CURO Business Model Canvas

Strategic playbook: Business Model Canvas for scaling, margin and revenue insight

Discover CURO’s strategic playbook with our concise Business Model Canvas—three to five-sentence insights into its value propositions, customer segments, and revenue mechanics that reveal how CURO scales and sustains margin. Ready for deep analysis? Purchase the full, editable Canvas to deploy these insights in your strategy, due diligence, or investor materials.

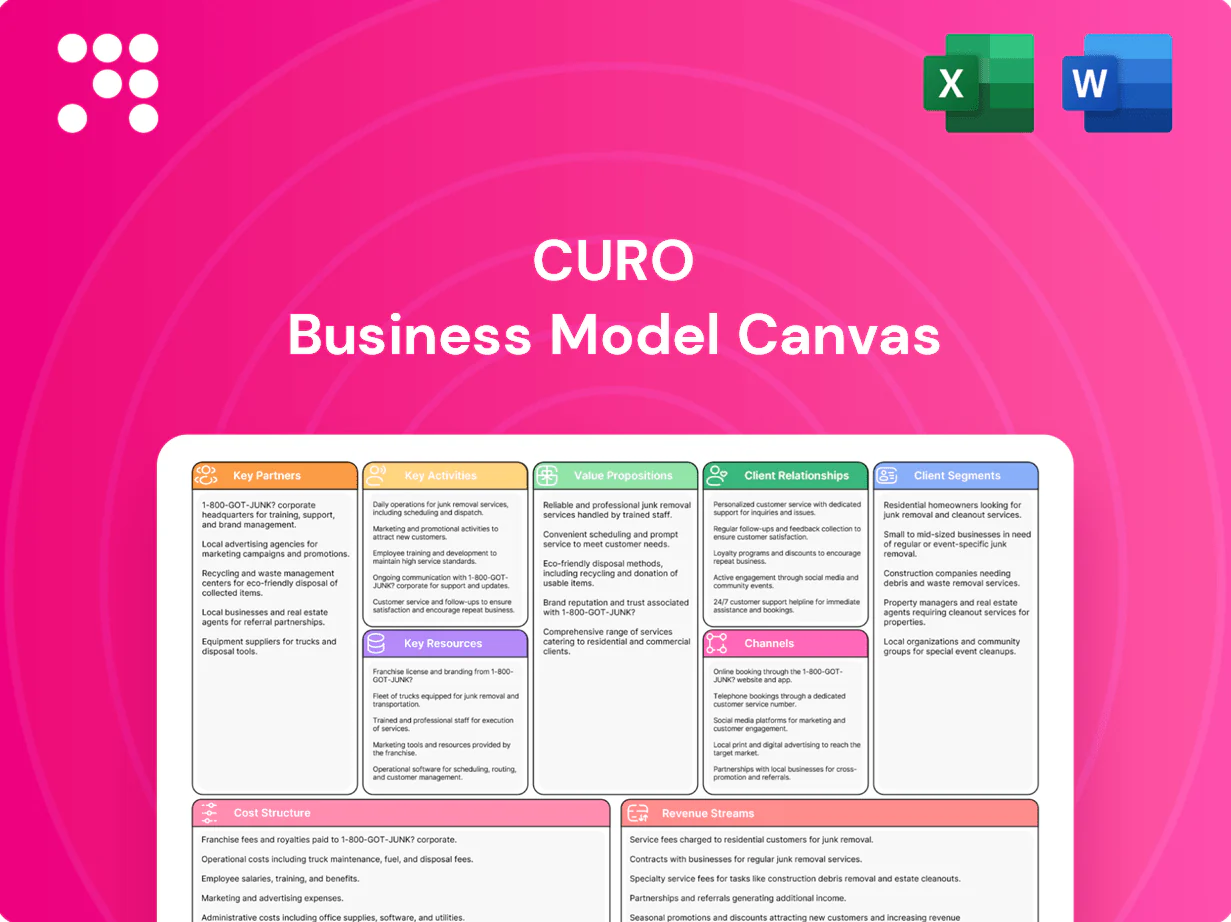

Partnerships

Banking and capital providers

In 2024 CURO’s relationships with banks, credit facilities and institutional lenders supply the funding to originate loans, ensuring operational continuity and regulatory compliance. Stable capital lines support growth and seasonality, smoothing origination volumes across quarters. A diversified lender base reduces funding risk and pricing pressure and enables securitization or whole-loan sales when advantageous.

