C&S Wholesale Grocers Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

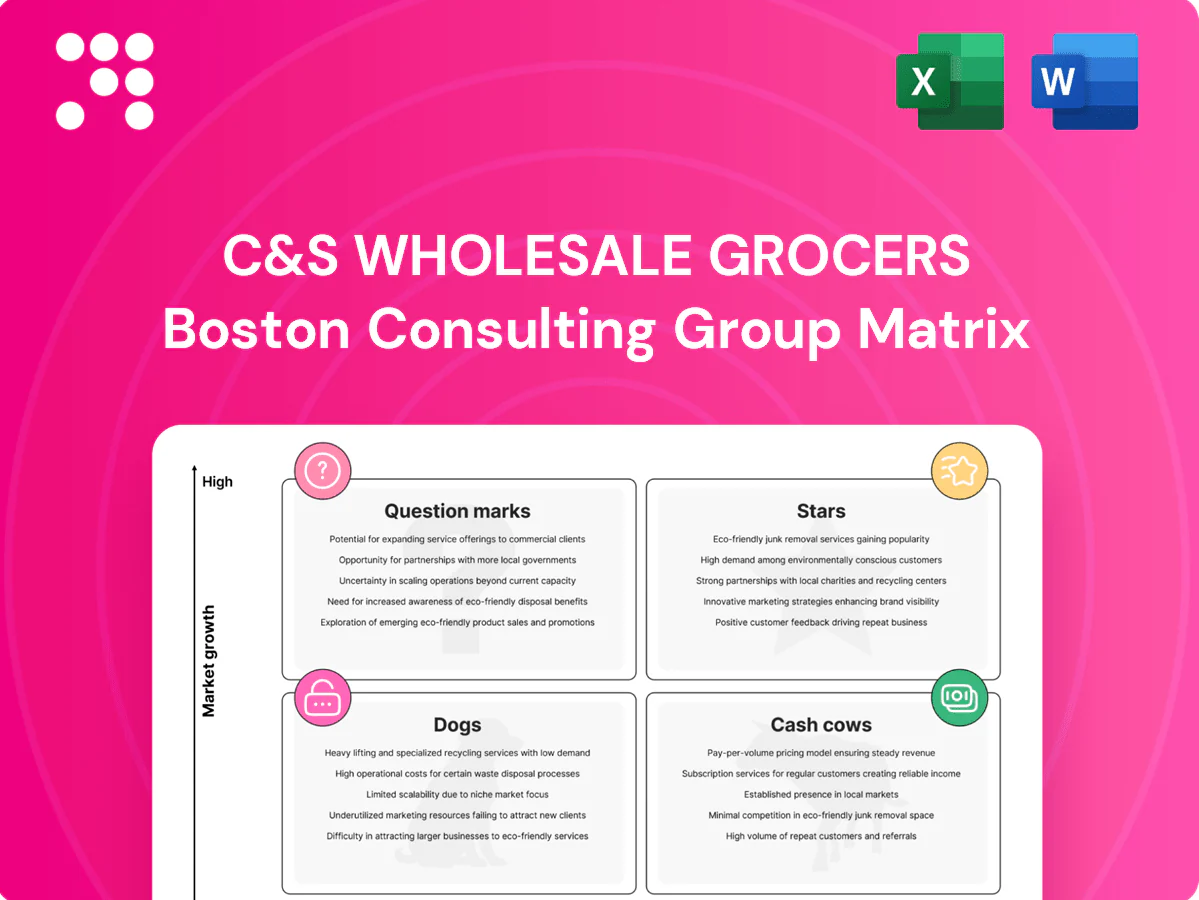

C&S Wholesale Grocers’ BCG Matrix snapshot shows where their product lines likely sit—dominant regional staples, low-growth SKUs sucking margin, and a few high-potential assortments worth watching. This preview teases the shifts and tensions; the full BCG Matrix gives you quadrant-by-quadrant placements, clear recommendations, and editable Word + Excel deliverables to act fast. Buy the complete report for a ready-to-use strategic playbook that saves you hours of analysis and points to where to invest or divest next.

