CTS Boston Consulting Group Matrix

Unlock Strategic Clarity

This CTS BCG Matrix preview spots the quick wins and the hidden drains—now imagine the full picture: quadrant-by-quadrant placements, data-backed priorities, and clear moves you can act on. Buy the complete BCG Matrix for a ready-to-present Word report plus an Excel summary that shows which products are Stars, Cash Cows, Dogs, or Question Marks and where to invest next. Skip the guesswork—get the strategic clarity your leadership team needs, fast.

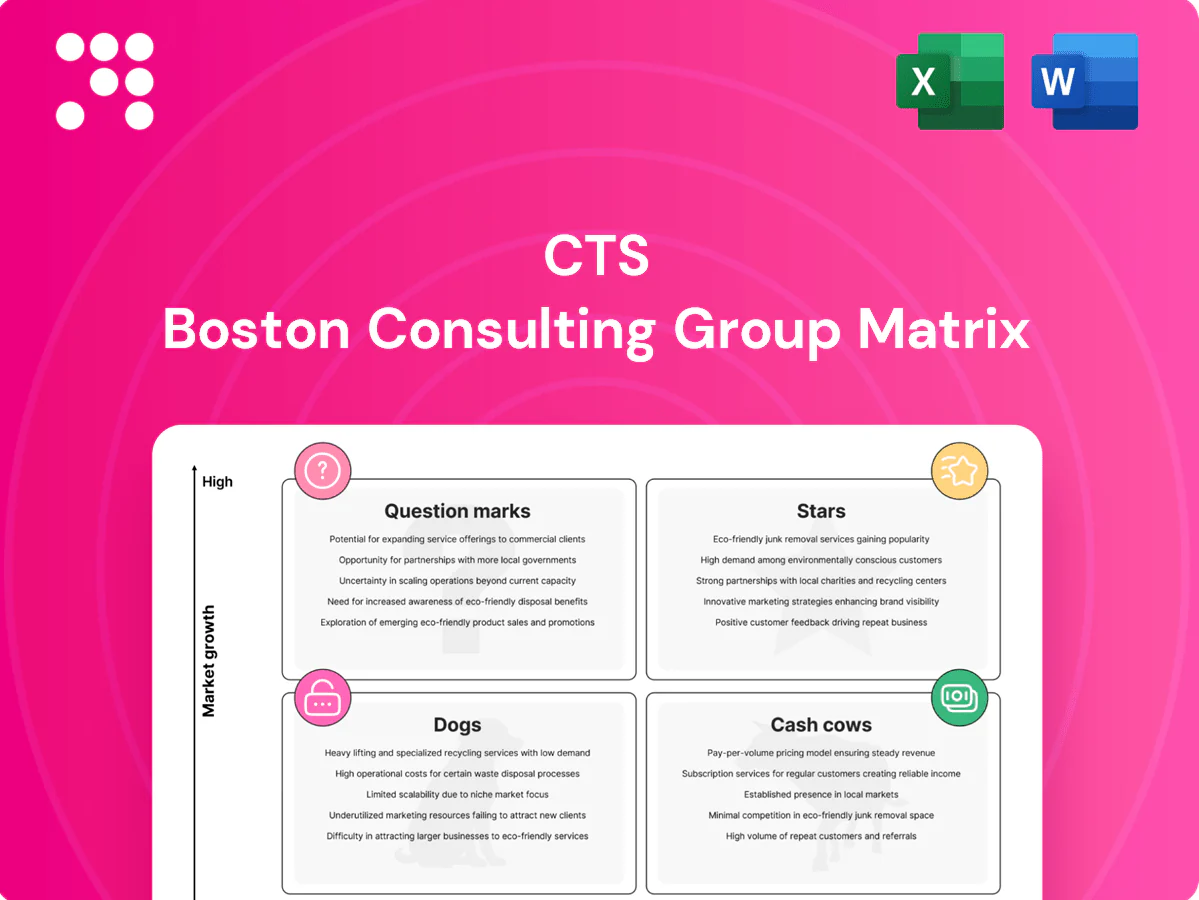

Stars

EV and ADAS sensor suites

EV and ADAS sensor suites sit in Stars: global EV sales surged to ~14.5 million in 2024, driving ADAS sensor market demand (~$34B in 2024) and high-growth transportation programs where CTS has a real shot at leading OEM packs. Volume is spiking, but validation costs and program launches are escalating — cash in, cash out as unit economics tighten. Keep the pedal down on design wins, software calibration support, and Tier‑1 partnerships to nail share now and convert to a cash cow when growth cools.

Medical-grade sensing for minimally invasive devices

Procedures for minimally invasive care are rising and hospitals demand smaller, smarter, fail-safe components; CTS’s reliability track record fits this Stars quadrant and post-approval margins can be high. PMA pathways often span multiple years and heavy clinical validation and field support continue to consume cash, so stay invested to lock market leadership before copycats arrive.

Aerospace drive and actuation assemblies

Defense and next‑gen aero platforms show multi‑year backlogs amid elevated defense spending (global military expenditure was $2.24 trillion in 2023, SIPRI), lifting demand for aerospace drive and actuation assemblies.

CTS sits in safety‑critical slots where performance wins but qualification and ramp costs are high, so maintain funding capacity, testing, and in‑program engineering.

Hold share; as qualification barriers ease these lines can mature into steady cash engines with predictable aftermarket revenues.

Industrial IoT condition-monitoring sensors

