Culp Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Culp faces nuanced competitive dynamics where supplier leverage, buyer expectations, and substitute threats shape margin pressure and growth prospects. Our snapshot highlights how scale, brand strength, and channel control influence competitive intensity and entry barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Culp’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty yarn and fiber sources

Mattress and upholstery fabrics depend on performance yarns, specialty fibers and finishing chemistries that have a limited pool of qualified suppliers, and strict certification and consistency requirements further narrow available vendors. Fewer alternatives give suppliers pricing and allocation leverage, especially during demand surges or raw‑material disruptions. Culp can mitigate risk by multi‑sourcing and qualifying substitutes, but qualification cycles and scale‑up typically take many months to years.

Dependency on dye/finish chemicals and processes

Finishing chemistries, coatings and flame‑retardants are highly regulated and specialized, driving switching friction; the global textile finishing chemicals market was about $20 billion in 2024 and suppliers often secure fast pass‑through of feedstock inflation (price moves of 10–20% seen in 2022–24). Technical approvals and recipe know‑how typically take 3–6 months, raising time costs and reinforcing supplier bargaining power.

Capital equipment and parts from few OEMs

Jacquard looms, knitting machines and cutting/sewing automation are concentrated among a handful of global OEMs (top vendors supply >60% of these segments), creating supplier leverage; lead times often exceed 12 months and spare-parts delays of 4–16 weeks can constrain capacity. Service contracts and proprietary software locks deepen dependence and industry reports show lifecycle maintenance and upgrade costs can rise by up to 25%.

Freight, energy, and FX pass‑through

Energy-intensive processes and long-haul logistics leave Culp exposed to volatile input costs; diesel averaged about $4.00/gal in the US in 2024 and ocean spot rates normalized but remained swing-prone, so suppliers commonly pass through fuel, freight, and FX moves.

- In tight markets surcharge resistance limited

- Hedging and regional sourcing cut but not eliminate exposure

- Freight/fuel can represent ~10–15% of product cost

Commodity fibers vs branded inputs

Commodity cotton and polyester are highly commoditized, keeping supplier power muted in normal 2024 cycles as ICE cotton futures averaged about $0.92/lb and global polyester feedstock prices eased versus 2023. Branded performance fibers and FR backings command higher margins and technical dependency, raising supplier influence in those segments. Shortages or feedstock disruptions in 2024 shifted bargaining temporarily to suppliers. Culp’s product mix between commodity and specialty inputs thus skews its overall supplier leverage.

- Commodity inputs: lower bargaining power, price-sensitive

- Specialty inputs: higher supplier influence, technical lock-in

- 2024 disruptions: temporary supplier advantage

- Culp mix: moderates overall leverage

Suppliers retain leverage in specialty fibers, finishing chemistries and OEM machinery

Suppliers hold elevated leverage for specialty fibers, finishing chemistries and OEM machinery where technical approval, proprietary know‑how and long lead times (>12 months) limit switching. Global textile finishing chemicals were ≈$20B in 2024 and saw feedstock pass‑throughs of 10–20% in 2022–24; diesel averaged $4.00/gal and freight can be ~10–15% of cost. Commodity cotton/polyester (ICE cotton ≈$0.92/lb in 2024) reduce overall supplier power.

