Xiamen Tungsten Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

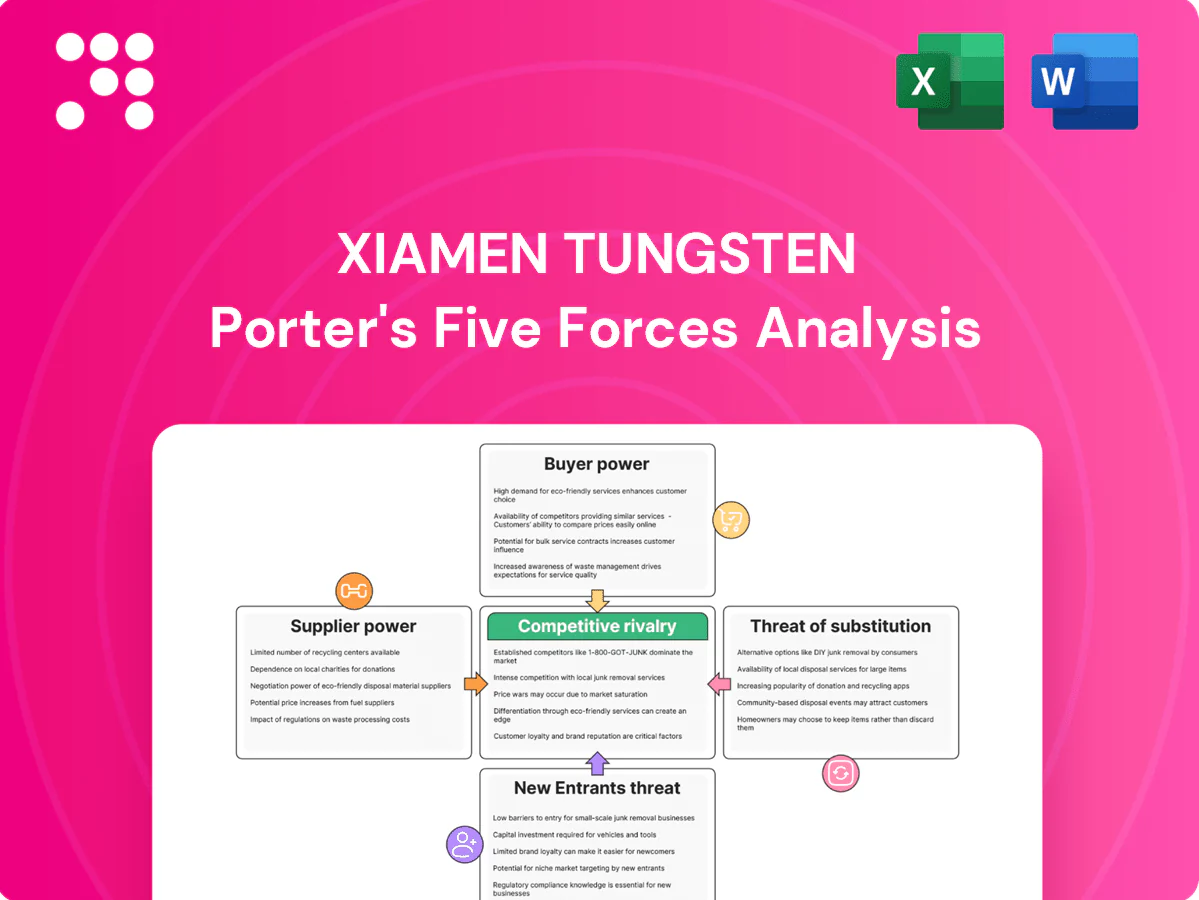

Xiamen Tungsten faces a resource‑intensive market with strong supplier influence, cyclical demand and concentrated buyers that compress margins and raise competitive intensity. Substitute materials and vertical integration create moderate disruption risks, while regulatory and capex barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xiamen Tungsten’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce tungsten ore resources

Primary feedstock is geologically scarce and concentrated: China accounted for roughly 85% of global tungsten mine production in 2023 (USGS 2024), with Vietnam and a few ROW mines supplying most of the remainder. Chinese quotas, licensing and geopolitical events can sharply tighten export flows, elevating upstream leverage and enabling swift input-price pass-through. Xiamen’s own mining operations reduce exposure but do not remove the systemic scarcity and country-concentration risk.

