Da Cin Construction Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

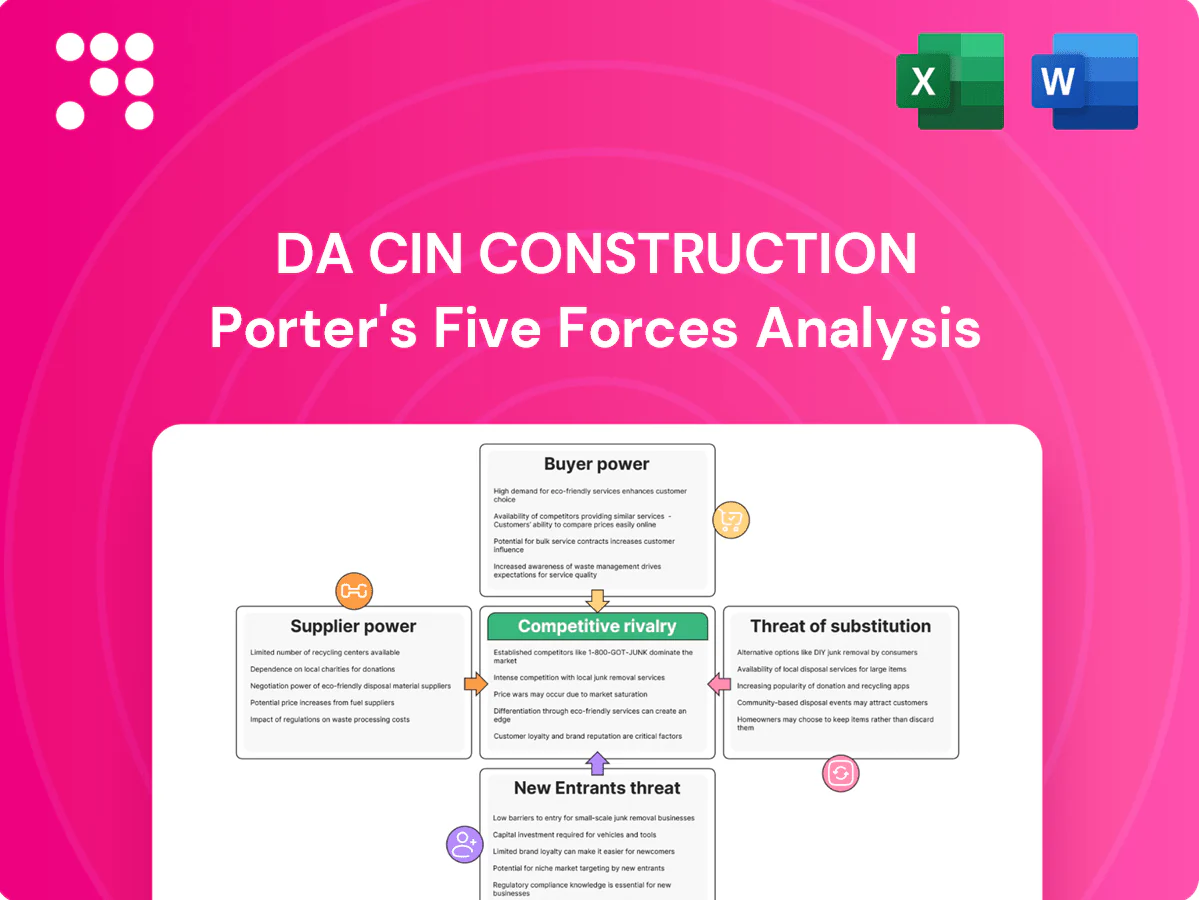

Da Cin Construction faces moderate buyer power, concentrated supplier relationships, and rising competitive intensity from regional builders, while regulatory and technological shifts shape barrier levels. This snapshot highlights key pressure points and strategic levers for management. Unlock the full Porter’s Five Forces analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement, asphalt and rebar in 2024 are sourced from a limited set of regional producers, giving key suppliers meaningful pricing leverage over Da Cin. The company’s broad project mix raises exposure to commodity swings across its civil and building backlog. Long-term contracts and bulk purchasing have tempered short-term spikes. Vendor diversification and hedging programs help preserve bid margins.

