Dai-ichi Life Porter's Five Forces Analysis

From Overview to Strategy Blueprint

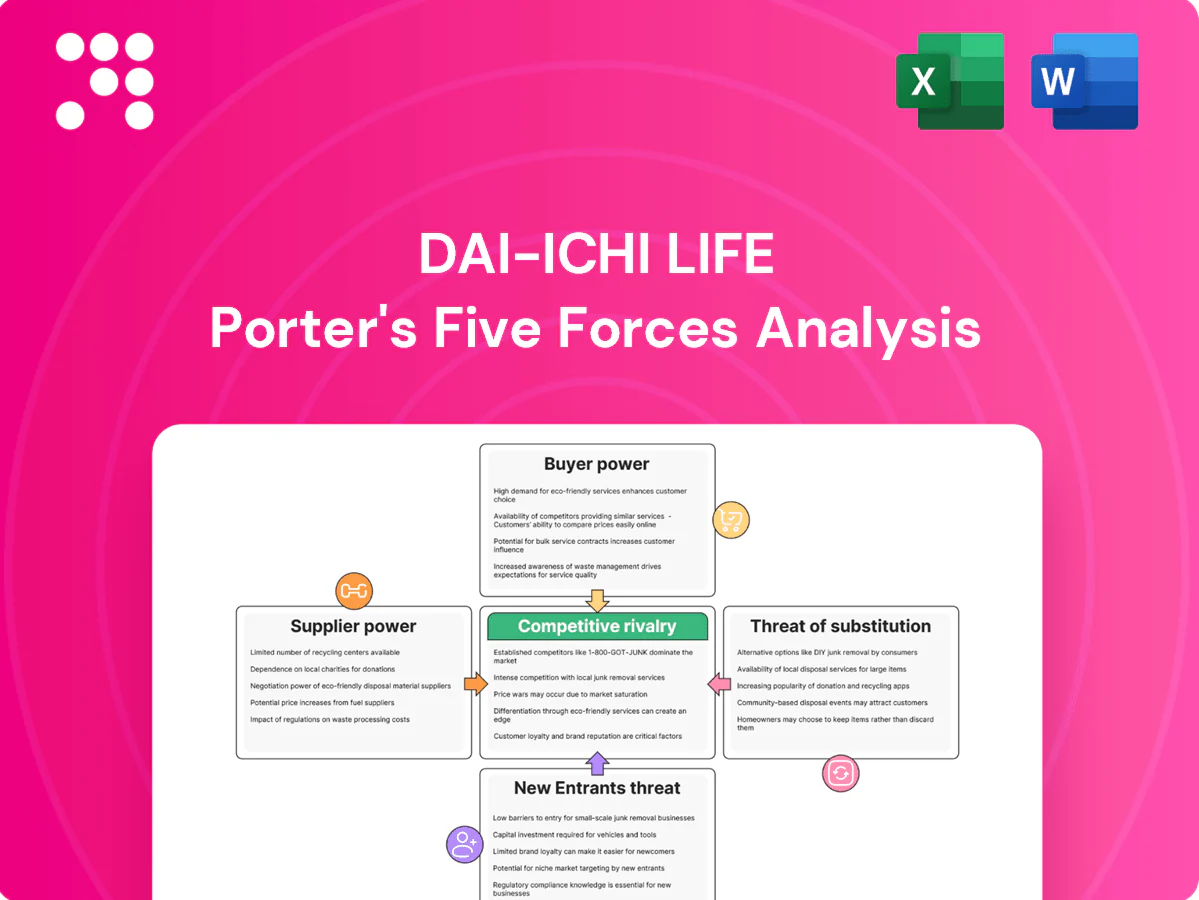

Dai-ichi Life faces moderate buyer power, regulatory-driven supplier constraints, and evolving substitute threats from insurtech and asset managers, while barriers to entry remain high due to capital and trust requirements. Competitive rivalry is intense among incumbents pursuing digital transformation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dai-ichi Life’s competitive dynamics in detail.

Suppliers Bargaining Power

Reinsurers and Capital Providers

Dai-ichi Life depends on global reinsurers and capital markets for risk transfer and solvency optimization; in 2024 tighter retrocession cycles after recent catastrophe years increased reinsurance costs and reduced optionality. Large, rated reinsurers exert moderate pricing leverage, particularly on catastrophe and longevity portfolios, but Dai-ichi’s scale, geographic diversification and long-term treaties temper that supplier power.