| Input | 2024 metric | Supplier power |

|---|---|---|

| Finishing chemicals | $20B market; 10–20% price moves | High |

| Machinery/OEM | Top vendors >60%; lead times >12m | High |

| Commodity fibers | ICE cotton ≈$0.92/lb | Low–Moderate |

What is included in the product

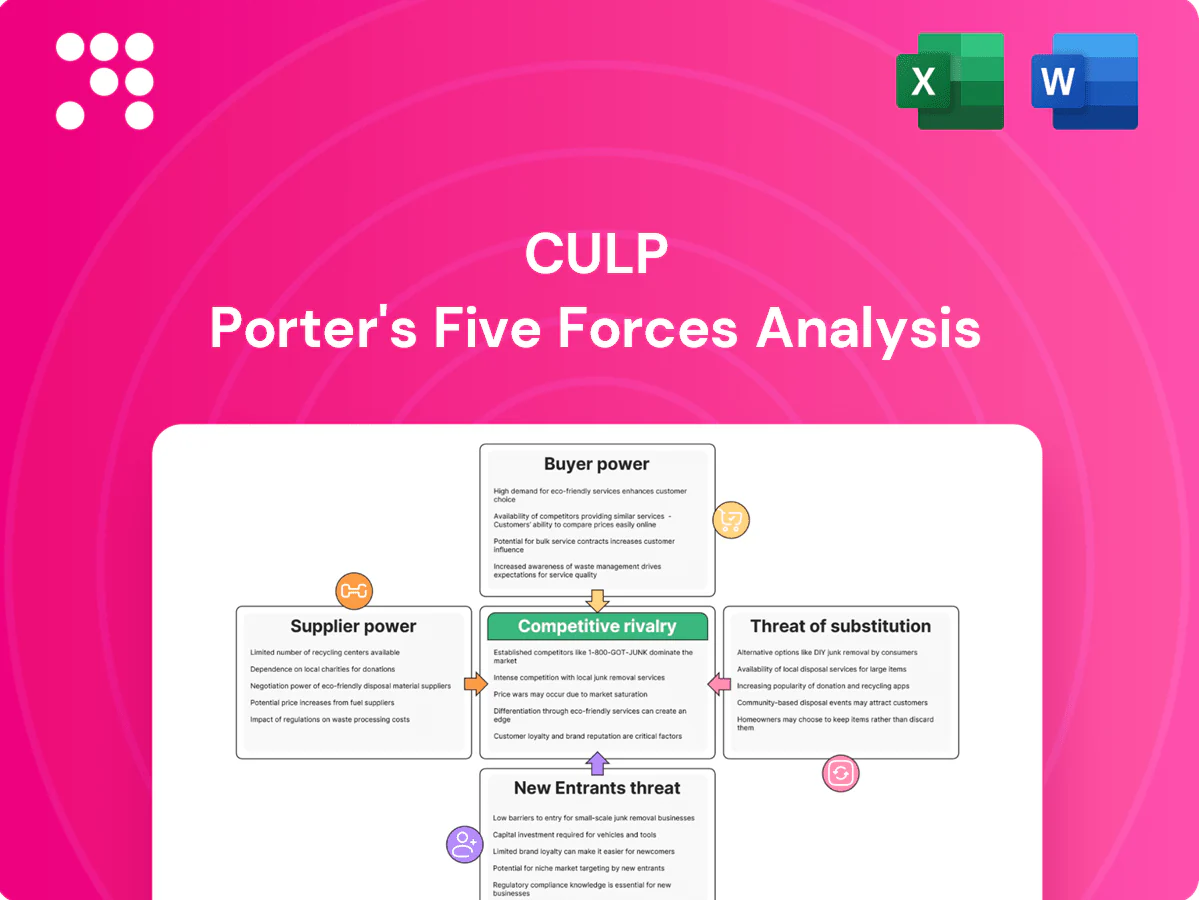

Concise Porter’s Five Forces analysis for Culp identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing, margins, and market positioning; includes emerging disruptors and actionable insights to bolster Culp’s defenses and growth opportunities.

One-sheet Culp Porter's Five Forces that instantly highlights competitive pain points and actionable pressures, with customizable scores and clean visuals ready for decks or dashboards—no complex setup required.

Customers Bargaining Power

Large, concentrated OEM customers

Mattress and furniture OEMs are highly consolidated and high-volume, with the largest mattress manufacturers capturing roughly 50–60% of US shipments in recent years; they negotiate aggressively on price and payment terms. Suppliers often have single accounts representing over 20% of sales, so losing a key OEM client materially reduces volumes and margin. This concentration raises buyer leverage across cycles, pressuring pricing and working capital.