Industrial IoT condition-monitoring sensors sit in Stars: factories digitize rapidly, predictive maintenance shows 20–40% lower maintenance costs and up to 50% less unplanned downtime; the global IIoT market was estimated near US$140 billion in 2024, driving strong demand. CTS has proven hardware capabilities; bundling analytics partners increases solution pull-through and average deal value while growth pressures working capital and deployment support.

- Push ecosystem deals to boost renewals

- Field apps for fleet lock-in

- Plan 6–12 month deployment CAPEX

- Monitor churn and ARR expansion

High-reliability motion control for robotics

Rising robotics adoption in logistics and manufacturing is creating Star-level demand for high-reliability motion control; precision actuators and encoders with tight specs place CTS on shortlists for major integrators.

New product introduction cycles and custom variants tie up engineering and cash — NPI efforts commonly span 9–18 months and can require $1–5M per platform.

Prioritize investment to standardize platforms and scale across multiple robot types to convert shortlists into repeatable, higher-margin wins.

- Market fit: logistics/manufacturing surge

- Competitive edge: tight-spec actuators/encoders

- Risk: 9–18 month NPI, $1–5M cost

- Action: standardize platforms, scale not one-offs

Stars: EV/ADAS, Medical, Defense, IIoT - 14.5M EVs, $140B

EV/ADAS, medical, defense/aero, IIoT/robotics are Stars for CTS: 2024 EV sales ~14.5M and ADAS market ~$34B; IIoT ~$140B (2024); 2023 military spend $2.24T. Growth requires heavy NPI/validation (medical PMA multi‑year; NPI 9–18m, $1–5M); prioritize design wins, standardization, and Tier‑1 partnerships.

| Segment | 2024/2023 size | Risk | Action |

|---|---|---|---|

| EV/ADAS | EVs ~14.5M; ADAS ~$34B | validation, ramp cost | push design wins |

| Medical | high post‑approval margins | PMA multi‑yr | fund clinical support |

| Defense/Aero | military spend $2.24T (2023) | qualification costs | maintain testing capacity |

| IIoT/Robotics | IIoT ~$140B; NPI $1–5M | deployment CAPEX | standardize platforms |

What is included in the product

CTS BCG Matrix: concise quadrant evaluation of products, advising invest, hold or divest with competitive risks and trend context.

One-page CTS BCG Matrix placing each business unit in a quadrant to simplify portfolio choices and speed executive decisions.

