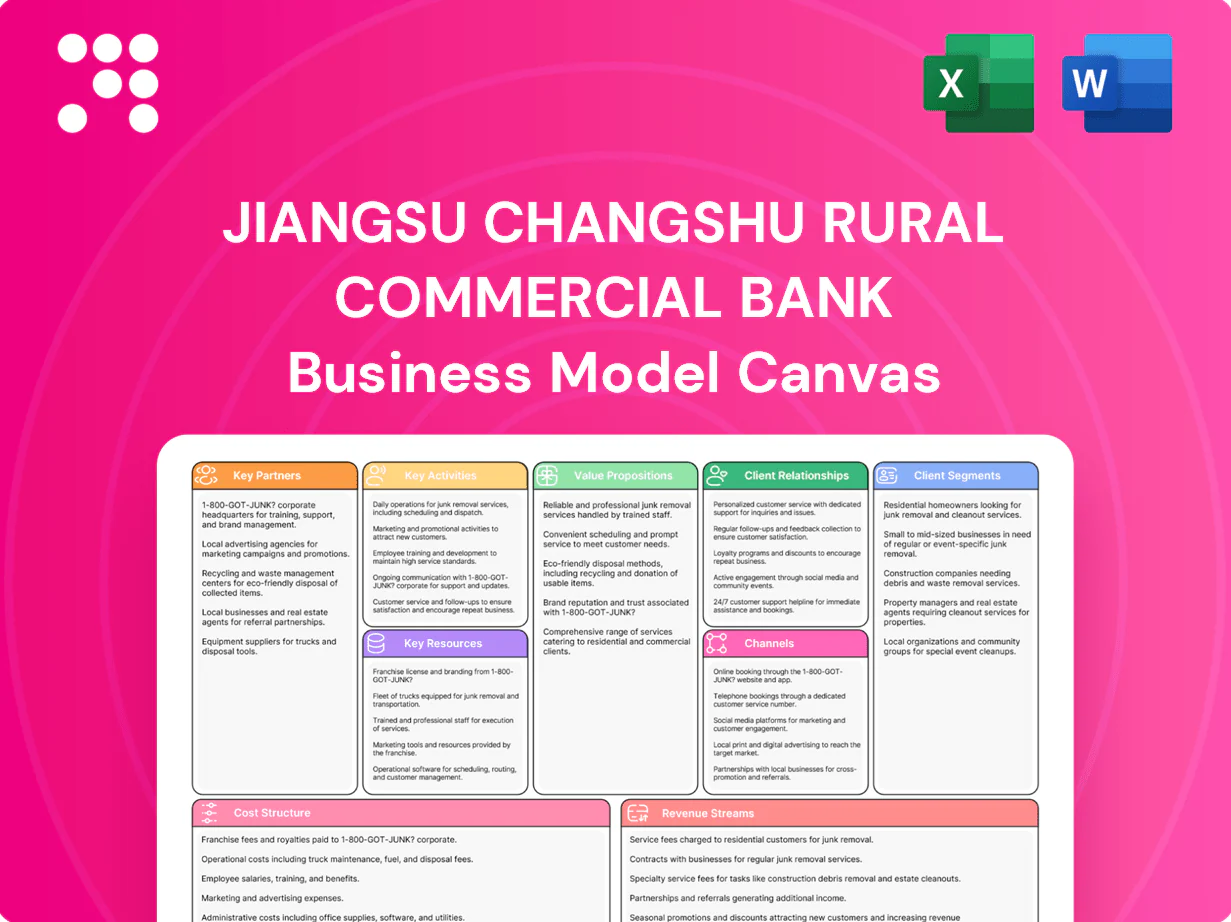

Jiangsu Changshu Rural Commercial Bank Business Model Canvas

Business Model Canvas: Rural Bank Strategy, Revenue Streams & Growth Levers

Unlock the full strategic blueprint behind Jiangsu Changshu Rural Commercial Bank with our Business Model Canvas. This in-depth canvas maps value propositions, customer segments, revenue streams and cost structure—ideal for investors, analysts and entrepreneurs. Download the editable Word and Excel files to benchmark strategy, identify growth levers, and apply insights immediately.