Price sensitivity and dual‑sourcing

Buyers in 2024 commonly qualify multiple fabric mills to keep options open, using transparent benchmarks that make price competition intense; frequent benchmarking platforms accelerate bidding. Once a mill secures technical approval, switching is feasible, lowering tactile and qualification barriers. This dual‑sourcing dynamic compresses supplier pricing power and pressures margins notably during demand slowdowns.

Design collaboration creates stickiness

Design collaboration—co-developed patterns, hand-feel and performance specs—deepens integration with Culp’s customers, making fabrics and program footprints bespoke and harder to replace. Custom SKUs and just-in-time programs raise practical switching costs and lock in supply chains. High service levels and speed-to-market in 2024 frequently trump pure price, offsetting buyer power on differentiated programs.

Ability to backward/forward integrate

Large mattress brands increasingly source finished covers or bring sewing in-house, while some furniture makers import fabrics directly, reducing dependence on converters like Culp. These vertical moves lower switching costs and raise the credible threat of backward/forward integration. That threat strengthens buyer negotiating power and compresses supplier margins.

- vertical_integration

- finished_covers

- direct_imports

- reduced_supplier_reliance

- increased_bargaining_power

Demand volatility and inventory strategies

Demand volatility from retail cycles, housing trends, and promotions drives erratic order patterns; 2024 US housing starts averaged about 1.45M annualized, amplifying order swings. Buyers push inventory risk upstream, demanding short lead times and flexible MOQs. This operational leverage increases buyer power in soft markets and compresses supplier margins.

- Housing starts ~1.45M (2024 YTD)

- Short lead times and flexible MOQs demanded

- Higher buyer leverage in soft markets

Top OEMs hold 50-60% share; suppliers face >20% single-account risk amid 1.45M housing starts

Buyer concentration is high: largest mattress OEMs capture ~50–60% of US shipments, giving them strong price and payment leverage.

Many suppliers have single accounts >20% of sales, so account loss materially cuts volumes and margin.

Dual‑sourcing and benchmarking in 2024 drive intense price competition; housing starts ~1.45M amplify demand volatility.

| Metric | 2024 |

|---|---|

| Top OEM share | 50–60% |

| Single-account exposure | >20% sales |

| US housing starts | ~1.45M |

Full Version Awaits

Culp Porter's Five Forces Analysis

This preview shows the exact Culp Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The analysis is fully formatted, professionally written, and ready for immediate download and use. What you see here is the complete deliverable you'll get instantly upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Culp faces nuanced competitive dynamics where supplier leverage, buyer expectations, and substitute threats shape margin pressure and growth prospects. Our snapshot highlights how scale, brand strength, and channel control influence competitive intensity and entry barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Culp’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty yarn and fiber sources

Mattress and upholstery fabrics depend on performance yarns, specialty fibers and finishing chemistries that have a limited pool of qualified suppliers, and strict certification and consistency requirements further narrow available vendors. Fewer alternatives give suppliers pricing and allocation leverage, especially during demand surges or raw‑material disruptions. Culp can mitigate risk by multi‑sourcing and qualifying substitutes, but qualification cycles and scale‑up typically take many months to years.

Dependency on dye/finish chemicals and processes

Finishing chemistries, coatings and flame‑retardants are highly regulated and specialized, driving switching friction; the global textile finishing chemicals market was about $20 billion in 2024 and suppliers often secure fast pass‑through of feedstock inflation (price moves of 10–20% seen in 2022–24). Technical approvals and recipe know‑how typically take 3–6 months, raising time costs and reinforcing supplier bargaining power.

Capital equipment and parts from few OEMs

Jacquard looms, knitting machines and cutting/sewing automation are concentrated among a handful of global OEMs (top vendors supply >60% of these segments), creating supplier leverage; lead times often exceed 12 months and spare-parts delays of 4–16 weeks can constrain capacity. Service contracts and proprietary software locks deepen dependence and industry reports show lifecycle maintenance and upgrade costs can rise by up to 25%.

