CVS Health SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

CVS Health’s SWOT reveals how scale, vertical integration, and digital investments counter regulatory pressure, reimbursement shifts, and retail competition. Explore actionable strengths, weaknesses, opportunities, and threats tailored for investors and strategists. Discover the full picture with our complete SWOT analysis—purchase now for the editable report and Excel matrix.

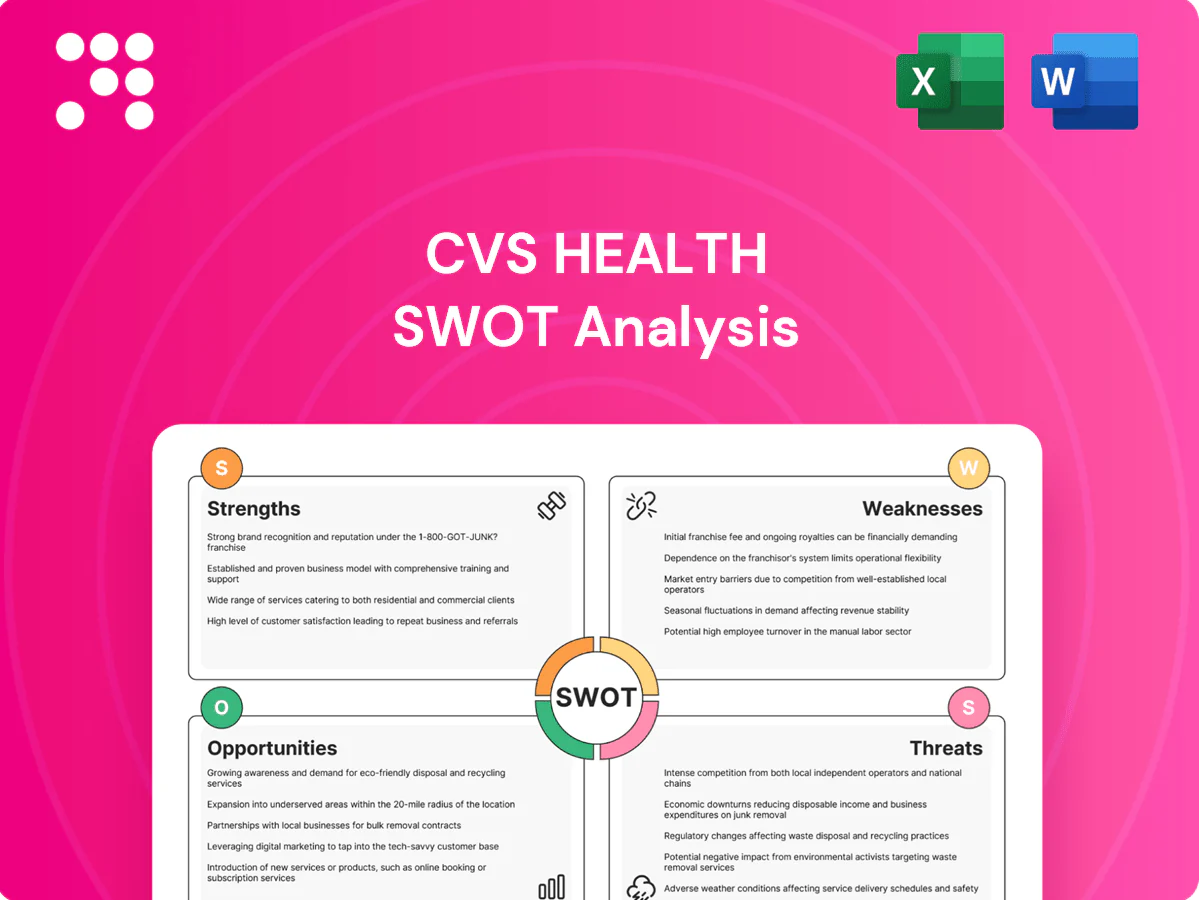

Strengths

Vertically integrated care model

CVS Health combines Caremark PBM (serving over 100 million members), Aetna insurance (~22 million members), ~9,900 retail pharmacies and 1,100+ MinuteClinics to control costs and outcomes. Integration enables data sharing, coordinated care and steerage to in‑network services, creating member and sponsor stickiness. This vertical model supports value‑based care and medical cost containment through aligned incentives and utilization management.

