Daikin Industries Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

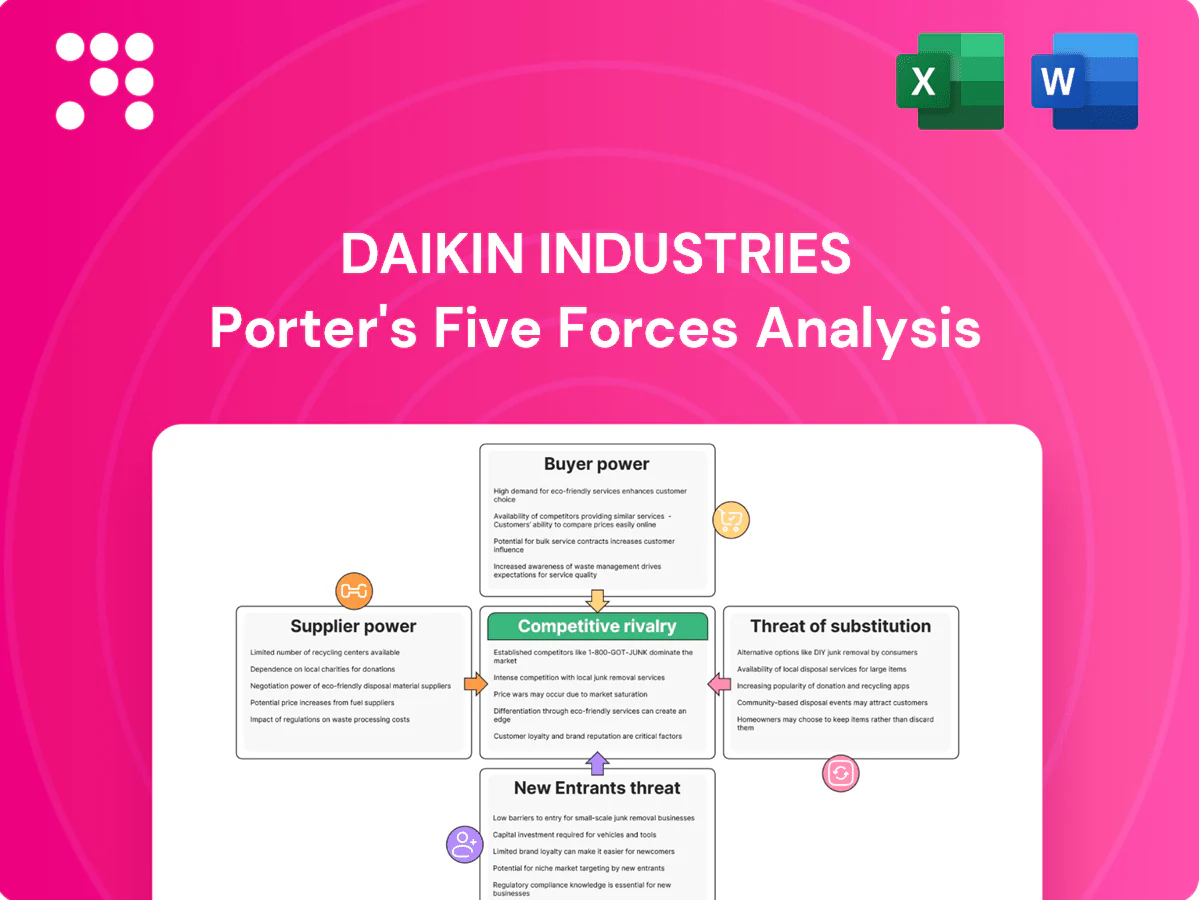

Daikin Industries faces intense industry rivalry tempered by strong brand scale and high entry barriers, with moderate buyer power and manageable supplier influence in HVAC components; substitute threats arise from energy-efficient alternatives and smart home integrations. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Daikin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical components concentration

Compressors, power electronics and semiconductors for Daikin come from a relatively concentrated supplier base, raising supplier leverage and price-setting power in key components. Rare earth magnets and copper expose Daikin to commodity volatility, with over 60% of rare earth production concentrated in China. Qualification cycles for HVAC components often exceed 12 months, making rapid switching costly. Dual-sourcing mitigates but cannot eliminate concentration risk.