Specialized subcontractors

Specialized subcontractors for MEP, façade, tunneling and high-rise trades are capacity-constrained in Taiwan; during 2024 demand peaks these subs often select projects and can push rates and terms, with observed rate premiums of 10–15% on high-complexity jobs. Prequalification pools and framework agreements cut scheduling delays and bid churn materially. Early engagement reduces rework and claims, lowering change-order incidence.

Equipment and rental dependencies

Da Cin relies heavily on rental markets for heavy machinery, cranes and formwork; the global equipment rental market was valued at about $141 billion in 2024, concentrating supply and driving spot-rate spikes of 10–20% that inflate costs and delay critical paths. Owning select bottleneck assets reduces exposure but ties up capital and increases fixed costs. Rigorous preventive maintenance and multi-vendor sourcing cut downtime risk and stabilize schedules.

Standards and green materials

In 2024 rising ESG and green-building specs have narrowed Da Cin Construction’s approved supplier lists, boosting bargaining power for certified low-carbon material providers. Qualified low-carbon materials command premiums, squeezing margins unless early spec alignment and approved alternates are secured. Supplier development programs in 2024 expanded compliant options, reducing single-supplier dependency over time.

- 2024: narrowed approved lists

- Premiums for low-carbon materials

- Early spec alignment protects budgets

- Supplier development expands options

Logistics and import exposure

Imported components expose Da Cin to FX volatility (typical 5–10% swings in 2023–24), shipping rate and customs risks that can add days to costs and weeks to lead times; port congestion or geopolitical shocks have caused disruptions of multiple weeks in recent years. Localization and 8–12 week buffer stock profiles reduce schedule slippage, and contracts should allocate freight, duty and delay penalties to suppliers.

- FX exposure: 5–10% moves (2023–24)

- Shipping/customs: weeks of potential delay

- Mitigation: localization + 8–12 week buffers

- Governance: contract clauses to share logistics risk

Supplier squeeze: $141B rentals; 5-12% low-carbon; 10-15% subcontractor

Supplier power is high in 2024 due to concentrated steel/cement producers and certified low‑carbon material premiums (5–12%), specialized subcontractor rate premiums of 10–15%, and equipment rental market pressures (global market ~$141B) that drive spot spikes. FX swings of 5–10% and shipping delays (weeks) further transfer cost risk to Da Cin; long contracts, hedging and selective asset ownership mitigate exposure.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Materials concentration | 5–12% premiums | Higher input costs |

| Subcontractors | 10–15% premiums | Margin pressure |

| Equipment rental | $141B market | Spot rate spikes 10–20% |

| FX/shipping | 5–10% moves; weeks delay | Schedule/cost risk |

What is included in the product

Tailored exclusively for Da Cin Construction, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and emerging threats, providing strategic insight into pricing power, profitability risks, and defensive opportunities for investors and management.

A concise, one-sheet Porter's Five Forces for Da Cin Construction that quantifies competitive pressures and highlights actionable levers to reduce margin squeeze and bidding risk.

Customers Bargaining Power

Government tender dominance

Government tenders, which OECD estimates account for about 12% of GDP, use transparent competitive bidding and strict specifications that intensify price pressure and compress differentiation. Consequently, past performance and safety records become decisive tie-breakers, while documented on-time delivery measurably improves future tender evaluation scores.

Large developers’ leverage

Large commercial and residential developers bundle projects to extract volume discounts, negotiate extended payment terms and liquidated damages, and shift risk to contractors; in 2024 design-build accounted for roughly 50% of US nonresidential delivery, increasing developer influence in scope-setting. Demonstrating lifecycle value via faster delivery and higher quality softens price pressure and preserves margin.

Bid comparability and transparency

Standardized BOQs and BIM-based tenders make bids directly comparable, and in 2024 award decisions often hinge on small cost gaps of 1-3% in competitive markets. Clear value‑engineering options present non-price advantages that can win contracts even when bids are near-equal. Robust documentation from BIM reduces claims and preserves client relationships, lowering post-award disputes and warranty costs.

