Currys PESTLE Analysis

Skip the Research. Get the Strategy.

Our Currys PESTLE Analysis highlights how political shifts, economic pressures, and rapid tech disruption are reshaping its retail strategy. See actionable insights on regulatory risks, consumer trends, and sustainability drivers. Ideal for investors and strategists seeking an evidence-based edge. Purchase the full report for the complete, ready-to-use breakdown and forecasts.

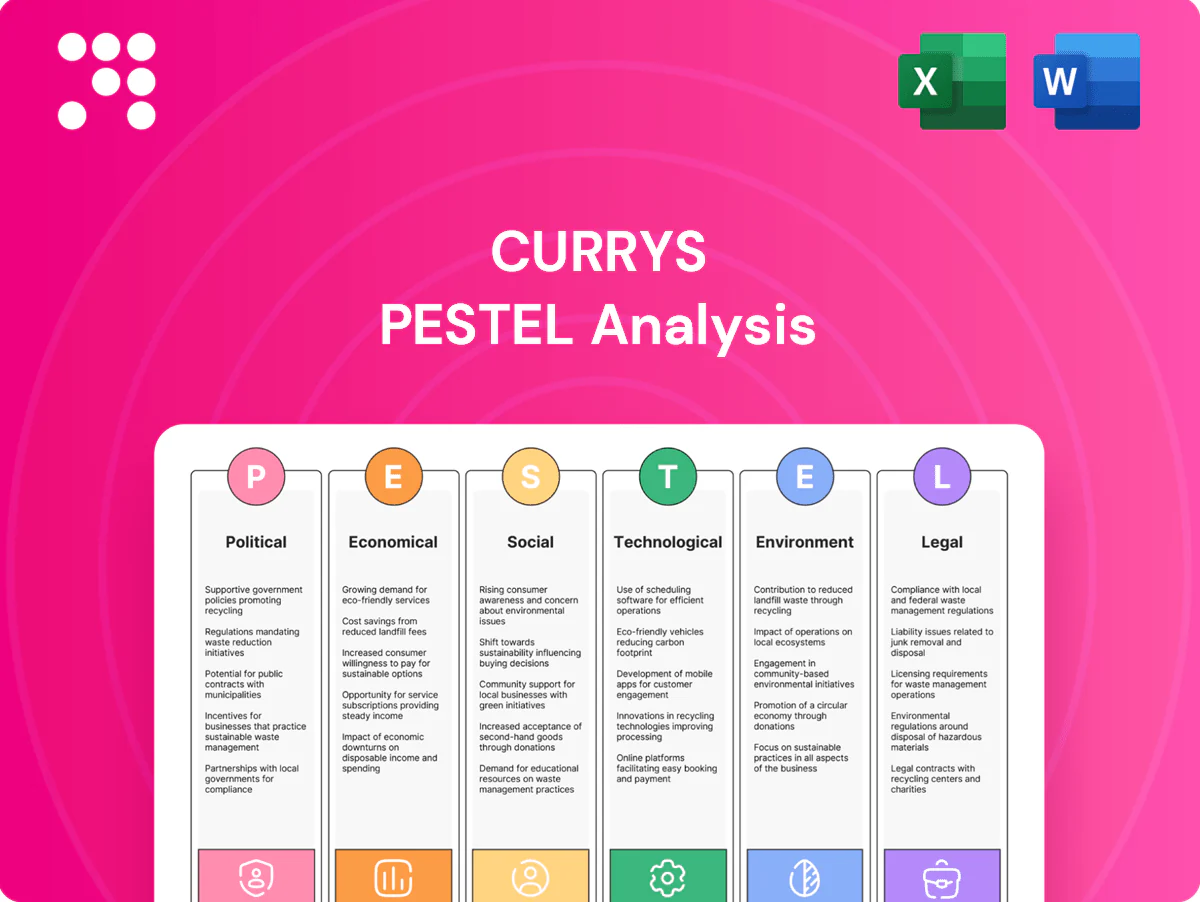

Political factors

UK trade and Brexit rules

Post-Brexit customs, rules-of-origin and VAT processes (VAT postponed accounting introduced Jan 2021) add clearance complexity that affects timing and landed cost for electronics; the EU still accounted for about 42% of UK goods and services trade in 2023, so smooth flows matter for Currys inventory availability. Delays or paperwork errors increase lead times and can raise working capital requirements by extending inventory days, forcing pricing or margin adjustments if duties or compliance costs rise.