Massive scale and distribution

CVS operates ~9,900 retail pharmacies and 1,100+ MinuteClinic/HealthHUB sites nationwide, supporting 2024 revenue of about $322 billion. This scale delivers strong purchasing leverage with manufacturers and wholesalers, lowering cost of goods. Broad, convenient footprint boosts medication adherence and customer retention. It enables rapid rollout of new care models and services across markets.

Strong PBM capabilities

Caremark's robust formulary management, rebates aggregation and specialty pharmacy expertise support optimized plan design and utilization management across tens of millions of members. Advanced analytics drive utilization edits and plan design optimization, while high mail-order and specialty penetration materially boosts margins. CVS reports measurable drug trend control for employers and payers, with billions in negotiated rebates and specialty savings annually.

Diversified revenue streams

CVS Health's diversified revenue mix — spanning pharmacy services, health benefits and retail — produced over $300 billion in revenue in 2024, giving balanced exposure across payors and channels. This mix reduces reliance on any single reimbursement source and creates material cross-selling between PBM, insurance and retail care. Strong operating cash flow has supported multi‑billion dollar investment and deleveraging initiatives.

- Revenue > $300B (2024)

- Balanced exposure: PBM, benefits, retail

- Enables cross-selling across segments

- Cash flow funds investment and debt paydown

Data and clinical assets

CVS Health combines multi-year medical and pharmacy claims from Aetna and its retail network, supporting longitudinal analytics across millions of members and encounters.

Integrated clinical programs for chronic care, medication adherence, and specialty care coordination enable personalized interventions at point of fill and care sites across 9,900+ pharmacies and ~1,100 clinics.

These assets power risk scoring, fraud/waste/abuse detection and outcomes measurement to improve quality and lower cost.

- Claims: multi-year, member-level

- Sites: 9,900+ pharmacies; ~1,100 clinics

- Uses: risk scoring, FWA detection, outcomes

Integrated PBM, payer, retail & clinic network; $322B revenue

CVS Health integrates Caremark PBM (100M+ members), Aetna (~22M members), ~9,900 pharmacies and ~1,100 clinics to drive coordinated, value‑based care and cost control. 2024 revenue ~ $322B with strong operating cash flow funding investment and deleveraging. Robust formulary, specialty pharmacy and analytics deliver rebates, utilization management and margin expansion.

| Metric | 2024 |

|---|---|

| Revenue | $322B |

| PBM members | 100M+ |

| Aetna members | 22M |

| Retail sites | 9,900 |

| Clinics | 1,100+ |

What is included in the product

Delivers a strategic overview of CVS Health’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position across retail pharmacy, health services, and pharmacy benefit management.

Provides a concise CVS Health SWOT matrix for fast, visual strategy alignment, highlighting pharmacy, PBM, retail strengths and material risks. Editable spreadsheet format allows easy updates to reflect regulatory shifts, M&A activity, and changing consumer trends for quick stakeholder review.

Weaknesses

Margin pressure in retail pharmacy

Reimbursement compression and unpredictable DIR fee dynamics have compressed pharmacy margins, reducing pharmacy gross margin contribution despite scale. Front-store traffic faces growing e-commerce competition, with digital prescriptions and online retailers capturing incremental share. Rising labor costs and shrink elevated operating expenses. CVS’s legacy footprint of about 9,900 U.S. stores limits agility to shutter low-performing locations.

Integration and execution complexity

Multiple acquired assets, notably Aetna (deal ~$69 billion) and Signify Health (approximate $8 billion), require ongoing harmonization of systems and culture across CVS’s roughly 300,000 employees. The complex operating model elevates risk of service lapses and cost overruns that could erode margins. IT modernization and interoperability demand significant capital, and execution missteps can dilute projected synergies and ROI.