Partnerships

Local government and regulators

Partnerships with municipal authorities and the CBIRC/PBoC secure licensing and policy alignment, supporting Changshu RCB’s role in local financial stability. Coordination channels enable delivery of rural revitalization programs and inclusive finance quotas, targeting underserved households and SMEs. These links provide access to incentives and risk-sharing schemes for agriculture and small businesses, and ongoing dialogue in 2024 strengthened compliance and local reputation.

Agricultural bureaus and cooperatives

Alliances with agricultural bureaus and cooperatives supply verified farm registries and seasonal calendars that allow the bank to tailor crop, livestock, and machinery loans with appropriate tenors. Cooperatives aggregate members for efficient credit screening and disbursement, reducing unit servicing costs and default risk. Joint programs with bureaus deliver financial literacy training and drive digital adoption among rural clients, improving loan uptake and repayment behavior.

Credit guarantee and financing platforms

Guarantee companies reduce collateral gaps for SMEs and micro-entrepreneurs, enabling lending where tangible collateral is scarce; SMEs accounted for over 60% of China GDP and 80% of urban employment in 2024. Risk-sharing with guarantors lowers pricing and can raise approval rates materially, improving NPL resilience. Provincial financing platforms in Jiangsu streamline documentation and channel subsidies, supporting diversification and better asset quality.

Payment networks and fintechs

Partnerships with UnionPay, national clearing houses and fintech API providers extend Changshu RCBs acceptance and settlement rails; in 2024 UnionPay remained China’s largest card network by transaction volume, while fintech APIs enabled seamless QR, mobile and e-commerce payments, raising authorization uptime and layered fraud controls to improve UX and conversion. Co-branded services increase product stickiness and cross-sell opportunities.

- UnionPay: largest domestic card network

- Clearing houses: faster settlement

- Fintech APIs: QR/mobile/e‑commerce

- Benefits: higher uptime, better fraud controls, deeper customer stickiness

Correspondent and interbank partners

In 2024 Jiangsu Changshu Rural Commercial Bank used correspondent and interbank partners to secure policy‑bank liquidity and RMB clearing, while treasury collaborations provided FX, bill handling and interbank placement channels that enabled larger‑ticket syndications for local corporates.

- Liquidity lines from city and policy banks

- Treasury support for FX, bills, placements

- Syndication capacity for larger local loans

- Network access expands products without heavy capex

Strategic municipal and fintech partnerships drive rural lending, compliance and digital payments

Changshu RCB’s key partnerships with municipal authorities and regulators secure licensing, policy alignment and delivery channels for rural revitalization; 2024 cooperation strengthened compliance and local standing. Agricultural bureaus and cooperatives enable targeted crop and machinery lending and digital adoption. Guarantee firms and correspondent banks close collateral and liquidity gaps; UnionPay and fintech APIs expand payments and customer stickiness.

| Partner | Role | 2024 data |

|---|---|---|

| Municipal/CBIRC/PBoC | Policy, licensing, program channels | Enhanced compliance 2024 |

| Agricultural bureaus/coops | Client verification, aggregation | Supports targeted seasonal loans |

| Guarantee companies | Risk sharing, collateral substitution | Supports SME lending; SMEs ≈60% GDP, 80% urban employment (2024) |

| UnionPay/fintech APIs | Payments, settlement, digital UX | UnionPay largest card network by transaction volume (2024) |

| Correspondent/treasury partners | Liquidity, FX, syndication | Enables larger local syndications |

What is included in the product

A concise, pre-written Business Model Canvas for Jiangsu Changshu Rural Commercial Bank detailing customer segments, channels, value propositions, revenue/cost streams and key resources/partners across the 9 BMC blocks, with competitive advantages, SWOT-linked risks/opportunities and polished narratives for presentations, investor discussions and strategic planning.

High-level view of Jiangsu Changshu Rural Commercial Bank’s business model with editable cells to quickly surface customer pain points and operational bottlenecks; saves hours by structuring strategy, risk and channel solutions into a single, shareable one-page snapshot for teams and boards.

