographies

Seasonal flu vaccines in stable geographies provide forecastable demand via annual procurement cycles and repeat tenders, with global production roughly 500–900 million doses per year. Efficient fill‑finish runs and harvested manufacturing learning curves keep unit costs low, making the franchise cash positive despite routine lifecycle management. Milk revenues while reallocating R&D into next‑gen platforms; Seqirus is among the top three global suppliers.

Established nephrology supportive therapies

Established nephrology supportive therapies are embedded in dialysis protocols with predictable utilization and stable demand; the US dialysis population remains ~550,000 patients (2024), anchoring recurring volume. Competitive set is well known and switching is low, enabling solid margins with modest upkeep; keep contracts tight and operations lean to protect cash flow.

- Embedded protocols: predictable utilization

- Market: US dialysis ~550,000 patients (2024)

- Switching: low, known competitors

- Economics: solid margins, modest upkeep

- Playbook: tight contracts, lean operations

Contracted government supply agreements

Contracted government supply agreements act as cash cows for CSL by smoothing volume and capacity planning through long-term buys; CSL reported FY2024 revenue of about A$13.0 billion, with government programs providing a durable, low-volatility cash base. Once agreements are secured, incremental sales costs are limited and cash visibility is high, supporting predictable free cash flow. Maintaining reliability SLAs above contractual targets preserves renewal rates and pricing leverage.

- Long-term buys: smoothes production planning

- Low incremental sales cost: improves margins

- High cash visibility: reduces volatility

- SLAs critical: drives renewals and pricing

Steady cash: high-margin albumin, IVIG, flu vaccines and nephrology fuel A$13.0bn FY2024

Mature albumin, legacy IVIG and Seqirus flu vaccines plus nephrology therapies and long‑term government contracts generate predictable, high‑margin cash for CSL; FY2024 revenue ~A$13.0bn. IVIG market ~USD18.5bn (2024); US dialysis ~550,000 patients (2024); flu supply 500–900M doses/yr. Prioritize throughput, contract retention and tight SLAs to sustain free cash.

| Cash Cow | 2024 metric | Role |

|---|---|---|

| Albumin | Stable institutional contracts | High margin, low promo |

| IVIG | Global market USD18.5bn | Steady cash flow |

| Seqirus | 500–900M doses/yr | Repeat annual revenue |

| Nephrology | US dialysis ~550k | Recurring demand |

| Govt contracts | Contributes to A$13.0bn | Volume visibility |

Preview = Final Product

CSL BCG Matrix

The file you're previewing is the exact CSL BCG Matrix report you'll receive after purchase. No watermarks, no demo text—just the fully formatted, market-tested analysis ready for strategy meetings. After buying, the final document is delivered immediately for editing, printing, or sharing with stakeholders. It's designed for clarity and action, so there are no surprises.