Cummins India Porter's Five Forces Analysis

Don't Miss the Bigger Picture

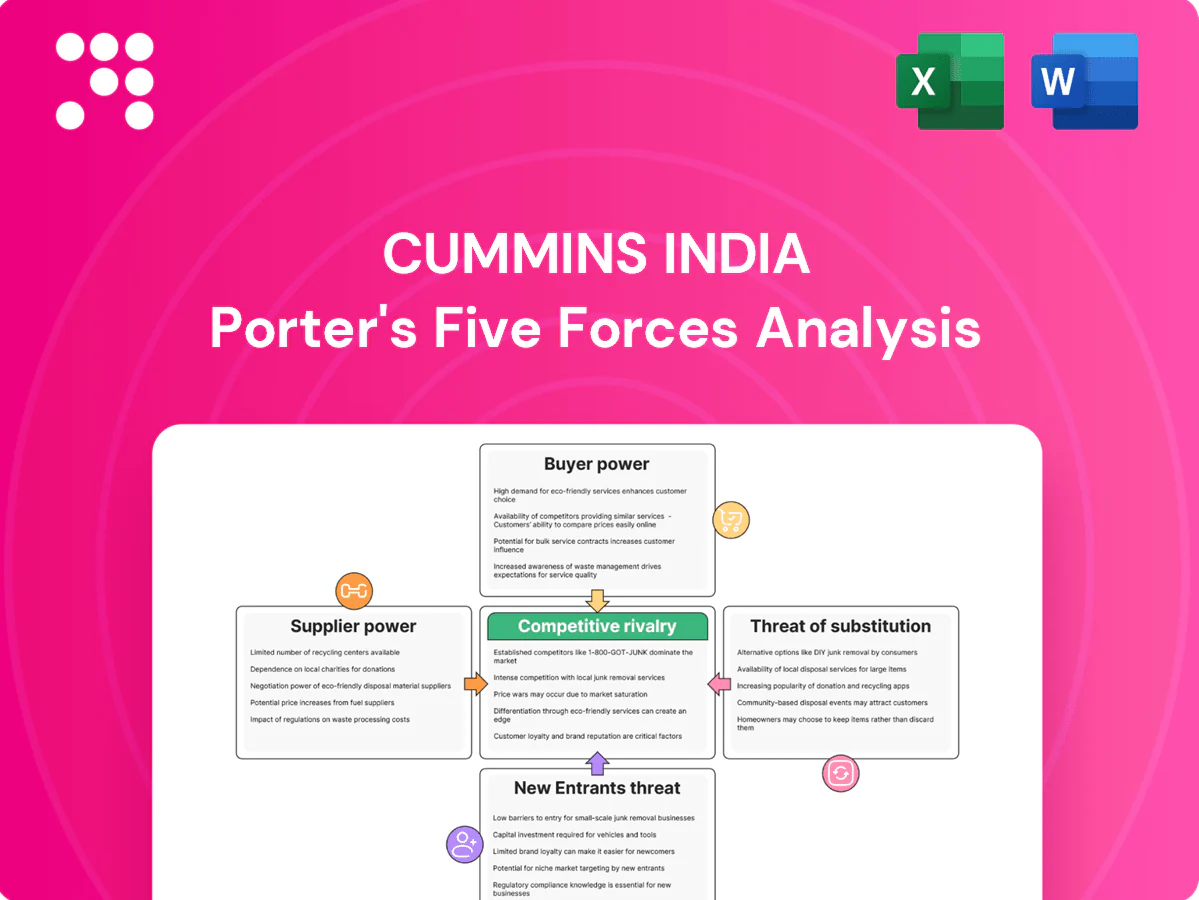

Cummins India faces moderate supplier power, intense rivalry in engines and power solutions, rising buyer price sensitivity, limited threat from new entrants, and growing substitution risk from electrification. Strengths include brand, distribution, and aftermarket services while regulatory shifts and commodity volatility pose risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cummins India’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized engine components

High-spec parts like turbochargers, fuel systems, aftertreatment and ECUs come from a limited set of qualified vendors, concentrating supplier power and raising switching costs and lead times. Cummins India benefits from Cummins’ global vendor base and formal dual-sourcing policies, reducing single-vendor exposure. Qualification cycles and validation testing typically take 6–12 months, deterring rapid supplier changes in 2024.

