CSL PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political, economic, social, technological, legal and environmental forces are reshaping CSL’s future—insights that inform investment, strategy and risk planning; buy the full PESTLE now for a ready-to-use, deep-dive report you can apply immediately.

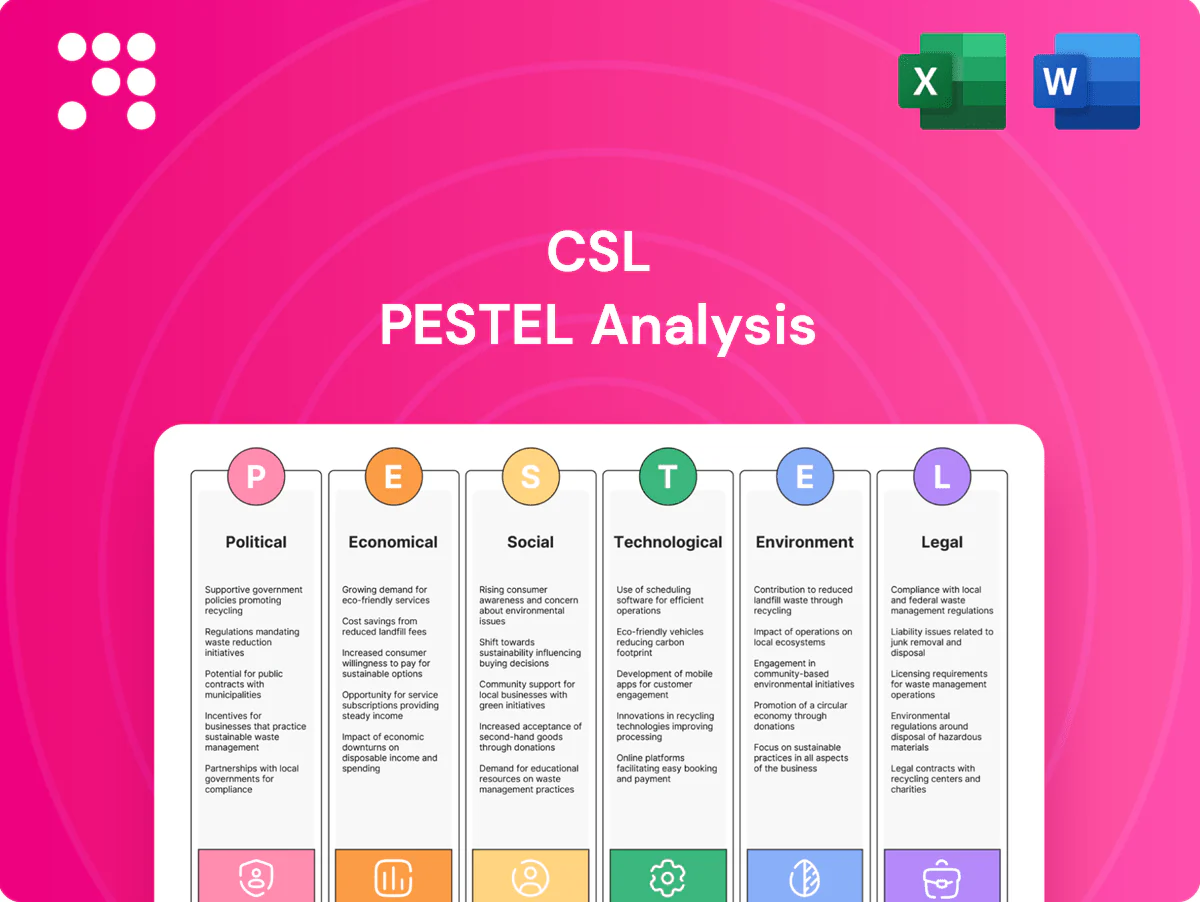

Political factors

Public health funding and vaccine procurement

Government budgets and pandemic-preparedness programs directly affect CSL’s influenza demand—the US alone saw about 171.6 million flu vaccine doses distributed in 2022–23, shaping stockpile and procurement plans. Multi-year tenders and BARDA-style bilateral contracts improve volume visibility and pricing power for suppliers. Rising national self-sufficiency and local fill–finish investments can re-route orders from exporters, while post-election policy shifts can rapidly reprioritize immunization versus rare-disease funding.

