CVS Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, social changes, and technological advances are reshaping CVS Group’s strategic outlook in our concise PESTLE summary. This snapshot highlights key risks and opportunities to inform investment and planning decisions. For the full, actionable breakdown with legal and environmental deep dives, download the complete PESTLE analysis now.

Political factors

Veterinary workforce policy

Post-Brexit mobility constraints since free movement ended in 2021 have reduced straightforward recruitment from the EU, increasing CVSs reliance on Skilled Worker visas and complicating hiring of vets and nurses.

Immigration rules and the Home Office shortage occupation designations materially affect supply; any relaxation or tightening will directly shift staffing costs and clinic capacity.

CVS must therefore engage in policy dialogue and diversify pipelines through UK graduate training, international hires and retention measures to stabilise staffing.

Animal health priorities

Government agendas on animal welfare, biosecurity and public health drive clinical protocols and client demand, especially as an estimated 60% of human pathogens are zoonotic and 75% of emerging infections originate from animals (WHO).

National vaccination campaigns and enhanced disease surveillance historically raise preventive service volumes and clinic throughput.

Targeted funding or incentives for rural and farm animal care shift service mix; CVS benefits by aligning offerings with these national welfare strategies.

Devolution and local funding

Devolution means UK home nations and local authorities (UK pop c.67m; Ireland 5.1m; Netherlands 17.8m) set divergent public‑health directives and practice standards, altering out‑of‑hours provision and emergency cover expectations. Variations increase compliance burdens and locality-specific staffing costs. Targeted grants or business‑rates reliefs (exceeding £10bn UK‑wide in 2023/24) can sustain clinics in underserved areas. CVS requires continuous localized policy monitoring across the UK, Ireland and the Netherlands.

Trade and supply chains

Customs frictions between the UK and EU continue to affect medicines, diagnostic kits and consumables, increasing paperwork and border risk for CVS Group. Political instability in supplier regions lengthens delivery times and raises freight and insurance costs. Changes to mutual recognition of veterinary medicines can sharply disrupt availability, while CVS mitigates risk via multi-sourcing and EU-based procurement hubs.

- Customs frictions: higher documentation and border risk

- Supplier stability: impacts lead times and costs

- Mutual recognition: regulatory changes threaten supply

- Mitigation: multi-sourcing and EU procurement hubs

Market scrutiny

- Regulatory risk: competition remedies possible

- Transparency: public sector demands

- Action: evidence-led engagement and compliance upgrades

Post-Brexit vet staff squeeze raises costs; zoonotic risk boosts preventive demand

Post-Brexit immigration limits and Skilled Worker visa reliance (UK net migration 504,000 in 2023) tighten veterinary labour supply, raising wages and agency costs. Government animal‑health campaigns and zoonotic risk (WHO: ~60% pathogens zoonotic) increase preventive demand. Customs friction and veterinary‑medicine recognition changes raise procurement costs and inventory risk for CVS Group.

| Factor | 2024/25 metric | Implication |

|---|---|---|

| Immigration | UK net migration 504,000 (2023) | Staff shortages, higher payroll |