Stars

Omnichannel grocery fulfillment

Omnichannel grocery fulfillment is riding ~10% US e-grocery penetration in 2024, so reliable upstream supply is critical and C&S, the largest US grocery wholesaler serving ~1,400 retailers and independents, sits squarely in that slipstream. Strong share with big chains gives leverage but requires heavy capex in automation and labor; keep funding WMS/robotics and tighter retailer integrations. Hold share now, scale automation to convert growth into a cash cow.

Temperature‑controlled network (fresh & frozen)

Cold chain demand is rising as shoppers shift to fresh and ready‑to‑cook; the global cold‑chain market was about $238B in 2023 and is forecast to grow ~7% CAGR to 2028, positioning C&S’s established refrigerated footprint as a market leader. Energy, equipment and compliance drive high cash needs, so flawless uptime and fill rates are required to secure contracts; at scale this capability converts into sustained margin expansion.

National & regional chain contracts

Anchor national and regional chain contracts concentrate volume and set category pace, with US grocery retail sales around $900B in 2024 reinforcing scale benefits; growth in store counts and broader assortments keeps the tap open while service-level pressure rises. Invest in dedicated lanes, vendor-managed inventory, and joint forecasting to stabilize fill rates and shrink variability. Protect the beachhead—secure margins and profits follow.

Automation-enabled mega DCs

Automation-enabled mega DCs deliver 2–3x throughput and 30–50% labor savings, converting high CAPEX (often $200–500m per site) into rapid unit-cost declines as order volumes rise; they push utilization and cut touches per case, fitting classic star math in a grocery e‑commerce market still growing ~5–7% in 2024. As growth cools, these assets flip into strong cash engines.

- Throughput: 2–3x

- Labor savings: 30–50%

- CAPEX: $200–500m/site

- Market growth 2024: ~5–7%

Retailer merchandising & reset services

Retailer merchandising & reset services sit as Stars: in 2024 retailers demanded faster planogram turns and sharper category insights, and C&S’s on-floor presence is deeply embedded and hard to dislodge. Pairing real-time data with execution during resets drives wins; deeper integration makes accounts stickier and raises switching costs.

- On-floor embedding

- Data + execution

- Faster planogram turns

- Higher account stickiness

Automation: 2-3x throughput, 30-50% labor cut

C&S’s Stars—omnichannel fulfillment, cold‑chain, merchandising—operate in 2024 markets growing ~5–10% with US e‑grocery ~10% penetration; they need heavy CAPEX but enable scale-driven margin expansion. Automation (CAPEX $200–500m/site) yields 2–3x throughput and 30–50% labor savings, converting growth to cash as markets mature. Protect share via tighter integrations, uptime, and VMI.

| Metric | 2023/24 |

|---|---|

| e‑grocery penetration | ~10% (2024) |

| Market growth | 5–7% (2024) |

| Cold‑chain market | $238B (2023) |

| CAPEX/site | $200–500M |

| Throughput | 2–3x |

| Labor savings | 30–50% |

What is included in the product

Concise BCG Matrix review of C&S: maps Stars, Cash Cows, Question Marks, Dogs and flags units to invest, hold, or divest.

One-page BCG matrix placing C&S units in quadrants—clean, export-ready for PowerPoint and C-suite sharing.

Cash Cows

Core ambient grocery distribution

Core ambient grocery distribution is a mature, high-share cash cow for C&S, delivering steady velocity across a national network as the largest privately held U.S. grocery wholesaler; ambient categories show low-single-digit growth (≈2% industry growth in 2024) but high volume density that generates reliable cash flow. Optimize routes, slotting, and case-pick efficiency to cut costs and protect margin. Milk the network for free cash while keeping service rock solid to retain retailer contracts and shrinkage gains.

Long‑term independent retailer programs

Long‑term independent retailer programs deliver decades‑deep relationships and highly predictable, recurring orders that require minimal promotional spend; margins are earned through reliability and service rather than flash. Investment priority is operational efficiency—warehouse automation, route optimization, supplier consolidation—rather than heavy sales campaigns. Cash flow stays tight and steady: mostly in, mostly out, with low volatility and high ROI on infrastructure upgrades.