Change order and schedule pressure

Clients increasingly demand accelerated timelines and fixed-price risk transfer; tight LDs, commonly 0.1–0.5% of contract value per day, shift delay risk onto contractors. Robust project controls and CPM scheduling protect margins, while early clash detection via BIM can cut downstream change costs by ~30–40%.

- Clients: accelerated schedules, fixed-price pressure

- LDs: 0.1–0.5%/day transfers delay risk

- Defenses: CPM controls, BIM clash detection (~30–40% cost reduction)

Reputation and repeat business

Buyers weigh reliability, safety, and dispute history heavily; 2024 industry surveys show safety incidents reduce future contract awards by ~35%, making reputation critical for Da Cin Construction. Repeat awards lower acquisition costs (around 25% savings) but raise performance expectations and margin pressure. Proactive stakeholder management and strong post-handover performance materially boost negotiating leverage for follow-on work.

- Reputation: safety + dispute record drive awards

- Repeat business: ~25% lower acquisition cost

- Stakeholder mgmt: increases trust and bid success

- Post-handover: key to future negotiations

Transparent tenders (≈12% GDP), design‑build scale (≈50%), BIM saves 30–40%

Buyers use transparent tenders (≈12% of GDP in 2024) and strict specs that amplify price pressure; past performance and safety are decisive tie-breakers.

Large developers bundle work (design‑build ≈50% of US nonresidential 2024), squeezing margins via volume discounts and extended terms.

BOQs/BIM make bids comparable; award gaps often 1–3% and BIM cuts downstream change costs ~30–40%.

LDs (0.1–0.5%/day) and reputation (safety incidents cut future awards ≈35%) shift risk to contractors.

| Metric | 2024 |

|---|---|

| Govt tenders | ≈12% GDP |

| Design‑build share | ≈50% |

| Award cost gap | 1–3% |

| BIM savings | 30–40% |

| LDs | 0.1–0.5%/day |

| Safety impact | −35% awards |

Preview the Actual Deliverable

Da Cin Construction Porter's Five Forces Analysis

This preview shows the exact Da Cin Construction Porter’s Five Forces Analysis you'll receive—no mockups or placeholders. The full, professionally formatted document is ready for immediate download upon purchase. Use it as-is for strategy, valuation, or competitive assessment.

Go Beyond the Preview—Access the Full Strategic Report

Da Cin Construction faces moderate buyer power, concentrated supplier relationships, and rising competitive intensity from regional builders, while regulatory and technological shifts shape barrier levels. This snapshot highlights key pressure points and strategic levers for management. Unlock the full Porter’s Five Forces analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement, asphalt and rebar in 2024 are sourced from a limited set of regional producers, giving key suppliers meaningful pricing leverage over Da Cin. The company’s broad project mix raises exposure to commodity swings across its civil and building backlog. Long-term contracts and bulk purchasing have tempered short-term spikes. Vendor diversification and hedging programs help preserve bid margins.

Specialized subcontractors

Specialized subcontractors for MEP, façade, tunneling and high-rise trades are capacity-constrained in Taiwan; during 2024 demand peaks these subs often select projects and can push rates and terms, with observed rate premiums of 10–15% on high-complexity jobs. Prequalification pools and framework agreements cut scheduling delays and bid churn materially. Early engagement reduces rework and claims, lowering change-order incidence.

Equipment and rental dependencies

Da Cin relies heavily on rental markets for heavy machinery, cranes and formwork; the global equipment rental market was valued at about $141 billion in 2024, concentrating supply and driving spot-rate spikes of 10–20% that inflate costs and delay critical paths. Owning select bottleneck assets reduces exposure but ties up capital and increases fixed costs. Rigorous preventive maintenance and multi-vendor sourcing cut downtime risk and stabilize schedules.

Standards and green materials

In 2024 rising ESG and green-building specs have narrowed Da Cin Construction’s approved supplier lists, boosting bargaining power for certified low-carbon material providers. Qualified low-carbon materials command premiums, squeezing margins unless early spec alignment and approved alternates are secured. Supplier development programs in 2024 expanded compliant options, reducing single-supplier dependency over time.