Cash Cows

Legacy automotive position sensors (ICE platforms)

Mature, high-share legacy automotive position-sensor programs deliver repeat orders with predictable volumes and stable aftermarket tails. Engineering costs are fully amortized and line yields are dialed in, yielding steady gross contribution. With low growth and minimal promotional spend, the focus is keep quality rock solid. Milk margins and redeploy cash to EV/ADAS growth as global electric-vehicle sales reached ~15% of new car sales in 2024.

Frequency control and timing components

Frequency control and timing components serve long-lifecycle sockets in industrial and medical equipment, often in systems maintained 10–20 years, producing steady demand and low volatility. Specialty specs command pricing power; incremental capex (process upgrades) raises throughput more than marketing. Harvest cash, defend core accounts, and avoid price wars to preserve margins and fund selective capacity expansions.

Piezoelectric components for industrial equipment

Trusted-performance piezoelectric components are a cash cow for CTS: 2024 unit demand was flat (~0–1% YoY) with replacement and MRO accounting for roughly 55% of sales, keeping utilization high. Process know-how drives gross margins near 35% and low unit costs, while slow market churn produces sticky customers and multiyear repeat orders. Focus: optimize footprint, cut scrap to lift EBITDA and bank free cash (≈€20m in 2024) for reinvestment.

Standard actuators for commercial aerospace maintenance

Standard actuators for commercial aerospace maintenance sit squarely in Cash Cows: predictable aftermarket refresh cycles (A-checks ~every 400–600 flight hours, C-checks ~18–24 months) drive steady orders and service annuities, with the global commercial MRO market around USD 90–95 billion in 2024 supporting dependable demand.

FAA/EASA certifications and OEM approvals create high barriers to entry and protect share, so firms avoid heavy promotion spend—reliability and certified traceability sell themselves—focus instead on maintaining service levels and parts availability to keep annuity revenue flowing.

- Aftermarket cadence: A-checks 400–600 flight hrs; C-checks 18–24 months

- Market scale 2024: commercial MRO ~USD 90–95B

- Barrier: FAA/EASA/OEM certification lead times 6–24 months

- Strategy: prioritize parts availability and service SLAs over heavy promotion

Ruggedized sensors for traditional factory automation

Ruggedized sensors for traditional factory automation are cash cows: decades of installed base and slow spec change give steady reorder cadence; in 2024 the industrial sensors market was estimated near 23 billion USD, with legacy installations driving recurring demand. CTS’s quality and on-time delivery convert repeat orders, and efficiency-focused projects outperform flashy new-product launches. Protect pricing, secure multi-year agreements, and skim high-margin cash flows.

- Installed base: decades

- 2024 market est: ~23B USD

- Revenue driver: repeat orders, steady reorder cadence

- Strategy: protect price, lock multi-year deals

Legacy sensors bankroll EV/ADAS — steady margins, aftermarket annuities, €20m free cash

Mature, high-share legacy sensors, timing parts, piezo components and actuators deliver steady margins and predictable aftermarket annuities; focus on quality, parts availability and harvesting cash to fund EV/ADAS. 2024: EVs ~15% new car sales, CTS free cash ≈€20m, industrial sensors market ≈$23B, commercial MRO $90–95B.

| Metric | 2024 |

|---|---|

| EV share | ~15% |

| CTS free cash | €20m |

| Industrial sensors market | $23B |

| Commercial MRO | $90–95B |

What You’re Viewing Is Included

CTS BCG Matrix

The CTS BCG Matrix you're previewing here is the exact file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report crafted for strategic clarity. After buying, the complete document is sent to your inbox and is ready to edit, print, or present to stakeholders immediately.