Industrial and digital policy

Government digital policy, notably Project Gigabit’s ≈£5bn rollout, raises broadband access and can boost Currys’ smart product uptake as 96% of UK households have internet access. Grants and tax incentives for low‑energy appliances and retrofit schemes increase demand for energy‑efficient ranges. Policy shifts could divert funding away from consumer tech, so Currys should monitor BEIS and DCMS consultations to align product mixes and services.

Trade tariffs and geopolitics

Tariffs on components from Asia and 2024-25 restrictions on Chinese tech risk raising Currys' input costs and narrowing assortment, while ongoing geopolitical tension since the 2020s has intermittently disrupted semiconductor supply chains. Currys must diversify suppliers across regions and negotiate supply contracts to protect margins. Active hedging and flexible multi-sourcing strategies reduce exposure to sudden shocks.

Public spending and consumer relief

Energy bill support measures largely wound down after the 2022–23 interventions, while the UK standard VAT rate remains 20%, so any temporary VAT cuts on appliances would materially pull forward demand for Currys. Cost-of-living policy shifts in 2024–25 continue to compress discretionary spend on electronics, so Currys can align targeted promotions with fiscal windows.

- VAT rate 20% — potential lever

- Energy support scaled back since 2023

- Monitor budgets and fiscal statements quarterly

- Time promotions to policy announcements

Devolution and local regulations

Regional recycling, planning and retail rules in the UK and Ireland differ (eg WEEE compliance for electronics), and Currys operates around 300 stores across both markets so permitting and business rates materially affect store economics and site selection. Cross-border differences force bespoke compliance processes and local stakeholder engagement speeds approvals and roll-outs.

- Regional WEEE rules

- ~300 stores UK & Ireland

- Permitting & business rates impact margins

- Local engagement eases execution

Post-Brexit customs raise clearance costs; EU trade ≈ 42%, VAT 20%

Post‑Brexit customs and VAT rules add clearance complexity affecting Currys' inventory and working capital; EU was ~42% of UK trade in 2023. Project Gigabit (~£5bn) and 96% household internet access boost smart product demand; VAT 20% and reduced energy support constrain discretionary spend. ~300 stores face varying WEEE, business rates and permitting costs.

| Metric | Value |

|---|---|

| EU share of UK trade (2023) | ≈42% |

| Project Gigabit | ≈£5bn |

| Household internet access | ≈96% |

| VAT | 20% |

| Stores (UK & Ireland) | ≈300 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Currys across six dimensions—Political, Economic, Social, Technological, Environmental and Legal—with data and trends tied to the UK/European consumer electronics and retail market. Designed for executives, consultants and investors, it provides detailed sub-points, forward-looking insights and scenario implications ready for business plans, pitch decks and strategy.

Concise, visually segmented Currys PESTLE summary that distills external risks and opportunities into an easily shareable, editable slide or note—perfect for quick alignment in meetings, strategy sessions, or client reports.

Economic factors

Consumer confidence and real incomes

Cost-of-living pressures curb demand for big-ticket electronics and white goods as UK CPI fell to about 2.1% by mid-2024 while GfK consumer confidence remained weak around -28, squeezing discretionary spend. Real regular pay rose roughly 3.3% year-on-year to mid-2024 (ONS), supporting some upgrade cycles. Currys can lean on financing, bundles and aftercare to sustain basket sizes, and should flex promotional intensity with sentiment.

Inflation and interest rates

High Bank of England base rate at 5.25% and persistent UK CPI around 4.0% dampen credit-funded appliance and tech purchases and raise Currys’ financing costs. Input and freight inflation—shipping rates up to double 2020 levels in peak years—squeeze gross margins. Price elasticity varies sharply by category, forcing precise, data-led pricing. Tight inventory turns and disciplined markdowns are vital to protect margins.