Technology and Data Vendors

Core policy admin, cloud, cybersecurity and analytics providers are highly concentrated (2024 cloud share: AWS ~32%, Microsoft ~23%, Google ~11%), raising switching costs and lock-in risks exacerbated by data-residency and resilience rules. Vendor lock-in and regulation increase Dai-ichi Life’s dependence, though its multi-vendor strategy and growing in-house capabilities mitigate single-vendor power. Rapid insurtech innovation — rising startup activity in 2024 — can rebalance terms through competition.

Distribution Intermediaries

Agencies, bancassurance partners and brokers can push for shelf space and higher commissions, with top bank partners in Asia often capturing roughly 25–35% of an insurer’s channel-sourced sales in 2024; large banks can secure preferential economics. Dai-ichi’s proprietary salesforce and omni-channel mix dilute intermediary leverage, while growth in digital direct channels—up ~15% y/y in online sales nationally in 2024—reduces dependence over time.

Medical Networks and Underwriting Services

Access to medical exam networks, health data, and underwriting tools is critical for Dai-ichi’s risk selection; localized networks exert bargaining power due to regulatory and privacy constraints, especially in Japan and SE Asia. Dai-ichi’s scale (over JPY 28 trillion consolidated assets in 2024) and standardized processes provide counter-leverage on pricing and SLAs. Adoption of fluidless/accelerated underwriting reached roughly 30% of new applications industry-wide by 2024, reducing reliance on external exams.

- Localized networks: regulatory/privacy-driven bargaining power

- Scale: JPY 28 trillion+ assets strengthens negotiating position

- Standardization: improves SLA/pricing leverage

- Fluidless underwriting: ~30% adoption lowers external exam dependency

Specialist Talent and Advisory

Specialist actuarial, risk and ALM expertise is scarce, giving senior consultants and quant talent strong bargaining power in Dai-ichi Life's supply chain in 2024. Wage inflation for quant and tech-adjacent roles has elevated hiring costs and retention pressures. Internal talent pipelines and increased global mobility reduce supplier concentration risk, while automation and model-governance tools partially mitigate reliance on external advisors.

- Scarcity of actuarial/ALM talent → higher consultant leverage

- Wage inflation in quant/tech roles → elevated total operating costs

- Internal pipelines + global mobility → lower supplier concentration risk

- Automation & governance tools → partial substitution of external advisors

Costs +15-25%; cloud AWS 32%

Dai-ichi faces moderate supplier power: reinsurers tightened pricing in 2024 (retrocession costs +15–25% post-cat years) but scale (JPY 28tn assets) and long treaties limit exposure.

Cloud/cyber vendors are concentrated (AWS 32%, MS 23%, GCP 11% in 2024), raising lock-in; multi-vendor + insourcing reduce risk.

Intermediaries and specialized talent hold regional leverage, though digital direct sales (+15% y/y) and automation cut dependency.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | Costs +15–25% | Moderate |

| Cloud | AWS32/MS23/GCP11 | High |

| Intermediaries | Channel share 25–35% | Moderate |

| Talent | Wage inflation ↑ | High |

What is included in the product

Tailored Porter's Five Forces analysis for Dai-ichi Life that uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive trends and market entry risks impacting its pricing, profitability and strategic positioning.

A concise one-sheet Porter's Five Forces for Dai-ichi Life—instantly highlights competitive pressures, regulatory risk and supplier/buyer dynamics to speed strategic decisions. Editable fields and a radar chart let you adjust scenarios and integrate findings straight into decks or reports.

Customers Bargaining Power

Price-Sensitive Retail Policyholders

Life and annuity buyers actively compare premiums, guarantees and projected returns across carriers, boosting buyer leverage as online aggregators and transparent illustrated disclosures widen price visibility. Switching costs are moderate due to surrender charges and tax implications, so policyholders may switch when price or guarantees diverge materially. Dai-ichi, as one of Japan’s top three life insurers, leverages brand trust and claims reputation to defend pricing.

Corporate and Group Clients

Large employers and affinity groups exert strong negotiating power over Dai-ichi Life, pressing for lower rates, enhanced features and higher service levels through competitive tenders. Tender processes heighten price competition and demand customized plan design, while Dai-ichi’s ability to bundle insurance with wellness programs and employee benefits helps mitigate discount pressure. Long-term contracts and measured service-quality metrics reduce churn and protect lifetime value.