Dependence on third-party concentrates and scrap

Supplemental feed from independent miners and recyclers remains material for Xiamen Tungsten, with recycling supplying about 20% of global tungsten in 2024 (ITIA). Scrap flows are cyclical and highly price-sensitive, so availability swings with market rates. When spot tightens, merchant traders capture outsized bargaining power and can push margins. Diversified sourcing and advances in recycling tech partially offset merchant leverage.

Energy, reagents, and environmental inputs

Smelting and powder processing are energy- and chemical-intensive, with energy and reagent inputs reported to account for roughly 25–35% of processing costs in tungsten refining (2024 industry estimates). Power price volatility and tighter 2024 compliance costs for emissions and wastewater have strengthened utility and reagent suppliers' leverage. Long-term power and reagent contracts plus local supplier clustering in Fujian temper short-term price spikes. Continuous process efficiency gains are reducing exposure to input-cost swings over time.

Rare earth and battery precursors

Upstream rare earth concentrates and battery precursors exhibit high supplier concentration, with China controlling >70% of refined rare earth processing capacity and the top five precursor producers supplying over 60% of global NCM/NCA precursors in 2024; policy controls and potential export restrictions therefore elevate supplier power. Vertical integration by Xiamen Tungsten and domestic supplier networks reduce exposure, while broader qualification of suppliers expands optionality.

- Concentration: >70% refined processing in China

- Top-5 control: >60% precursor supply

- Mitigation: vertical integration + domestic networks

- Optionality: broadened supplier qualification

Equipment and technology licensors

- OEM concentration: specialized suppliers dominate

- Switching cost: high due to calibration/IP

- Supplier levers: upgrade & service revenue

- Xiamen strengths: multi-sourcing + in-house engineering

China controls ~85% of tungsten mines; recycling ~20% reduces supplier risk

High supplier concentration (China ~85% tungsten mine share, USGS 2024) and upstream policy risk give suppliers strong leverage; recycling (~20% of supply, ITIA 2024) and Xiamen’s vertical integration partially mitigate. Energy/reagent costs (~25–35% of refining costs, 2024) and specialized OEMs (cemented carbide market ~$5.8bn 2024) sustain supplier power; long-term contracts and in-house engineering reduce exposure.

| Metric | Value |

|---|---|

| China mine share | ~85% (2023) |

| Recycling | ~20% (2024) |

| Energy/reagent cost | 25–35% (2024) |

| OEM market | $5.8bn (2024) |

| Rare earth processing | >70% China (2024) |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitute threats, and rivalry specifically for Xiamen Tungsten, with strategic implications for pricing and profitability.

Clear, one-sheet Porter's Five Forces for Xiamen Tungsten—instantly spot supply, buyer and substitute pressures to guide sourcing and pricing decisions. Swap in live data or duplicate scenarios to model post-regulation shifts or new entrants without coding.

Customers Bargaining Power

Industrial OEMs and toolmakers

Industrial OEMs and toolmakers (cutting tools, wear parts, aerospace, electronics) are concentrated and sophisticated in 2024, driving hard negotiations on volume, quality and delivery terms. Multi-year supply agreements in 2024 have reduced spot-price volatility but sustain strong competitive pricing pressure. Qualification is sticky, yet dual-sourcing remains common, limiting Xiamen Tungsten’s unilateral pricing power.