FX exposure and sourcing

USD and EUR movements materially affect Currys landed costs for globally sourced tech: in 2024 average GBP/USD was about 1.27 and GBP/EUR about 1.17, pushing import prices when sterling weakens. Hedging via forwards and options can smooth cashflow but cannot eliminate spot-driven margin shocks. Assortment planning should model multiple currency scenarios and pass-through elasticities. Supplier negotiations can allocate FX risk via currency clauses or shared hedging.

Supply chain and semiconductor cycles

Component tightness or gluts shift availability and pricing, causing short-term margin pressure on consumer electronics; lead-time variability forces Currys to hold higher stock or increase working capital to avoid out-of-stock losses.

Currys leverages vendor partnerships and demand-forecasting tools to smooth purchasing cycles, while services and repairs revenue help offset hardware margin swings and stabilize gross margin.

- Supply volatility: affects pricing and stock

- Lead times: raise inventory and working capital

- Vendor ties: improve availability and forecasting

- Services: buffer hardware margin fluctuations

E-commerce growth and channel mix

UK online retail accounted for about 30.8% of sales in 2024 (ONS), and consumer electronics sees roughly 60% online penetration (Statista 2023), so Currys' online share materially raises fulfillment and last-mile costs while shifting cost-to-serve. Click-and-collect and ship-from-store improve margins and speed; omnichannel customers typically spend more and return less, boosting cohort LTV. Investment should follow cohort profitability, prioritising high-LTV, low-return segments.

- Online share: 30.8% (ONS 2024)

- Electronics online ~60% (Statista 2023)

- Omnichannel: higher spend, lower returns

- Prioritise investments by cohort profitability

Post-Brexit customs raise clearance costs; EU trade ≈ 42%, VAT 20%

Cost-of-living and weak confidence (GfK -28) curb big-ticket demand despite real regular pay +3.3% yoy to mid-2024; Currys must drive financing, bundles and targeted promos. High BoE rate 5.25% and FX moves (GBP/USD ~1.27) raise funding and import costs, pressuring margins. Omnichannel mix (online retail 30.8%, electronics ~60% online) shifts cost-to-serve toward fulfillment.

| Metric | Value |

|---|---|

| GfK Consumer Confidence | -28 |

| Real pay (mid-2024) | +3.3% yoy |

| BoE base rate | 5.25% |

Preview the Actual Deliverable

Currys PESTLE Analysis

The preview shown here is the exact Currys PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or teasers—this is the final, professionally structured file.

Skip the Research. Get the Strategy.

Our Currys PESTLE Analysis highlights how political shifts, economic pressures, and rapid tech disruption are reshaping its retail strategy. See actionable insights on regulatory risks, consumer trends, and sustainability drivers. Ideal for investors and strategists seeking an evidence-based edge. Purchase the full report for the complete, ready-to-use breakdown and forecasts.

Political factors

UK trade and Brexit rules

Post-Brexit customs, rules-of-origin and VAT processes (VAT postponed accounting introduced Jan 2021) add clearance complexity that affects timing and landed cost for electronics; the EU still accounted for about 42% of UK goods and services trade in 2023, so smooth flows matter for Currys inventory availability. Delays or paperwork errors increase lead times and can raise working capital requirements by extending inventory days, forcing pricing or margin adjustments if duties or compliance costs rise.

Industrial and digital policy

Government digital policy, notably Project Gigabit’s ≈£5bn rollout, raises broadband access and can boost Currys’ smart product uptake as 96% of UK households have internet access. Grants and tax incentives for low‑energy appliances and retrofit schemes increase demand for energy‑efficient ranges. Policy shifts could divert funding away from consumer tech, so Currys should monitor BEIS and DCMS consultations to align product mixes and services.

Trade tariffs and geopolitics

Tariffs on components from Asia and 2024-25 restrictions on Chinese tech risk raising Currys' input costs and narrowing assortment, while ongoing geopolitical tension since the 2020s has intermittently disrupted semiconductor supply chains. Currys must diversify suppliers across regions and negotiate supply contracts to protect margins. Active hedging and flexible multi-sourcing strategies reduce exposure to sudden shocks.