Activities

Deposit mobilization

Design and price savings, current and time deposits tailored for households and SMEs, emphasizing competitive tiered rates and digital onboarding to deepen relationships. Run localized campaigns and community outreach to grow low-cost CASA balances and capture deposits from local SMEs. Continuously manage liquidity forecasts and interest-rate gaps using daily gap analysis and stress tests. Maintain branch and digital service quality metrics to reduce churn and boost retention.

Credit underwriting and monitoring

Assess SME, agricultural and retail borrowers using cashflow-based underwriting, stress-testing projections and sector benchmarks; set exposure limits, collateral requirements and covenants calibrated to the bank’s risk appetite. Post-lending reviews and early-warning monitoring occur at least quarterly to detect deterioration; China’s banking NPL ratio was about 1.31% in 2023, guiding tolerance levels. Collections and restructuring follow defined playbooks to contain losses and preserve recoveries.

Payments and settlement operations

Process domestic transfers, payroll and merchant acquiring with daily clearing, reconciliation and exception handling to meet operational deadlines and regulatory reporting. Maintain AML/CFT screening and sanctions checks in line with China’s Anti-Money Laundering Law and PBOC requirements effective since 2022. Continuously optimize STP workflows to lower operational costs and reduce manual exceptions, targeting industry-standard efficiency improvements.

Risk and compliance management

Operate robust frameworks for credit, market, liquidity, and operational risk, monitoring NPLs, coverage ratios and concentration metrics; perform KYC/AML, regulatory reporting and internal audits; run periodic stress tests and promptly update policies to reflect CBIRC guidance and market signals.

- Frameworks: credit, market, liquidity, operational

- Monitoring: NPLs, coverage, concentration

- Compliance: KYC/AML, reporting, internal audit

- Controls: stress testing, policy updates per regulator

Digital channel development

Drive digital onboarding to achieve 40% CASA with cashflow SME underwriting

Design and price deposit products and digital onboarding to grow low-cost CASA; cashflow‑based SME and agri underwriting with quarterly early‑warning reviews; process payments, AML/KYC and STP optimization; run credit, market, liquidity risk frameworks and cybersecurity upgrades to support digital growth.

| Metric | Value |

|---|---|

| CASA share target | 40% |

| NPL (China, 2023) | 1.31% |

| Mobile pay users (2024) | 1B+ |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the exact Jiangsu Changshu Rural Commercial Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this file contains the same structured, editable content and layout. After payment you'll download the full, ready-to-use document for editing, presenting, and sharing.

Business Model Canvas: Rural Bank Strategy, Revenue Streams & Growth Levers

Unlock the full strategic blueprint behind Jiangsu Changshu Rural Commercial Bank with our Business Model Canvas. This in-depth canvas maps value propositions, customer segments, revenue streams and cost structure—ideal for investors, analysts and entrepreneurs. Download the editable Word and Excel files to benchmark strategy, identify growth levers, and apply insights immediately.

Partnerships

Local government and regulators

Partnerships with municipal authorities and the CBIRC/PBoC secure licensing and policy alignment, supporting Changshu RCB’s role in local financial stability. Coordination channels enable delivery of rural revitalization programs and inclusive finance quotas, targeting underserved households and SMEs. These links provide access to incentives and risk-sharing schemes for agriculture and small businesses, and ongoing dialogue in 2024 strengthened compliance and local reputation.

Agricultural bureaus and cooperatives

Alliances with agricultural bureaus and cooperatives supply verified farm registries and seasonal calendars that allow the bank to tailor crop, livestock, and machinery loans with appropriate tenors. Cooperatives aggregate members for efficient credit screening and disbursement, reducing unit servicing costs and default risk. Joint programs with bureaus deliver financial literacy training and drive digital adoption among rural clients, improving loan uptake and repayment behavior.

Credit guarantee and financing platforms

Guarantee companies reduce collateral gaps for SMEs and micro-entrepreneurs, enabling lending where tangible collateral is scarce; SMEs accounted for over 60% of China GDP and 80% of urban employment in 2024. Risk-sharing with guarantors lowers pricing and can raise approval rates materially, improving NPL resilience. Provincial financing platforms in Jiangsu streamline documentation and channel subsidies, supporting diversification and better asset quality.