International Customer Mix

Across Asia-Pacific and other markets buyers face diverse regulatory regimes and financial literacy levels; Asia accounted for 56% of global life insurance premiums in 2023, amplifying heterogenous demand patterns. In developing markets roughly 65% of new business remains agent-driven, so price and agent advice limit individual buyer power. In mature markets, sophisticated customers push transparency and performance, raising disclosure demands. Dai-ichi’s local subsidiaries tailor products and distribution to manage these power dynamics.

Switching and Surrender Dynamics

Policyholders weigh surrender penalties, tax impacts and underwriting requalification, so Dai-ichi faces moderate attrition pressure as customers compare net cash-on-surrender in 2024 market conditions.

Health deterioration for protection products raises switching frictions and reduces buyer power; for savings and annuities low-rate sensitivity increases focus on credited rates and fees; loyalty bonuses and riders further lock in relationships.

- Retention drivers: surrender penalties, tax treatment, underwriting

- Protection: health-linked frictions lower switching

- Savings/annuities: rate/fee sensitivity

- Design: loyalty bonuses/riders increase lock-in

Service and Digital Experience Expectations

Customers now expect seamless onboarding, claims and policy servicing; strong digital UX reduces price salience and weakens buyer leverage. Poor service raises complaints and switching intent, a risk Dai-ichi flags in its 2024 annual report. Dai-ichi’s continued omnichannel investments help contain buyer power by improving retention and speed.

- 2024 annual report: omnichannel focus

- Seamless UX lowers price sensitivity

- Poor service increases churn risk

APAC insurers face moderate buyer power; omnichannel moves ease price pressure

Buyers exert moderate bargaining power: retail policyholders compare premiums/guarantees online but face surrender/tax frictions, while large employers use tenders to demand price/custom features; Dai-ichi’s brand, loyalty riders and omnichannel service (2024 focus) mitigate pressure. Market heterogeneity across APAC alters buyer leverage by distribution channel and financial literacy.

| Metric | Value | Year/Source |

|---|---|---|

| Asia share of global premiums | 56% | 2023 |

| New business agent-driven (developing markets) | 65% | 2023 |

| Dai-ichi strategic focus | Omnichannel investments | 2024 annual report |

Preview Before You Purchase

Dai-ichi Life Porter's Five Forces Analysis

This preview shows the exact Dai‑ichi Life Porter's Five Forces analysis you'll receive after purchase—fully formatted and ready to use. No placeholders, mockups, or samples: the file available for instant download is this same document with no surprises. Complete your purchase and gain immediate access to the identical, professionally written analysis.

From Overview to Strategy Blueprint

Dai-ichi Life faces moderate buyer power, regulatory-driven supplier constraints, and evolving substitute threats from insurtech and asset managers, while barriers to entry remain high due to capital and trust requirements. Competitive rivalry is intense among incumbents pursuing digital transformation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dai-ichi Life’s competitive dynamics in detail.

Suppliers Bargaining Power

Reinsurers and Capital Providers

Dai-ichi Life depends on global reinsurers and capital markets for risk transfer and solvency optimization; in 2024 tighter retrocession cycles after recent catastrophe years increased reinsurance costs and reduced optionality. Large, rated reinsurers exert moderate pricing leverage, particularly on catastrophe and longevity portfolios, but Dai-ichi’s scale, geographic diversification and long-term treaties temper that supplier power.

Technology and Data Vendors

Core policy admin, cloud, cybersecurity and analytics providers are highly concentrated (2024 cloud share: AWS ~32%, Microsoft ~23%, Google ~11%), raising switching costs and lock-in risks exacerbated by data-residency and resilience rules. Vendor lock-in and regulation increase Dai-ichi Life’s dependence, though its multi-vendor strategy and growing in-house capabilities mitigate single-vendor power. Rapid insurtech innovation — rising startup activity in 2024 — can rebalance terms through competition.

Distribution Intermediaries

Agencies, bancassurance partners and brokers can push for shelf space and higher commissions, with top bank partners in Asia often capturing roughly 25–35% of an insurer’s channel-sourced sales in 2024; large banks can secure preferential economics. Dai-ichi’s proprietary salesforce and omni-channel mix dilute intermediary leverage, while growth in digital direct channels—up ~15% y/y in online sales nationally in 2024—reduces dependence over time.

Medical Networks and Underwriting Services

Access to medical exam networks, health data, and underwriting tools is critical for Dai-ichi’s risk selection; localized networks exert bargaining power due to regulatory and privacy constraints, especially in Japan and SE Asia. Dai-ichi’s scale (over JPY 28 trillion consolidated assets in 2024) and standardized processes provide counter-leverage on pricing and SLAs. Adoption of fluidless/accelerated underwriting reached roughly 30% of new applications industry-wide by 2024, reducing reliance on external exams.