Engine-grade materials

Alloy steels, castings and precision machined parts for engines require micron-level tolerances and certifications such as ISO 9001 and IATF 16949 plus material traceability. Commodity volatility and strict quality needs give capable foundries and forgers pricing leverage. Long-term supply contracts and commodity hedging are used to stabilize input costs. Localization reduces import dependence and currency exposure.

Electronics and semiconductors

Power electronics and chips face cyclical shortages and allocation risk, with the global semiconductor market at roughly $556 billion in 2023 and OEMs reporting carryover allocation issues into 2024. Emission-control electronics raise content per engine, increasing supplier influence and margin exposure. Design-to-availability and alternate BOMs improve resilience, while strategic inventories and global procurement scale reduce disruption risk.

Proprietary emissions tech

Proprietary SCR, DPF, sensor and catalyst licensors hold IP advantages that elevate supplier bargaining power, especially as CPCB IV+ and BS VI norms (implemented in India from 2020) tighten component specifications through 2024, narrowing approved sources.

Cummins India’s in-house emissions tech and Pune R&D capabilities reduce external dependence, while co-development agreements with select suppliers help rebalance power and secure supply continuity.

- IP holders: concentrated

- Regulatory tightening: fewer approved vendors

- Cummins in-house R&D: lowers supplier risk

- Co-development: strategic mitigation

Logistics and energy inputs

Freight, energy prices and import duties materially affect landed cost of heavy components for Cummins India; 2024 saw global container rates ease from 2021–22 peaks, improving landed-cost pressure while oil price volatility kept energy input risk elevated. Supply‑chain shocks compress margins or extend lead times, so regional footprints and vendor‑managed inventory/nearshoring improve continuity and cut bottlenecks.

- Freight and energy drive landed cost

- Supply shocks → margin compression/longer lead times

- Regional manufacturing eases bottlenecks

- VMI and nearshoring improve continuity

Supplier power rises in engines, emissions IP & semiconductors; 6–12 months

Supplier power is elevated for high-spec engine components, emissions IP and semiconductors due to concentrated vendors, long 6–12 month qualification cycles and regulatory-approved source limits, though Cummins’ global sourcing, Pune R&D and co-development lower risk and reliance in 2024.

| Metric | Value |

|---|---|

| Qualification cycle | 6–12 months |

| Semiconductor market (2023) | $556B |

What is included in the product

Tailored Porter's Five Forces analysis for Cummins India that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary on implications for pricing, margins and market positioning.

A one-sheet Porter's Five Forces for Cummins India that clarifies supplier, buyer, rivalry, entry and substitute pressures for fast strategic decisions; customizable pressure levels and an instant radar view ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Large OEMs and EPCs

Large automotive and industrial OEMs and EPC/infra buyers place sizable recurring engine and power-system orders, with India vehicle production at about 26.2 million units in FY 2023‑24, amplifying buyer scale and negotiating clout. Their volume gives leverage to demand price concessions and stringent SLAs, often formalized via framework agreements that exchange visibility for better pricing. Performance guarantees and penalty clauses in contracts further strengthen buyer bargaining power.

Aftermarket and service

Cummins India’s large installed base drives steady demand for parts, maintenance and overhauls, creating customer lock-in and ongoing aftermarket revenue. Genuine parts and proprietary technical know-how elevate switching costs and preserve margins. Multi-year service contracts, typically 3–5 years, stabilize cash flow and dilute buyer bargaining power. Uptime-linked contracts shift procurement focus from price to value, aligning incentives on availability.