Debt load from acquisitions

CVS carries elevated leverage from major acquisitions, with net leverage around 3.5x on a trailing-12-month basis in 2024 versus lower ratios at pure-play peers; total debt remained high into 2024. Higher interest expense—roughly $3.2 billion in 2024—limits capital allocation and buyback capacity. Deleveraging could stretch further in a weak macro or reimbursement downturn, and credit ratings (S&P BBB, Moody’s Baa2) keep financing costs sensitive to shocks.

Regulatory scrutiny and litigation exposure

Regulatory scrutiny around PBM practices, rebate structures and prior opioid-related matters creates significant legal and settlement exposure; PBMs now manage over 80% of US prescription claims, drawing intense oversight, and nationwide opioid litigation has produced tens of billions in settlements that raise precedent risk for CVS.

- PBM/rebates: heightened investigation risk

- Opioid legacy: exposure to large settlements

- Compliance: rising, resource-intensive demands

- Pricing transparency: threatens existing margins

- Adverse rulings: potential earnings and reputational hit

Perception and customer experience challenges

Consumer sentiment toward PBMs and retail pharmacies is mixed; CVS faces perception risk despite Caremark covering over 100 million lives and nearly 10,000 stores. Store wait times, staffing shortages and service variability drive dissatisfaction and fuel churn to competitors, while brand complexity blurs propositions across segments and negative press can accelerate defections.

- Perception: mixed on PBMs

- Scale: >100M lives, ~10,000 stores

- Operations: wait times & staffing

- Reputation: negative press → higher churn

DIR fee volatility and reimbursement compression plus integration risk squeeze margins

Reimbursement compression and DIR fee volatility have squeezed pharmacy margins despite scale. E‑commerce and digital scripts erode front‑store traffic while rising labor and shrink inflate costs. Complex post‑Aetna/Signify integration across ~300,000 employees and ~9,900 stores raises execution and IT modernization risk. Elevated leverage (net leverage ~3.5x TTM 2024) and ~$3.2B 2024 interest expense limit capital flexibility.

| Metric | Value |

|---|---|

| U.S. stores | ~9,900 |

| Employees | ~300,000 |

| Caremark lives | >100M |

| Net leverage (TTM 2024) | ~3.5x |

| Interest expense (2024) | ~$3.2B |

Full Version Awaits

CVS Health SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the final CVS Health SWOT report you'll get. Purchase unlocks the full, editable version ready for use.

Elevate Your Analysis with the Complete SWOT Report

CVS Health’s SWOT reveals how scale, vertical integration, and digital investments counter regulatory pressure, reimbursement shifts, and retail competition. Explore actionable strengths, weaknesses, opportunities, and threats tailored for investors and strategists. Discover the full picture with our complete SWOT analysis—purchase now for the editable report and Excel matrix.

Strengths

Vertically integrated care model

CVS Health combines Caremark PBM (serving over 100 million members), Aetna insurance (~22 million members), ~9,900 retail pharmacies and 1,100+ MinuteClinics to control costs and outcomes. Integration enables data sharing, coordinated care and steerage to in‑network services, creating member and sponsor stickiness. This vertical model supports value‑based care and medical cost containment through aligned incentives and utilization management.

Massive scale and distribution

CVS operates ~9,900 retail pharmacies and 1,100+ MinuteClinic/HealthHUB sites nationwide, supporting 2024 revenue of about $322 billion. This scale delivers strong purchasing leverage with manufacturers and wholesalers, lowering cost of goods. Broad, convenient footprint boosts medication adherence and customer retention. It enables rapid rollout of new care models and services across markets.

Strong PBM capabilities

Caremark's robust formulary management, rebates aggregation and specialty pharmacy expertise support optimized plan design and utilization management across tens of millions of members. Advanced analytics drive utilization edits and plan design optimization, while high mail-order and specialty penetration materially boosts margins. CVS reports measurable drug trend control for employers and payers, with billions in negotiated rebates and specialty savings annually.