| Zoonoses | ~60% pathogens zoonotic (WHO) | ↑ Preventive services |

| Trade | Post‑Brexit customs friction | Procurement delays/costs |

What is included in the product

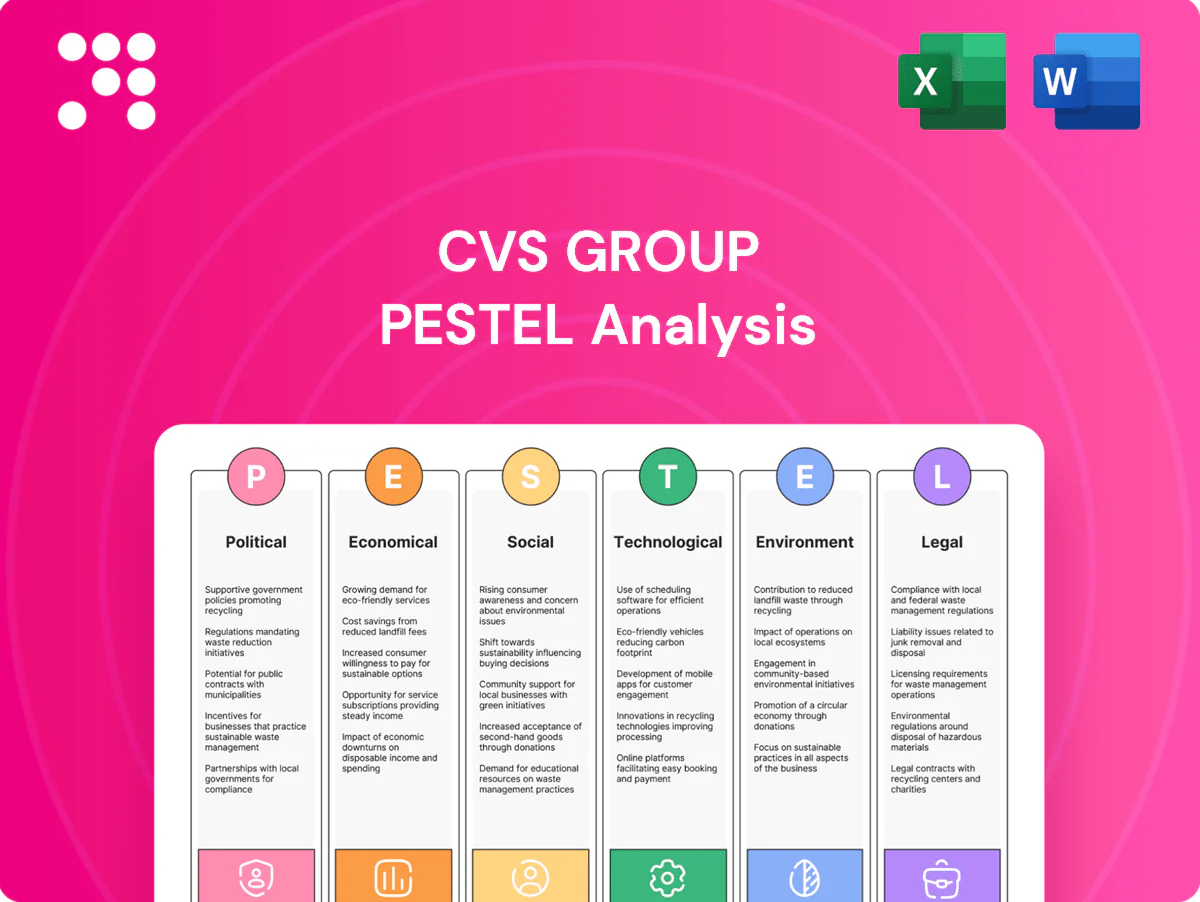

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the CVS Group, providing data-backed trends, sector-specific subpoints and forward-looking insights to inform strategy, risk mitigation and investor-ready materials.

A concise PESTLE summary of CVS Group that’s visually segmented for quick meeting reference, easily editable for regional or business-line notes and drop-in ready for presentations—ideal for aligning teams and supporting external risk and market-positioning discussions.

Economic factors

Consumer spending on pets

Pet humanization underpins resilient demand—US pet spending reached 136.8 billion in 2023 (APPA), but remains income‑sensitive as inflation elevated living costs (US CPI 2023: 3.4%). Inflation and higher energy bills can defer elective procedures while essentials hold. Low pet insurance penetration (around 3% in the US) moderates out‑of‑pocket volatility. CVS can optimize tiered offerings and wellness plans to capture price‑sensitive segments.

Wage and talent inflation

Scarcity of vets—RCVS 2024 reported c.20% of practices had clinical vacancies—fuels pay inflation and signing bonuses, while rising locum day rates materially squeeze margins and complicate rota planning. Investment in retention and training can offset turnover costs; CVS can leverage scale to standardize productivity, centralize benefits and negotiate locum supply to mitigate wage pressure.

Interest rates and M&A

Higher interest rates (effective federal funds target 5.25–5.50% in mid‑2025) raise acquisition and capex financing costs, pressuring deal economics and favoring organic investment. Valuation multiples for physician practices are under compression, shifting some buy‑vs‑build decisions toward selective internal growth. CVS’s strong cash flow supports targeted consolidation, but the company must prioritize high‑ROIC projects and disciplined integration.