Plasma collection policy and donor compensation

National rules on donor remuneration and licensing directly affect plasma input; the United States supplies roughly 70% of plasma used for fractionation, while most EU states prohibit paid donation, constraining supply diversity. Such cross-border differences create sourcing and logistics complexity and can tighten or expand availability and margins. Heightened political scrutiny of donor welfare has intensified compliance and monitoring requirements, raising operating costs.

Drug pricing and reimbursement politics

Price controls and HTA decisions increasingly constrain CSL pricing power: specialty medicines now represent about 48% of global drug spend (IQVIA 2024), and European HTA QALY thresholds (commonly €20k–€50k) pressure biotherapy valuations. Reference pricing and biosimilar entry have cut prices 30–60% in EU markets, squeezing iron therapy economics. Vaccines largely receive public funding but tender discounts (often 20–80% via Gavi/UNICEF) compress margins. Statutory rebates and Medicaid-like clawbacks (e.g., US base rebate 23.1% plus inflation penalties) and reimbursement delays can push cash conversion cycles out by months.

Geopolitics, trade, and supply chain security

Export controls, sanctions and customs delays have disrupted plasma and single-use inputs, pushing some biopharma lead times up by ~20% in 2023–24 and prompting governments to prioritize domestic supplies during health crises (e.g., emergency stockpiles expanded 15–30% in several markets by 2024). Diversification mandates and friend-shoring raise network costs and capex, while political risk insurance and larger inventory buffers are now strategic hedges.

- export-controls: supply lead times +~20% (2023–24)

- domestic-priority: stockpile growth 15–30% (by 2024)

- friend-shoring: higher network capex and OPEX

- mitigants: political-risk insurance, inventory buffers

Regulatory alignment and international standards

Convergence or divergence among FDA, EMA, TGA and NMPA materially alters trial design and time-to-approval: FDA Priority Review targets six months versus a 10-month standard under PDUFA, EMA central procedures aim for 210 active days, and divergent local data requirements can add months to global launches. Priority review and fast-track schemes (e.g., FDA Accelerated Approval pathways) compress market entry but often impose confirmatory post-market commitments tied to public policy, raising lifecycle costs. Political scrutiny of safety signals can force rapid label changes or usage restrictions, as seen in multiple regulatory actions since 2023 that shifted prescribing and reimbursement decisions within weeks.

- Regulatory timelines: FDA 6m priority / 10m standard; EMA 210 active days

- Fast-track impact: accelerates launch but increases post-market obligations

- Lifecycle costs: post-market commitments raise compliance spend and trial burden

- Political risk: safety events can prompt swift label or usage shifts

Political shifts drive vaccine procurement volatility, pricing pressure, plasma supply risk

Political shifts drive demand, procurement and stockpiles (US 171.6M flu doses 2022–23; stockpile growth 15–30% by 2024), reshape pricing via HTA and rebates, and constrain plasma supply (US ~70% of plasma). Export controls raised lead times ~20% (2023–24) and friend-shoring increases capex/OPEX. Regulatory divergence (FDA 6m priority/10m standard; EMA ~210 days) speeds launches but raises post-market costs.

| Metric | Figure | Impact |

|---|---|---|

| Flu doses (US) | 171.6M (22–23) | Procurement volatility |

| Plasma share (US) | ~70% | Supply concentration |

| Lead times | +~20% | Supply risk |

| Regulatory | FDA 6m/10m; EMA 210d | Launch timing |

What is included in the product

Explores how external macro-environmental factors uniquely affect CSL across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific insights and forward-looking scenario analysis; designed for executives, consultants and investors and delivered in clean, report-ready format to identify threats and opportunities.

