Dainichiseika Color & Chemicals Mfg Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

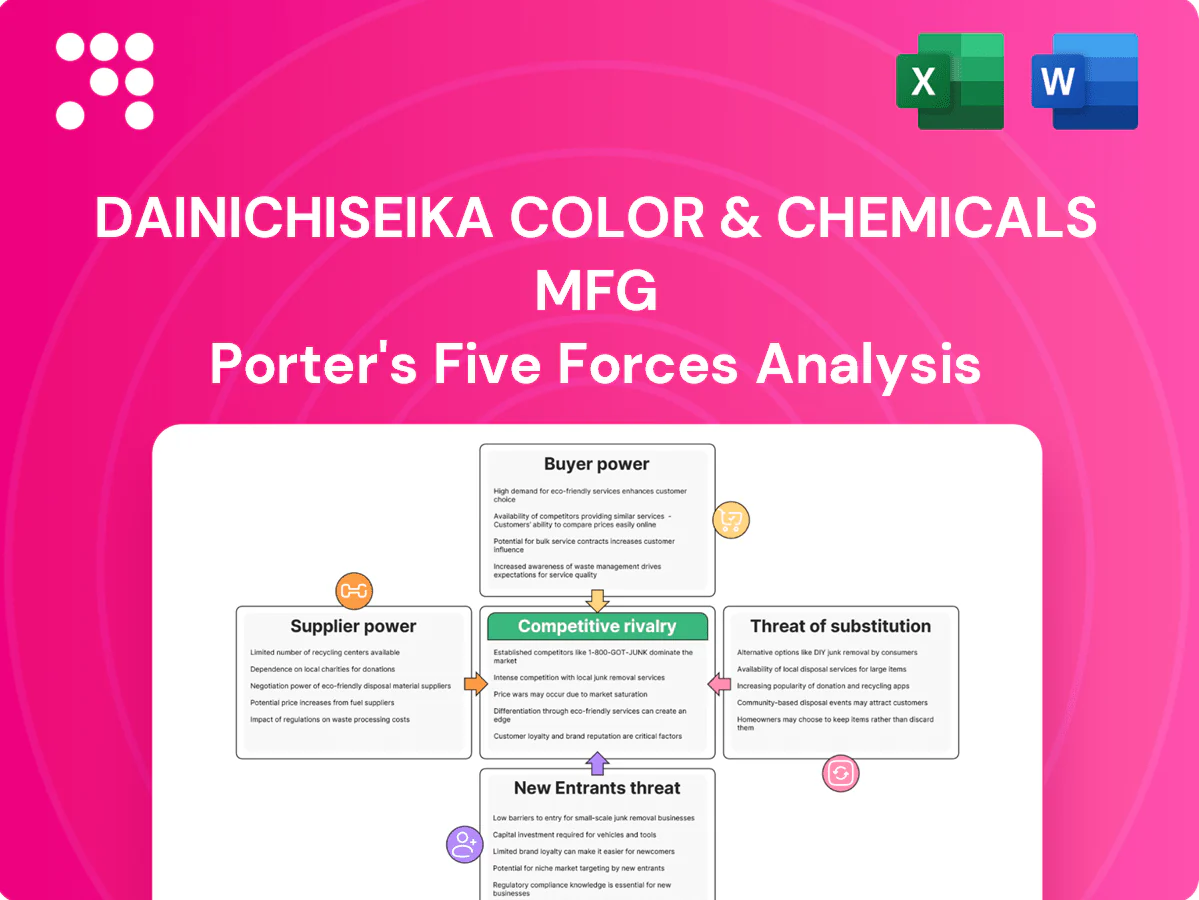

Dainichiseika Color & Chemicals faces moderate rivalry driven by specialized pigments, high supplier influence for key intermediates, and limited substitution thanks to formulation expertise, while regulatory and scale barriers keep new entrants in check. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dainichiseika Color & Chemicals Mfg’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Petrochemical feedstock dependence

Many pigments, resins and solvents at Dainichiseika are petrochemical-derived, tying input costs to oil and naphtha cycles; Brent averaged about $86/bbl in 2024, linking feedstock cost swings directly to margins. Volatility can shift bargaining leverage to upstream suppliers during tight markets, while long-term contracts and hedging reduce but do not eliminate exposure. Diversifying feedstock sources and integrating select intermediates lowers supplier power and cost pass-through risk.