Price sensitivity and cyclicality

End-market cyclicality (industrial and automotive demand) raises buyer price sensitivity during downturns, increasing pressure on Xiamen Tungsten to cut prices. Tungsten indexation — tied to CRU/MB tungsten oxide benchmarks — exposes margins to pass-through timing, with index swings (~±15% in 2024 YTD) widening gaps between spot and contract prices. Buyers demand surcharges and rebates; Xiamen offsets via higher-margin product mix and hedging (reported ~30% coverage in 2024).

High specifications and quality assurance

Tight specs on grain size (commonly 0.5–3 µm) and purity (>99.9%) raise switching costs for buyers, as requalification can take months and add 10–20% higher initial scrap risk. High failure risk reduces willingness to change vendors quickly, reinforcing incumbent leverage. Approved-vendor status grants pricing and contract power, while continuous QA (inline testing, ISO/TS certifications) sustains premium positioning.

Backward integration risk

Some large toolmakers and hardmetal firms have internal powder capabilities that can cap supplier pricing, but few can scale upstream into mining and smelting; China supplies over 80% of global tungsten raw materials (2024), reinforcing scale barriers. Xiamen Tungsten’s integrated chain from concentrate to finished products materially offsets buyer backward-integration threats.

- Buyer powder capability: limited to downstream processing

- Upstream scale barrier: mining/smelting capital intensive

- Xiamen advantage: vertical integration reduces displacement risk

Demand from EV and electronics

- Rapid buyer scale: global EVs ≈14M (2024)

- Volume = visibility, preferred pricing

- Qualification 12–24 months limits quick switches

- Value-added offerings reduce pure price focus

EV OEM contracts, ±15% tungsten swings and China 80% supply sustain margin squeeze

Large, sophisticated OEMs (EVs ≈14M 2024) exert strong price/contract pressure; multi-year deals reduce spot volatility but sustain margin squeeze. Index-linked tungsten swings (~±15% YTD 2024) and ~30% hedging coverage affect pass-through timing. Qualification (12–24 months) and tight specs (≥99.9% purity) raise switching costs; Xiamen’s vertical integration (China ≈80% raw supply 2024) limits displacement risk.

| Metric | 2024 value |

|---|---|

| China share of raw supply | ≈80% |

| Global EV sales | ≈14M |

| Tungsten index swing | ±15% YTD |

| Hedging coverage | ~30% |

| Qualification cycle | 12–24 months |

What You See Is What You Get

Xiamen Tungsten Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Xiamen Tungsten you'll receive immediately after purchase—no surprises, no placeholders. The document provides a complete, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. It's ready for instant download and use.

A Must-Have Tool for Decision-Makers

Xiamen Tungsten faces a resource‑intensive market with strong supplier influence, cyclical demand and concentrated buyers that compress margins and raise competitive intensity. Substitute materials and vertical integration create moderate disruption risks, while regulatory and capex barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xiamen Tungsten’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce tungsten ore resources

Primary feedstock is geologically scarce and concentrated: China accounted for roughly 85% of global tungsten mine production in 2023 (USGS 2024), with Vietnam and a few ROW mines supplying most of the remainder. Chinese quotas, licensing and geopolitical events can sharply tighten export flows, elevating upstream leverage and enabling swift input-price pass-through. Xiamen’s own mining operations reduce exposure but do not remove the systemic scarcity and country-concentration risk.

Dependence on third-party concentrates and scrap

Supplemental feed from independent miners and recyclers remains material for Xiamen Tungsten, with recycling supplying about 20% of global tungsten in 2024 (ITIA). Scrap flows are cyclical and highly price-sensitive, so availability swings with market rates. When spot tightens, merchant traders capture outsized bargaining power and can push margins. Diversified sourcing and advances in recycling tech partially offset merchant leverage.

Energy, reagents, and environmental inputs

Smelting and powder processing are energy- and chemical-intensive, with energy and reagent inputs reported to account for roughly 25–35% of processing costs in tungsten refining (2024 industry estimates). Power price volatility and tighter 2024 compliance costs for emissions and wastewater have strengthened utility and reagent suppliers' leverage. Long-term power and reagent contracts plus local supplier clustering in Fujian temper short-term price spikes. Continuous process efficiency gains are reducing exposure to input-cost swings over time.