A concise, visually segmented CSL PESTLE summary that’s easy to drop into presentations, editable for regional or business-line notes, and shareable across teams to quickly align on external risks and market positioning.

Economic factors

Macroeconomic cycles and healthcare budgets

Recessions squeeze payer budgets and can delay elective or non-urgent treatments, even as essential therapies and vaccines remain resilient but encounter tougher price negotiations; US healthcare spending was about 18% of GDP in 2023. Inflation-driven wage, energy and consumable cost increases—US CPI averaged roughly 3.4% in 2024—raise manufacturing and cold-chain expenses. Public budget cycles and tender timing drive stocking patterns and procurement pacing in key markets.

FX exposure and cost base mix

CSL’s predominantly USD/EUR-denominated global sales against an AUD cost base creates both translation and transaction risk, causing reported margins and capital allocation to vary with FX moves. Multi-region manufacturing and sales provide natural hedges that reduce but do not eliminate exposure. Active hedging programs are used to smooth P&L volatility, at direct financial cost and potential opportunity loss.

Plasma supply economics and donor incentives

Donor compensation (commonly 20-60 USD per plasma donation of ~600-800 mL), center throughput and mandatory screening costs are major contributors to COGS for plasma-derived products. Tight labor markets (US unemployment ~3.7% in 2024) have elevated operating expenses and acquisition cost per liter. Scale efficiencies in fractionation blunt unit costs, but competition for donors intensifies in winter peak seasons.

Tender dynamics and payer mix

Seqirus’ influenza revenues remain highly seasonal and hinge on Northern/Southern hemisphere tenders versus private markets; winning national tenders drives volume but often compresses ASPs, while private-channel sales preserve margins. Specialty biotherapies rely on reimbursement in high-income markets for uptake, with slower access in emerging markets. CSL Vifor’s nephrology footprint is exposed to dialysis provider contract dynamics following CSL’s acquisition of Vifor completed in 2022.

- Tender wins = volume, lower price

- Private markets = higher margin, less volume volatility

- Biotherapies need high-income reimbursement for scale

- Vifor sensitive to dialysis provider contracts

Capital intensity and R&D productivity

Biologics manufacturing, plasma fractionation plants and fill–finish lines demand sustained capex (fill–finish typically 20–100m, fractionation facilities often 500m+), while industry clinical success from Phase I to approval remains low (~11%), making pipeline success critical to long-term ROI and valuation. Rising cost of capital (pharma WACC ~8–10% in 2024–25) shifts build‑vs‑partner decisions for new modalities; active portfolio pruning reallocates spend to higher NPV assets.

- Capex: fill–finish 20–100m, fractionation 500m+

- Pipeline success: ~11% Phase I→approval

- Cost of capital: WACC ~8–10% (2024–25)

- Strategy: pruning redirects capital to higher NPV projects

Political shifts drive vaccine procurement volatility, pricing pressure, plasma supply risk

Recessions pressure payer budgets and elective care, while essential therapies/vaccines remain resilient; US health spend ~18% GDP (2023) and 2024 CPI ~3.4% raise manufacturing and cold‑chain costs. FX exposure from USD/EUR sales vs AUD base affects margins despite hedging. Plasma donation costs ~20–60 USD/donation and US unemployment ~3.7% (2024) raise COGS; pharma WACC ~8–10% (2024–25).

| Metric | Value |

|---|---|

| US health spend (2023) | ~18% GDP |

| CPI (2024) | ~3.4% |

| Plasma donation cost | 20–60 USD/donation |

| US unemployment (2024) | ~3.7% |

| Pharma WACC (2024–25) | 8–10% |

What You See Is What You Get

CSL PESTLE Analysis

The preview of the CSL PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure are final with no placeholders or teasers. After checkout you’ll instantly download this same professional file, ready for analysis and presentation.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political, economic, social, technological, legal and environmental forces are reshaping CSL’s future—insights that inform investment, strategy and risk planning; buy the full PESTLE now for a ready-to-use, deep-dive report you can apply immediately.