Specialty chemicals and precursors concentration

High-purity intermediates such as azo and phthalocyanine precursors are produced by a limited global base, concentrating supply for Dainichiseika Color & Chemicals. Supplier substitution is constrained by regulatory scrutiny and qualification cycles typically taking 12–18 months. Automotive and electronics approved supplier lists further entrench lock-in. This concentration gives niche suppliers clear pricing and delivery leverage.

Compliance and sustainability constraints

REACH candidate list exceeded 200 SVHCs by 2024, RoHS restricts 10 substance groups, and EU food-contact rules (Reg. 10/2011) plus tightening VOC limits narrow acceptable raw materials for Dainichiseika Color & Chemicals. Suppliers offering REACH-, RoHS-, and food-safe certified low-toxicity inputs therefore gain negotiating strength. Switching to compliant alternatives requires weeks–months of migration/testing and validation, raising switching costs and increasing supplier influence.

Logistics and regional supply risks

Shipping constraints, port disruptions and currency swings hit imported inputs for Dainichiseika — Q1 2024 saw continued freight volatility and sporadic port congestion that lengthened lead times for chemical feedstocks in Japan and Asia. Regional geopolitical tensions and seasonal typhoon risks raise interruption probability; suppliers with integrated logistics networks have been able to command premiums. Multi-region sourcing and 60–120 day inventory buffers reduce this supplier leverage.

Scale of procurement vs. supplier size

Dainichiseika’s large-volume procurement gives it stronger pricing and payment terms with bulk commodity suppliers, while niche pigments and functional additives remain supplier-dominated because some vendors are larger and few in number, limiting buyer leverage. Co-development partnerships frequently exchange tighter pricing for early access to novel chemistries and customization, so supplier power is mixed across categories.

- Scale leverage: bulk commodities — favorable to Dainichiseika

- Niche inputs: supplier scale can exceed buyer power

- Co-development: price concessions for innovation access

- Overall: supplier power varies by material category

Supplier power split: Brent-linked feedstocks, concentrated pigment precursors, 12–18 month quals

Suppliers hold mixed power: commodity feedstocks tied to Brent (avg $86/bbl in 2024) give Dainichiseika scale leverage, while high-purity pigment precursors remain concentrated, raising supplier pricing leverage and long 12–18 month qualification cycles. Regulatory constraints (REACH >200 SVHCs in 2024) and Q1 2024 freight volatility increase switching costs and logistics premiums.

| Metric | 2024 value | Impact |

|---|---|---|

| Brent oil | $86/bbl | feedstock cost exposure |

| Qualification time | 12–18 months | high switching cost |

| REACH SVHCs | >200 | restricted inputs |

What is included in the product

Tailored Porter's Five Forces for Dainichiseika Color & Chemicals Mfg uncover key competitive drivers, supplier and buyer power, substitutes and new-entry risks, and highlight disruptive threats and protective market dynamics for strategic planning.

A single-sheet Porter’s Five Forces snapshot tailored to Dainichiseika Color & Chemicals—clarifies supplier power, buyer dynamics, competitive rivalry, substitution and entry threats for fast, boardroom-ready strategic decisions.

Customers Bargaining Power

Large OEMs demand cost-downs

Automotive, electronics and packaging majors impose strong price pressure on Dainichiseika, with many OEMs setting 2–4% cost-down targets in 2024. Consolidated purchasing and qualification cycles of 12–24 months amplify their leverage. Widespread dual-sourcing keeps supplier pricing competitive. Delivering measurable, value-added performance is essential to avoid commoditization.

High performance and regulatory specs

Buyers demand consistency, colorfastness, heat/UV resistance and certifications such as REACH, RoHS and ISO 9001, making technical specs central to procurement decisions. Consistently meeting these specs raises switching costs and moderates buyer power as reformulating colors or requalifying suppliers is costly. Failures can trigger recalls and brand damage, transferring financial and reputational risk to suppliers. Vendors that demonstrably exceed specs can command premium margins and tighter long-term contracts.