Diversified revenue streams

CVS Health's diversified revenue mix — spanning pharmacy services, health benefits and retail — produced over $300 billion in revenue in 2024, giving balanced exposure across payors and channels. This mix reduces reliance on any single reimbursement source and creates material cross-selling between PBM, insurance and retail care. Strong operating cash flow has supported multi‑billion dollar investment and deleveraging initiatives.

- Revenue > $300B (2024)

- Balanced exposure: PBM, benefits, retail

- Enables cross-selling across segments

- Cash flow funds investment and debt paydown

Data and clinical assets

CVS Health combines multi-year medical and pharmacy claims from Aetna and its retail network, supporting longitudinal analytics across millions of members and encounters.

Integrated clinical programs for chronic care, medication adherence, and specialty care coordination enable personalized interventions at point of fill and care sites across 9,900+ pharmacies and ~1,100 clinics.

These assets power risk scoring, fraud/waste/abuse detection and outcomes measurement to improve quality and lower cost.

- Claims: multi-year, member-level

- Sites: 9,900+ pharmacies; ~1,100 clinics

- Uses: risk scoring, FWA detection, outcomes

Integrated PBM, payer, retail & clinic network; $322B revenue

CVS Health integrates Caremark PBM (100M+ members), Aetna (~22M members), ~9,900 pharmacies and ~1,100 clinics to drive coordinated, value‑based care and cost control. 2024 revenue ~ $322B with strong operating cash flow funding investment and deleveraging. Robust formulary, specialty pharmacy and analytics deliver rebates, utilization management and margin expansion.

| Metric | 2024 |

|---|---|

| Revenue | $322B |

| PBM members | 100M+ |

| Aetna members | 22M |

| Retail sites | 9,900 |

| Clinics | 1,100+ |

What is included in the product

Delivers a strategic overview of CVS Health’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position across retail pharmacy, health services, and pharmacy benefit management.

Provides a concise CVS Health SWOT matrix for fast, visual strategy alignment, highlighting pharmacy, PBM, retail strengths and material risks. Editable spreadsheet format allows easy updates to reflect regulatory shifts, M&A activity, and changing consumer trends for quick stakeholder review.

Weaknesses

Margin pressure in retail pharmacy

Reimbursement compression and unpredictable DIR fee dynamics have compressed pharmacy margins, reducing pharmacy gross margin contribution despite scale. Front-store traffic faces growing e-commerce competition, with digital prescriptions and online retailers capturing incremental share. Rising labor costs and shrink elevated operating expenses. CVS’s legacy footprint of about 9,900 U.S. stores limits agility to shutter low-performing locations.

Integration and execution complexity

Multiple acquired assets, notably Aetna (deal ~$69 billion) and Signify Health (approximate $8 billion), require ongoing harmonization of systems and culture across CVS’s roughly 300,000 employees. The complex operating model elevates risk of service lapses and cost overruns that could erode margins. IT modernization and interoperability demand significant capital, and execution missteps can dilute projected synergies and ROI.

Debt load from acquisitions

CVS carries elevated leverage from major acquisitions, with net leverage around 3.5x on a trailing-12-month basis in 2024 versus lower ratios at pure-play peers; total debt remained high into 2024. Higher interest expense—roughly $3.2 billion in 2024—limits capital allocation and buyback capacity. Deleveraging could stretch further in a weak macro or reimbursement downturn, and credit ratings (S&P BBB, Moody’s Baa2) keep financing costs sensitive to shocks.

Regulatory scrutiny and litigation exposure

Regulatory scrutiny around PBM practices, rebate structures and prior opioid-related matters creates significant legal and settlement exposure; PBMs now manage over 80% of US prescription claims, drawing intense oversight, and nationwide opioid litigation has produced tens of billions in settlements that raise precedent risk for CVS.

- PBM/rebates: heightened investigation risk

- Opioid legacy: exposure to large settlements

- Compliance: rising, resource-intensive demands

- Pricing transparency: threatens existing margins

- Adverse rulings: potential earnings and reputational hit

Perception and customer experience challenges

Consumer sentiment toward PBMs and retail pharmacies is mixed; CVS faces perception risk despite Caremark covering over 100 million lives and nearly 10,000 stores. Store wait times, staffing shortages and service variability drive dissatisfaction and fuel churn to competitors, while brand complexity blurs propositions across segments and negative press can accelerate defections.