- 2024: narrowed approved lists

- Premiums for low-carbon materials

- Early spec alignment protects budgets

- Supplier development expands options

Logistics and import exposure

Imported components expose Da Cin to FX volatility (typical 5–10% swings in 2023–24), shipping rate and customs risks that can add days to costs and weeks to lead times; port congestion or geopolitical shocks have caused disruptions of multiple weeks in recent years. Localization and 8–12 week buffer stock profiles reduce schedule slippage, and contracts should allocate freight, duty and delay penalties to suppliers.

- FX exposure: 5–10% moves (2023–24)

- Shipping/customs: weeks of potential delay

- Mitigation: localization + 8–12 week buffers

- Governance: contract clauses to share logistics risk

Supplier squeeze: $141B rentals; 5-12% low-carbon; 10-15% subcontractor

Supplier power is high in 2024 due to concentrated steel/cement producers and certified low‑carbon material premiums (5–12%), specialized subcontractor rate premiums of 10–15%, and equipment rental market pressures (global market ~$141B) that drive spot spikes. FX swings of 5–10% and shipping delays (weeks) further transfer cost risk to Da Cin; long contracts, hedging and selective asset ownership mitigate exposure.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Materials concentration | 5–12% premiums | Higher input costs |

| Subcontractors | 10–15% premiums | Margin pressure |

| Equipment rental | $141B market | Spot rate spikes 10–20% |

| FX/shipping | 5–10% moves; weeks delay | Schedule/cost risk |

What is included in the product

Tailored exclusively for Da Cin Construction, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and emerging threats, providing strategic insight into pricing power, profitability risks, and defensive opportunities for investors and management.

A concise, one-sheet Porter's Five Forces for Da Cin Construction that quantifies competitive pressures and highlights actionable levers to reduce margin squeeze and bidding risk.

Customers Bargaining Power

Government tender dominance

Government tenders, which OECD estimates account for about 12% of GDP, use transparent competitive bidding and strict specifications that intensify price pressure and compress differentiation. Consequently, past performance and safety records become decisive tie-breakers, while documented on-time delivery measurably improves future tender evaluation scores.

Large developers’ leverage

Large commercial and residential developers bundle projects to extract volume discounts, negotiate extended payment terms and liquidated damages, and shift risk to contractors; in 2024 design-build accounted for roughly 50% of US nonresidential delivery, increasing developer influence in scope-setting. Demonstrating lifecycle value via faster delivery and higher quality softens price pressure and preserves margin.

Bid comparability and transparency

Standardized BOQs and BIM-based tenders make bids directly comparable, and in 2024 award decisions often hinge on small cost gaps of 1-3% in competitive markets. Clear value‑engineering options present non-price advantages that can win contracts even when bids are near-equal. Robust documentation from BIM reduces claims and preserves client relationships, lowering post-award disputes and warranty costs.

Change order and schedule pressure

Clients increasingly demand accelerated timelines and fixed-price risk transfer; tight LDs, commonly 0.1–0.5% of contract value per day, shift delay risk onto contractors. Robust project controls and CPM scheduling protect margins, while early clash detection via BIM can cut downstream change costs by ~30–40%.

- Clients: accelerated schedules, fixed-price pressure

- LDs: 0.1–0.5%/day transfers delay risk

- Defenses: CPM controls, BIM clash detection (~30–40% cost reduction)

Reputation and repeat business

Buyers weigh reliability, safety, and dispute history heavily; 2024 industry surveys show safety incidents reduce future contract awards by ~35%, making reputation critical for Da Cin Construction. Repeat awards lower acquisition costs (around 25% savings) but raise performance expectations and margin pressure. Proactive stakeholder management and strong post-handover performance materially boost negotiating leverage for follow-on work.