- Localized networks: regulatory/privacy-driven bargaining power

- Scale: JPY 28 trillion+ assets strengthens negotiating position

- Standardization: improves SLA/pricing leverage

- Fluidless underwriting: ~30% adoption lowers external exam dependency

Specialist Talent and Advisory

Specialist actuarial, risk and ALM expertise is scarce, giving senior consultants and quant talent strong bargaining power in Dai-ichi Life's supply chain in 2024. Wage inflation for quant and tech-adjacent roles has elevated hiring costs and retention pressures. Internal talent pipelines and increased global mobility reduce supplier concentration risk, while automation and model-governance tools partially mitigate reliance on external advisors.

- Scarcity of actuarial/ALM talent → higher consultant leverage

- Wage inflation in quant/tech roles → elevated total operating costs

- Internal pipelines + global mobility → lower supplier concentration risk

- Automation & governance tools → partial substitution of external advisors

Costs +15-25%; cloud AWS 32%

Dai-ichi faces moderate supplier power: reinsurers tightened pricing in 2024 (retrocession costs +15–25% post-cat years) but scale (JPY 28tn assets) and long treaties limit exposure.

Cloud/cyber vendors are concentrated (AWS 32%, MS 23%, GCP 11% in 2024), raising lock-in; multi-vendor + insourcing reduce risk.

Intermediaries and specialized talent hold regional leverage, though digital direct sales (+15% y/y) and automation cut dependency.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | Costs +15–25% | Moderate |

| Cloud | AWS32/MS23/GCP11 | High |

| Intermediaries | Channel share 25–35% | Moderate |

| Talent | Wage inflation ↑ | High |

What is included in the product

Tailored Porter's Five Forces analysis for Dai-ichi Life that uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive trends and market entry risks impacting its pricing, profitability and strategic positioning.

A concise one-sheet Porter's Five Forces for Dai-ichi Life—instantly highlights competitive pressures, regulatory risk and supplier/buyer dynamics to speed strategic decisions. Editable fields and a radar chart let you adjust scenarios and integrate findings straight into decks or reports.

Customers Bargaining Power

Price-Sensitive Retail Policyholders

Life and annuity buyers actively compare premiums, guarantees and projected returns across carriers, boosting buyer leverage as online aggregators and transparent illustrated disclosures widen price visibility. Switching costs are moderate due to surrender charges and tax implications, so policyholders may switch when price or guarantees diverge materially. Dai-ichi, as one of Japan’s top three life insurers, leverages brand trust and claims reputation to defend pricing.

Corporate and Group Clients

Large employers and affinity groups exert strong negotiating power over Dai-ichi Life, pressing for lower rates, enhanced features and higher service levels through competitive tenders. Tender processes heighten price competition and demand customized plan design, while Dai-ichi’s ability to bundle insurance with wellness programs and employee benefits helps mitigate discount pressure. Long-term contracts and measured service-quality metrics reduce churn and protect lifetime value.

International Customer Mix

Across Asia-Pacific and other markets buyers face diverse regulatory regimes and financial literacy levels; Asia accounted for 56% of global life insurance premiums in 2023, amplifying heterogenous demand patterns. In developing markets roughly 65% of new business remains agent-driven, so price and agent advice limit individual buyer power. In mature markets, sophisticated customers push transparency and performance, raising disclosure demands. Dai-ichi’s local subsidiaries tailor products and distribution to manage these power dynamics.

Switching and Surrender Dynamics

Policyholders weigh surrender penalties, tax impacts and underwriting requalification, so Dai-ichi faces moderate attrition pressure as customers compare net cash-on-surrender in 2024 market conditions.

Health deterioration for protection products raises switching frictions and reduces buyer power; for savings and annuities low-rate sensitivity increases focus on credited rates and fees; loyalty bonuses and riders further lock in relationships.

- Retention drivers: surrender penalties, tax treatment, underwriting

- Protection: health-linked frictions lower switching

- Savings/annuities: rate/fee sensitivity

- Design: loyalty bonuses/riders increase lock-in

Service and Digital Experience Expectations

Customers now expect seamless onboarding, claims and policy servicing; strong digital UX reduces price salience and weakens buyer leverage. Poor service raises complaints and switching intent, a risk Dai-ichi flags in its 2024 annual report. Dai-ichi’s continued omnichannel investments help contain buyer power by improving retention and speed.