Private label sourcing & consolidation

Private label sourcing and consolidation is a cash cow: US private-label penetration reached about 18% of grocery sales in 2024, making contracts sticky with retailers. Scale purchasing and QA at C&S (roughly $34B revenue in 2023) deliver dependable contribution and typically add 200–400 basis points to margins versus national brands. Tightening vendor terms and reducing packaging costs can widen that spread; maintain assortment and avoid unnecessary innovation spend to protect yield.

Transportation backhauls & lane density

Transportation backhauls and lane density are cash cows: high asset utilization in a slow-growth 2024 freight market prints margin as every filled mile reduces empty-mile cost. Focus on load planning, dwell reduction, and fuel programs; U.S. freight demand was essentially flat in 2024 while diesel averaged about 4.00–4.05 USD/gal (EIA 2024), so efficiency drives profit.

- Prioritize load planning

- Reduce dwell times

- Implement fuel & routing programs

- Maximize backhaul fill to cut empty miles

Cross‑dock and flow‑through programs

Cross‑dock and flow‑through programs at C&S are mature operations that trim inventory and handling, with industry studies showing cross‑docking can reduce on‑hand days 30–50% and handling labor 20–40%. Low marketing needs and high repeatability make them steady cash cows; modest systems tuning often converts directly to working‑capital relief and margin uplift. Don’t overbuild; maintain throughput and reliability to keep cash flow steady.

- Inventory days reduced: 30–50%

- Handling labor savings: 20–40%

- High repeatability, low marketing

- Small systems tweaks = immediate cash benefit

- Strategy: avoid overbuilding, sustain throughput

Scale and density: ambient, private‑label, transport backhauls and cross‑dock protect margins

Core ambient distribution, private label, transport backhauls and cross‑dock are C&S cash cows: steady cash flow from scale (C&S ≈$34B revenue 2023), low growth (~2% grocery growth 2024), private‑label 18% penetration, diesel ≈$4.00/gal 2024; optimize routes, vendor terms and throughput to protect margins.

| Segment | 2024 metric | Margin lift |

|---|---|---|

| Ambient | ≈2% growth | Stable |

| Private label | 18% penetration | +200–400bps |

| Transport | diesel $4/gal | High via density |

| Cross‑dock | −30–50% days | Working capital |

What You’re Viewing Is Included

C&S Wholesale Grocers BCG Matrix

The file you’re previewing is the exact BCG Matrix report you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready document. It’s designed for immediate editing, printing, or presenting to your team. Delivered instantly to your inbox with clear visuals and market-backed insights. Buy once and use it however you need.

Visual. Strategic. Downloadable.

C&S Wholesale Grocers’ BCG Matrix snapshot shows where their product lines likely sit—dominant regional staples, low-growth SKUs sucking margin, and a few high-potential assortments worth watching. This preview teases the shifts and tensions; the full BCG Matrix gives you quadrant-by-quadrant placements, clear recommendations, and editable Word + Excel deliverables to act fast. Buy the complete report for a ready-to-use strategic playbook that saves you hours of analysis and points to where to invest or divest next.

Stars

Omnichannel grocery fulfillment

Omnichannel grocery fulfillment is riding ~10% US e-grocery penetration in 2024, so reliable upstream supply is critical and C&S, the largest US grocery wholesaler serving ~1,400 retailers and independents, sits squarely in that slipstream. Strong share with big chains gives leverage but requires heavy capex in automation and labor; keep funding WMS/robotics and tighter retailer integrations. Hold share now, scale automation to convert growth into a cash cow.

Temperature‑controlled network (fresh & frozen)

Cold chain demand is rising as shoppers shift to fresh and ready‑to‑cook; the global cold‑chain market was about $238B in 2023 and is forecast to grow ~7% CAGR to 2028, positioning C&S’s established refrigerated footprint as a market leader. Energy, equipment and compliance drive high cash needs, so flawless uptime and fill rates are required to secure contracts; at scale this capability converts into sustained margin expansion.

National & regional chain contracts

Anchor national and regional chain contracts concentrate volume and set category pace, with US grocery retail sales around $900B in 2024 reinforcing scale benefits; growth in store counts and broader assortments keeps the tap open while service-level pressure rises. Invest in dedicated lanes, vendor-managed inventory, and joint forecasting to stabilize fill rates and shrink variability. Protect the beachhead—secure margins and profits follow.