- Reputation: safety + dispute record drive awards

- Repeat business: ~25% lower acquisition cost

- Stakeholder mgmt: increases trust and bid success

- Post-handover: key to future negotiations

Transparent tenders (≈12% GDP), design‑build scale (≈50%), BIM saves 30–40%

Buyers use transparent tenders (≈12% of GDP in 2024) and strict specs that amplify price pressure; past performance and safety are decisive tie-breakers.

Large developers bundle work (design‑build ≈50% of US nonresidential 2024), squeezing margins via volume discounts and extended terms.

BOQs/BIM make bids comparable; award gaps often 1–3% and BIM cuts downstream change costs ~30–40%.

LDs (0.1–0.5%/day) and reputation (safety incidents cut future awards ≈35%) shift risk to contractors.

| Metric | 2024 |

|---|---|

| Govt tenders | ≈12% GDP |

| Design‑build share | ≈50% |

| Award cost gap | 1–3% |

| BIM savings | 30–40% |

| LDs | 0.1–0.5%/day |

| Safety impact | −35% awards |

Preview the Actual Deliverable

Da Cin Construction Porter's Five Forces Analysis

This preview shows the exact Da Cin Construction Porter’s Five Forces Analysis you'll receive—no mockups or placeholders. The full, professionally formatted document is ready for immediate download upon purchase. Use it as-is for strategy, valuation, or competitive assessment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Da Cin Construction faces moderate buyer power, concentrated supplier relationships, and rising competitive intensity from regional builders, while regulatory and technological shifts shape barrier levels. This snapshot highlights key pressure points and strategic levers for management. Unlock the full Porter’s Five Forces analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement, asphalt and rebar in 2024 are sourced from a limited set of regional producers, giving key suppliers meaningful pricing leverage over Da Cin. The company’s broad project mix raises exposure to commodity swings across its civil and building backlog. Long-term contracts and bulk purchasing have tempered short-term spikes. Vendor diversification and hedging programs help preserve bid margins.

Specialized subcontractors

Specialized subcontractors for MEP, façade, tunneling and high-rise trades are capacity-constrained in Taiwan; during 2024 demand peaks these subs often select projects and can push rates and terms, with observed rate premiums of 10–15% on high-complexity jobs. Prequalification pools and framework agreements cut scheduling delays and bid churn materially. Early engagement reduces rework and claims, lowering change-order incidence.

Equipment and rental dependencies

Da Cin relies heavily on rental markets for heavy machinery, cranes and formwork; the global equipment rental market was valued at about $141 billion in 2024, concentrating supply and driving spot-rate spikes of 10–20% that inflate costs and delay critical paths. Owning select bottleneck assets reduces exposure but ties up capital and increases fixed costs. Rigorous preventive maintenance and multi-vendor sourcing cut downtime risk and stabilize schedules.

Standards and green materials

In 2024 rising ESG and green-building specs have narrowed Da Cin Construction’s approved supplier lists, boosting bargaining power for certified low-carbon material providers. Qualified low-carbon materials command premiums, squeezing margins unless early spec alignment and approved alternates are secured. Supplier development programs in 2024 expanded compliant options, reducing single-supplier dependency over time.

- 2024: narrowed approved lists

- Premiums for low-carbon materials

- Early spec alignment protects budgets

- Supplier development expands options

Logistics and import exposure

Imported components expose Da Cin to FX volatility (typical 5–10% swings in 2023–24), shipping rate and customs risks that can add days to costs and weeks to lead times; port congestion or geopolitical shocks have caused disruptions of multiple weeks in recent years. Localization and 8–12 week buffer stock profiles reduce schedule slippage, and contracts should allocate freight, duty and delay penalties to suppliers.