- Perception: mixed on PBMs

- Scale: >100M lives, ~10,000 stores

- Operations: wait times & staffing

- Reputation: negative press → higher churn

DIR fee volatility and reimbursement compression plus integration risk squeeze margins

Reimbursement compression and DIR fee volatility have squeezed pharmacy margins despite scale. E‑commerce and digital scripts erode front‑store traffic while rising labor and shrink inflate costs. Complex post‑Aetna/Signify integration across ~300,000 employees and ~9,900 stores raises execution and IT modernization risk. Elevated leverage (net leverage ~3.5x TTM 2024) and ~$3.2B 2024 interest expense limit capital flexibility.

| Metric | Value |

|---|---|

| U.S. stores | ~9,900 |

| Employees | ~300,000 |

| Caremark lives | >100M |

| Net leverage (TTM 2024) | ~3.5x |

| Interest expense (2024) | ~$3.2B |

Full Version Awaits

CVS Health SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the final CVS Health SWOT report you'll get. Purchase unlocks the full, editable version ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

CVS Health’s SWOT reveals how scale, vertical integration, and digital investments counter regulatory pressure, reimbursement shifts, and retail competition. Explore actionable strengths, weaknesses, opportunities, and threats tailored for investors and strategists. Discover the full picture with our complete SWOT analysis—purchase now for the editable report and Excel matrix.

Strengths

Vertically integrated care model

CVS Health combines Caremark PBM (serving over 100 million members), Aetna insurance (~22 million members), ~9,900 retail pharmacies and 1,100+ MinuteClinics to control costs and outcomes. Integration enables data sharing, coordinated care and steerage to in‑network services, creating member and sponsor stickiness. This vertical model supports value‑based care and medical cost containment through aligned incentives and utilization management.

Massive scale and distribution

CVS operates ~9,900 retail pharmacies and 1,100+ MinuteClinic/HealthHUB sites nationwide, supporting 2024 revenue of about $322 billion. This scale delivers strong purchasing leverage with manufacturers and wholesalers, lowering cost of goods. Broad, convenient footprint boosts medication adherence and customer retention. It enables rapid rollout of new care models and services across markets.

Strong PBM capabilities

Caremark's robust formulary management, rebates aggregation and specialty pharmacy expertise support optimized plan design and utilization management across tens of millions of members. Advanced analytics drive utilization edits and plan design optimization, while high mail-order and specialty penetration materially boosts margins. CVS reports measurable drug trend control for employers and payers, with billions in negotiated rebates and specialty savings annually.

Diversified revenue streams

CVS Health's diversified revenue mix — spanning pharmacy services, health benefits and retail — produced over $300 billion in revenue in 2024, giving balanced exposure across payors and channels. This mix reduces reliance on any single reimbursement source and creates material cross-selling between PBM, insurance and retail care. Strong operating cash flow has supported multi‑billion dollar investment and deleveraging initiatives.

- Revenue > $300B (2024)

- Balanced exposure: PBM, benefits, retail

- Enables cross-selling across segments

- Cash flow funds investment and debt paydown

Data and clinical assets

CVS Health combines multi-year medical and pharmacy claims from Aetna and its retail network, supporting longitudinal analytics across millions of members and encounters.

Integrated clinical programs for chronic care, medication adherence, and specialty care coordination enable personalized interventions at point of fill and care sites across 9,900+ pharmacies and ~1,100 clinics.

These assets power risk scoring, fraud/waste/abuse detection and outcomes measurement to improve quality and lower cost.