Freight, energy, and FX pass‑through

Energy-intensive processes and long-haul logistics leave Culp exposed to volatile input costs; diesel averaged about $4.00/gal in the US in 2024 and ocean spot rates normalized but remained swing-prone, so suppliers commonly pass through fuel, freight, and FX moves.

- In tight markets surcharge resistance limited

- Hedging and regional sourcing cut but not eliminate exposure

- Freight/fuel can represent ~10–15% of product cost

Commodity fibers vs branded inputs

Commodity cotton and polyester are highly commoditized, keeping supplier power muted in normal 2024 cycles as ICE cotton futures averaged about $0.92/lb and global polyester feedstock prices eased versus 2023. Branded performance fibers and FR backings command higher margins and technical dependency, raising supplier influence in those segments. Shortages or feedstock disruptions in 2024 shifted bargaining temporarily to suppliers. Culp’s product mix between commodity and specialty inputs thus skews its overall supplier leverage.

- Commodity inputs: lower bargaining power, price-sensitive

- Specialty inputs: higher supplier influence, technical lock-in

- 2024 disruptions: temporary supplier advantage

- Culp mix: moderates overall leverage

Suppliers retain leverage in specialty fibers, finishing chemistries and OEM machinery

Suppliers hold elevated leverage for specialty fibers, finishing chemistries and OEM machinery where technical approval, proprietary know‑how and long lead times (>12 months) limit switching. Global textile finishing chemicals were ≈$20B in 2024 and saw feedstock pass‑throughs of 10–20% in 2022–24; diesel averaged $4.00/gal and freight can be ~10–15% of cost. Commodity cotton/polyester (ICE cotton ≈$0.92/lb in 2024) reduce overall supplier power.

| Input | 2024 metric | Supplier power |

|---|---|---|

| Finishing chemicals | $20B market; 10–20% price moves | High |

| Machinery/OEM | Top vendors >60%; lead times >12m | High |

| Commodity fibers | ICE cotton ≈$0.92/lb | Low–Moderate |

What is included in the product

Concise Porter’s Five Forces analysis for Culp identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing, margins, and market positioning; includes emerging disruptors and actionable insights to bolster Culp’s defenses and growth opportunities.

One-sheet Culp Porter's Five Forces that instantly highlights competitive pain points and actionable pressures, with customizable scores and clean visuals ready for decks or dashboards—no complex setup required.

Customers Bargaining Power

Large, concentrated OEM customers

Mattress and furniture OEMs are highly consolidated and high-volume, with the largest mattress manufacturers capturing roughly 50–60% of US shipments in recent years; they negotiate aggressively on price and payment terms. Suppliers often have single accounts representing over 20% of sales, so losing a key OEM client materially reduces volumes and margin. This concentration raises buyer leverage across cycles, pressuring pricing and working capital.

Price sensitivity and dual‑sourcing

Buyers in 2024 commonly qualify multiple fabric mills to keep options open, using transparent benchmarks that make price competition intense; frequent benchmarking platforms accelerate bidding. Once a mill secures technical approval, switching is feasible, lowering tactile and qualification barriers. This dual‑sourcing dynamic compresses supplier pricing power and pressures margins notably during demand slowdowns.

Design collaboration creates stickiness

Design collaboration—co-developed patterns, hand-feel and performance specs—deepens integration with Culp’s customers, making fabrics and program footprints bespoke and harder to replace. Custom SKUs and just-in-time programs raise practical switching costs and lock in supply chains. High service levels and speed-to-market in 2024 frequently trump pure price, offsetting buyer power on differentiated programs.

Ability to backward/forward integrate

Large mattress brands increasingly source finished covers or bring sewing in-house, while some furniture makers import fabrics directly, reducing dependence on converters like Culp. These vertical moves lower switching costs and raise the credible threat of backward/forward integration. That threat strengthens buyer negotiating power and compresses supplier margins.