Political factors

Public health funding and vaccine procurement

Government budgets and pandemic-preparedness programs directly affect CSL’s influenza demand—the US alone saw about 171.6 million flu vaccine doses distributed in 2022–23, shaping stockpile and procurement plans. Multi-year tenders and BARDA-style bilateral contracts improve volume visibility and pricing power for suppliers. Rising national self-sufficiency and local fill–finish investments can re-route orders from exporters, while post-election policy shifts can rapidly reprioritize immunization versus rare-disease funding.

Plasma collection policy and donor compensation

National rules on donor remuneration and licensing directly affect plasma input; the United States supplies roughly 70% of plasma used for fractionation, while most EU states prohibit paid donation, constraining supply diversity. Such cross-border differences create sourcing and logistics complexity and can tighten or expand availability and margins. Heightened political scrutiny of donor welfare has intensified compliance and monitoring requirements, raising operating costs.

Drug pricing and reimbursement politics

Price controls and HTA decisions increasingly constrain CSL pricing power: specialty medicines now represent about 48% of global drug spend (IQVIA 2024), and European HTA QALY thresholds (commonly €20k–€50k) pressure biotherapy valuations. Reference pricing and biosimilar entry have cut prices 30–60% in EU markets, squeezing iron therapy economics. Vaccines largely receive public funding but tender discounts (often 20–80% via Gavi/UNICEF) compress margins. Statutory rebates and Medicaid-like clawbacks (e.g., US base rebate 23.1% plus inflation penalties) and reimbursement delays can push cash conversion cycles out by months.

Geopolitics, trade, and supply chain security

Export controls, sanctions and customs delays have disrupted plasma and single-use inputs, pushing some biopharma lead times up by ~20% in 2023–24 and prompting governments to prioritize domestic supplies during health crises (e.g., emergency stockpiles expanded 15–30% in several markets by 2024). Diversification mandates and friend-shoring raise network costs and capex, while political risk insurance and larger inventory buffers are now strategic hedges.

- export-controls: supply lead times +~20% (2023–24)

- domestic-priority: stockpile growth 15–30% (by 2024)

- friend-shoring: higher network capex and OPEX

- mitigants: political-risk insurance, inventory buffers

Regulatory alignment and international standards

Convergence or divergence among FDA, EMA, TGA and NMPA materially alters trial design and time-to-approval: FDA Priority Review targets six months versus a 10-month standard under PDUFA, EMA central procedures aim for 210 active days, and divergent local data requirements can add months to global launches. Priority review and fast-track schemes (e.g., FDA Accelerated Approval pathways) compress market entry but often impose confirmatory post-market commitments tied to public policy, raising lifecycle costs. Political scrutiny of safety signals can force rapid label changes or usage restrictions, as seen in multiple regulatory actions since 2023 that shifted prescribing and reimbursement decisions within weeks.

- Regulatory timelines: FDA 6m priority / 10m standard; EMA 210 active days

- Fast-track impact: accelerates launch but increases post-market obligations

- Lifecycle costs: post-market commitments raise compliance spend and trial burden

- Political risk: safety events can prompt swift label or usage shifts

Political shifts drive vaccine procurement volatility, pricing pressure, plasma supply risk

Political shifts drive demand, procurement and stockpiles (US 171.6M flu doses 2022–23; stockpile growth 15–30% by 2024), reshape pricing via HTA and rebates, and constrain plasma supply (US ~70% of plasma). Export controls raised lead times ~20% (2023–24) and friend-shoring increases capex/OPEX. Regulatory divergence (FDA 6m priority/10m standard; EMA ~210 days) speeds launches but raises post-market costs.

| Metric | Figure | Impact |

|---|---|---|

| Flu doses (US) | 171.6M (22–23) | Procurement volatility |

| Plasma share (US) | ~70% | Supply concentration |

| Lead times | +~20% | Supply risk |

| Regulatory | FDA 6m/10m; EMA 210d | Launch timing |

What is included in the product

Explores how external macro-environmental factors uniquely affect CSL across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific insights and forward-looking scenario analysis; designed for executives, consultants and investors and delivered in clean, report-ready format to identify threats and opportunities.