Tender-driven pricing

Tender-driven pricing forces sharp competition as public sector and large corporate tenders in 2024 often drive bids to lowest-cost; transparent benchmarks compress margins on standardized gensets. Differentiation through lower lifecycle cost and reduced emissions lets Cummins India defend pricing in specification-sensitive contracts. Pre-qualification criteria in 2024 frequently favored established OEMs with service networks and compliance track records.

Customization requirements

Segment-specific duty cycles and regulatory needs force Cummins India to deliver engineered, custom power solutions, which reduce directly comparable alternatives and lower buyer bargaining power. Buyers still solicit competitive quotes for similar specs, keeping price pressure. Application engineering teams in FY2024 remained central to win rates and margins.

- Customization narrows alternatives

- Competitive quoting persists

- Application engineering = moat

Total cost of ownership focus

Buyers focus on total cost of ownership, prioritizing fuel efficiency, reliability and nationwide service coverage over upfront price; predictive maintenance and remote monitoring (predictive maintenance market ~7.0 billion USD in 2024) strengthen Cummins India’s value proposition and lower downtime. Gas engines gain share where fuel economics favor them, and extended warranties plus uptime commitments materially reduce churn.

- Fuel efficiency & reliability over price

- Predictive maintenance market ~7.0B USD (2024)

- Gas engines competitive where fuel costs permit

- Extended warranties/uptime lower churn

Scale buyers compress margins; SLAs and ~7.0B USD predictive maintenance defend pricing

Large OEMs and infra buyers (India vehicle prod ~26.2M in FY2023‑24) exert scale-driven price/contract leverage, but Cummins India’s installed base, proprietary parts and multi-year SLAs raise switching costs and shift focus to uptime and TCO. Tender-driven low-bid dynamics compress margins, while customization, application engineering and predictive maintenance (~7.0B USD market in 2024) defend pricing.

| Metric | 2024 |

|---|---|

| India vehicle production | 26.2M |

| Predictive maintenance market | ~7.0B USD |

Preview the Actual Deliverable

Cummins India Porter's Five Forces Analysis

This preview shows the exact Cummins India Porter’s Five Forces analysis you’ll receive after purchase—no samples or placeholders. It’s the complete, professionally formatted document ready for immediate download and use. Upon payment you’ll get instant access to this same file, fully compiled and ready to support your strategic or investment decisions.

Don't Miss the Bigger Picture

Cummins India faces moderate supplier power, intense rivalry in engines and power solutions, rising buyer price sensitivity, limited threat from new entrants, and growing substitution risk from electrification. Strengths include brand, distribution, and aftermarket services while regulatory shifts and commodity volatility pose risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cummins India’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized engine components

High-spec parts like turbochargers, fuel systems, aftertreatment and ECUs come from a limited set of qualified vendors, concentrating supplier power and raising switching costs and lead times. Cummins India benefits from Cummins’ global vendor base and formal dual-sourcing policies, reducing single-vendor exposure. Qualification cycles and validation testing typically take 6–12 months, deterring rapid supplier changes in 2024.

Engine-grade materials

Alloy steels, castings and precision machined parts for engines require micron-level tolerances and certifications such as ISO 9001 and IATF 16949 plus material traceability. Commodity volatility and strict quality needs give capable foundries and forgers pricing leverage. Long-term supply contracts and commodity hedging are used to stabilize input costs. Localization reduces import dependence and currency exposure.

Electronics and semiconductors

Power electronics and chips face cyclical shortages and allocation risk, with the global semiconductor market at roughly $556 billion in 2023 and OEMs reporting carryover allocation issues into 2024. Emission-control electronics raise content per engine, increasing supplier influence and margin exposure. Design-to-availability and alternate BOMs improve resilience, while strategic inventories and global procurement scale reduce disruption risk.