- vertical_integration

- finished_covers

- direct_imports

- reduced_supplier_reliance

- increased_bargaining_power

Demand volatility and inventory strategies

Demand volatility from retail cycles, housing trends, and promotions drives erratic order patterns; 2024 US housing starts averaged about 1.45M annualized, amplifying order swings. Buyers push inventory risk upstream, demanding short lead times and flexible MOQs. This operational leverage increases buyer power in soft markets and compresses supplier margins.

- Housing starts ~1.45M (2024 YTD)

- Short lead times and flexible MOQs demanded

- Higher buyer leverage in soft markets

Top OEMs hold 50-60% share; suppliers face >20% single-account risk amid 1.45M housing starts

Buyer concentration is high: largest mattress OEMs capture ~50–60% of US shipments, giving them strong price and payment leverage.

Many suppliers have single accounts >20% of sales, so account loss materially cuts volumes and margin.

Dual‑sourcing and benchmarking in 2024 drive intense price competition; housing starts ~1.45M amplify demand volatility.

| Metric | 2024 |

|---|---|

| Top OEM share | 50–60% |

| Single-account exposure | >20% sales |

| US housing starts | ~1.45M |

Full Version Awaits

Culp Porter's Five Forces Analysis

This preview shows the exact Culp Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The analysis is fully formatted, professionally written, and ready for immediate download and use. What you see here is the complete deliverable you'll get instantly upon payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Culp faces nuanced competitive dynamics where supplier leverage, buyer expectations, and substitute threats shape margin pressure and growth prospects. Our snapshot highlights how scale, brand strength, and channel control influence competitive intensity and entry barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Culp’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty yarn and fiber sources

Mattress and upholstery fabrics depend on performance yarns, specialty fibers and finishing chemistries that have a limited pool of qualified suppliers, and strict certification and consistency requirements further narrow available vendors. Fewer alternatives give suppliers pricing and allocation leverage, especially during demand surges or raw‑material disruptions. Culp can mitigate risk by multi‑sourcing and qualifying substitutes, but qualification cycles and scale‑up typically take many months to years.

Dependency on dye/finish chemicals and processes

Finishing chemistries, coatings and flame‑retardants are highly regulated and specialized, driving switching friction; the global textile finishing chemicals market was about $20 billion in 2024 and suppliers often secure fast pass‑through of feedstock inflation (price moves of 10–20% seen in 2022–24). Technical approvals and recipe know‑how typically take 3–6 months, raising time costs and reinforcing supplier bargaining power.

Capital equipment and parts from few OEMs

Jacquard looms, knitting machines and cutting/sewing automation are concentrated among a handful of global OEMs (top vendors supply >60% of these segments), creating supplier leverage; lead times often exceed 12 months and spare-parts delays of 4–16 weeks can constrain capacity. Service contracts and proprietary software locks deepen dependence and industry reports show lifecycle maintenance and upgrade costs can rise by up to 25%.

Freight, energy, and FX pass‑through

Energy-intensive processes and long-haul logistics leave Culp exposed to volatile input costs; diesel averaged about $4.00/gal in the US in 2024 and ocean spot rates normalized but remained swing-prone, so suppliers commonly pass through fuel, freight, and FX moves.

- In tight markets surcharge resistance limited

- Hedging and regional sourcing cut but not eliminate exposure

- Freight/fuel can represent ~10–15% of product cost

Commodity fibers vs branded inputs

Commodity cotton and polyester are highly commoditized, keeping supplier power muted in normal 2024 cycles as ICE cotton futures averaged about $0.92/lb and global polyester feedstock prices eased versus 2023. Branded performance fibers and FR backings command higher margins and technical dependency, raising supplier influence in those segments. Shortages or feedstock disruptions in 2024 shifted bargaining temporarily to suppliers. Culp’s product mix between commodity and specialty inputs thus skews its overall supplier leverage.