Payment processors and money movement

Payment processors enable ACH, debit and instant disbursements/repayments, with the ACH network handling over 30 billion transactions annually as of 2024, improving speed and cash flow. Reliable rails cut failed payments and friction, boosting customer experience and lowering delinquencies. Negotiated fees protect margins at scale, while processor redundancy limits downtime and collections disruption.

Credit bureaus and data vendors

Credit bureaus and data vendors supply credit files, alternative data and identity signals that strengthen CURO underwriting for underbanked profiles and enable expanded approvals. Ongoing daily or real-time feeds support account monitoring and dynamic line management. Dispute handling and FCRA-mandated investigation timelines (30 days under 15 U.S.C. §1681i) ensure regulatory compliance in 2024.

Compliance, legal, and regulatory advisors

Compliance, legal, and regulatory advisors guide CURO through multi-jurisdictional lending requirements across 50+ markets, implement policies for disclosures, fair lending, and privacy, and provide rapid interpretation of rule changes to reduce enforcement risk and litigation exposure while training staff and conducting audits to reinforce a compliant culture.

- specialists: multi-jurisdiction expertise

- policies: disclosures, fair lending, privacy

- speed: rapid rule interpretation

- controls: training & audits

Collections and servicing partners

External agencies complement CURO’s in-house collections for late-stage accounts, with performance-based contracts tying fees to net recoveries (industry fee ranges ~10–25% in 2024). Payment-plan and hardship partners boost cure rates and lower roll rates, while vendors supply skip-tracing and recovery analytics to increase contact rates and recoveries.

- performance-based fees: 10–25% (2024 industry range)

- skip-trace & analytics: higher contact/recovery rates

- payment-plan & hardship partners: improved cure rates

Diversified funding across 50+ markets, ACH scale of 30B txns/yr boosts origination and recovery

CURO relies on diversified bank and institutional funding to smooth origination volumes and enable securitization across 50+ markets in 2024. Payment processors (ACH ~30 billion txns/yr as of 2024) and redundant rails reduce failures and speed disbursements. External recovery partners use performance fees (industry 10–25% in 2024) and skip‑trace analytics to lift recoveries.

| Partner | Role | 2024 metric |

|---|---|---|

| Lenders | Funding/capital lines | 50+ markets |

| Processors | Disburse/repay | ACH ~30B txns/yr |

| Collectors | Late-stage recovery | Fees 10–25% |

What is included in the product

A comprehensive pre-written Business Model Canvas tailored to CURO’s strategy, covering nine BMC blocks with detailed customer segments, value propositions, channels, revenue streams and core operations; includes competitive analysis and SWOT linkage, and a clean, polished design for investor presentations, internal planning, and validation using real company data.

CURO Business Model Canvas delivers a clean, editable one-page snapshot that saves hours of formatting by structuring core components for fast boardroom-ready summaries and seamless team collaboration.

Activities

Risk underwriting and pricing

Model development uses alternative data to assess repayment probability for thin-file borrowers, enabling approvals where traditional scores fail. Pricing balances modeled risk with regulatory limits such as the 36% APR Military Lending Act cap and customer affordability metrics. Champion–challenger testing refines cutoffs and yield. Continuous monitoring adjusts pricing and reserves to macro shifts like 2024 US CPI ~3.4%.

Loan origination and servicing

Streamlined application, verification, and funding processes maximize conversion by reducing time-to-fund and dropout rates, with automated ID and income checks accelerating decisions. Servicing handles statements, payment reminders, and renewals to sustain repayment performance. Hardship accommodations and extensions are processed within policy and regulatory frameworks to mitigate losses. Quality control enforces data accuracy and preserves customer trust.