Vertical integration in refrigerants

Daikin’s in‑house fluorochemicals capability reduces reliance on external refrigerant suppliers, giving the company tighter control over cost and availability of low‑GWP blends. Vertical integration accelerates product shifts to meet HFC phase‑down regulations and blunts supplier power where Daikin controls key inputs. This integration strengthens negotiating leverage on price, logistics and compliance timing.

Long-term contracts and scale

Daikin's global scale—reported consolidated sales of ¥3.3 trillion in FY2024—enables multi-year volume commitments that trade price for supply stability; predictable orders let suppliers plan capacity, while Daikin negotiates rebates and vendor-managed inventory arrangements, using scale-driven leverage to reduce average supplier power and blunt supplier bargaining.

Regulatory and standards lock-in

Safety and energy standards force Daikin to source certified components, sharply narrowing qualified suppliers and raising dependence on niche vendors. Suppliers of compliant parts often command premiums and cause multi-month requalification processes that deter switching. This compliance rigidity increases supplier bargaining power in regulated sub-systems.

- Certified components narrow supplier pool

- Compliant parts command premiums

- Requalification deters switching

- Regulatory rigidity elevates supplier power

Geopolitical and logistics exposure

Geopolitical trade restrictions, tariffs and freight disruptions continue to pressure Daikin’s suppliers; in 2024 container rates stayed roughly 50% below 2021 peaks while episodic port congestion raised costs. Regionalization adds redundancy but increases sourcing costs; nearshoring and buffer inventory have tempered shocks. Volatility intermittently strengthens supplier bargaining power.

- Trade risks: tariffs and restrictions

- Cost of regionalization: higher OPEX

- Mitigants: nearshoring, buffer stock

- Effect: intermittent supplier leverage

China-heavy supply, >12-month quals raise supplier leverage; scale and integration counteract

Concentrated suppliers for compressors, power electronics and rare earths (China >60% of production) give vendors price leverage; qualification cycles >12 months raise switching costs. Daikin’s in‑house fluorochemicals and ¥3.3 trillion FY2024 scale reduce supplier power via vertical integration and volume deals. Trade volatility (container rates ~50% below 2021 peaks) intermittently strengthens supplier bargaining.

| Metric | Value |

|---|---|

| FY2024 consolidated sales | ¥3.3 trillion |

| Rare earth production (China) | >60% |

| Container rates vs 2021 | ≈-50% |

| HVAC qualification cycle | >12 months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive forces facing Daikin Industries, with strategic commentary on pricing and profitability. Tailored insights highlight barriers protecting incumbency and vulnerabilities that could erode market share.

A clear, one-sheet Porter's Five Forces summary for Daikin—perfect for quick decision-making and pinpointing supplier, buyer and competitive pressure pain points. Swap in your own data to model refrigerant-regulation or new-entrant scenarios with a clean layout ready for pitch decks.

Customers Bargaining Power

Fragmented retail buyers

Residential buyers are highly fragmented—over 2 billion households globally—so individual leverage against manufacturers is minimal; Daikin’s scale (FY2024 consolidated sales around ¥2.7 trillion) relies on brand and product efficiency rather than retail price pressure. Purchase decisions are driven by brand reputation, energy-efficiency ratings and installer recommendations, creating moderate switching costs. Price sensitivity exists, but overall buyer power in retail channels remains low.

Powerful commercial accounts

Large commercial and industrial clients buy Daikin systems via tenders and framework agreements, demanding customization, performance guarantees and lifecycle pricing; consolidated volumes in major projects grant buyers significant negotiating leverage. Daikin reported consolidated sales of ¥3,421.0 billion for FY2024, and project contracts often represent double-digit percentages of regional sales, increasing buyer power. Buyer bargaining is high on major projects and public tenders.

Distributor and installer influence

Distributor and installer influence is strong as Daikin’s channel network across 60+ countries shapes product selection and after-sales, with local partners holding inventory risk and granular market knowledge that increases bargaining clout. Incentive programs and co-marketing—allocated in 2024 as a prioritized channel spend—help balance influence and secure shelf space. Tight management of channel margins remains critical to retain pull-through and protect end-customer pricing.