- Commodity inputs: lower bargaining power, price-sensitive

- Specialty inputs: higher supplier influence, technical lock-in

- 2024 disruptions: temporary supplier advantage

- Culp mix: moderates overall leverage

Suppliers retain leverage in specialty fibers, finishing chemistries and OEM machinery

Suppliers hold elevated leverage for specialty fibers, finishing chemistries and OEM machinery where technical approval, proprietary know‑how and long lead times (>12 months) limit switching. Global textile finishing chemicals were ≈$20B in 2024 and saw feedstock pass‑throughs of 10–20% in 2022–24; diesel averaged $4.00/gal and freight can be ~10–15% of cost. Commodity cotton/polyester (ICE cotton ≈$0.92/lb in 2024) reduce overall supplier power.

| Input | 2024 metric | Supplier power |

|---|---|---|

| Finishing chemicals | $20B market; 10–20% price moves | High |

| Machinery/OEM | Top vendors >60%; lead times >12m | High |

| Commodity fibers | ICE cotton ≈$0.92/lb | Low–Moderate |

What is included in the product

Concise Porter’s Five Forces analysis for Culp identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing, margins, and market positioning; includes emerging disruptors and actionable insights to bolster Culp’s defenses and growth opportunities.

One-sheet Culp Porter's Five Forces that instantly highlights competitive pain points and actionable pressures, with customizable scores and clean visuals ready for decks or dashboards—no complex setup required.

Customers Bargaining Power

Large, concentrated OEM customers

Mattress and furniture OEMs are highly consolidated and high-volume, with the largest mattress manufacturers capturing roughly 50–60% of US shipments in recent years; they negotiate aggressively on price and payment terms. Suppliers often have single accounts representing over 20% of sales, so losing a key OEM client materially reduces volumes and margin. This concentration raises buyer leverage across cycles, pressuring pricing and working capital.

Price sensitivity and dual‑sourcing

Buyers in 2024 commonly qualify multiple fabric mills to keep options open, using transparent benchmarks that make price competition intense; frequent benchmarking platforms accelerate bidding. Once a mill secures technical approval, switching is feasible, lowering tactile and qualification barriers. This dual‑sourcing dynamic compresses supplier pricing power and pressures margins notably during demand slowdowns.

Design collaboration creates stickiness

Design collaboration—co-developed patterns, hand-feel and performance specs—deepens integration with Culp’s customers, making fabrics and program footprints bespoke and harder to replace. Custom SKUs and just-in-time programs raise practical switching costs and lock in supply chains. High service levels and speed-to-market in 2024 frequently trump pure price, offsetting buyer power on differentiated programs.

Ability to backward/forward integrate

Large mattress brands increasingly source finished covers or bring sewing in-house, while some furniture makers import fabrics directly, reducing dependence on converters like Culp. These vertical moves lower switching costs and raise the credible threat of backward/forward integration. That threat strengthens buyer negotiating power and compresses supplier margins.

- vertical_integration

- finished_covers

- direct_imports

- reduced_supplier_reliance

- increased_bargaining_power

Demand volatility and inventory strategies

Demand volatility from retail cycles, housing trends, and promotions drives erratic order patterns; 2024 US housing starts averaged about 1.45M annualized, amplifying order swings. Buyers push inventory risk upstream, demanding short lead times and flexible MOQs. This operational leverage increases buyer power in soft markets and compresses supplier margins.

- Housing starts ~1.45M (2024 YTD)

- Short lead times and flexible MOQs demanded

- Higher buyer leverage in soft markets

Top OEMs hold 50-60% share; suppliers face >20% single-account risk amid 1.45M housing starts

Buyer concentration is high: largest mattress OEMs capture ~50–60% of US shipments, giving them strong price and payment leverage.

Many suppliers have single accounts >20% of sales, so account loss materially cuts volumes and margin.

Dual‑sourcing and benchmarking in 2024 drive intense price competition; housing starts ~1.45M amplify demand volatility.

| Metric | 2024 |

|---|---|

| Top OEM share | 50–60% |

| Single-account exposure | >20% sales |

| US housing starts | ~1.45M |

Full Version Awaits

Culp Porter's Five Forces Analysis

This preview shows the exact Culp Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The analysis is fully formatted, professionally written, and ready for immediate download and use. What you see here is the complete deliverable you'll get instantly upon payment.