Rare earth and battery precursors

Upstream rare earth concentrates and battery precursors exhibit high supplier concentration, with China controlling >70% of refined rare earth processing capacity and the top five precursor producers supplying over 60% of global NCM/NCA precursors in 2024; policy controls and potential export restrictions therefore elevate supplier power. Vertical integration by Xiamen Tungsten and domestic supplier networks reduce exposure, while broader qualification of suppliers expands optionality.

- Concentration: >70% refined processing in China

- Top-5 control: >60% precursor supply

- Mitigation: vertical integration + domestic networks

- Optionality: broadened supplier qualification

Equipment and technology licensors

- OEM concentration: specialized suppliers dominate

- Switching cost: high due to calibration/IP

- Supplier levers: upgrade & service revenue

- Xiamen strengths: multi-sourcing + in-house engineering

China controls ~85% of tungsten mines; recycling ~20% reduces supplier risk

High supplier concentration (China ~85% tungsten mine share, USGS 2024) and upstream policy risk give suppliers strong leverage; recycling (~20% of supply, ITIA 2024) and Xiamen’s vertical integration partially mitigate. Energy/reagent costs (~25–35% of refining costs, 2024) and specialized OEMs (cemented carbide market ~$5.8bn 2024) sustain supplier power; long-term contracts and in-house engineering reduce exposure.

| Metric | Value |

|---|---|

| China mine share | ~85% (2023) |

| Recycling | ~20% (2024) |

| Energy/reagent cost | 25–35% (2024) |

| OEM market | $5.8bn (2024) |

| Rare earth processing | >70% China (2024) |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitute threats, and rivalry specifically for Xiamen Tungsten, with strategic implications for pricing and profitability.

Clear, one-sheet Porter's Five Forces for Xiamen Tungsten—instantly spot supply, buyer and substitute pressures to guide sourcing and pricing decisions. Swap in live data or duplicate scenarios to model post-regulation shifts or new entrants without coding.

Customers Bargaining Power

Industrial OEMs and toolmakers

Industrial OEMs and toolmakers (cutting tools, wear parts, aerospace, electronics) are concentrated and sophisticated in 2024, driving hard negotiations on volume, quality and delivery terms. Multi-year supply agreements in 2024 have reduced spot-price volatility but sustain strong competitive pricing pressure. Qualification is sticky, yet dual-sourcing remains common, limiting Xiamen Tungsten’s unilateral pricing power.

Price sensitivity and cyclicality

End-market cyclicality (industrial and automotive demand) raises buyer price sensitivity during downturns, increasing pressure on Xiamen Tungsten to cut prices. Tungsten indexation — tied to CRU/MB tungsten oxide benchmarks — exposes margins to pass-through timing, with index swings (~±15% in 2024 YTD) widening gaps between spot and contract prices. Buyers demand surcharges and rebates; Xiamen offsets via higher-margin product mix and hedging (reported ~30% coverage in 2024).

High specifications and quality assurance

Tight specs on grain size (commonly 0.5–3 µm) and purity (>99.9%) raise switching costs for buyers, as requalification can take months and add 10–20% higher initial scrap risk. High failure risk reduces willingness to change vendors quickly, reinforcing incumbent leverage. Approved-vendor status grants pricing and contract power, while continuous QA (inline testing, ISO/TS certifications) sustains premium positioning.

Backward integration risk

Some large toolmakers and hardmetal firms have internal powder capabilities that can cap supplier pricing, but few can scale upstream into mining and smelting; China supplies over 80% of global tungsten raw materials (2024), reinforcing scale barriers. Xiamen Tungsten’s integrated chain from concentrate to finished products materially offsets buyer backward-integration threats.