Proprietary emissions tech

Proprietary SCR, DPF, sensor and catalyst licensors hold IP advantages that elevate supplier bargaining power, especially as CPCB IV+ and BS VI norms (implemented in India from 2020) tighten component specifications through 2024, narrowing approved sources.

Cummins India’s in-house emissions tech and Pune R&D capabilities reduce external dependence, while co-development agreements with select suppliers help rebalance power and secure supply continuity.

- IP holders: concentrated

- Regulatory tightening: fewer approved vendors

- Cummins in-house R&D: lowers supplier risk

- Co-development: strategic mitigation

Logistics and energy inputs

Freight, energy prices and import duties materially affect landed cost of heavy components for Cummins India; 2024 saw global container rates ease from 2021–22 peaks, improving landed-cost pressure while oil price volatility kept energy input risk elevated. Supply‑chain shocks compress margins or extend lead times, so regional footprints and vendor‑managed inventory/nearshoring improve continuity and cut bottlenecks.

- Freight and energy drive landed cost

- Supply shocks → margin compression/longer lead times

- Regional manufacturing eases bottlenecks

- VMI and nearshoring improve continuity

Supplier power rises in engines, emissions IP & semiconductors; 6–12 months

Supplier power is elevated for high-spec engine components, emissions IP and semiconductors due to concentrated vendors, long 6–12 month qualification cycles and regulatory-approved source limits, though Cummins’ global sourcing, Pune R&D and co-development lower risk and reliance in 2024.

| Metric | Value |

|---|---|

| Qualification cycle | 6–12 months |

| Semiconductor market (2023) | $556B |

What is included in the product

Tailored Porter's Five Forces analysis for Cummins India that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary on implications for pricing, margins and market positioning.

A one-sheet Porter's Five Forces for Cummins India that clarifies supplier, buyer, rivalry, entry and substitute pressures for fast strategic decisions; customizable pressure levels and an instant radar view ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Large OEMs and EPCs

Large automotive and industrial OEMs and EPC/infra buyers place sizable recurring engine and power-system orders, with India vehicle production at about 26.2 million units in FY 2023‑24, amplifying buyer scale and negotiating clout. Their volume gives leverage to demand price concessions and stringent SLAs, often formalized via framework agreements that exchange visibility for better pricing. Performance guarantees and penalty clauses in contracts further strengthen buyer bargaining power.

Aftermarket and service

Cummins India’s large installed base drives steady demand for parts, maintenance and overhauls, creating customer lock-in and ongoing aftermarket revenue. Genuine parts and proprietary technical know-how elevate switching costs and preserve margins. Multi-year service contracts, typically 3–5 years, stabilize cash flow and dilute buyer bargaining power. Uptime-linked contracts shift procurement focus from price to value, aligning incentives on availability.

Tender-driven pricing

Tender-driven pricing forces sharp competition as public sector and large corporate tenders in 2024 often drive bids to lowest-cost; transparent benchmarks compress margins on standardized gensets. Differentiation through lower lifecycle cost and reduced emissions lets Cummins India defend pricing in specification-sensitive contracts. Pre-qualification criteria in 2024 frequently favored established OEMs with service networks and compliance track records.

Customization requirements

Segment-specific duty cycles and regulatory needs force Cummins India to deliver engineered, custom power solutions, which reduce directly comparable alternatives and lower buyer bargaining power. Buyers still solicit competitive quotes for similar specs, keeping price pressure. Application engineering teams in FY2024 remained central to win rates and margins.

- Customization narrows alternatives

- Competitive quoting persists

- Application engineering = moat

Total cost of ownership focus

Buyers focus on total cost of ownership, prioritizing fuel efficiency, reliability and nationwide service coverage over upfront price; predictive maintenance and remote monitoring (predictive maintenance market ~7.0 billion USD in 2024) strengthen Cummins India’s value proposition and lower downtime. Gas engines gain share where fuel economics favor them, and extended warranties plus uptime commitments materially reduce churn.