Fraud prevention and identity verification

Device, behavioral, and KYC tools block first‑ and third‑party fraud by correlating device signals, transaction patterns, and verified identity data; industry deployments reported multi‑layer stacks cut fraud attempts substantially in 2024. Step‑up authentication reduces friction for good customers by allowing low‑risk flows to stay seamless while escalating only suspicious sessions. Loss analytics target rings and mule behavior with network analysis and feedback loops that continually refine rules and machine‑learning models.

Regulatory compliance management

Policies and controls enforce clear disclosures, UDAP/UDAAP and privacy safeguards; licensing and reporting cover federal, state and provincial requirements; complaint handling and QA drive remediation cycles; ongoing training and audits sustain compliance. CFPB logged over 1 million consumer complaints in 2024, underscoring remediation and reporting workloads.

- Disclosures, UDAP/UDAAP, privacy controls

- Licensing/reporting across federal, state, provincial rules

- Complaint handling + QA → remediation

- Training and audits for continuous adherence

Marketing and omnichannel distribution

Marketing and omnichannel distribution combine digital acquisition that targets intent and underserved audiences with retail locations that build trust and local access; partnerships and affiliates expand reach cost-effectively while CRM drives repeat usage and cross-sells, supporting unit economics and customer lifetime value.

- Digital-first: targets intent/underserved

- Retail: trust + local access

- Partners: low-cost scale

- CRM: repeat sales, cross-sell

Alt-data opens thin-file approvals; pricing capped at 36% APR

Alt-data modeling extends approvals to thin-file borrowers while pricing adheres to caps like the 36% APR MLA and reacts to 2024 US CPI ~3.4%.

Fast digital onboarding, automated verifications and servicing sustain conversion and repayment; hardship workflows and reserves mitigate losses.

Multi-layer fraud/KYC, compliance (UDAP/UDAAP, licensing) and omnichannel marketing drive growth and risk control; CFPB logged >1M complaints in 2024.

| Activity | Key 2024 Metric | Note |

|---|---|---|

| Modeling/Pricing | CPI 3.4% / MLA 36% APR | Alt-data for thin-file |

| Onboarding/Servicing | Automated verif. speed | Lower dropout, faster funding |

| Fraud/Compliance | CFPB >1M complaints | Multi-layer controls |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual CURO Business Model Canvas, not a mockup or sample. When you purchase, you'll receive this exact file with all content and pages included. The deliverable is provided in editable Word and Excel formats, ready to present, edit, or share.

Strategic playbook: Business Model Canvas for scaling, margin and revenue insight

Discover CURO’s strategic playbook with our concise Business Model Canvas—three to five-sentence insights into its value propositions, customer segments, and revenue mechanics that reveal how CURO scales and sustains margin. Ready for deep analysis? Purchase the full, editable Canvas to deploy these insights in your strategy, due diligence, or investor materials.

Partnerships

Banking and capital providers

In 2024 CURO’s relationships with banks, credit facilities and institutional lenders supply the funding to originate loans, ensuring operational continuity and regulatory compliance. Stable capital lines support growth and seasonality, smoothing origination volumes across quarters. A diversified lender base reduces funding risk and pricing pressure and enables securitization or whole-loan sales when advantageous.

Payment processors and money movement

Payment processors enable ACH, debit and instant disbursements/repayments, with the ACH network handling over 30 billion transactions annually as of 2024, improving speed and cash flow. Reliable rails cut failed payments and friction, boosting customer experience and lowering delinquencies. Negotiated fees protect margins at scale, while processor redundancy limits downtime and collections disruption.

Credit bureaus and data vendors

Credit bureaus and data vendors supply credit files, alternative data and identity signals that strengthen CURO underwriting for underbanked profiles and enable expanded approvals. Ongoing daily or real-time feeds support account monitoring and dynamic line management. Dispute handling and FCRA-mandated investigation timelines (30 days under 15 U.S.C. §1681i) ensure regulatory compliance in 2024.