FX exposure

Operations across the UK, Ireland and the Netherlands create material GBP/EUR exposure: currency swings directly affect reported revenues, input costs and lab kits priced in euros. Hedging policies using forwards/options can stabilize cash flows; with GBP trading around EUR1.17 in July 2025, a 5% move meaningfully shifts euro-denominated costs. Pricing and sourcing strategies must align with currency trends to protect margins.

- GBP≈EUR1.17 (Jul 2025)

- Euro-priced lab kits = FX-sensitive cost

- Hedging can smooth cash flow volatility

- Align pricing/sourcing to currency moves

Insurance dynamics

Changes in pet insurer policies in 2024 tightened prior‑authorization and claim checks, affecting treatment approvals and extending billing cycles; higher claim scrutiny has delayed revenue recognition for UK vets by several weeks. Co‑pay shifts toward higher client contribution have reduced elective diagnostics but maintained emergency surgery volumes. CVS benefits from insurer partnerships and streamlined prior‑auth workflows implemented in 2024.

- 2024 UK pet insurance GWP ~£1.1bn

- Prior‑auth delays extended billing by weeks

- Co‑pay rises dampen diagnostics

- Insurer partnerships accelerate approvals

Post-Brexit vet staff squeeze raises costs; zoonotic risk boosts preventive demand

Pet humanization sustains demand (US pet spend 136.8bn 2023) but remains income‑sensitive (US CPI 2023: 3.4%); pet insurance low (~3% US) limits payor cushioning. Vet shortages (RCVS 2024: ~20% practices with vacancies) and higher rates (Fed funds 5.25–5.50% mid‑2025) raise wage and financing costs. GBP≈EUR1.17 (Jul 2025) and UK pet insurance GWP ~£1.1bn 2024 affect margins and cash flow.

| Metric | Value |

|---|---|

| US pet spend 2023 | $136.8bn |

| US CPI 2023 | 3.4% |

| Vet vacancies (RCVS 2024) | ~20% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| GBP≈EUR (Jul 2025) | 1.17 |

| UK pet insurance GWP 2024 | £1.1bn |

Same Document Delivered

CVS Group PESTLE Analysis

This CVS Group PESTLE Analysis delivers concise political, economic, social, technological, legal and environmental insights tailored for strategic decision‑making. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the file is ready to download and implement immediately.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, social changes, and technological advances are reshaping CVS Group’s strategic outlook in our concise PESTLE summary. This snapshot highlights key risks and opportunities to inform investment and planning decisions. For the full, actionable breakdown with legal and environmental deep dives, download the complete PESTLE analysis now.

Political factors

Veterinary workforce policy

Post-Brexit mobility constraints since free movement ended in 2021 have reduced straightforward recruitment from the EU, increasing CVSs reliance on Skilled Worker visas and complicating hiring of vets and nurses.

Immigration rules and the Home Office shortage occupation designations materially affect supply; any relaxation or tightening will directly shift staffing costs and clinic capacity.

CVS must therefore engage in policy dialogue and diversify pipelines through UK graduate training, international hires and retention measures to stabilise staffing.

Animal health priorities

Government agendas on animal welfare, biosecurity and public health drive clinical protocols and client demand, especially as an estimated 60% of human pathogens are zoonotic and 75% of emerging infections originate from animals (WHO).

National vaccination campaigns and enhanced disease surveillance historically raise preventive service volumes and clinic throughput.

Targeted funding or incentives for rural and farm animal care shift service mix; CVS benefits by aligning offerings with these national welfare strategies.

Devolution and local funding

Devolution means UK home nations and local authorities (UK pop c.67m; Ireland 5.1m; Netherlands 17.8m) set divergent public‑health directives and practice standards, altering out‑of‑hours provision and emergency cover expectations. Variations increase compliance burdens and locality-specific staffing costs. Targeted grants or business‑rates reliefs (exceeding £10bn UK‑wide in 2023/24) can sustain clinics in underserved areas. CVS requires continuous localized policy monitoring across the UK, Ireland and the Netherlands.