- 2024 annual report: omnichannel focus

- Seamless UX lowers price sensitivity

- Poor service increases churn risk

APAC insurers face moderate buyer power; omnichannel moves ease price pressure

Buyers exert moderate bargaining power: retail policyholders compare premiums/guarantees online but face surrender/tax frictions, while large employers use tenders to demand price/custom features; Dai-ichi’s brand, loyalty riders and omnichannel service (2024 focus) mitigate pressure. Market heterogeneity across APAC alters buyer leverage by distribution channel and financial literacy.

| Metric | Value | Year/Source |

|---|---|---|

| Asia share of global premiums | 56% | 2023 |

| New business agent-driven (developing markets) | 65% | 2023 |

| Dai-ichi strategic focus | Omnichannel investments | 2024 annual report |

Preview Before You Purchase

Dai-ichi Life Porter's Five Forces Analysis

This preview shows the exact Dai‑ichi Life Porter's Five Forces analysis you'll receive after purchase—fully formatted and ready to use. No placeholders, mockups, or samples: the file available for instant download is this same document with no surprises. Complete your purchase and gain immediate access to the identical, professionally written analysis.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Dai-ichi Life faces moderate buyer power, regulatory-driven supplier constraints, and evolving substitute threats from insurtech and asset managers, while barriers to entry remain high due to capital and trust requirements. Competitive rivalry is intense among incumbents pursuing digital transformation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dai-ichi Life’s competitive dynamics in detail.

Suppliers Bargaining Power

Reinsurers and Capital Providers

Dai-ichi Life depends on global reinsurers and capital markets for risk transfer and solvency optimization; in 2024 tighter retrocession cycles after recent catastrophe years increased reinsurance costs and reduced optionality. Large, rated reinsurers exert moderate pricing leverage, particularly on catastrophe and longevity portfolios, but Dai-ichi’s scale, geographic diversification and long-term treaties temper that supplier power.

Technology and Data Vendors

Core policy admin, cloud, cybersecurity and analytics providers are highly concentrated (2024 cloud share: AWS ~32%, Microsoft ~23%, Google ~11%), raising switching costs and lock-in risks exacerbated by data-residency and resilience rules. Vendor lock-in and regulation increase Dai-ichi Life’s dependence, though its multi-vendor strategy and growing in-house capabilities mitigate single-vendor power. Rapid insurtech innovation — rising startup activity in 2024 — can rebalance terms through competition.

Distribution Intermediaries

Agencies, bancassurance partners and brokers can push for shelf space and higher commissions, with top bank partners in Asia often capturing roughly 25–35% of an insurer’s channel-sourced sales in 2024; large banks can secure preferential economics. Dai-ichi’s proprietary salesforce and omni-channel mix dilute intermediary leverage, while growth in digital direct channels—up ~15% y/y in online sales nationally in 2024—reduces dependence over time.

Medical Networks and Underwriting Services

Access to medical exam networks, health data, and underwriting tools is critical for Dai-ichi’s risk selection; localized networks exert bargaining power due to regulatory and privacy constraints, especially in Japan and SE Asia. Dai-ichi’s scale (over JPY 28 trillion consolidated assets in 2024) and standardized processes provide counter-leverage on pricing and SLAs. Adoption of fluidless/accelerated underwriting reached roughly 30% of new applications industry-wide by 2024, reducing reliance on external exams.

- Localized networks: regulatory/privacy-driven bargaining power

- Scale: JPY 28 trillion+ assets strengthens negotiating position

- Standardization: improves SLA/pricing leverage

- Fluidless underwriting: ~30% adoption lowers external exam dependency

Specialist Talent and Advisory

Specialist actuarial, risk and ALM expertise is scarce, giving senior consultants and quant talent strong bargaining power in Dai-ichi Life's supply chain in 2024. Wage inflation for quant and tech-adjacent roles has elevated hiring costs and retention pressures. Internal talent pipelines and increased global mobility reduce supplier concentration risk, while automation and model-governance tools partially mitigate reliance on external advisors.

- Scarcity of actuarial/ALM talent → higher consultant leverage

- Wage inflation in quant/tech roles → elevated total operating costs

- Internal pipelines + global mobility → lower supplier concentration risk

- Automation & governance tools → partial substitution of external advisors

Costs +15-25%; cloud AWS 32%

Dai-ichi faces moderate supplier power: reinsurers tightened pricing in 2024 (retrocession costs +15–25% post-cat years) but scale (JPY 28tn assets) and long treaties limit exposure.