Total cost of ownership focus

Regulatory and subsidy effects

Fragmented buyers, FY2024 sales ¥3,421.0bn, reach 60+ countries

Residential buyers are fragmented (>2 billion households) so retail bargaining is low; FY2024 consolidated sales ¥3,421.0 billion underpin brand pricing power. Commercial tenders and large projects give buyers high leverage, often representing double‑digit shares of regional sales. Distributor/installer networks (60+ countries) and TCO/sustainability demands raise buyer sophistication and price/spec pressure.

| Metric | Value |

|---|---|

| FY2024 consolidated sales | ¥3,421.0 billion |

| Household market | >2 billion households |

| Channel reach | 60+ countries |

| Project impact | Double‑digit % regional sales |

Preview Before You Purchase

Daikin Industries Porter's Five Forces Analysis

This preview shows the exact Daikin Industries Porter's Five Forces analysis you’ll receive—no samples or placeholders. The full document is fully formatted and ready for immediate download upon purchase. What you see here is precisely the deliverable you’ll get, instantly and unchanged.

Go Beyond the Preview—Access the Full Strategic Report

Daikin Industries faces intense industry rivalry tempered by strong brand scale and high entry barriers, with moderate buyer power and manageable supplier influence in HVAC components; substitute threats arise from energy-efficient alternatives and smart home integrations. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Daikin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical components concentration

Compressors, power electronics and semiconductors for Daikin come from a relatively concentrated supplier base, raising supplier leverage and price-setting power in key components. Rare earth magnets and copper expose Daikin to commodity volatility, with over 60% of rare earth production concentrated in China. Qualification cycles for HVAC components often exceed 12 months, making rapid switching costly. Dual-sourcing mitigates but cannot eliminate concentration risk.

Vertical integration in refrigerants

Daikin’s in‑house fluorochemicals capability reduces reliance on external refrigerant suppliers, giving the company tighter control over cost and availability of low‑GWP blends. Vertical integration accelerates product shifts to meet HFC phase‑down regulations and blunts supplier power where Daikin controls key inputs. This integration strengthens negotiating leverage on price, logistics and compliance timing.

Long-term contracts and scale

Daikin's global scale—reported consolidated sales of ¥3.3 trillion in FY2024—enables multi-year volume commitments that trade price for supply stability; predictable orders let suppliers plan capacity, while Daikin negotiates rebates and vendor-managed inventory arrangements, using scale-driven leverage to reduce average supplier power and blunt supplier bargaining.

Regulatory and standards lock-in

Safety and energy standards force Daikin to source certified components, sharply narrowing qualified suppliers and raising dependence on niche vendors. Suppliers of compliant parts often command premiums and cause multi-month requalification processes that deter switching. This compliance rigidity increases supplier bargaining power in regulated sub-systems.

- Certified components narrow supplier pool

- Compliant parts command premiums

- Requalification deters switching

- Regulatory rigidity elevates supplier power

Geopolitical and logistics exposure

Geopolitical trade restrictions, tariffs and freight disruptions continue to pressure Daikin’s suppliers; in 2024 container rates stayed roughly 50% below 2021 peaks while episodic port congestion raised costs. Regionalization adds redundancy but increases sourcing costs; nearshoring and buffer inventory have tempered shocks. Volatility intermittently strengthens supplier bargaining power.

- Trade risks: tariffs and restrictions

- Cost of regionalization: higher OPEX

- Mitigants: nearshoring, buffer stock

- Effect: intermittent supplier leverage

China-heavy supply, >12-month quals raise supplier leverage; scale and integration counteract

Concentrated suppliers for compressors, power electronics and rare earths (China >60% of production) give vendors price leverage; qualification cycles >12 months raise switching costs. Daikin’s in‑house fluorochemicals and ¥3.3 trillion FY2024 scale reduce supplier power via vertical integration and volume deals. Trade volatility (container rates ~50% below 2021 peaks) intermittently strengthens supplier bargaining.

| Metric | Value |

|---|---|

| FY2024 consolidated sales | ¥3.3 trillion |

| Rare earth production (China) | >60% |

| Container rates vs 2021 | ≈-50% |

| HVAC qualification cycle | >12 months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive forces facing Daikin Industries, with strategic commentary on pricing and profitability. Tailored insights highlight barriers protecting incumbency and vulnerabilities that could erode market share.

A clear, one-sheet Porter's Five Forces summary for Daikin—perfect for quick decision-making and pinpointing supplier, buyer and competitive pressure pain points. Swap in your own data to model refrigerant-regulation or new-entrant scenarios with a clean layout ready for pitch decks.