Unlock Strategic Clarity

This CTS BCG Matrix preview spots the quick wins and the hidden drains—now imagine the full picture: quadrant-by-quadrant placements, data-backed priorities, and clear moves you can act on. Buy the complete BCG Matrix for a ready-to-present Word report plus an Excel summary that shows which products are Stars, Cash Cows, Dogs, or Question Marks and where to invest next. Skip the guesswork—get the strategic clarity your leadership team needs, fast.

Stars

EV and ADAS sensor suites

EV and ADAS sensor suites sit in Stars: global EV sales surged to ~14.5 million in 2024, driving ADAS sensor market demand (~$34B in 2024) and high-growth transportation programs where CTS has a real shot at leading OEM packs. Volume is spiking, but validation costs and program launches are escalating — cash in, cash out as unit economics tighten. Keep the pedal down on design wins, software calibration support, and Tier‑1 partnerships to nail share now and convert to a cash cow when growth cools.

Medical-grade sensing for minimally invasive devices

Procedures for minimally invasive care are rising and hospitals demand smaller, smarter, fail-safe components; CTS’s reliability track record fits this Stars quadrant and post-approval margins can be high. PMA pathways often span multiple years and heavy clinical validation and field support continue to consume cash, so stay invested to lock market leadership before copycats arrive.

Aerospace drive and actuation assemblies

Defense and next‑gen aero platforms show multi‑year backlogs amid elevated defense spending (global military expenditure was $2.24 trillion in 2023, SIPRI), lifting demand for aerospace drive and actuation assemblies.

CTS sits in safety‑critical slots where performance wins but qualification and ramp costs are high, so maintain funding capacity, testing, and in‑program engineering.

Hold share; as qualification barriers ease these lines can mature into steady cash engines with predictable aftermarket revenues.

Industrial IoT condition-monitoring sensors

Industrial IoT condition-monitoring sensors sit in Stars: factories digitize rapidly, predictive maintenance shows 20–40% lower maintenance costs and up to 50% less unplanned downtime; the global IIoT market was estimated near US$140 billion in 2024, driving strong demand. CTS has proven hardware capabilities; bundling analytics partners increases solution pull-through and average deal value while growth pressures working capital and deployment support.

- Push ecosystem deals to boost renewals

- Field apps for fleet lock-in

- Plan 6–12 month deployment CAPEX

- Monitor churn and ARR expansion

High-reliability motion control for robotics

Rising robotics adoption in logistics and manufacturing is creating Star-level demand for high-reliability motion control; precision actuators and encoders with tight specs place CTS on shortlists for major integrators.

New product introduction cycles and custom variants tie up engineering and cash — NPI efforts commonly span 9–18 months and can require $1–5M per platform.

Prioritize investment to standardize platforms and scale across multiple robot types to convert shortlists into repeatable, higher-margin wins.

- Market fit: logistics/manufacturing surge

- Competitive edge: tight-spec actuators/encoders

- Risk: 9–18 month NPI, $1–5M cost

- Action: standardize platforms, scale not one-offs

Stars: EV/ADAS, Medical, Defense, IIoT - 14.5M EVs, $140B

EV/ADAS, medical, defense/aero, IIoT/robotics are Stars for CTS: 2024 EV sales ~14.5M and ADAS market ~$34B; IIoT ~$140B (2024); 2023 military spend $2.24T. Growth requires heavy NPI/validation (medical PMA multi‑year; NPI 9–18m, $1–5M); prioritize design wins, standardization, and Tier‑1 partnerships.

| Segment | 2024/2023 size | Risk | Action |

|---|---|---|---|

| EV/ADAS | EVs ~14.5M; ADAS ~$34B | validation, ramp cost | push design wins |

| Medical | high post‑approval margins | PMA multi‑yr | fund clinical support |

| Defense/Aero | military spend $2.24T (2023) | qualification costs | maintain testing capacity |

| IIoT/Robotics | IIoT ~$140B; NPI $1–5M | deployment CAPEX | standardize platforms |

What is included in the product

CTS BCG Matrix: concise quadrant evaluation of products, advising invest, hold or divest with competitive risks and trend context.