Payment networks and fintechs

Partnerships with UnionPay, national clearing houses and fintech API providers extend Changshu RCBs acceptance and settlement rails; in 2024 UnionPay remained China’s largest card network by transaction volume, while fintech APIs enabled seamless QR, mobile and e-commerce payments, raising authorization uptime and layered fraud controls to improve UX and conversion. Co-branded services increase product stickiness and cross-sell opportunities.

- UnionPay: largest domestic card network

- Clearing houses: faster settlement

- Fintech APIs: QR/mobile/e‑commerce

- Benefits: higher uptime, better fraud controls, deeper customer stickiness

Correspondent and interbank partners

In 2024 Jiangsu Changshu Rural Commercial Bank used correspondent and interbank partners to secure policy‑bank liquidity and RMB clearing, while treasury collaborations provided FX, bill handling and interbank placement channels that enabled larger‑ticket syndications for local corporates.

- Liquidity lines from city and policy banks

- Treasury support for FX, bills, placements

- Syndication capacity for larger local loans

- Network access expands products without heavy capex

Strategic municipal and fintech partnerships drive rural lending, compliance and digital payments

Changshu RCB’s key partnerships with municipal authorities and regulators secure licensing, policy alignment and delivery channels for rural revitalization; 2024 cooperation strengthened compliance and local standing. Agricultural bureaus and cooperatives enable targeted crop and machinery lending and digital adoption. Guarantee firms and correspondent banks close collateral and liquidity gaps; UnionPay and fintech APIs expand payments and customer stickiness.

| Partner | Role | 2024 data |

|---|---|---|

| Municipal/CBIRC/PBoC | Policy, licensing, program channels | Enhanced compliance 2024 |

| Agricultural bureaus/coops | Client verification, aggregation | Supports targeted seasonal loans |

| Guarantee companies | Risk sharing, collateral substitution | Supports SME lending; SMEs ≈60% GDP, 80% urban employment (2024) |

| UnionPay/fintech APIs | Payments, settlement, digital UX | UnionPay largest card network by transaction volume (2024) |

| Correspondent/treasury partners | Liquidity, FX, syndication | Enables larger local syndications |

What is included in the product

A concise, pre-written Business Model Canvas for Jiangsu Changshu Rural Commercial Bank detailing customer segments, channels, value propositions, revenue/cost streams and key resources/partners across the 9 BMC blocks, with competitive advantages, SWOT-linked risks/opportunities and polished narratives for presentations, investor discussions and strategic planning.

High-level view of Jiangsu Changshu Rural Commercial Bank’s business model with editable cells to quickly surface customer pain points and operational bottlenecks; saves hours by structuring strategy, risk and channel solutions into a single, shareable one-page snapshot for teams and boards.

Activities

Deposit mobilization

Design and price savings, current and time deposits tailored for households and SMEs, emphasizing competitive tiered rates and digital onboarding to deepen relationships. Run localized campaigns and community outreach to grow low-cost CASA balances and capture deposits from local SMEs. Continuously manage liquidity forecasts and interest-rate gaps using daily gap analysis and stress tests. Maintain branch and digital service quality metrics to reduce churn and boost retention.

Credit underwriting and monitoring

Assess SME, agricultural and retail borrowers using cashflow-based underwriting, stress-testing projections and sector benchmarks; set exposure limits, collateral requirements and covenants calibrated to the bank’s risk appetite. Post-lending reviews and early-warning monitoring occur at least quarterly to detect deterioration; China’s banking NPL ratio was about 1.31% in 2023, guiding tolerance levels. Collections and restructuring follow defined playbooks to contain losses and preserve recoveries.

Payments and settlement operations

Process domestic transfers, payroll and merchant acquiring with daily clearing, reconciliation and exception handling to meet operational deadlines and regulatory reporting. Maintain AML/CFT screening and sanctions checks in line with China’s Anti-Money Laundering Law and PBOC requirements effective since 2022. Continuously optimize STP workflows to lower operational costs and reduce manual exceptions, targeting industry-standard efficiency improvements.