Compliance, legal, and regulatory advisors

Compliance, legal, and regulatory advisors guide CURO through multi-jurisdictional lending requirements across 50+ markets, implement policies for disclosures, fair lending, and privacy, and provide rapid interpretation of rule changes to reduce enforcement risk and litigation exposure while training staff and conducting audits to reinforce a compliant culture.

- specialists: multi-jurisdiction expertise

- policies: disclosures, fair lending, privacy

- speed: rapid rule interpretation

- controls: training & audits

Collections and servicing partners

External agencies complement CURO’s in-house collections for late-stage accounts, with performance-based contracts tying fees to net recoveries (industry fee ranges ~10–25% in 2024). Payment-plan and hardship partners boost cure rates and lower roll rates, while vendors supply skip-tracing and recovery analytics to increase contact rates and recoveries.

- performance-based fees: 10–25% (2024 industry range)

- skip-trace & analytics: higher contact/recovery rates

- payment-plan & hardship partners: improved cure rates

Diversified funding across 50+ markets, ACH scale of 30B txns/yr boosts origination and recovery

CURO relies on diversified bank and institutional funding to smooth origination volumes and enable securitization across 50+ markets in 2024. Payment processors (ACH ~30 billion txns/yr as of 2024) and redundant rails reduce failures and speed disbursements. External recovery partners use performance fees (industry 10–25% in 2024) and skip‑trace analytics to lift recoveries.

| Partner | Role | 2024 metric |

|---|---|---|

| Lenders | Funding/capital lines | 50+ markets |

| Processors | Disburse/repay | ACH ~30B txns/yr |

| Collectors | Late-stage recovery | Fees 10–25% |

What is included in the product

A comprehensive pre-written Business Model Canvas tailored to CURO’s strategy, covering nine BMC blocks with detailed customer segments, value propositions, channels, revenue streams and core operations; includes competitive analysis and SWOT linkage, and a clean, polished design for investor presentations, internal planning, and validation using real company data.

CURO Business Model Canvas delivers a clean, editable one-page snapshot that saves hours of formatting by structuring core components for fast boardroom-ready summaries and seamless team collaboration.

Activities

Risk underwriting and pricing

Model development uses alternative data to assess repayment probability for thin-file borrowers, enabling approvals where traditional scores fail. Pricing balances modeled risk with regulatory limits such as the 36% APR Military Lending Act cap and customer affordability metrics. Champion–challenger testing refines cutoffs and yield. Continuous monitoring adjusts pricing and reserves to macro shifts like 2024 US CPI ~3.4%.

Loan origination and servicing

Streamlined application, verification, and funding processes maximize conversion by reducing time-to-fund and dropout rates, with automated ID and income checks accelerating decisions. Servicing handles statements, payment reminders, and renewals to sustain repayment performance. Hardship accommodations and extensions are processed within policy and regulatory frameworks to mitigate losses. Quality control enforces data accuracy and preserves customer trust.

Fraud prevention and identity verification

Device, behavioral, and KYC tools block first‑ and third‑party fraud by correlating device signals, transaction patterns, and verified identity data; industry deployments reported multi‑layer stacks cut fraud attempts substantially in 2024. Step‑up authentication reduces friction for good customers by allowing low‑risk flows to stay seamless while escalating only suspicious sessions. Loss analytics target rings and mule behavior with network analysis and feedback loops that continually refine rules and machine‑learning models.

Regulatory compliance management

Policies and controls enforce clear disclosures, UDAP/UDAAP and privacy safeguards; licensing and reporting cover federal, state and provincial requirements; complaint handling and QA drive remediation cycles; ongoing training and audits sustain compliance. CFPB logged over 1 million consumer complaints in 2024, underscoring remediation and reporting workloads.

- Disclosures, UDAP/UDAAP, privacy controls

- Licensing/reporting across federal, state, provincial rules

- Complaint handling + QA → remediation

- Training and audits for continuous adherence

Marketing and omnichannel distribution

Marketing and omnichannel distribution combine digital acquisition that targets intent and underserved audiences with retail locations that build trust and local access; partnerships and affiliates expand reach cost-effectively while CRM drives repeat usage and cross-sells, supporting unit economics and customer lifetime value.