Cloud/cyber vendors are concentrated (AWS 32%, MS 23%, GCP 11% in 2024), raising lock-in; multi-vendor + insourcing reduce risk.

Intermediaries and specialized talent hold regional leverage, though digital direct sales (+15% y/y) and automation cut dependency.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | Costs +15–25% | Moderate |

| Cloud | AWS32/MS23/GCP11 | High |

| Intermediaries | Channel share 25–35% | Moderate |

| Talent | Wage inflation ↑ | High |

What is included in the product

Tailored Porter's Five Forces analysis for Dai-ichi Life that uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive trends and market entry risks impacting its pricing, profitability and strategic positioning.

A concise one-sheet Porter's Five Forces for Dai-ichi Life—instantly highlights competitive pressures, regulatory risk and supplier/buyer dynamics to speed strategic decisions. Editable fields and a radar chart let you adjust scenarios and integrate findings straight into decks or reports.

Customers Bargaining Power

Price-Sensitive Retail Policyholders

Life and annuity buyers actively compare premiums, guarantees and projected returns across carriers, boosting buyer leverage as online aggregators and transparent illustrated disclosures widen price visibility. Switching costs are moderate due to surrender charges and tax implications, so policyholders may switch when price or guarantees diverge materially. Dai-ichi, as one of Japan’s top three life insurers, leverages brand trust and claims reputation to defend pricing.

Corporate and Group Clients

Large employers and affinity groups exert strong negotiating power over Dai-ichi Life, pressing for lower rates, enhanced features and higher service levels through competitive tenders. Tender processes heighten price competition and demand customized plan design, while Dai-ichi’s ability to bundle insurance with wellness programs and employee benefits helps mitigate discount pressure. Long-term contracts and measured service-quality metrics reduce churn and protect lifetime value.

International Customer Mix

Across Asia-Pacific and other markets buyers face diverse regulatory regimes and financial literacy levels; Asia accounted for 56% of global life insurance premiums in 2023, amplifying heterogenous demand patterns. In developing markets roughly 65% of new business remains agent-driven, so price and agent advice limit individual buyer power. In mature markets, sophisticated customers push transparency and performance, raising disclosure demands. Dai-ichi’s local subsidiaries tailor products and distribution to manage these power dynamics.

Switching and Surrender Dynamics

Policyholders weigh surrender penalties, tax impacts and underwriting requalification, so Dai-ichi faces moderate attrition pressure as customers compare net cash-on-surrender in 2024 market conditions.

Health deterioration for protection products raises switching frictions and reduces buyer power; for savings and annuities low-rate sensitivity increases focus on credited rates and fees; loyalty bonuses and riders further lock in relationships.

- Retention drivers: surrender penalties, tax treatment, underwriting

- Protection: health-linked frictions lower switching

- Savings/annuities: rate/fee sensitivity

- Design: loyalty bonuses/riders increase lock-in

Service and Digital Experience Expectations

Customers now expect seamless onboarding, claims and policy servicing; strong digital UX reduces price salience and weakens buyer leverage. Poor service raises complaints and switching intent, a risk Dai-ichi flags in its 2024 annual report. Dai-ichi’s continued omnichannel investments help contain buyer power by improving retention and speed.

- 2024 annual report: omnichannel focus

- Seamless UX lowers price sensitivity

- Poor service increases churn risk

APAC insurers face moderate buyer power; omnichannel moves ease price pressure

Buyers exert moderate bargaining power: retail policyholders compare premiums/guarantees online but face surrender/tax frictions, while large employers use tenders to demand price/custom features; Dai-ichi’s brand, loyalty riders and omnichannel service (2024 focus) mitigate pressure. Market heterogeneity across APAC alters buyer leverage by distribution channel and financial literacy.

| Metric | Value | Year/Source |

|---|---|---|

| Asia share of global premiums | 56% | 2023 |

| New business agent-driven (developing markets) | 65% | 2023 |

| Dai-ichi strategic focus | Omnichannel investments | 2024 annual report |

Preview Before You Purchase

Dai-ichi Life Porter's Five Forces Analysis

This preview shows the exact Dai‑ichi Life Porter's Five Forces analysis you'll receive after purchase—fully formatted and ready to use. No placeholders, mockups, or samples: the file available for instant download is this same document with no surprises. Complete your purchase and gain immediate access to the identical, professionally written analysis.