One-page CTS BCG Matrix placing each business unit in a quadrant to simplify portfolio choices and speed executive decisions.

Cash Cows

Legacy automotive position sensors (ICE platforms)

Mature, high-share legacy automotive position-sensor programs deliver repeat orders with predictable volumes and stable aftermarket tails. Engineering costs are fully amortized and line yields are dialed in, yielding steady gross contribution. With low growth and minimal promotional spend, the focus is keep quality rock solid. Milk margins and redeploy cash to EV/ADAS growth as global electric-vehicle sales reached ~15% of new car sales in 2024.

Frequency control and timing components

Frequency control and timing components serve long-lifecycle sockets in industrial and medical equipment, often in systems maintained 10–20 years, producing steady demand and low volatility. Specialty specs command pricing power; incremental capex (process upgrades) raises throughput more than marketing. Harvest cash, defend core accounts, and avoid price wars to preserve margins and fund selective capacity expansions.

Piezoelectric components for industrial equipment

Trusted-performance piezoelectric components are a cash cow for CTS: 2024 unit demand was flat (~0–1% YoY) with replacement and MRO accounting for roughly 55% of sales, keeping utilization high. Process know-how drives gross margins near 35% and low unit costs, while slow market churn produces sticky customers and multiyear repeat orders. Focus: optimize footprint, cut scrap to lift EBITDA and bank free cash (≈€20m in 2024) for reinvestment.

Standard actuators for commercial aerospace maintenance

Standard actuators for commercial aerospace maintenance sit squarely in Cash Cows: predictable aftermarket refresh cycles (A-checks ~every 400–600 flight hours, C-checks ~18–24 months) drive steady orders and service annuities, with the global commercial MRO market around USD 90–95 billion in 2024 supporting dependable demand.

FAA/EASA certifications and OEM approvals create high barriers to entry and protect share, so firms avoid heavy promotion spend—reliability and certified traceability sell themselves—focus instead on maintaining service levels and parts availability to keep annuity revenue flowing.

- Aftermarket cadence: A-checks 400–600 flight hrs; C-checks 18–24 months

- Market scale 2024: commercial MRO ~USD 90–95B

- Barrier: FAA/EASA/OEM certification lead times 6–24 months

- Strategy: prioritize parts availability and service SLAs over heavy promotion

Ruggedized sensors for traditional factory automation

Ruggedized sensors for traditional factory automation are cash cows: decades of installed base and slow spec change give steady reorder cadence; in 2024 the industrial sensors market was estimated near 23 billion USD, with legacy installations driving recurring demand. CTS’s quality and on-time delivery convert repeat orders, and efficiency-focused projects outperform flashy new-product launches. Protect pricing, secure multi-year agreements, and skim high-margin cash flows.

- Installed base: decades

- 2024 market est: ~23B USD

- Revenue driver: repeat orders, steady reorder cadence

- Strategy: protect price, lock multi-year deals

Legacy sensors bankroll EV/ADAS — steady margins, aftermarket annuities, €20m free cash

Mature, high-share legacy sensors, timing parts, piezo components and actuators deliver steady margins and predictable aftermarket annuities; focus on quality, parts availability and harvesting cash to fund EV/ADAS. 2024: EVs ~15% new car sales, CTS free cash ≈€20m, industrial sensors market ≈$23B, commercial MRO $90–95B.

| Metric | 2024 |

|---|---|

| EV share | ~15% |

| CTS free cash | €20m |

| Industrial sensors market | $23B |

| Commercial MRO | $90–95B |

What You’re Viewing Is Included

CTS BCG Matrix

The CTS BCG Matrix you're previewing here is the exact file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report crafted for strategic clarity. After buying, the complete document is sent to your inbox and is ready to edit, print, or present to stakeholders immediately.