Customization and technical service

As of 2024 Dainichiseika's color matching, dispersion tuning, and application support embed its formulations into customer production lines, raising switching costs. Deep technical integration and on-site support reduce buyer ability to switch quickly. Technical lock-in from bespoke dispersions can offset price bargaining. Service differentiation thus serves as a key lever against customer bargaining power.

Substitution and backward integration options

Large converters and printers can switch to alternative ink systems or pigment vendors, and in 2024 the global printing inks market was about $42.5 billion, increasing suppliers' exposure. Some major converters pursue private-label or limited in-house compounding, raising buyer leverage; defensive long-term contracts and IP-anchored formulations mitigate this threat.

Demand cyclicality and inventory strategies

End-market cyclicality strengthens customers’ bargaining power as buyers push for flexible pricing and consignment during soft demand; in downturns they delay orders and renegotiate lead times and payment terms, while upcycles produce rush orders that swing leverage back to suppliers. Dainichiseika mitigates swings through agile supply agreements and tiered lead-time clauses to balance power across cycles.

- Buyers demand consignment and flexible pricing

- Downturns: order delays and renegotiation

- Upcycles: rush orders increase supplier leverage

- Mitigation: agile, tiered supply agreements

OEMs push 2–4% cuts; premiums endure amid $42.5B inks market

Automotive, electronics and packaging OEMs set 2–4% cost-down targets in 2024, consolidating purchasing and exerting strong price pressure.

Technical specs (REACH, RoHS, ISO) and 12–24 month qualification cycles raise switching costs, enabling premium pricing for superior performers.

Private-label and in-house compounding trends plus a $42.5B global inks market in 2024 increase buyer options; long-term contracts and IP mitigate leverage.

| Metric | 2024 |

|---|---|

| OEM cost-down targets | 2–4% |

| Qualification cycle | 12–24 months |

| Global printing inks market | $42.5B |

Same Document Delivered

Dainichiseika Color & Chemicals Mfg Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Dainichiseika Color & Chemicals Mfg you'll receive—no placeholders or samples. The full document is fully formatted, actionable and ready for download immediately after purchase. It covers rivalry, supplier and buyer power, and threats of entry and substitutes with data-driven insight.

A Must-Have Tool for Decision-Makers

Dainichiseika Color & Chemicals faces moderate rivalry driven by specialized pigments, high supplier influence for key intermediates, and limited substitution thanks to formulation expertise, while regulatory and scale barriers keep new entrants in check. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dainichiseika Color & Chemicals Mfg’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Petrochemical feedstock dependence

Many pigments, resins and solvents at Dainichiseika are petrochemical-derived, tying input costs to oil and naphtha cycles; Brent averaged about $86/bbl in 2024, linking feedstock cost swings directly to margins. Volatility can shift bargaining leverage to upstream suppliers during tight markets, while long-term contracts and hedging reduce but do not eliminate exposure. Diversifying feedstock sources and integrating select intermediates lowers supplier power and cost pass-through risk.

Specialty chemicals and precursors concentration

High-purity intermediates such as azo and phthalocyanine precursors are produced by a limited global base, concentrating supply for Dainichiseika Color & Chemicals. Supplier substitution is constrained by regulatory scrutiny and qualification cycles typically taking 12–18 months. Automotive and electronics approved supplier lists further entrench lock-in. This concentration gives niche suppliers clear pricing and delivery leverage.

Compliance and sustainability constraints

REACH candidate list exceeded 200 SVHCs by 2024, RoHS restricts 10 substance groups, and EU food-contact rules (Reg. 10/2011) plus tightening VOC limits narrow acceptable raw materials for Dainichiseika Color & Chemicals. Suppliers offering REACH-, RoHS-, and food-safe certified low-toxicity inputs therefore gain negotiating strength. Switching to compliant alternatives requires weeks–months of migration/testing and validation, raising switching costs and increasing supplier influence.