Public spending and consumer relief

Energy bill support measures largely wound down after the 2022–23 interventions, while the UK standard VAT rate remains 20%, so any temporary VAT cuts on appliances would materially pull forward demand for Currys. Cost-of-living policy shifts in 2024–25 continue to compress discretionary spend on electronics, so Currys can align targeted promotions with fiscal windows.

- VAT rate 20% — potential lever

- Energy support scaled back since 2023

- Monitor budgets and fiscal statements quarterly

- Time promotions to policy announcements

Devolution and local regulations

Regional recycling, planning and retail rules in the UK and Ireland differ (eg WEEE compliance for electronics), and Currys operates around 300 stores across both markets so permitting and business rates materially affect store economics and site selection. Cross-border differences force bespoke compliance processes and local stakeholder engagement speeds approvals and roll-outs.

- Regional WEEE rules

- ~300 stores UK & Ireland

- Permitting & business rates impact margins

- Local engagement eases execution

Post-Brexit customs raise clearance costs; EU trade ≈ 42%, VAT 20%

Post‑Brexit customs and VAT rules add clearance complexity affecting Currys' inventory and working capital; EU was ~42% of UK trade in 2023. Project Gigabit (~£5bn) and 96% household internet access boost smart product demand; VAT 20% and reduced energy support constrain discretionary spend. ~300 stores face varying WEEE, business rates and permitting costs.

| Metric | Value |

|---|---|

| EU share of UK trade (2023) | ≈42% |

| Project Gigabit | ≈£5bn |

| Household internet access | ≈96% |

| VAT | 20% |

| Stores (UK & Ireland) | ≈300 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Currys across six dimensions—Political, Economic, Social, Technological, Environmental and Legal—with data and trends tied to the UK/European consumer electronics and retail market. Designed for executives, consultants and investors, it provides detailed sub-points, forward-looking insights and scenario implications ready for business plans, pitch decks and strategy.

Concise, visually segmented Currys PESTLE summary that distills external risks and opportunities into an easily shareable, editable slide or note—perfect for quick alignment in meetings, strategy sessions, or client reports.

Economic factors

Consumer confidence and real incomes

Cost-of-living pressures curb demand for big-ticket electronics and white goods as UK CPI fell to about 2.1% by mid-2024 while GfK consumer confidence remained weak around -28, squeezing discretionary spend. Real regular pay rose roughly 3.3% year-on-year to mid-2024 (ONS), supporting some upgrade cycles. Currys can lean on financing, bundles and aftercare to sustain basket sizes, and should flex promotional intensity with sentiment.

Inflation and interest rates

High Bank of England base rate at 5.25% and persistent UK CPI around 4.0% dampen credit-funded appliance and tech purchases and raise Currys’ financing costs. Input and freight inflation—shipping rates up to double 2020 levels in peak years—squeeze gross margins. Price elasticity varies sharply by category, forcing precise, data-led pricing. Tight inventory turns and disciplined markdowns are vital to protect margins.

FX exposure and sourcing

USD and EUR movements materially affect Currys landed costs for globally sourced tech: in 2024 average GBP/USD was about 1.27 and GBP/EUR about 1.17, pushing import prices when sterling weakens. Hedging via forwards and options can smooth cashflow but cannot eliminate spot-driven margin shocks. Assortment planning should model multiple currency scenarios and pass-through elasticities. Supplier negotiations can allocate FX risk via currency clauses or shared hedging.

Supply chain and semiconductor cycles

Component tightness or gluts shift availability and pricing, causing short-term margin pressure on consumer electronics; lead-time variability forces Currys to hold higher stock or increase working capital to avoid out-of-stock losses.

Currys leverages vendor partnerships and demand-forecasting tools to smooth purchasing cycles, while services and repairs revenue help offset hardware margin swings and stabilize gross margin.

- Supply volatility: affects pricing and stock

- Lead times: raise inventory and working capital

- Vendor ties: improve availability and forecasting

- Services: buffer hardware margin fluctuations

E-commerce growth and channel mix

UK online retail accounted for about 30.8% of sales in 2024 (ONS), and consumer electronics sees roughly 60% online penetration (Statista 2023), so Currys' online share materially raises fulfillment and last-mile costs while shifting cost-to-serve. Click-and-collect and ship-from-store improve margins and speed; omnichannel customers typically spend more and return less, boosting cohort LTV. Investment should follow cohort profitability, prioritising high-LTV, low-return segments.