Original: $10.00

-65%$10.00

$3.50Description

Unlock Strategic Clarity

This CTS BCG Matrix preview spots the quick wins and the hidden drains—now imagine the full picture: quadrant-by-quadrant placements, data-backed priorities, and clear moves you can act on. Buy the complete BCG Matrix for a ready-to-present Word report plus an Excel summary that shows which products are Stars, Cash Cows, Dogs, or Question Marks and where to invest next. Skip the guesswork—get the strategic clarity your leadership team needs, fast.

Stars

EV and ADAS sensor suites

EV and ADAS sensor suites sit in Stars: global EV sales surged to ~14.5 million in 2024, driving ADAS sensor market demand (~$34B in 2024) and high-growth transportation programs where CTS has a real shot at leading OEM packs. Volume is spiking, but validation costs and program launches are escalating — cash in, cash out as unit economics tighten. Keep the pedal down on design wins, software calibration support, and Tier‑1 partnerships to nail share now and convert to a cash cow when growth cools.

Medical-grade sensing for minimally invasive devices

Procedures for minimally invasive care are rising and hospitals demand smaller, smarter, fail-safe components; CTS’s reliability track record fits this Stars quadrant and post-approval margins can be high. PMA pathways often span multiple years and heavy clinical validation and field support continue to consume cash, so stay invested to lock market leadership before copycats arrive.

Aerospace drive and actuation assemblies

Defense and next‑gen aero platforms show multi‑year backlogs amid elevated defense spending (global military expenditure was $2.24 trillion in 2023, SIPRI), lifting demand for aerospace drive and actuation assemblies.

CTS sits in safety‑critical slots where performance wins but qualification and ramp costs are high, so maintain funding capacity, testing, and in‑program engineering.

Hold share; as qualification barriers ease these lines can mature into steady cash engines with predictable aftermarket revenues.

Industrial IoT condition-monitoring sensors

Industrial IoT condition-monitoring sensors sit in Stars: factories digitize rapidly, predictive maintenance shows 20–40% lower maintenance costs and up to 50% less unplanned downtime; the global IIoT market was estimated near US$140 billion in 2024, driving strong demand. CTS has proven hardware capabilities; bundling analytics partners increases solution pull-through and average deal value while growth pressures working capital and deployment support.

- Push ecosystem deals to boost renewals

- Field apps for fleet lock-in

- Plan 6–12 month deployment CAPEX

- Monitor churn and ARR expansion

High-reliability motion control for robotics

Rising robotics adoption in logistics and manufacturing is creating Star-level demand for high-reliability motion control; precision actuators and encoders with tight specs place CTS on shortlists for major integrators.

New product introduction cycles and custom variants tie up engineering and cash — NPI efforts commonly span 9–18 months and can require $1–5M per platform.

Prioritize investment to standardize platforms and scale across multiple robot types to convert shortlists into repeatable, higher-margin wins.

- Market fit: logistics/manufacturing surge

- Competitive edge: tight-spec actuators/encoders

- Risk: 9–18 month NPI, $1–5M cost

- Action: standardize platforms, scale not one-offs

Stars: EV/ADAS, Medical, Defense, IIoT - 14.5M EVs, $140B

EV/ADAS, medical, defense/aero, IIoT/robotics are Stars for CTS: 2024 EV sales ~14.5M and ADAS market ~$34B; IIoT ~$140B (2024); 2023 military spend $2.24T. Growth requires heavy NPI/validation (medical PMA multi‑year; NPI 9–18m, $1–5M); prioritize design wins, standardization, and Tier‑1 partnerships.

| Segment | 2024/2023 size | Risk | Action |

|---|---|---|---|

| EV/ADAS | EVs ~14.5M; ADAS ~$34B | validation, ramp cost | push design wins |

| Medical | high post‑approval margins | PMA multi‑yr | fund clinical support |

| Defense/Aero | military spend $2.24T (2023) | qualification costs | maintain testing capacity |

| IIoT/Robotics | IIoT ~$140B; NPI $1–5M | deployment CAPEX | standardize platforms |

What is included in the product

CTS BCG Matrix: concise quadrant evaluation of products, advising invest, hold or divest with competitive risks and trend context.