Automation-enabled mega DCs

Automation-enabled mega DCs deliver 2–3x throughput and 30–50% labor savings, converting high CAPEX (often $200–500m per site) into rapid unit-cost declines as order volumes rise; they push utilization and cut touches per case, fitting classic star math in a grocery e‑commerce market still growing ~5–7% in 2024. As growth cools, these assets flip into strong cash engines.

- Throughput: 2–3x

- Labor savings: 30–50%

- CAPEX: $200–500m/site

- Market growth 2024: ~5–7%

Retailer merchandising & reset services

Retailer merchandising & reset services sit as Stars: in 2024 retailers demanded faster planogram turns and sharper category insights, and C&S’s on-floor presence is deeply embedded and hard to dislodge. Pairing real-time data with execution during resets drives wins; deeper integration makes accounts stickier and raises switching costs.

- On-floor embedding

- Data + execution

- Faster planogram turns

- Higher account stickiness

Automation: 2-3x throughput, 30-50% labor cut

C&S’s Stars—omnichannel fulfillment, cold‑chain, merchandising—operate in 2024 markets growing ~5–10% with US e‑grocery ~10% penetration; they need heavy CAPEX but enable scale-driven margin expansion. Automation (CAPEX $200–500m/site) yields 2–3x throughput and 30–50% labor savings, converting growth to cash as markets mature. Protect share via tighter integrations, uptime, and VMI.

| Metric | 2023/24 |

|---|---|

| e‑grocery penetration | ~10% (2024) |

| Market growth | 5–7% (2024) |

| Cold‑chain market | $238B (2023) |

| CAPEX/site | $200–500M |

| Throughput | 2–3x |

| Labor savings | 30–50% |

What is included in the product

Concise BCG Matrix review of C&S: maps Stars, Cash Cows, Question Marks, Dogs and flags units to invest, hold, or divest.

One-page BCG matrix placing C&S units in quadrants—clean, export-ready for PowerPoint and C-suite sharing.

Cash Cows

Core ambient grocery distribution

Core ambient grocery distribution is a mature, high-share cash cow for C&S, delivering steady velocity across a national network as the largest privately held U.S. grocery wholesaler; ambient categories show low-single-digit growth (≈2% industry growth in 2024) but high volume density that generates reliable cash flow. Optimize routes, slotting, and case-pick efficiency to cut costs and protect margin. Milk the network for free cash while keeping service rock solid to retain retailer contracts and shrinkage gains.

Long‑term independent retailer programs

Long‑term independent retailer programs deliver decades‑deep relationships and highly predictable, recurring orders that require minimal promotional spend; margins are earned through reliability and service rather than flash. Investment priority is operational efficiency—warehouse automation, route optimization, supplier consolidation—rather than heavy sales campaigns. Cash flow stays tight and steady: mostly in, mostly out, with low volatility and high ROI on infrastructure upgrades.

Private label sourcing & consolidation

Private label sourcing and consolidation is a cash cow: US private-label penetration reached about 18% of grocery sales in 2024, making contracts sticky with retailers. Scale purchasing and QA at C&S (roughly $34B revenue in 2023) deliver dependable contribution and typically add 200–400 basis points to margins versus national brands. Tightening vendor terms and reducing packaging costs can widen that spread; maintain assortment and avoid unnecessary innovation spend to protect yield.

Transportation backhauls & lane density

Transportation backhauls and lane density are cash cows: high asset utilization in a slow-growth 2024 freight market prints margin as every filled mile reduces empty-mile cost. Focus on load planning, dwell reduction, and fuel programs; U.S. freight demand was essentially flat in 2024 while diesel averaged about 4.00–4.05 USD/gal (EIA 2024), so efficiency drives profit.

- Prioritize load planning

- Reduce dwell times

- Implement fuel & routing programs

- Maximize backhaul fill to cut empty miles

Cross‑dock and flow‑through programs

Cross‑dock and flow‑through programs at C&S are mature operations that trim inventory and handling, with industry studies showing cross‑docking can reduce on‑hand days 30–50% and handling labor 20–40%. Low marketing needs and high repeatability make them steady cash cows; modest systems tuning often converts directly to working‑capital relief and margin uplift. Don’t overbuild; maintain throughput and reliability to keep cash flow steady.