A concise, visually segmented CSL PESTLE summary that’s easy to drop into presentations, editable for regional or business-line notes, and shareable across teams to quickly align on external risks and market positioning.

Economic factors

Macroeconomic cycles and healthcare budgets

Recessions squeeze payer budgets and can delay elective or non-urgent treatments, even as essential therapies and vaccines remain resilient but encounter tougher price negotiations; US healthcare spending was about 18% of GDP in 2023. Inflation-driven wage, energy and consumable cost increases—US CPI averaged roughly 3.4% in 2024—raise manufacturing and cold-chain expenses. Public budget cycles and tender timing drive stocking patterns and procurement pacing in key markets.

FX exposure and cost base mix

CSL’s predominantly USD/EUR-denominated global sales against an AUD cost base creates both translation and transaction risk, causing reported margins and capital allocation to vary with FX moves. Multi-region manufacturing and sales provide natural hedges that reduce but do not eliminate exposure. Active hedging programs are used to smooth P&L volatility, at direct financial cost and potential opportunity loss.

Plasma supply economics and donor incentives

Donor compensation (commonly 20-60 USD per plasma donation of ~600-800 mL), center throughput and mandatory screening costs are major contributors to COGS for plasma-derived products. Tight labor markets (US unemployment ~3.7% in 2024) have elevated operating expenses and acquisition cost per liter. Scale efficiencies in fractionation blunt unit costs, but competition for donors intensifies in winter peak seasons.

Tender dynamics and payer mix

Seqirus’ influenza revenues remain highly seasonal and hinge on Northern/Southern hemisphere tenders versus private markets; winning national tenders drives volume but often compresses ASPs, while private-channel sales preserve margins. Specialty biotherapies rely on reimbursement in high-income markets for uptake, with slower access in emerging markets. CSL Vifor’s nephrology footprint is exposed to dialysis provider contract dynamics following CSL’s acquisition of Vifor completed in 2022.

- Tender wins = volume, lower price

- Private markets = higher margin, less volume volatility

- Biotherapies need high-income reimbursement for scale

- Vifor sensitive to dialysis provider contracts

Capital intensity and R&D productivity

Biologics manufacturing, plasma fractionation plants and fill–finish lines demand sustained capex (fill–finish typically 20–100m, fractionation facilities often 500m+), while industry clinical success from Phase I to approval remains low (~11%), making pipeline success critical to long-term ROI and valuation. Rising cost of capital (pharma WACC ~8–10% in 2024–25) shifts build‑vs‑partner decisions for new modalities; active portfolio pruning reallocates spend to higher NPV assets.

- Capex: fill–finish 20–100m, fractionation 500m+

- Pipeline success: ~11% Phase I→approval

- Cost of capital: WACC ~8–10% (2024–25)

- Strategy: pruning redirects capital to higher NPV projects

Political shifts drive vaccine procurement volatility, pricing pressure, plasma supply risk

Recessions pressure payer budgets and elective care, while essential therapies/vaccines remain resilient; US health spend ~18% GDP (2023) and 2024 CPI ~3.4% raise manufacturing and cold‑chain costs. FX exposure from USD/EUR sales vs AUD base affects margins despite hedging. Plasma donation costs ~20–60 USD/donation and US unemployment ~3.7% (2024) raise COGS; pharma WACC ~8–10% (2024–25).

| Metric | Value |

|---|---|

| US health spend (2023) | ~18% GDP |

| CPI (2024) | ~3.4% |

| Plasma donation cost | 20–60 USD/donation |

| US unemployment (2024) | ~3.7% |

| Pharma WACC (2024–25) | 8–10% |

What You See Is What You Get

CSL PESTLE Analysis

The preview of the CSL PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure are final with no placeholders or teasers. After checkout you’ll instantly download this same professional file, ready for analysis and presentation.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political, economic, social, technological, legal and environmental forces are reshaping CSL’s future—insights that inform investment, strategy and risk planning; buy the full PESTLE now for a ready-to-use, deep-dive report you can apply immediately.