Trade and supply chains

Customs frictions between the UK and EU continue to affect medicines, diagnostic kits and consumables, increasing paperwork and border risk for CVS Group. Political instability in supplier regions lengthens delivery times and raises freight and insurance costs. Changes to mutual recognition of veterinary medicines can sharply disrupt availability, while CVS mitigates risk via multi-sourcing and EU-based procurement hubs.

- Customs frictions: higher documentation and border risk

- Supplier stability: impacts lead times and costs

- Mutual recognition: regulatory changes threaten supply

- Mitigation: multi-sourcing and EU procurement hubs

Market scrutiny

- Regulatory risk: competition remedies possible

- Transparency: public sector demands

- Action: evidence-led engagement and compliance upgrades

Post-Brexit vet staff squeeze raises costs; zoonotic risk boosts preventive demand

Post-Brexit immigration limits and Skilled Worker visa reliance (UK net migration 504,000 in 2023) tighten veterinary labour supply, raising wages and agency costs. Government animal‑health campaigns and zoonotic risk (WHO: ~60% pathogens zoonotic) increase preventive demand. Customs friction and veterinary‑medicine recognition changes raise procurement costs and inventory risk for CVS Group.

| Factor | 2024/25 metric | Implication |

|---|---|---|

| Immigration | UK net migration 504,000 (2023) | Staff shortages, higher payroll |

| Zoonoses | ~60% pathogens zoonotic (WHO) | ↑ Preventive services |

| Trade | Post‑Brexit customs friction | Procurement delays/costs |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the CVS Group, providing data-backed trends, sector-specific subpoints and forward-looking insights to inform strategy, risk mitigation and investor-ready materials.

A concise PESTLE summary of CVS Group that’s visually segmented for quick meeting reference, easily editable for regional or business-line notes and drop-in ready for presentations—ideal for aligning teams and supporting external risk and market-positioning discussions.

Economic factors

Consumer spending on pets

Pet humanization underpins resilient demand—US pet spending reached 136.8 billion in 2023 (APPA), but remains income‑sensitive as inflation elevated living costs (US CPI 2023: 3.4%). Inflation and higher energy bills can defer elective procedures while essentials hold. Low pet insurance penetration (around 3% in the US) moderates out‑of‑pocket volatility. CVS can optimize tiered offerings and wellness plans to capture price‑sensitive segments.

Wage and talent inflation

Scarcity of vets—RCVS 2024 reported c.20% of practices had clinical vacancies—fuels pay inflation and signing bonuses, while rising locum day rates materially squeeze margins and complicate rota planning. Investment in retention and training can offset turnover costs; CVS can leverage scale to standardize productivity, centralize benefits and negotiate locum supply to mitigate wage pressure.

Interest rates and M&A

Higher interest rates (effective federal funds target 5.25–5.50% in mid‑2025) raise acquisition and capex financing costs, pressuring deal economics and favoring organic investment. Valuation multiples for physician practices are under compression, shifting some buy‑vs‑build decisions toward selective internal growth. CVS’s strong cash flow supports targeted consolidation, but the company must prioritize high‑ROIC projects and disciplined integration.

FX exposure

Operations across the UK, Ireland and the Netherlands create material GBP/EUR exposure: currency swings directly affect reported revenues, input costs and lab kits priced in euros. Hedging policies using forwards/options can stabilize cash flows; with GBP trading around EUR1.17 in July 2025, a 5% move meaningfully shifts euro-denominated costs. Pricing and sourcing strategies must align with currency trends to protect margins.

- GBP≈EUR1.17 (Jul 2025)

- Euro-priced lab kits = FX-sensitive cost

- Hedging can smooth cash flow volatility

- Align pricing/sourcing to currency moves

Insurance dynamics

Changes in pet insurer policies in 2024 tightened prior‑authorization and claim checks, affecting treatment approvals and extending billing cycles; higher claim scrutiny has delayed revenue recognition for UK vets by several weeks. Co‑pay shifts toward higher client contribution have reduced elective diagnostics but maintained emergency surgery volumes. CVS benefits from insurer partnerships and streamlined prior‑auth workflows implemented in 2024.