- Digital-first: targets intent/underserved

- Retail: trust + local access

- Partners: low-cost scale

- CRM: repeat sales, cross-sell

Alt-data opens thin-file approvals; pricing capped at 36% APR

Alt-data modeling extends approvals to thin-file borrowers while pricing adheres to caps like the 36% APR MLA and reacts to 2024 US CPI ~3.4%.

Fast digital onboarding, automated verifications and servicing sustain conversion and repayment; hardship workflows and reserves mitigate losses.

Multi-layer fraud/KYC, compliance (UDAP/UDAAP, licensing) and omnichannel marketing drive growth and risk control; CFPB logged >1M complaints in 2024.

| Activity | Key 2024 Metric | Note |

|---|---|---|

| Modeling/Pricing | CPI 3.4% / MLA 36% APR | Alt-data for thin-file |

| Onboarding/Servicing | Automated verif. speed | Lower dropout, faster funding |

| Fraud/Compliance | CFPB >1M complaints | Multi-layer controls |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual CURO Business Model Canvas, not a mockup or sample. When you purchase, you'll receive this exact file with all content and pages included. The deliverable is provided in editable Word and Excel formats, ready to present, edit, or share.

Description

Strategic playbook: Business Model Canvas for scaling, margin and revenue insight

Discover CURO’s strategic playbook with our concise Business Model Canvas—three to five-sentence insights into its value propositions, customer segments, and revenue mechanics that reveal how CURO scales and sustains margin. Ready for deep analysis? Purchase the full, editable Canvas to deploy these insights in your strategy, due diligence, or investor materials.

Partnerships

Banking and capital providers

In 2024 CURO’s relationships with banks, credit facilities and institutional lenders supply the funding to originate loans, ensuring operational continuity and regulatory compliance. Stable capital lines support growth and seasonality, smoothing origination volumes across quarters. A diversified lender base reduces funding risk and pricing pressure and enables securitization or whole-loan sales when advantageous.

Payment processors and money movement

Payment processors enable ACH, debit and instant disbursements/repayments, with the ACH network handling over 30 billion transactions annually as of 2024, improving speed and cash flow. Reliable rails cut failed payments and friction, boosting customer experience and lowering delinquencies. Negotiated fees protect margins at scale, while processor redundancy limits downtime and collections disruption.

Credit bureaus and data vendors

Credit bureaus and data vendors supply credit files, alternative data and identity signals that strengthen CURO underwriting for underbanked profiles and enable expanded approvals. Ongoing daily or real-time feeds support account monitoring and dynamic line management. Dispute handling and FCRA-mandated investigation timelines (30 days under 15 U.S.C. §1681i) ensure regulatory compliance in 2024.

Compliance, legal, and regulatory advisors

Compliance, legal, and regulatory advisors guide CURO through multi-jurisdictional lending requirements across 50+ markets, implement policies for disclosures, fair lending, and privacy, and provide rapid interpretation of rule changes to reduce enforcement risk and litigation exposure while training staff and conducting audits to reinforce a compliant culture.

- specialists: multi-jurisdiction expertise

- policies: disclosures, fair lending, privacy

- speed: rapid rule interpretation

- controls: training & audits

Collections and servicing partners

External agencies complement CURO’s in-house collections for late-stage accounts, with performance-based contracts tying fees to net recoveries (industry fee ranges ~10–25% in 2024). Payment-plan and hardship partners boost cure rates and lower roll rates, while vendors supply skip-tracing and recovery analytics to increase contact rates and recoveries.