- Online share: 30.8% (ONS 2024)

- Electronics online ~60% (Statista 2023)

- Omnichannel: higher spend, lower returns

- Prioritise investments by cohort profitability

Post-Brexit customs raise clearance costs; EU trade ≈ 42%, VAT 20%

Cost-of-living and weak confidence (GfK -28) curb big-ticket demand despite real regular pay +3.3% yoy to mid-2024; Currys must drive financing, bundles and targeted promos. High BoE rate 5.25% and FX moves (GBP/USD ~1.27) raise funding and import costs, pressuring margins. Omnichannel mix (online retail 30.8%, electronics ~60% online) shifts cost-to-serve toward fulfillment.

| Metric | Value |

|---|---|

| GfK Consumer Confidence | -28 |

| Real pay (mid-2024) | +3.3% yoy |

| BoE base rate | 5.25% |

Preview the Actual Deliverable

Currys PESTLE Analysis

The preview shown here is the exact Currys PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or teasers—this is the final, professionally structured file.

Description

Skip the Research. Get the Strategy.

Our Currys PESTLE Analysis highlights how political shifts, economic pressures, and rapid tech disruption are reshaping its retail strategy. See actionable insights on regulatory risks, consumer trends, and sustainability drivers. Ideal for investors and strategists seeking an evidence-based edge. Purchase the full report for the complete, ready-to-use breakdown and forecasts.

Political factors

UK trade and Brexit rules

Post-Brexit customs, rules-of-origin and VAT processes (VAT postponed accounting introduced Jan 2021) add clearance complexity that affects timing and landed cost for electronics; the EU still accounted for about 42% of UK goods and services trade in 2023, so smooth flows matter for Currys inventory availability. Delays or paperwork errors increase lead times and can raise working capital requirements by extending inventory days, forcing pricing or margin adjustments if duties or compliance costs rise.

Industrial and digital policy

Government digital policy, notably Project Gigabit’s ≈£5bn rollout, raises broadband access and can boost Currys’ smart product uptake as 96% of UK households have internet access. Grants and tax incentives for low‑energy appliances and retrofit schemes increase demand for energy‑efficient ranges. Policy shifts could divert funding away from consumer tech, so Currys should monitor BEIS and DCMS consultations to align product mixes and services.

Trade tariffs and geopolitics

Tariffs on components from Asia and 2024-25 restrictions on Chinese tech risk raising Currys' input costs and narrowing assortment, while ongoing geopolitical tension since the 2020s has intermittently disrupted semiconductor supply chains. Currys must diversify suppliers across regions and negotiate supply contracts to protect margins. Active hedging and flexible multi-sourcing strategies reduce exposure to sudden shocks.

Public spending and consumer relief

Energy bill support measures largely wound down after the 2022–23 interventions, while the UK standard VAT rate remains 20%, so any temporary VAT cuts on appliances would materially pull forward demand for Currys. Cost-of-living policy shifts in 2024–25 continue to compress discretionary spend on electronics, so Currys can align targeted promotions with fiscal windows.

- VAT rate 20% — potential lever

- Energy support scaled back since 2023

- Monitor budgets and fiscal statements quarterly

- Time promotions to policy announcements

Devolution and local regulations

Regional recycling, planning and retail rules in the UK and Ireland differ (eg WEEE compliance for electronics), and Currys operates around 300 stores across both markets so permitting and business rates materially affect store economics and site selection. Cross-border differences force bespoke compliance processes and local stakeholder engagement speeds approvals and roll-outs.