Logistics and regional supply risks

Shipping constraints, port disruptions and currency swings hit imported inputs for Dainichiseika — Q1 2024 saw continued freight volatility and sporadic port congestion that lengthened lead times for chemical feedstocks in Japan and Asia. Regional geopolitical tensions and seasonal typhoon risks raise interruption probability; suppliers with integrated logistics networks have been able to command premiums. Multi-region sourcing and 60–120 day inventory buffers reduce this supplier leverage.

Scale of procurement vs. supplier size

Dainichiseika’s large-volume procurement gives it stronger pricing and payment terms with bulk commodity suppliers, while niche pigments and functional additives remain supplier-dominated because some vendors are larger and few in number, limiting buyer leverage. Co-development partnerships frequently exchange tighter pricing for early access to novel chemistries and customization, so supplier power is mixed across categories.

- Scale leverage: bulk commodities — favorable to Dainichiseika

- Niche inputs: supplier scale can exceed buyer power

- Co-development: price concessions for innovation access

- Overall: supplier power varies by material category

Supplier power split: Brent-linked feedstocks, concentrated pigment precursors, 12–18 month quals

Suppliers hold mixed power: commodity feedstocks tied to Brent (avg $86/bbl in 2024) give Dainichiseika scale leverage, while high-purity pigment precursors remain concentrated, raising supplier pricing leverage and long 12–18 month qualification cycles. Regulatory constraints (REACH >200 SVHCs in 2024) and Q1 2024 freight volatility increase switching costs and logistics premiums.

| Metric | 2024 value | Impact |

|---|---|---|

| Brent oil | $86/bbl | feedstock cost exposure |

| Qualification time | 12–18 months | high switching cost |

| REACH SVHCs | >200 | restricted inputs |

What is included in the product

Tailored Porter's Five Forces for Dainichiseika Color & Chemicals Mfg uncover key competitive drivers, supplier and buyer power, substitutes and new-entry risks, and highlight disruptive threats and protective market dynamics for strategic planning.

A single-sheet Porter’s Five Forces snapshot tailored to Dainichiseika Color & Chemicals—clarifies supplier power, buyer dynamics, competitive rivalry, substitution and entry threats for fast, boardroom-ready strategic decisions.

Customers Bargaining Power

Large OEMs demand cost-downs

Automotive, electronics and packaging majors impose strong price pressure on Dainichiseika, with many OEMs setting 2–4% cost-down targets in 2024. Consolidated purchasing and qualification cycles of 12–24 months amplify their leverage. Widespread dual-sourcing keeps supplier pricing competitive. Delivering measurable, value-added performance is essential to avoid commoditization.

High performance and regulatory specs

Buyers demand consistency, colorfastness, heat/UV resistance and certifications such as REACH, RoHS and ISO 9001, making technical specs central to procurement decisions. Consistently meeting these specs raises switching costs and moderates buyer power as reformulating colors or requalifying suppliers is costly. Failures can trigger recalls and brand damage, transferring financial and reputational risk to suppliers. Vendors that demonstrably exceed specs can command premium margins and tighter long-term contracts.

Customization and technical service

As of 2024 Dainichiseika's color matching, dispersion tuning, and application support embed its formulations into customer production lines, raising switching costs. Deep technical integration and on-site support reduce buyer ability to switch quickly. Technical lock-in from bespoke dispersions can offset price bargaining. Service differentiation thus serves as a key lever against customer bargaining power.

Substitution and backward integration options

Large converters and printers can switch to alternative ink systems or pigment vendors, and in 2024 the global printing inks market was about $42.5 billion, increasing suppliers' exposure. Some major converters pursue private-label or limited in-house compounding, raising buyer leverage; defensive long-term contracts and IP-anchored formulations mitigate this threat.

Demand cyclicality and inventory strategies

End-market cyclicality strengthens customers’ bargaining power as buyers push for flexible pricing and consignment during soft demand; in downturns they delay orders and renegotiate lead times and payment terms, while upcycles produce rush orders that swing leverage back to suppliers. Dainichiseika mitigates swings through agile supply agreements and tiered lead-time clauses to balance power across cycles.