Political factors

Public health funding and vaccine procurement

Government budgets and pandemic-preparedness programs directly affect CSL’s influenza demand—the US alone saw about 171.6 million flu vaccine doses distributed in 2022–23, shaping stockpile and procurement plans. Multi-year tenders and BARDA-style bilateral contracts improve volume visibility and pricing power for suppliers. Rising national self-sufficiency and local fill–finish investments can re-route orders from exporters, while post-election policy shifts can rapidly reprioritize immunization versus rare-disease funding.

Plasma collection policy and donor compensation

National rules on donor remuneration and licensing directly affect plasma input; the United States supplies roughly 70% of plasma used for fractionation, while most EU states prohibit paid donation, constraining supply diversity. Such cross-border differences create sourcing and logistics complexity and can tighten or expand availability and margins. Heightened political scrutiny of donor welfare has intensified compliance and monitoring requirements, raising operating costs.

Drug pricing and reimbursement politics

Price controls and HTA decisions increasingly constrain CSL pricing power: specialty medicines now represent about 48% of global drug spend (IQVIA 2024), and European HTA QALY thresholds (commonly €20k–€50k) pressure biotherapy valuations. Reference pricing and biosimilar entry have cut prices 30–60% in EU markets, squeezing iron therapy economics. Vaccines largely receive public funding but tender discounts (often 20–80% via Gavi/UNICEF) compress margins. Statutory rebates and Medicaid-like clawbacks (e.g., US base rebate 23.1% plus inflation penalties) and reimbursement delays can push cash conversion cycles out by months.

Geopolitics, trade, and supply chain security

Export controls, sanctions and customs delays have disrupted plasma and single-use inputs, pushing some biopharma lead times up by ~20% in 2023–24 and prompting governments to prioritize domestic supplies during health crises (e.g., emergency stockpiles expanded 15–30% in several markets by 2024). Diversification mandates and friend-shoring raise network costs and capex, while political risk insurance and larger inventory buffers are now strategic hedges.

- export-controls: supply lead times +~20% (2023–24)

- domestic-priority: stockpile growth 15–30% (by 2024)

- friend-shoring: higher network capex and OPEX

- mitigants: political-risk insurance, inventory buffers

Regulatory alignment and international standards

Convergence or divergence among FDA, EMA, TGA and NMPA materially alters trial design and time-to-approval: FDA Priority Review targets six months versus a 10-month standard under PDUFA, EMA central procedures aim for 210 active days, and divergent local data requirements can add months to global launches. Priority review and fast-track schemes (e.g., FDA Accelerated Approval pathways) compress market entry but often impose confirmatory post-market commitments tied to public policy, raising lifecycle costs. Political scrutiny of safety signals can force rapid label changes or usage restrictions, as seen in multiple regulatory actions since 2023 that shifted prescribing and reimbursement decisions within weeks.

- Regulatory timelines: FDA 6m priority / 10m standard; EMA 210 active days

- Fast-track impact: accelerates launch but increases post-market obligations

- Lifecycle costs: post-market commitments raise compliance spend and trial burden

- Political risk: safety events can prompt swift label or usage shifts

Political shifts drive vaccine procurement volatility, pricing pressure, plasma supply risk

Political shifts drive demand, procurement and stockpiles (US 171.6M flu doses 2022–23; stockpile growth 15–30% by 2024), reshape pricing via HTA and rebates, and constrain plasma supply (US ~70% of plasma). Export controls raised lead times ~20% (2023–24) and friend-shoring increases capex/OPEX. Regulatory divergence (FDA 6m priority/10m standard; EMA ~210 days) speeds launches but raises post-market costs.

| Metric | Figure | Impact |

|---|---|---|

| Flu doses (US) | 171.6M (22–23) | Procurement volatility |

| Plasma share (US) | ~70% | Supply concentration |

| Lead times | +~20% | Supply risk |

| Regulatory | FDA 6m/10m; EMA 210d | Launch timing |

What is included in the product

Explores how external macro-environmental factors uniquely affect CSL across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific insights and forward-looking scenario analysis; designed for executives, consultants and investors and delivered in clean, report-ready format to identify threats and opportunities.