- Regional WEEE rules

- ~300 stores UK & Ireland

- Permitting & business rates impact margins

- Local engagement eases execution

Post-Brexit customs raise clearance costs; EU trade ≈ 42%, VAT 20%

Post‑Brexit customs and VAT rules add clearance complexity affecting Currys' inventory and working capital; EU was ~42% of UK trade in 2023. Project Gigabit (~£5bn) and 96% household internet access boost smart product demand; VAT 20% and reduced energy support constrain discretionary spend. ~300 stores face varying WEEE, business rates and permitting costs.

| Metric | Value |

|---|---|

| EU share of UK trade (2023) | ≈42% |

| Project Gigabit | ≈£5bn |

| Household internet access | ≈96% |

| VAT | 20% |

| Stores (UK & Ireland) | ≈300 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Currys across six dimensions—Political, Economic, Social, Technological, Environmental and Legal—with data and trends tied to the UK/European consumer electronics and retail market. Designed for executives, consultants and investors, it provides detailed sub-points, forward-looking insights and scenario implications ready for business plans, pitch decks and strategy.

Concise, visually segmented Currys PESTLE summary that distills external risks and opportunities into an easily shareable, editable slide or note—perfect for quick alignment in meetings, strategy sessions, or client reports.

Economic factors

Consumer confidence and real incomes

Cost-of-living pressures curb demand for big-ticket electronics and white goods as UK CPI fell to about 2.1% by mid-2024 while GfK consumer confidence remained weak around -28, squeezing discretionary spend. Real regular pay rose roughly 3.3% year-on-year to mid-2024 (ONS), supporting some upgrade cycles. Currys can lean on financing, bundles and aftercare to sustain basket sizes, and should flex promotional intensity with sentiment.

Inflation and interest rates

High Bank of England base rate at 5.25% and persistent UK CPI around 4.0% dampen credit-funded appliance and tech purchases and raise Currys’ financing costs. Input and freight inflation—shipping rates up to double 2020 levels in peak years—squeeze gross margins. Price elasticity varies sharply by category, forcing precise, data-led pricing. Tight inventory turns and disciplined markdowns are vital to protect margins.

FX exposure and sourcing

USD and EUR movements materially affect Currys landed costs for globally sourced tech: in 2024 average GBP/USD was about 1.27 and GBP/EUR about 1.17, pushing import prices when sterling weakens. Hedging via forwards and options can smooth cashflow but cannot eliminate spot-driven margin shocks. Assortment planning should model multiple currency scenarios and pass-through elasticities. Supplier negotiations can allocate FX risk via currency clauses or shared hedging.

Supply chain and semiconductor cycles

Component tightness or gluts shift availability and pricing, causing short-term margin pressure on consumer electronics; lead-time variability forces Currys to hold higher stock or increase working capital to avoid out-of-stock losses.

Currys leverages vendor partnerships and demand-forecasting tools to smooth purchasing cycles, while services and repairs revenue help offset hardware margin swings and stabilize gross margin.

- Supply volatility: affects pricing and stock

- Lead times: raise inventory and working capital

- Vendor ties: improve availability and forecasting

- Services: buffer hardware margin fluctuations

E-commerce growth and channel mix

UK online retail accounted for about 30.8% of sales in 2024 (ONS), and consumer electronics sees roughly 60% online penetration (Statista 2023), so Currys' online share materially raises fulfillment and last-mile costs while shifting cost-to-serve. Click-and-collect and ship-from-store improve margins and speed; omnichannel customers typically spend more and return less, boosting cohort LTV. Investment should follow cohort profitability, prioritising high-LTV, low-return segments.

- Online share: 30.8% (ONS 2024)

- Electronics online ~60% (Statista 2023)

- Omnichannel: higher spend, lower returns

- Prioritise investments by cohort profitability

Post-Brexit customs raise clearance costs; EU trade ≈ 42%, VAT 20%

Cost-of-living and weak confidence (GfK -28) curb big-ticket demand despite real regular pay +3.3% yoy to mid-2024; Currys must drive financing, bundles and targeted promos. High BoE rate 5.25% and FX moves (GBP/USD ~1.27) raise funding and import costs, pressuring margins. Omnichannel mix (online retail 30.8%, electronics ~60% online) shifts cost-to-serve toward fulfillment.

| Metric | Value |

|---|---|

| GfK Consumer Confidence | -28 |

| Real pay (mid-2024) | +3.3% yoy |

| BoE base rate | 5.25% |

Preview the Actual Deliverable

Currys PESTLE Analysis

The preview shown here is the exact Currys PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or teasers—this is the final, professionally structured file.