- Fuel efficiency & reliability over price

- Predictive maintenance market ~7.0B USD (2024)

- Gas engines competitive where fuel costs permit

- Extended warranties/uptime lower churn

Scale buyers compress margins; SLAs and ~7.0B USD predictive maintenance defend pricing

Large OEMs and infra buyers (India vehicle prod ~26.2M in FY2023‑24) exert scale-driven price/contract leverage, but Cummins India’s installed base, proprietary parts and multi-year SLAs raise switching costs and shift focus to uptime and TCO. Tender-driven low-bid dynamics compress margins, while customization, application engineering and predictive maintenance (~7.0B USD market in 2024) defend pricing.

| Metric | 2024 |

|---|---|

| India vehicle production | 26.2M |

| Predictive maintenance market | ~7.0B USD |

Preview the Actual Deliverable

Cummins India Porter's Five Forces Analysis

This preview shows the exact Cummins India Porter’s Five Forces analysis you’ll receive after purchase—no samples or placeholders. It’s the complete, professionally formatted document ready for immediate download and use. Upon payment you’ll get instant access to this same file, fully compiled and ready to support your strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Cummins India faces moderate supplier power, intense rivalry in engines and power solutions, rising buyer price sensitivity, limited threat from new entrants, and growing substitution risk from electrification. Strengths include brand, distribution, and aftermarket services while regulatory shifts and commodity volatility pose risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cummins India’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized engine components

High-spec parts like turbochargers, fuel systems, aftertreatment and ECUs come from a limited set of qualified vendors, concentrating supplier power and raising switching costs and lead times. Cummins India benefits from Cummins’ global vendor base and formal dual-sourcing policies, reducing single-vendor exposure. Qualification cycles and validation testing typically take 6–12 months, deterring rapid supplier changes in 2024.

Engine-grade materials

Alloy steels, castings and precision machined parts for engines require micron-level tolerances and certifications such as ISO 9001 and IATF 16949 plus material traceability. Commodity volatility and strict quality needs give capable foundries and forgers pricing leverage. Long-term supply contracts and commodity hedging are used to stabilize input costs. Localization reduces import dependence and currency exposure.

Electronics and semiconductors

Power electronics and chips face cyclical shortages and allocation risk, with the global semiconductor market at roughly $556 billion in 2023 and OEMs reporting carryover allocation issues into 2024. Emission-control electronics raise content per engine, increasing supplier influence and margin exposure. Design-to-availability and alternate BOMs improve resilience, while strategic inventories and global procurement scale reduce disruption risk.

Proprietary emissions tech

Proprietary SCR, DPF, sensor and catalyst licensors hold IP advantages that elevate supplier bargaining power, especially as CPCB IV+ and BS VI norms (implemented in India from 2020) tighten component specifications through 2024, narrowing approved sources.

Cummins India’s in-house emissions tech and Pune R&D capabilities reduce external dependence, while co-development agreements with select suppliers help rebalance power and secure supply continuity.

- IP holders: concentrated

- Regulatory tightening: fewer approved vendors

- Cummins in-house R&D: lowers supplier risk

- Co-development: strategic mitigation

Logistics and energy inputs

Freight, energy prices and import duties materially affect landed cost of heavy components for Cummins India; 2024 saw global container rates ease from 2021–22 peaks, improving landed-cost pressure while oil price volatility kept energy input risk elevated. Supply‑chain shocks compress margins or extend lead times, so regional footprints and vendor‑managed inventory/nearshoring improve continuity and cut bottlenecks.