- Buyers demand consignment and flexible pricing

- Downturns: order delays and renegotiation

- Upcycles: rush orders increase supplier leverage

- Mitigation: agile, tiered supply agreements

OEMs push 2–4% cuts; premiums endure amid $42.5B inks market

Automotive, electronics and packaging OEMs set 2–4% cost-down targets in 2024, consolidating purchasing and exerting strong price pressure.

Technical specs (REACH, RoHS, ISO) and 12–24 month qualification cycles raise switching costs, enabling premium pricing for superior performers.

Private-label and in-house compounding trends plus a $42.5B global inks market in 2024 increase buyer options; long-term contracts and IP mitigate leverage.

| Metric | 2024 |

|---|---|

| OEM cost-down targets | 2–4% |

| Qualification cycle | 12–24 months |

| Global printing inks market | $42.5B |

Same Document Delivered

Dainichiseika Color & Chemicals Mfg Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Dainichiseika Color & Chemicals Mfg you'll receive—no placeholders or samples. The full document is fully formatted, actionable and ready for download immediately after purchase. It covers rivalry, supplier and buyer power, and threats of entry and substitutes with data-driven insight.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Dainichiseika Color & Chemicals faces moderate rivalry driven by specialized pigments, high supplier influence for key intermediates, and limited substitution thanks to formulation expertise, while regulatory and scale barriers keep new entrants in check. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dainichiseika Color & Chemicals Mfg’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Petrochemical feedstock dependence

Many pigments, resins and solvents at Dainichiseika are petrochemical-derived, tying input costs to oil and naphtha cycles; Brent averaged about $86/bbl in 2024, linking feedstock cost swings directly to margins. Volatility can shift bargaining leverage to upstream suppliers during tight markets, while long-term contracts and hedging reduce but do not eliminate exposure. Diversifying feedstock sources and integrating select intermediates lowers supplier power and cost pass-through risk.

Specialty chemicals and precursors concentration

High-purity intermediates such as azo and phthalocyanine precursors are produced by a limited global base, concentrating supply for Dainichiseika Color & Chemicals. Supplier substitution is constrained by regulatory scrutiny and qualification cycles typically taking 12–18 months. Automotive and electronics approved supplier lists further entrench lock-in. This concentration gives niche suppliers clear pricing and delivery leverage.

Compliance and sustainability constraints

REACH candidate list exceeded 200 SVHCs by 2024, RoHS restricts 10 substance groups, and EU food-contact rules (Reg. 10/2011) plus tightening VOC limits narrow acceptable raw materials for Dainichiseika Color & Chemicals. Suppliers offering REACH-, RoHS-, and food-safe certified low-toxicity inputs therefore gain negotiating strength. Switching to compliant alternatives requires weeks–months of migration/testing and validation, raising switching costs and increasing supplier influence.

Logistics and regional supply risks

Shipping constraints, port disruptions and currency swings hit imported inputs for Dainichiseika — Q1 2024 saw continued freight volatility and sporadic port congestion that lengthened lead times for chemical feedstocks in Japan and Asia. Regional geopolitical tensions and seasonal typhoon risks raise interruption probability; suppliers with integrated logistics networks have been able to command premiums. Multi-region sourcing and 60–120 day inventory buffers reduce this supplier leverage.

Scale of procurement vs. supplier size

Dainichiseika’s large-volume procurement gives it stronger pricing and payment terms with bulk commodity suppliers, while niche pigments and functional additives remain supplier-dominated because some vendors are larger and few in number, limiting buyer leverage. Co-development partnerships frequently exchange tighter pricing for early access to novel chemistries and customization, so supplier power is mixed across categories.