Risk and compliance management

Operate robust frameworks for credit, market, liquidity, and operational risk, monitoring NPLs, coverage ratios and concentration metrics; perform KYC/AML, regulatory reporting and internal audits; run periodic stress tests and promptly update policies to reflect CBIRC guidance and market signals.

- Frameworks: credit, market, liquidity, operational

- Monitoring: NPLs, coverage, concentration

- Compliance: KYC/AML, reporting, internal audit

- Controls: stress testing, policy updates per regulator

Digital channel development

Drive digital onboarding to achieve 40% CASA with cashflow SME underwriting

Design and price deposit products and digital onboarding to grow low-cost CASA; cashflow‑based SME and agri underwriting with quarterly early‑warning reviews; process payments, AML/KYC and STP optimization; run credit, market, liquidity risk frameworks and cybersecurity upgrades to support digital growth.

| Metric | Value |

|---|---|

| CASA share target | 40% |

| NPL (China, 2023) | 1.31% |

| Mobile pay users (2024) | 1B+ |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the exact Jiangsu Changshu Rural Commercial Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this file contains the same structured, editable content and layout. After payment you'll download the full, ready-to-use document for editing, presenting, and sharing.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: Rural Bank Strategy, Revenue Streams & Growth Levers

Unlock the full strategic blueprint behind Jiangsu Changshu Rural Commercial Bank with our Business Model Canvas. This in-depth canvas maps value propositions, customer segments, revenue streams and cost structure—ideal for investors, analysts and entrepreneurs. Download the editable Word and Excel files to benchmark strategy, identify growth levers, and apply insights immediately.

Partnerships

Local government and regulators

Partnerships with municipal authorities and the CBIRC/PBoC secure licensing and policy alignment, supporting Changshu RCB’s role in local financial stability. Coordination channels enable delivery of rural revitalization programs and inclusive finance quotas, targeting underserved households and SMEs. These links provide access to incentives and risk-sharing schemes for agriculture and small businesses, and ongoing dialogue in 2024 strengthened compliance and local reputation.

Agricultural bureaus and cooperatives

Alliances with agricultural bureaus and cooperatives supply verified farm registries and seasonal calendars that allow the bank to tailor crop, livestock, and machinery loans with appropriate tenors. Cooperatives aggregate members for efficient credit screening and disbursement, reducing unit servicing costs and default risk. Joint programs with bureaus deliver financial literacy training and drive digital adoption among rural clients, improving loan uptake and repayment behavior.

Credit guarantee and financing platforms

Guarantee companies reduce collateral gaps for SMEs and micro-entrepreneurs, enabling lending where tangible collateral is scarce; SMEs accounted for over 60% of China GDP and 80% of urban employment in 2024. Risk-sharing with guarantors lowers pricing and can raise approval rates materially, improving NPL resilience. Provincial financing platforms in Jiangsu streamline documentation and channel subsidies, supporting diversification and better asset quality.

Payment networks and fintechs

Partnerships with UnionPay, national clearing houses and fintech API providers extend Changshu RCBs acceptance and settlement rails; in 2024 UnionPay remained China’s largest card network by transaction volume, while fintech APIs enabled seamless QR, mobile and e-commerce payments, raising authorization uptime and layered fraud controls to improve UX and conversion. Co-branded services increase product stickiness and cross-sell opportunities.

- UnionPay: largest domestic card network

- Clearing houses: faster settlement

- Fintech APIs: QR/mobile/e‑commerce

- Benefits: higher uptime, better fraud controls, deeper customer stickiness

Correspondent and interbank partners

In 2024 Jiangsu Changshu Rural Commercial Bank used correspondent and interbank partners to secure policy‑bank liquidity and RMB clearing, while treasury collaborations provided FX, bill handling and interbank placement channels that enabled larger‑ticket syndications for local corporates.