- Inventory days reduced: 30–50%

- Handling labor savings: 20–40%

- High repeatability, low marketing

- Small systems tweaks = immediate cash benefit

- Strategy: avoid overbuilding, sustain throughput

Scale and density: ambient, private‑label, transport backhauls and cross‑dock protect margins

Core ambient distribution, private label, transport backhauls and cross‑dock are C&S cash cows: steady cash flow from scale (C&S ≈$34B revenue 2023), low growth (~2% grocery growth 2024), private‑label 18% penetration, diesel ≈$4.00/gal 2024; optimize routes, vendor terms and throughput to protect margins.

| Segment | 2024 metric | Margin lift |

|---|---|---|

| Ambient | ≈2% growth | Stable |

| Private label | 18% penetration | +200–400bps |

| Transport | diesel $4/gal | High via density |

| Cross‑dock | −30–50% days | Working capital |

What You’re Viewing Is Included

C&S Wholesale Grocers BCG Matrix

The file you’re previewing is the exact BCG Matrix report you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready document. It’s designed for immediate editing, printing, or presenting to your team. Delivered instantly to your inbox with clear visuals and market-backed insights. Buy once and use it however you need.

Original: $10.00

-65%$10.00

$3.50Description

Visual. Strategic. Downloadable.

C&S Wholesale Grocers’ BCG Matrix snapshot shows where their product lines likely sit—dominant regional staples, low-growth SKUs sucking margin, and a few high-potential assortments worth watching. This preview teases the shifts and tensions; the full BCG Matrix gives you quadrant-by-quadrant placements, clear recommendations, and editable Word + Excel deliverables to act fast. Buy the complete report for a ready-to-use strategic playbook that saves you hours of analysis and points to where to invest or divest next.

Stars

Omnichannel grocery fulfillment

Omnichannel grocery fulfillment is riding ~10% US e-grocery penetration in 2024, so reliable upstream supply is critical and C&S, the largest US grocery wholesaler serving ~1,400 retailers and independents, sits squarely in that slipstream. Strong share with big chains gives leverage but requires heavy capex in automation and labor; keep funding WMS/robotics and tighter retailer integrations. Hold share now, scale automation to convert growth into a cash cow.

Temperature‑controlled network (fresh & frozen)

Cold chain demand is rising as shoppers shift to fresh and ready‑to‑cook; the global cold‑chain market was about $238B in 2023 and is forecast to grow ~7% CAGR to 2028, positioning C&S’s established refrigerated footprint as a market leader. Energy, equipment and compliance drive high cash needs, so flawless uptime and fill rates are required to secure contracts; at scale this capability converts into sustained margin expansion.

National & regional chain contracts

Anchor national and regional chain contracts concentrate volume and set category pace, with US grocery retail sales around $900B in 2024 reinforcing scale benefits; growth in store counts and broader assortments keeps the tap open while service-level pressure rises. Invest in dedicated lanes, vendor-managed inventory, and joint forecasting to stabilize fill rates and shrink variability. Protect the beachhead—secure margins and profits follow.

Automation-enabled mega DCs

Automation-enabled mega DCs deliver 2–3x throughput and 30–50% labor savings, converting high CAPEX (often $200–500m per site) into rapid unit-cost declines as order volumes rise; they push utilization and cut touches per case, fitting classic star math in a grocery e‑commerce market still growing ~5–7% in 2024. As growth cools, these assets flip into strong cash engines.

- Throughput: 2–3x

- Labor savings: 30–50%

- CAPEX: $200–500m/site

- Market growth 2024: ~5–7%

Retailer merchandising & reset services

Retailer merchandising & reset services sit as Stars: in 2024 retailers demanded faster planogram turns and sharper category insights, and C&S’s on-floor presence is deeply embedded and hard to dislodge. Pairing real-time data with execution during resets drives wins; deeper integration makes accounts stickier and raises switching costs.