A concise, visually segmented CSL PESTLE summary that’s easy to drop into presentations, editable for regional or business-line notes, and shareable across teams to quickly align on external risks and market positioning.

Economic factors

Macroeconomic cycles and healthcare budgets

Recessions squeeze payer budgets and can delay elective or non-urgent treatments, even as essential therapies and vaccines remain resilient but encounter tougher price negotiations; US healthcare spending was about 18% of GDP in 2023. Inflation-driven wage, energy and consumable cost increases—US CPI averaged roughly 3.4% in 2024—raise manufacturing and cold-chain expenses. Public budget cycles and tender timing drive stocking patterns and procurement pacing in key markets.

FX exposure and cost base mix

CSL’s predominantly USD/EUR-denominated global sales against an AUD cost base creates both translation and transaction risk, causing reported margins and capital allocation to vary with FX moves. Multi-region manufacturing and sales provide natural hedges that reduce but do not eliminate exposure. Active hedging programs are used to smooth P&L volatility, at direct financial cost and potential opportunity loss.

Plasma supply economics and donor incentives

Donor compensation (commonly 20-60 USD per plasma donation of ~600-800 mL), center throughput and mandatory screening costs are major contributors to COGS for plasma-derived products. Tight labor markets (US unemployment ~3.7% in 2024) have elevated operating expenses and acquisition cost per liter. Scale efficiencies in fractionation blunt unit costs, but competition for donors intensifies in winter peak seasons.

Tender dynamics and payer mix

Seqirus’ influenza revenues remain highly seasonal and hinge on Northern/Southern hemisphere tenders versus private markets; winning national tenders drives volume but often compresses ASPs, while private-channel sales preserve margins. Specialty biotherapies rely on reimbursement in high-income markets for uptake, with slower access in emerging markets. CSL Vifor’s nephrology footprint is exposed to dialysis provider contract dynamics following CSL’s acquisition of Vifor completed in 2022.

- Tender wins = volume, lower price

- Private markets = higher margin, less volume volatility

- Biotherapies need high-income reimbursement for scale

- Vifor sensitive to dialysis provider contracts

Capital intensity and R&D productivity

Biologics manufacturing, plasma fractionation plants and fill–finish lines demand sustained capex (fill–finish typically 20–100m, fractionation facilities often 500m+), while industry clinical success from Phase I to approval remains low (~11%), making pipeline success critical to long-term ROI and valuation. Rising cost of capital (pharma WACC ~8–10% in 2024–25) shifts build‑vs‑partner decisions for new modalities; active portfolio pruning reallocates spend to higher NPV assets.

- Capex: fill–finish 20–100m, fractionation 500m+

- Pipeline success: ~11% Phase I→approval

- Cost of capital: WACC ~8–10% (2024–25)

- Strategy: pruning redirects capital to higher NPV projects

Political shifts drive vaccine procurement volatility, pricing pressure, plasma supply risk

Recessions pressure payer budgets and elective care, while essential therapies/vaccines remain resilient; US health spend ~18% GDP (2023) and 2024 CPI ~3.4% raise manufacturing and cold‑chain costs. FX exposure from USD/EUR sales vs AUD base affects margins despite hedging. Plasma donation costs ~20–60 USD/donation and US unemployment ~3.7% (2024) raise COGS; pharma WACC ~8–10% (2024–25).

| Metric | Value |

|---|---|

| US health spend (2023) | ~18% GDP |

| CPI (2024) | ~3.4% |

| Plasma donation cost | 20–60 USD/donation |

| US unemployment (2024) | ~3.7% |

| Pharma WACC (2024–25) | 8–10% |

What You See Is What You Get

CSL PESTLE Analysis

The preview of the CSL PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure are final with no placeholders or teasers. After checkout you’ll instantly download this same professional file, ready for analysis and presentation.