- 2024 UK pet insurance GWP ~£1.1bn

- Prior‑auth delays extended billing by weeks

- Co‑pay rises dampen diagnostics

- Insurer partnerships accelerate approvals

Post-Brexit vet staff squeeze raises costs; zoonotic risk boosts preventive demand

Pet humanization sustains demand (US pet spend 136.8bn 2023) but remains income‑sensitive (US CPI 2023: 3.4%); pet insurance low (~3% US) limits payor cushioning. Vet shortages (RCVS 2024: ~20% practices with vacancies) and higher rates (Fed funds 5.25–5.50% mid‑2025) raise wage and financing costs. GBP≈EUR1.17 (Jul 2025) and UK pet insurance GWP ~£1.1bn 2024 affect margins and cash flow.

| Metric | Value |

|---|---|

| US pet spend 2023 | $136.8bn |

| US CPI 2023 | 3.4% |

| Vet vacancies (RCVS 2024) | ~20% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| GBP≈EUR (Jul 2025) | 1.17 |

| UK pet insurance GWP 2024 | £1.1bn |

Same Document Delivered

CVS Group PESTLE Analysis

This CVS Group PESTLE Analysis delivers concise political, economic, social, technological, legal and environmental insights tailored for strategic decision‑making. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the file is ready to download and implement immediately.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, social changes, and technological advances are reshaping CVS Group’s strategic outlook in our concise PESTLE summary. This snapshot highlights key risks and opportunities to inform investment and planning decisions. For the full, actionable breakdown with legal and environmental deep dives, download the complete PESTLE analysis now.

Political factors

Veterinary workforce policy

Post-Brexit mobility constraints since free movement ended in 2021 have reduced straightforward recruitment from the EU, increasing CVSs reliance on Skilled Worker visas and complicating hiring of vets and nurses.

Immigration rules and the Home Office shortage occupation designations materially affect supply; any relaxation or tightening will directly shift staffing costs and clinic capacity.

CVS must therefore engage in policy dialogue and diversify pipelines through UK graduate training, international hires and retention measures to stabilise staffing.

Animal health priorities

Government agendas on animal welfare, biosecurity and public health drive clinical protocols and client demand, especially as an estimated 60% of human pathogens are zoonotic and 75% of emerging infections originate from animals (WHO).

National vaccination campaigns and enhanced disease surveillance historically raise preventive service volumes and clinic throughput.

Targeted funding or incentives for rural and farm animal care shift service mix; CVS benefits by aligning offerings with these national welfare strategies.

Devolution and local funding

Devolution means UK home nations and local authorities (UK pop c.67m; Ireland 5.1m; Netherlands 17.8m) set divergent public‑health directives and practice standards, altering out‑of‑hours provision and emergency cover expectations. Variations increase compliance burdens and locality-specific staffing costs. Targeted grants or business‑rates reliefs (exceeding £10bn UK‑wide in 2023/24) can sustain clinics in underserved areas. CVS requires continuous localized policy monitoring across the UK, Ireland and the Netherlands.

Trade and supply chains

Customs frictions between the UK and EU continue to affect medicines, diagnostic kits and consumables, increasing paperwork and border risk for CVS Group. Political instability in supplier regions lengthens delivery times and raises freight and insurance costs. Changes to mutual recognition of veterinary medicines can sharply disrupt availability, while CVS mitigates risk via multi-sourcing and EU-based procurement hubs.

- Customs frictions: higher documentation and border risk

- Supplier stability: impacts lead times and costs

- Mutual recognition: regulatory changes threaten supply

- Mitigation: multi-sourcing and EU procurement hubs

Market scrutiny

- Regulatory risk: competition remedies possible

- Transparency: public sector demands

- Action: evidence-led engagement and compliance upgrades

Post-Brexit vet staff squeeze raises costs; zoonotic risk boosts preventive demand

Post-Brexit immigration limits and Skilled Worker visa reliance (UK net migration 504,000 in 2023) tighten veterinary labour supply, raising wages and agency costs. Government animal‑health campaigns and zoonotic risk (WHO: ~60% pathogens zoonotic) increase preventive demand. Customs friction and veterinary‑medicine recognition changes raise procurement costs and inventory risk for CVS Group.

| Factor | 2024/25 metric | Implication |

|---|---|---|

| Immigration | UK net migration 504,000 (2023) | Staff shortages, higher payroll |

| Zoonoses | ~60% pathogens zoonotic (WHO) | ↑ Preventive services |

| Trade | Post‑Brexit customs friction | Procurement delays/costs |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the CVS Group, providing data-backed trends, sector-specific subpoints and forward-looking insights to inform strategy, risk mitigation and investor-ready materials.