- Scale leverage: bulk commodities — favorable to Dainichiseika

- Niche inputs: supplier scale can exceed buyer power

- Co-development: price concessions for innovation access

- Overall: supplier power varies by material category

Supplier power split: Brent-linked feedstocks, concentrated pigment precursors, 12–18 month quals

Suppliers hold mixed power: commodity feedstocks tied to Brent (avg $86/bbl in 2024) give Dainichiseika scale leverage, while high-purity pigment precursors remain concentrated, raising supplier pricing leverage and long 12–18 month qualification cycles. Regulatory constraints (REACH >200 SVHCs in 2024) and Q1 2024 freight volatility increase switching costs and logistics premiums.

| Metric | 2024 value | Impact |

|---|---|---|

| Brent oil | $86/bbl | feedstock cost exposure |

| Qualification time | 12–18 months | high switching cost |

| REACH SVHCs | >200 | restricted inputs |

What is included in the product

Tailored Porter's Five Forces for Dainichiseika Color & Chemicals Mfg uncover key competitive drivers, supplier and buyer power, substitutes and new-entry risks, and highlight disruptive threats and protective market dynamics for strategic planning.

A single-sheet Porter’s Five Forces snapshot tailored to Dainichiseika Color & Chemicals—clarifies supplier power, buyer dynamics, competitive rivalry, substitution and entry threats for fast, boardroom-ready strategic decisions.

Customers Bargaining Power

Large OEMs demand cost-downs

Automotive, electronics and packaging majors impose strong price pressure on Dainichiseika, with many OEMs setting 2–4% cost-down targets in 2024. Consolidated purchasing and qualification cycles of 12–24 months amplify their leverage. Widespread dual-sourcing keeps supplier pricing competitive. Delivering measurable, value-added performance is essential to avoid commoditization.

High performance and regulatory specs

Buyers demand consistency, colorfastness, heat/UV resistance and certifications such as REACH, RoHS and ISO 9001, making technical specs central to procurement decisions. Consistently meeting these specs raises switching costs and moderates buyer power as reformulating colors or requalifying suppliers is costly. Failures can trigger recalls and brand damage, transferring financial and reputational risk to suppliers. Vendors that demonstrably exceed specs can command premium margins and tighter long-term contracts.

Customization and technical service

As of 2024 Dainichiseika's color matching, dispersion tuning, and application support embed its formulations into customer production lines, raising switching costs. Deep technical integration and on-site support reduce buyer ability to switch quickly. Technical lock-in from bespoke dispersions can offset price bargaining. Service differentiation thus serves as a key lever against customer bargaining power.

Substitution and backward integration options

Large converters and printers can switch to alternative ink systems or pigment vendors, and in 2024 the global printing inks market was about $42.5 billion, increasing suppliers' exposure. Some major converters pursue private-label or limited in-house compounding, raising buyer leverage; defensive long-term contracts and IP-anchored formulations mitigate this threat.

Demand cyclicality and inventory strategies

End-market cyclicality strengthens customers’ bargaining power as buyers push for flexible pricing and consignment during soft demand; in downturns they delay orders and renegotiate lead times and payment terms, while upcycles produce rush orders that swing leverage back to suppliers. Dainichiseika mitigates swings through agile supply agreements and tiered lead-time clauses to balance power across cycles.

- Buyers demand consignment and flexible pricing

- Downturns: order delays and renegotiation

- Upcycles: rush orders increase supplier leverage

- Mitigation: agile, tiered supply agreements

OEMs push 2–4% cuts; premiums endure amid $42.5B inks market

Automotive, electronics and packaging OEMs set 2–4% cost-down targets in 2024, consolidating purchasing and exerting strong price pressure.

Technical specs (REACH, RoHS, ISO) and 12–24 month qualification cycles raise switching costs, enabling premium pricing for superior performers.

Private-label and in-house compounding trends plus a $42.5B global inks market in 2024 increase buyer options; long-term contracts and IP mitigate leverage.

| Metric | 2024 |

|---|---|

| OEM cost-down targets | 2–4% |

| Qualification cycle | 12–24 months |

| Global printing inks market | $42.5B |

Same Document Delivered

Dainichiseika Color & Chemicals Mfg Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Dainichiseika Color & Chemicals Mfg you'll receive—no placeholders or samples. The full document is fully formatted, actionable and ready for download immediately after purchase. It covers rivalry, supplier and buyer power, and threats of entry and substitutes with data-driven insight.