- performance-based fees: 10–25% (2024 industry range)

- skip-trace & analytics: higher contact/recovery rates

- payment-plan & hardship partners: improved cure rates

Diversified funding across 50+ markets, ACH scale of 30B txns/yr boosts origination and recovery

CURO relies on diversified bank and institutional funding to smooth origination volumes and enable securitization across 50+ markets in 2024. Payment processors (ACH ~30 billion txns/yr as of 2024) and redundant rails reduce failures and speed disbursements. External recovery partners use performance fees (industry 10–25% in 2024) and skip‑trace analytics to lift recoveries.

| Partner | Role | 2024 metric |

|---|---|---|

| Lenders | Funding/capital lines | 50+ markets |

| Processors | Disburse/repay | ACH ~30B txns/yr |

| Collectors | Late-stage recovery | Fees 10–25% |

What is included in the product

A comprehensive pre-written Business Model Canvas tailored to CURO’s strategy, covering nine BMC blocks with detailed customer segments, value propositions, channels, revenue streams and core operations; includes competitive analysis and SWOT linkage, and a clean, polished design for investor presentations, internal planning, and validation using real company data.

CURO Business Model Canvas delivers a clean, editable one-page snapshot that saves hours of formatting by structuring core components for fast boardroom-ready summaries and seamless team collaboration.

Activities

Risk underwriting and pricing

Model development uses alternative data to assess repayment probability for thin-file borrowers, enabling approvals where traditional scores fail. Pricing balances modeled risk with regulatory limits such as the 36% APR Military Lending Act cap and customer affordability metrics. Champion–challenger testing refines cutoffs and yield. Continuous monitoring adjusts pricing and reserves to macro shifts like 2024 US CPI ~3.4%.

Loan origination and servicing

Streamlined application, verification, and funding processes maximize conversion by reducing time-to-fund and dropout rates, with automated ID and income checks accelerating decisions. Servicing handles statements, payment reminders, and renewals to sustain repayment performance. Hardship accommodations and extensions are processed within policy and regulatory frameworks to mitigate losses. Quality control enforces data accuracy and preserves customer trust.

Fraud prevention and identity verification

Device, behavioral, and KYC tools block first‑ and third‑party fraud by correlating device signals, transaction patterns, and verified identity data; industry deployments reported multi‑layer stacks cut fraud attempts substantially in 2024. Step‑up authentication reduces friction for good customers by allowing low‑risk flows to stay seamless while escalating only suspicious sessions. Loss analytics target rings and mule behavior with network analysis and feedback loops that continually refine rules and machine‑learning models.

Regulatory compliance management

Policies and controls enforce clear disclosures, UDAP/UDAAP and privacy safeguards; licensing and reporting cover federal, state and provincial requirements; complaint handling and QA drive remediation cycles; ongoing training and audits sustain compliance. CFPB logged over 1 million consumer complaints in 2024, underscoring remediation and reporting workloads.

- Disclosures, UDAP/UDAAP, privacy controls

- Licensing/reporting across federal, state, provincial rules

- Complaint handling + QA → remediation

- Training and audits for continuous adherence

Marketing and omnichannel distribution

Marketing and omnichannel distribution combine digital acquisition that targets intent and underserved audiences with retail locations that build trust and local access; partnerships and affiliates expand reach cost-effectively while CRM drives repeat usage and cross-sells, supporting unit economics and customer lifetime value.

- Digital-first: targets intent/underserved

- Retail: trust + local access

- Partners: low-cost scale

- CRM: repeat sales, cross-sell

Alt-data opens thin-file approvals; pricing capped at 36% APR

Alt-data modeling extends approvals to thin-file borrowers while pricing adheres to caps like the 36% APR MLA and reacts to 2024 US CPI ~3.4%.

Fast digital onboarding, automated verifications and servicing sustain conversion and repayment; hardship workflows and reserves mitigate losses.

Multi-layer fraud/KYC, compliance (UDAP/UDAAP, licensing) and omnichannel marketing drive growth and risk control; CFPB logged >1M complaints in 2024.

| Activity | Key 2024 Metric | Note |

|---|---|---|

| Modeling/Pricing | CPI 3.4% / MLA 36% APR | Alt-data for thin-file |

| Onboarding/Servicing | Automated verif. speed | Lower dropout, faster funding |

| Fraud/Compliance | CFPB >1M complaints | Multi-layer controls |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the actual CURO Business Model Canvas, not a mockup or sample. When you purchase, you'll receive this exact file with all content and pages included. The deliverable is provided in editable Word and Excel formats, ready to present, edit, or share.