- Buyer powder capability: limited to downstream processing

- Upstream scale barrier: mining/smelting capital intensive

- Xiamen advantage: vertical integration reduces displacement risk

Demand from EV and electronics

- Rapid buyer scale: global EVs ≈14M (2024)

- Volume = visibility, preferred pricing

- Qualification 12–24 months limits quick switches

- Value-added offerings reduce pure price focus

EV OEM contracts, ±15% tungsten swings and China 80% supply sustain margin squeeze

Large, sophisticated OEMs (EVs ≈14M 2024) exert strong price/contract pressure; multi-year deals reduce spot volatility but sustain margin squeeze. Index-linked tungsten swings (~±15% YTD 2024) and ~30% hedging coverage affect pass-through timing. Qualification (12–24 months) and tight specs (≥99.9% purity) raise switching costs; Xiamen’s vertical integration (China ≈80% raw supply 2024) limits displacement risk.

| Metric | 2024 value |

|---|---|

| China share of raw supply | ≈80% |

| Global EV sales | ≈14M |

| Tungsten index swing | ±15% YTD |

| Hedging coverage | ~30% |

| Qualification cycle | 12–24 months |

What You See Is What You Get

Xiamen Tungsten Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Xiamen Tungsten you'll receive immediately after purchase—no surprises, no placeholders. The document provides a complete, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. It's ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Xiamen Tungsten faces a resource‑intensive market with strong supplier influence, cyclical demand and concentrated buyers that compress margins and raise competitive intensity. Substitute materials and vertical integration create moderate disruption risks, while regulatory and capex barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xiamen Tungsten’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce tungsten ore resources

Primary feedstock is geologically scarce and concentrated: China accounted for roughly 85% of global tungsten mine production in 2023 (USGS 2024), with Vietnam and a few ROW mines supplying most of the remainder. Chinese quotas, licensing and geopolitical events can sharply tighten export flows, elevating upstream leverage and enabling swift input-price pass-through. Xiamen’s own mining operations reduce exposure but do not remove the systemic scarcity and country-concentration risk.

Dependence on third-party concentrates and scrap

Supplemental feed from independent miners and recyclers remains material for Xiamen Tungsten, with recycling supplying about 20% of global tungsten in 2024 (ITIA). Scrap flows are cyclical and highly price-sensitive, so availability swings with market rates. When spot tightens, merchant traders capture outsized bargaining power and can push margins. Diversified sourcing and advances in recycling tech partially offset merchant leverage.

Energy, reagents, and environmental inputs

Smelting and powder processing are energy- and chemical-intensive, with energy and reagent inputs reported to account for roughly 25–35% of processing costs in tungsten refining (2024 industry estimates). Power price volatility and tighter 2024 compliance costs for emissions and wastewater have strengthened utility and reagent suppliers' leverage. Long-term power and reagent contracts plus local supplier clustering in Fujian temper short-term price spikes. Continuous process efficiency gains are reducing exposure to input-cost swings over time.

Rare earth and battery precursors

Upstream rare earth concentrates and battery precursors exhibit high supplier concentration, with China controlling >70% of refined rare earth processing capacity and the top five precursor producers supplying over 60% of global NCM/NCA precursors in 2024; policy controls and potential export restrictions therefore elevate supplier power. Vertical integration by Xiamen Tungsten and domestic supplier networks reduce exposure, while broader qualification of suppliers expands optionality.

- Concentration: >70% refined processing in China

- Top-5 control: >60% precursor supply

- Mitigation: vertical integration + domestic networks

- Optionality: broadened supplier qualification

Equipment and technology licensors

- OEM concentration: specialized suppliers dominate

- Switching cost: high due to calibration/IP

- Supplier levers: upgrade & service revenue

- Xiamen strengths: multi-sourcing + in-house engineering

China controls ~85% of tungsten mines; recycling ~20% reduces supplier risk

High supplier concentration (China ~85% tungsten mine share, USGS 2024) and upstream policy risk give suppliers strong leverage; recycling (~20% of supply, ITIA 2024) and Xiamen’s vertical integration partially mitigate. Energy/reagent costs (~25–35% of refining costs, 2024) and specialized OEMs (cemented carbide market ~$5.8bn 2024) sustain supplier power; long-term contracts and in-house engineering reduce exposure.