- Liquidity lines from city and policy banks

- Treasury support for FX, bills, placements

- Syndication capacity for larger local loans

- Network access expands products without heavy capex

Strategic municipal and fintech partnerships drive rural lending, compliance and digital payments

Changshu RCB’s key partnerships with municipal authorities and regulators secure licensing, policy alignment and delivery channels for rural revitalization; 2024 cooperation strengthened compliance and local standing. Agricultural bureaus and cooperatives enable targeted crop and machinery lending and digital adoption. Guarantee firms and correspondent banks close collateral and liquidity gaps; UnionPay and fintech APIs expand payments and customer stickiness.

| Partner | Role | 2024 data |

|---|---|---|

| Municipal/CBIRC/PBoC | Policy, licensing, program channels | Enhanced compliance 2024 |

| Agricultural bureaus/coops | Client verification, aggregation | Supports targeted seasonal loans |

| Guarantee companies | Risk sharing, collateral substitution | Supports SME lending; SMEs ≈60% GDP, 80% urban employment (2024) |

| UnionPay/fintech APIs | Payments, settlement, digital UX | UnionPay largest card network by transaction volume (2024) |

| Correspondent/treasury partners | Liquidity, FX, syndication | Enables larger local syndications |

What is included in the product

A concise, pre-written Business Model Canvas for Jiangsu Changshu Rural Commercial Bank detailing customer segments, channels, value propositions, revenue/cost streams and key resources/partners across the 9 BMC blocks, with competitive advantages, SWOT-linked risks/opportunities and polished narratives for presentations, investor discussions and strategic planning.

High-level view of Jiangsu Changshu Rural Commercial Bank’s business model with editable cells to quickly surface customer pain points and operational bottlenecks; saves hours by structuring strategy, risk and channel solutions into a single, shareable one-page snapshot for teams and boards.

Activities

Deposit mobilization

Design and price savings, current and time deposits tailored for households and SMEs, emphasizing competitive tiered rates and digital onboarding to deepen relationships. Run localized campaigns and community outreach to grow low-cost CASA balances and capture deposits from local SMEs. Continuously manage liquidity forecasts and interest-rate gaps using daily gap analysis and stress tests. Maintain branch and digital service quality metrics to reduce churn and boost retention.

Credit underwriting and monitoring

Assess SME, agricultural and retail borrowers using cashflow-based underwriting, stress-testing projections and sector benchmarks; set exposure limits, collateral requirements and covenants calibrated to the bank’s risk appetite. Post-lending reviews and early-warning monitoring occur at least quarterly to detect deterioration; China’s banking NPL ratio was about 1.31% in 2023, guiding tolerance levels. Collections and restructuring follow defined playbooks to contain losses and preserve recoveries.

Payments and settlement operations

Process domestic transfers, payroll and merchant acquiring with daily clearing, reconciliation and exception handling to meet operational deadlines and regulatory reporting. Maintain AML/CFT screening and sanctions checks in line with China’s Anti-Money Laundering Law and PBOC requirements effective since 2022. Continuously optimize STP workflows to lower operational costs and reduce manual exceptions, targeting industry-standard efficiency improvements.

Risk and compliance management

Operate robust frameworks for credit, market, liquidity, and operational risk, monitoring NPLs, coverage ratios and concentration metrics; perform KYC/AML, regulatory reporting and internal audits; run periodic stress tests and promptly update policies to reflect CBIRC guidance and market signals.

- Frameworks: credit, market, liquidity, operational

- Monitoring: NPLs, coverage, concentration

- Compliance: KYC/AML, reporting, internal audit

- Controls: stress testing, policy updates per regulator

Digital channel development

Drive digital onboarding to achieve 40% CASA with cashflow SME underwriting

Design and price deposit products and digital onboarding to grow low-cost CASA; cashflow‑based SME and agri underwriting with quarterly early‑warning reviews; process payments, AML/KYC and STP optimization; run credit, market, liquidity risk frameworks and cybersecurity upgrades to support digital growth.

| Metric | Value |

|---|---|

| CASA share target | 40% |

| NPL (China, 2023) | 1.31% |

| Mobile pay users (2024) | 1B+ |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the exact Jiangsu Changshu Rural Commercial Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this file contains the same structured, editable content and layout. After payment you'll download the full, ready-to-use document for editing, presenting, and sharing.