- On-floor embedding

- Data + execution

- Faster planogram turns

- Higher account stickiness

Automation: 2-3x throughput, 30-50% labor cut

C&S’s Stars—omnichannel fulfillment, cold‑chain, merchandising—operate in 2024 markets growing ~5–10% with US e‑grocery ~10% penetration; they need heavy CAPEX but enable scale-driven margin expansion. Automation (CAPEX $200–500m/site) yields 2–3x throughput and 30–50% labor savings, converting growth to cash as markets mature. Protect share via tighter integrations, uptime, and VMI.

| Metric | 2023/24 |

|---|---|

| e‑grocery penetration | ~10% (2024) |

| Market growth | 5–7% (2024) |

| Cold‑chain market | $238B (2023) |

| CAPEX/site | $200–500M |

| Throughput | 2–3x |

| Labor savings | 30–50% |

What is included in the product

Concise BCG Matrix review of C&S: maps Stars, Cash Cows, Question Marks, Dogs and flags units to invest, hold, or divest.

One-page BCG matrix placing C&S units in quadrants—clean, export-ready for PowerPoint and C-suite sharing.

Cash Cows

Core ambient grocery distribution

Core ambient grocery distribution is a mature, high-share cash cow for C&S, delivering steady velocity across a national network as the largest privately held U.S. grocery wholesaler; ambient categories show low-single-digit growth (≈2% industry growth in 2024) but high volume density that generates reliable cash flow. Optimize routes, slotting, and case-pick efficiency to cut costs and protect margin. Milk the network for free cash while keeping service rock solid to retain retailer contracts and shrinkage gains.

Long‑term independent retailer programs

Long‑term independent retailer programs deliver decades‑deep relationships and highly predictable, recurring orders that require minimal promotional spend; margins are earned through reliability and service rather than flash. Investment priority is operational efficiency—warehouse automation, route optimization, supplier consolidation—rather than heavy sales campaigns. Cash flow stays tight and steady: mostly in, mostly out, with low volatility and high ROI on infrastructure upgrades.

Private label sourcing & consolidation

Private label sourcing and consolidation is a cash cow: US private-label penetration reached about 18% of grocery sales in 2024, making contracts sticky with retailers. Scale purchasing and QA at C&S (roughly $34B revenue in 2023) deliver dependable contribution and typically add 200–400 basis points to margins versus national brands. Tightening vendor terms and reducing packaging costs can widen that spread; maintain assortment and avoid unnecessary innovation spend to protect yield.

Transportation backhauls & lane density

Transportation backhauls and lane density are cash cows: high asset utilization in a slow-growth 2024 freight market prints margin as every filled mile reduces empty-mile cost. Focus on load planning, dwell reduction, and fuel programs; U.S. freight demand was essentially flat in 2024 while diesel averaged about 4.00–4.05 USD/gal (EIA 2024), so efficiency drives profit.

- Prioritize load planning

- Reduce dwell times

- Implement fuel & routing programs

- Maximize backhaul fill to cut empty miles

Cross‑dock and flow‑through programs

Cross‑dock and flow‑through programs at C&S are mature operations that trim inventory and handling, with industry studies showing cross‑docking can reduce on‑hand days 30–50% and handling labor 20–40%. Low marketing needs and high repeatability make them steady cash cows; modest systems tuning often converts directly to working‑capital relief and margin uplift. Don’t overbuild; maintain throughput and reliability to keep cash flow steady.

- Inventory days reduced: 30–50%

- Handling labor savings: 20–40%

- High repeatability, low marketing

- Small systems tweaks = immediate cash benefit

- Strategy: avoid overbuilding, sustain throughput

Scale and density: ambient, private‑label, transport backhauls and cross‑dock protect margins

Core ambient distribution, private label, transport backhauls and cross‑dock are C&S cash cows: steady cash flow from scale (C&S ≈$34B revenue 2023), low growth (~2% grocery growth 2024), private‑label 18% penetration, diesel ≈$4.00/gal 2024; optimize routes, vendor terms and throughput to protect margins.

| Segment | 2024 metric | Margin lift |

|---|---|---|

| Ambient | ≈2% growth | Stable |

| Private label | 18% penetration | +200–400bps |

| Transport | diesel $4/gal | High via density |

| Cross‑dock | −30–50% days | Working capital |

What You’re Viewing Is Included

C&S Wholesale Grocers BCG Matrix

The file you’re previewing is the exact BCG Matrix report you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready document. It’s designed for immediate editing, printing, or presenting to your team. Delivered instantly to your inbox with clear visuals and market-backed insights. Buy once and use it however you need.