| Metric | Value |

|---|---|

| China mine share | ~85% (2023) |

| Recycling | ~20% (2024) |

| Energy/reagent cost | 25–35% (2024) |

| OEM market | $5.8bn (2024) |

| Rare earth processing | >70% China (2024) |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitute threats, and rivalry specifically for Xiamen Tungsten, with strategic implications for pricing and profitability.

Clear, one-sheet Porter's Five Forces for Xiamen Tungsten—instantly spot supply, buyer and substitute pressures to guide sourcing and pricing decisions. Swap in live data or duplicate scenarios to model post-regulation shifts or new entrants without coding.

Customers Bargaining Power

Industrial OEMs and toolmakers

Industrial OEMs and toolmakers (cutting tools, wear parts, aerospace, electronics) are concentrated and sophisticated in 2024, driving hard negotiations on volume, quality and delivery terms. Multi-year supply agreements in 2024 have reduced spot-price volatility but sustain strong competitive pricing pressure. Qualification is sticky, yet dual-sourcing remains common, limiting Xiamen Tungsten’s unilateral pricing power.

Price sensitivity and cyclicality

End-market cyclicality (industrial and automotive demand) raises buyer price sensitivity during downturns, increasing pressure on Xiamen Tungsten to cut prices. Tungsten indexation — tied to CRU/MB tungsten oxide benchmarks — exposes margins to pass-through timing, with index swings (~±15% in 2024 YTD) widening gaps between spot and contract prices. Buyers demand surcharges and rebates; Xiamen offsets via higher-margin product mix and hedging (reported ~30% coverage in 2024).

High specifications and quality assurance

Tight specs on grain size (commonly 0.5–3 µm) and purity (>99.9%) raise switching costs for buyers, as requalification can take months and add 10–20% higher initial scrap risk. High failure risk reduces willingness to change vendors quickly, reinforcing incumbent leverage. Approved-vendor status grants pricing and contract power, while continuous QA (inline testing, ISO/TS certifications) sustains premium positioning.

Backward integration risk

Some large toolmakers and hardmetal firms have internal powder capabilities that can cap supplier pricing, but few can scale upstream into mining and smelting; China supplies over 80% of global tungsten raw materials (2024), reinforcing scale barriers. Xiamen Tungsten’s integrated chain from concentrate to finished products materially offsets buyer backward-integration threats.

- Buyer powder capability: limited to downstream processing

- Upstream scale barrier: mining/smelting capital intensive

- Xiamen advantage: vertical integration reduces displacement risk

Demand from EV and electronics

- Rapid buyer scale: global EVs ≈14M (2024)

- Volume = visibility, preferred pricing

- Qualification 12–24 months limits quick switches

- Value-added offerings reduce pure price focus

EV OEM contracts, ±15% tungsten swings and China 80% supply sustain margin squeeze

Large, sophisticated OEMs (EVs ≈14M 2024) exert strong price/contract pressure; multi-year deals reduce spot volatility but sustain margin squeeze. Index-linked tungsten swings (~±15% YTD 2024) and ~30% hedging coverage affect pass-through timing. Qualification (12–24 months) and tight specs (≥99.9% purity) raise switching costs; Xiamen’s vertical integration (China ≈80% raw supply 2024) limits displacement risk.

| Metric | 2024 value |

|---|---|

| China share of raw supply | ≈80% |

| Global EV sales | ≈14M |

| Tungsten index swing | ±15% YTD |

| Hedging coverage | ~30% |

| Qualification cycle | 12–24 months |

What You See Is What You Get

Xiamen Tungsten Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Xiamen Tungsten you'll receive immediately after purchase—no surprises, no placeholders. The document provides a complete, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. It's ready for instant download and use.