One-page CTS BCG Matrix placing each business unit in a quadrant to simplify portfolio choices and speed executive decisions.

Cash Cows

Legacy automotive position sensors (ICE platforms)

Mature, high-share legacy automotive position-sensor programs deliver repeat orders with predictable volumes and stable aftermarket tails. Engineering costs are fully amortized and line yields are dialed in, yielding steady gross contribution. With low growth and minimal promotional spend, the focus is keep quality rock solid. Milk margins and redeploy cash to EV/ADAS growth as global electric-vehicle sales reached ~15% of new car sales in 2024.

Frequency control and timing components

Frequency control and timing components serve long-lifecycle sockets in industrial and medical equipment, often in systems maintained 10–20 years, producing steady demand and low volatility. Specialty specs command pricing power; incremental capex (process upgrades) raises throughput more than marketing. Harvest cash, defend core accounts, and avoid price wars to preserve margins and fund selective capacity expansions.

Piezoelectric components for industrial equipment

Trusted-performance piezoelectric components are a cash cow for CTS: 2024 unit demand was flat (~0–1% YoY) with replacement and MRO accounting for roughly 55% of sales, keeping utilization high. Process know-how drives gross margins near 35% and low unit costs, while slow market churn produces sticky customers and multiyear repeat orders. Focus: optimize footprint, cut scrap to lift EBITDA and bank free cash (≈€20m in 2024) for reinvestment.

Standard actuators for commercial aerospace maintenance

Standard actuators for commercial aerospace maintenance sit squarely in Cash Cows: predictable aftermarket refresh cycles (A-checks ~every 400–600 flight hours, C-checks ~18–24 months) drive steady orders and service annuities, with the global commercial MRO market around USD 90–95 billion in 2024 supporting dependable demand.

FAA/EASA certifications and OEM approvals create high barriers to entry and protect share, so firms avoid heavy promotion spend—reliability and certified traceability sell themselves—focus instead on maintaining service levels and parts availability to keep annuity revenue flowing.

- Aftermarket cadence: A-checks 400–600 flight hrs; C-checks 18–24 months

- Market scale 2024: commercial MRO ~USD 90–95B

- Barrier: FAA/EASA/OEM certification lead times 6–24 months

- Strategy: prioritize parts availability and service SLAs over heavy promotion

Ruggedized sensors for traditional factory automation

Ruggedized sensors for traditional factory automation are cash cows: decades of installed base and slow spec change give steady reorder cadence; in 2024 the industrial sensors market was estimated near 23 billion USD, with legacy installations driving recurring demand. CTS’s quality and on-time delivery convert repeat orders, and efficiency-focused projects outperform flashy new-product launches. Protect pricing, secure multi-year agreements, and skim high-margin cash flows.

- Installed base: decades

- 2024 market est: ~23B USD

- Revenue driver: repeat orders, steady reorder cadence

- Strategy: protect price, lock multi-year deals

Legacy sensors bankroll EV/ADAS — steady margins, aftermarket annuities, €20m free cash

Mature, high-share legacy sensors, timing parts, piezo components and actuators deliver steady margins and predictable aftermarket annuities; focus on quality, parts availability and harvesting cash to fund EV/ADAS. 2024: EVs ~15% new car sales, CTS free cash ≈€20m, industrial sensors market ≈$23B, commercial MRO $90–95B.

| Metric | 2024 |

|---|---|

| EV share | ~15% |

| CTS free cash | €20m |

| Industrial sensors market | $23B |

| Commercial MRO | $90–95B |

What You’re Viewing Is Included

CTS BCG Matrix

The CTS BCG Matrix you're previewing here is the exact file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report crafted for strategic clarity. After buying, the complete document is sent to your inbox and is ready to edit, print, or present to stakeholders immediately.