A concise PESTLE summary of CVS Group that’s visually segmented for quick meeting reference, easily editable for regional or business-line notes and drop-in ready for presentations—ideal for aligning teams and supporting external risk and market-positioning discussions.

Economic factors

Consumer spending on pets

Pet humanization underpins resilient demand—US pet spending reached 136.8 billion in 2023 (APPA), but remains income‑sensitive as inflation elevated living costs (US CPI 2023: 3.4%). Inflation and higher energy bills can defer elective procedures while essentials hold. Low pet insurance penetration (around 3% in the US) moderates out‑of‑pocket volatility. CVS can optimize tiered offerings and wellness plans to capture price‑sensitive segments.

Wage and talent inflation

Scarcity of vets—RCVS 2024 reported c.20% of practices had clinical vacancies—fuels pay inflation and signing bonuses, while rising locum day rates materially squeeze margins and complicate rota planning. Investment in retention and training can offset turnover costs; CVS can leverage scale to standardize productivity, centralize benefits and negotiate locum supply to mitigate wage pressure.

Interest rates and M&A

Higher interest rates (effective federal funds target 5.25–5.50% in mid‑2025) raise acquisition and capex financing costs, pressuring deal economics and favoring organic investment. Valuation multiples for physician practices are under compression, shifting some buy‑vs‑build decisions toward selective internal growth. CVS’s strong cash flow supports targeted consolidation, but the company must prioritize high‑ROIC projects and disciplined integration.

FX exposure

Operations across the UK, Ireland and the Netherlands create material GBP/EUR exposure: currency swings directly affect reported revenues, input costs and lab kits priced in euros. Hedging policies using forwards/options can stabilize cash flows; with GBP trading around EUR1.17 in July 2025, a 5% move meaningfully shifts euro-denominated costs. Pricing and sourcing strategies must align with currency trends to protect margins.

- GBP≈EUR1.17 (Jul 2025)

- Euro-priced lab kits = FX-sensitive cost

- Hedging can smooth cash flow volatility

- Align pricing/sourcing to currency moves

Insurance dynamics

Changes in pet insurer policies in 2024 tightened prior‑authorization and claim checks, affecting treatment approvals and extending billing cycles; higher claim scrutiny has delayed revenue recognition for UK vets by several weeks. Co‑pay shifts toward higher client contribution have reduced elective diagnostics but maintained emergency surgery volumes. CVS benefits from insurer partnerships and streamlined prior‑auth workflows implemented in 2024.

- 2024 UK pet insurance GWP ~£1.1bn

- Prior‑auth delays extended billing by weeks

- Co‑pay rises dampen diagnostics

- Insurer partnerships accelerate approvals

Post-Brexit vet staff squeeze raises costs; zoonotic risk boosts preventive demand

Pet humanization sustains demand (US pet spend 136.8bn 2023) but remains income‑sensitive (US CPI 2023: 3.4%); pet insurance low (~3% US) limits payor cushioning. Vet shortages (RCVS 2024: ~20% practices with vacancies) and higher rates (Fed funds 5.25–5.50% mid‑2025) raise wage and financing costs. GBP≈EUR1.17 (Jul 2025) and UK pet insurance GWP ~£1.1bn 2024 affect margins and cash flow.

| Metric | Value |

|---|---|

| US pet spend 2023 | $136.8bn |

| US CPI 2023 | 3.4% |

| Vet vacancies (RCVS 2024) | ~20% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| GBP≈EUR (Jul 2025) | 1.17 |

| UK pet insurance GWP 2024 | £1.1bn |

Same Document Delivered

CVS Group PESTLE Analysis

This CVS Group PESTLE Analysis delivers concise political, economic, social, technological, legal and environmental insights tailored for strategic decision‑making. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the file is ready to download and implement immediately.