- Claims: multi-year, member-level

- Sites: 9,900+ pharmacies; ~1,100 clinics

- Uses: risk scoring, FWA detection, outcomes

Integrated PBM, payer, retail & clinic network; $322B revenue

CVS Health integrates Caremark PBM (100M+ members), Aetna (~22M members), ~9,900 pharmacies and ~1,100 clinics to drive coordinated, value‑based care and cost control. 2024 revenue ~ $322B with strong operating cash flow funding investment and deleveraging. Robust formulary, specialty pharmacy and analytics deliver rebates, utilization management and margin expansion.

| Metric | 2024 |

|---|---|

| Revenue | $322B |

| PBM members | 100M+ |

| Aetna members | 22M |

| Retail sites | 9,900 |

| Clinics | 1,100+ |

What is included in the product

Delivers a strategic overview of CVS Health’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position across retail pharmacy, health services, and pharmacy benefit management.

Provides a concise CVS Health SWOT matrix for fast, visual strategy alignment, highlighting pharmacy, PBM, retail strengths and material risks. Editable spreadsheet format allows easy updates to reflect regulatory shifts, M&A activity, and changing consumer trends for quick stakeholder review.

Weaknesses

Margin pressure in retail pharmacy

Reimbursement compression and unpredictable DIR fee dynamics have compressed pharmacy margins, reducing pharmacy gross margin contribution despite scale. Front-store traffic faces growing e-commerce competition, with digital prescriptions and online retailers capturing incremental share. Rising labor costs and shrink elevated operating expenses. CVS’s legacy footprint of about 9,900 U.S. stores limits agility to shutter low-performing locations.

Integration and execution complexity

Multiple acquired assets, notably Aetna (deal ~$69 billion) and Signify Health (approximate $8 billion), require ongoing harmonization of systems and culture across CVS’s roughly 300,000 employees. The complex operating model elevates risk of service lapses and cost overruns that could erode margins. IT modernization and interoperability demand significant capital, and execution missteps can dilute projected synergies and ROI.

Debt load from acquisitions

CVS carries elevated leverage from major acquisitions, with net leverage around 3.5x on a trailing-12-month basis in 2024 versus lower ratios at pure-play peers; total debt remained high into 2024. Higher interest expense—roughly $3.2 billion in 2024—limits capital allocation and buyback capacity. Deleveraging could stretch further in a weak macro or reimbursement downturn, and credit ratings (S&P BBB, Moody’s Baa2) keep financing costs sensitive to shocks.

Regulatory scrutiny and litigation exposure

Regulatory scrutiny around PBM practices, rebate structures and prior opioid-related matters creates significant legal and settlement exposure; PBMs now manage over 80% of US prescription claims, drawing intense oversight, and nationwide opioid litigation has produced tens of billions in settlements that raise precedent risk for CVS.

- PBM/rebates: heightened investigation risk

- Opioid legacy: exposure to large settlements

- Compliance: rising, resource-intensive demands

- Pricing transparency: threatens existing margins

- Adverse rulings: potential earnings and reputational hit

Perception and customer experience challenges

Consumer sentiment toward PBMs and retail pharmacies is mixed; CVS faces perception risk despite Caremark covering over 100 million lives and nearly 10,000 stores. Store wait times, staffing shortages and service variability drive dissatisfaction and fuel churn to competitors, while brand complexity blurs propositions across segments and negative press can accelerate defections.

- Perception: mixed on PBMs

- Scale: >100M lives, ~10,000 stores

- Operations: wait times & staffing

- Reputation: negative press → higher churn

DIR fee volatility and reimbursement compression plus integration risk squeeze margins

Reimbursement compression and DIR fee volatility have squeezed pharmacy margins despite scale. E‑commerce and digital scripts erode front‑store traffic while rising labor and shrink inflate costs. Complex post‑Aetna/Signify integration across ~300,000 employees and ~9,900 stores raises execution and IT modernization risk. Elevated leverage (net leverage ~3.5x TTM 2024) and ~$3.2B 2024 interest expense limit capital flexibility.

| Metric | Value |

|---|---|

| U.S. stores | ~9,900 |

| Employees | ~300,000 |

| Caremark lives | >100M |

| Net leverage (TTM 2024) | ~3.5x |

| Interest expense (2024) | ~$3.2B |

Full Version Awaits

CVS Health SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the final CVS Health SWOT report you'll get. Purchase unlocks the full, editable version ready for use.