- FX exposure: 5–10% moves (2023–24)

- Shipping/customs: weeks of potential delay

- Mitigation: localization + 8–12 week buffers

- Governance: contract clauses to share logistics risk

Supplier squeeze: $141B rentals; 5-12% low-carbon; 10-15% subcontractor

Supplier power is high in 2024 due to concentrated steel/cement producers and certified low‑carbon material premiums (5–12%), specialized subcontractor rate premiums of 10–15%, and equipment rental market pressures (global market ~$141B) that drive spot spikes. FX swings of 5–10% and shipping delays (weeks) further transfer cost risk to Da Cin; long contracts, hedging and selective asset ownership mitigate exposure.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Materials concentration | 5–12% premiums | Higher input costs |

| Subcontractors | 10–15% premiums | Margin pressure |

| Equipment rental | $141B market | Spot rate spikes 10–20% |

| FX/shipping | 5–10% moves; weeks delay | Schedule/cost risk |

What is included in the product

Tailored exclusively for Da Cin Construction, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and emerging threats, providing strategic insight into pricing power, profitability risks, and defensive opportunities for investors and management.

A concise, one-sheet Porter's Five Forces for Da Cin Construction that quantifies competitive pressures and highlights actionable levers to reduce margin squeeze and bidding risk.

Customers Bargaining Power

Government tender dominance

Government tenders, which OECD estimates account for about 12% of GDP, use transparent competitive bidding and strict specifications that intensify price pressure and compress differentiation. Consequently, past performance and safety records become decisive tie-breakers, while documented on-time delivery measurably improves future tender evaluation scores.

Large developers’ leverage

Large commercial and residential developers bundle projects to extract volume discounts, negotiate extended payment terms and liquidated damages, and shift risk to contractors; in 2024 design-build accounted for roughly 50% of US nonresidential delivery, increasing developer influence in scope-setting. Demonstrating lifecycle value via faster delivery and higher quality softens price pressure and preserves margin.

Bid comparability and transparency

Standardized BOQs and BIM-based tenders make bids directly comparable, and in 2024 award decisions often hinge on small cost gaps of 1-3% in competitive markets. Clear value‑engineering options present non-price advantages that can win contracts even when bids are near-equal. Robust documentation from BIM reduces claims and preserves client relationships, lowering post-award disputes and warranty costs.

Change order and schedule pressure

Clients increasingly demand accelerated timelines and fixed-price risk transfer; tight LDs, commonly 0.1–0.5% of contract value per day, shift delay risk onto contractors. Robust project controls and CPM scheduling protect margins, while early clash detection via BIM can cut downstream change costs by ~30–40%.

- Clients: accelerated schedules, fixed-price pressure

- LDs: 0.1–0.5%/day transfers delay risk

- Defenses: CPM controls, BIM clash detection (~30–40% cost reduction)

Reputation and repeat business

Buyers weigh reliability, safety, and dispute history heavily; 2024 industry surveys show safety incidents reduce future contract awards by ~35%, making reputation critical for Da Cin Construction. Repeat awards lower acquisition costs (around 25% savings) but raise performance expectations and margin pressure. Proactive stakeholder management and strong post-handover performance materially boost negotiating leverage for follow-on work.

- Reputation: safety + dispute record drive awards

- Repeat business: ~25% lower acquisition cost

- Stakeholder mgmt: increases trust and bid success

- Post-handover: key to future negotiations

Transparent tenders (≈12% GDP), design‑build scale (≈50%), BIM saves 30–40%

Buyers use transparent tenders (≈12% of GDP in 2024) and strict specs that amplify price pressure; past performance and safety are decisive tie-breakers.

Large developers bundle work (design‑build ≈50% of US nonresidential 2024), squeezing margins via volume discounts and extended terms.

BOQs/BIM make bids comparable; award gaps often 1–3% and BIM cuts downstream change costs ~30–40%.

LDs (0.1–0.5%/day) and reputation (safety incidents cut future awards ≈35%) shift risk to contractors.

| Metric | 2024 |

|---|---|

| Govt tenders | ≈12% GDP |

| Design‑build share | ≈50% |

| Award cost gap | 1–3% |

| BIM savings | 30–40% |

| LDs | 0.1–0.5%/day |

| Safety impact | −35% awards |

Preview the Actual Deliverable

Da Cin Construction Porter's Five Forces Analysis

This preview shows the exact Da Cin Construction Porter’s Five Forces Analysis you'll receive—no mockups or placeholders. The full, professionally formatted document is ready for immediate download upon purchase. Use it as-is for strategy, valuation, or competitive assessment.