- Freight and energy drive landed cost

- Supply shocks → margin compression/longer lead times

- Regional manufacturing eases bottlenecks

- VMI and nearshoring improve continuity

Supplier power rises in engines, emissions IP & semiconductors; 6–12 months

Supplier power is elevated for high-spec engine components, emissions IP and semiconductors due to concentrated vendors, long 6–12 month qualification cycles and regulatory-approved source limits, though Cummins’ global sourcing, Pune R&D and co-development lower risk and reliance in 2024.

| Metric | Value |

|---|---|

| Qualification cycle | 6–12 months |

| Semiconductor market (2023) | $556B |

What is included in the product

Tailored Porter's Five Forces analysis for Cummins India that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary on implications for pricing, margins and market positioning.

A one-sheet Porter's Five Forces for Cummins India that clarifies supplier, buyer, rivalry, entry and substitute pressures for fast strategic decisions; customizable pressure levels and an instant radar view ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Large OEMs and EPCs

Large automotive and industrial OEMs and EPC/infra buyers place sizable recurring engine and power-system orders, with India vehicle production at about 26.2 million units in FY 2023‑24, amplifying buyer scale and negotiating clout. Their volume gives leverage to demand price concessions and stringent SLAs, often formalized via framework agreements that exchange visibility for better pricing. Performance guarantees and penalty clauses in contracts further strengthen buyer bargaining power.

Aftermarket and service

Cummins India’s large installed base drives steady demand for parts, maintenance and overhauls, creating customer lock-in and ongoing aftermarket revenue. Genuine parts and proprietary technical know-how elevate switching costs and preserve margins. Multi-year service contracts, typically 3–5 years, stabilize cash flow and dilute buyer bargaining power. Uptime-linked contracts shift procurement focus from price to value, aligning incentives on availability.

Tender-driven pricing

Tender-driven pricing forces sharp competition as public sector and large corporate tenders in 2024 often drive bids to lowest-cost; transparent benchmarks compress margins on standardized gensets. Differentiation through lower lifecycle cost and reduced emissions lets Cummins India defend pricing in specification-sensitive contracts. Pre-qualification criteria in 2024 frequently favored established OEMs with service networks and compliance track records.

Customization requirements

Segment-specific duty cycles and regulatory needs force Cummins India to deliver engineered, custom power solutions, which reduce directly comparable alternatives and lower buyer bargaining power. Buyers still solicit competitive quotes for similar specs, keeping price pressure. Application engineering teams in FY2024 remained central to win rates and margins.

- Customization narrows alternatives

- Competitive quoting persists

- Application engineering = moat

Total cost of ownership focus

Buyers focus on total cost of ownership, prioritizing fuel efficiency, reliability and nationwide service coverage over upfront price; predictive maintenance and remote monitoring (predictive maintenance market ~7.0 billion USD in 2024) strengthen Cummins India’s value proposition and lower downtime. Gas engines gain share where fuel economics favor them, and extended warranties plus uptime commitments materially reduce churn.

- Fuel efficiency & reliability over price

- Predictive maintenance market ~7.0B USD (2024)

- Gas engines competitive where fuel costs permit

- Extended warranties/uptime lower churn

Scale buyers compress margins; SLAs and ~7.0B USD predictive maintenance defend pricing

Large OEMs and infra buyers (India vehicle prod ~26.2M in FY2023‑24) exert scale-driven price/contract leverage, but Cummins India’s installed base, proprietary parts and multi-year SLAs raise switching costs and shift focus to uptime and TCO. Tender-driven low-bid dynamics compress margins, while customization, application engineering and predictive maintenance (~7.0B USD market in 2024) defend pricing.

| Metric | 2024 |

|---|---|

| India vehicle production | 26.2M |

| Predictive maintenance market | ~7.0B USD |

Preview the Actual Deliverable

Cummins India Porter's Five Forces Analysis

This preview shows the exact Cummins India Porter’s Five Forces analysis you’ll receive after purchase—no samples or placeholders. It’s the complete, professionally formatted document ready for immediate download and use. Upon payment you’ll get instant access to this same file, fully compiled and ready to support your strategic or investment decisions.