Customers Bargaining Power

Fragmented retail buyers

Residential buyers are highly fragmented—over 2 billion households globally—so individual leverage against manufacturers is minimal; Daikin’s scale (FY2024 consolidated sales around ¥2.7 trillion) relies on brand and product efficiency rather than retail price pressure. Purchase decisions are driven by brand reputation, energy-efficiency ratings and installer recommendations, creating moderate switching costs. Price sensitivity exists, but overall buyer power in retail channels remains low.

Powerful commercial accounts

Large commercial and industrial clients buy Daikin systems via tenders and framework agreements, demanding customization, performance guarantees and lifecycle pricing; consolidated volumes in major projects grant buyers significant negotiating leverage. Daikin reported consolidated sales of ¥3,421.0 billion for FY2024, and project contracts often represent double-digit percentages of regional sales, increasing buyer power. Buyer bargaining is high on major projects and public tenders.

Distributor and installer influence

Distributor and installer influence is strong as Daikin’s channel network across 60+ countries shapes product selection and after-sales, with local partners holding inventory risk and granular market knowledge that increases bargaining clout. Incentive programs and co-marketing—allocated in 2024 as a prioritized channel spend—help balance influence and secure shelf space. Tight management of channel margins remains critical to retain pull-through and protect end-customer pricing.

Total cost of ownership focus

Regulatory and subsidy effects

Fragmented buyers, FY2024 sales ¥3,421.0bn, reach 60+ countries

Residential buyers are fragmented (>2 billion households) so retail bargaining is low; FY2024 consolidated sales ¥3,421.0 billion underpin brand pricing power. Commercial tenders and large projects give buyers high leverage, often representing double‑digit shares of regional sales. Distributor/installer networks (60+ countries) and TCO/sustainability demands raise buyer sophistication and price/spec pressure.

| Metric | Value |

|---|---|

| FY2024 consolidated sales | ¥3,421.0 billion |

| Household market | >2 billion households |

| Channel reach | 60+ countries |

| Project impact | Double‑digit % regional sales |

Preview Before You Purchase

Daikin Industries Porter's Five Forces Analysis

This preview shows the exact Daikin Industries Porter's Five Forces analysis you’ll receive—no samples or placeholders. The full document is fully formatted and ready for immediate download upon purchase. What you see here is precisely the deliverable you’ll get, instantly and unchanged.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Daikin Industries faces intense industry rivalry tempered by strong brand scale and high entry barriers, with moderate buyer power and manageable supplier influence in HVAC components; substitute threats arise from energy-efficient alternatives and smart home integrations. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Daikin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical components concentration

Compressors, power electronics and semiconductors for Daikin come from a relatively concentrated supplier base, raising supplier leverage and price-setting power in key components. Rare earth magnets and copper expose Daikin to commodity volatility, with over 60% of rare earth production concentrated in China. Qualification cycles for HVAC components often exceed 12 months, making rapid switching costly. Dual-sourcing mitigates but cannot eliminate concentration risk.

Vertical integration in refrigerants

Daikin’s in‑house fluorochemicals capability reduces reliance on external refrigerant suppliers, giving the company tighter control over cost and availability of low‑GWP blends. Vertical integration accelerates product shifts to meet HFC phase‑down regulations and blunts supplier power where Daikin controls key inputs. This integration strengthens negotiating leverage on price, logistics and compliance timing.

Long-term contracts and scale

Daikin's global scale—reported consolidated sales of ¥3.3 trillion in FY2024—enables multi-year volume commitments that trade price for supply stability; predictable orders let suppliers plan capacity, while Daikin negotiates rebates and vendor-managed inventory arrangements, using scale-driven leverage to reduce average supplier power and blunt supplier bargaining.

Regulatory and standards lock-in

Safety and energy standards force Daikin to source certified components, sharply narrowing qualified suppliers and raising dependence on niche vendors. Suppliers of compliant parts often command premiums and cause multi-month requalification processes that deter switching. This compliance rigidity increases supplier bargaining power in regulated sub-systems.

- Certified components narrow supplier pool

- Compliant parts command premiums

- Requalification deters switching

- Regulatory rigidity elevates supplier power

Geopolitical and logistics exposure

Geopolitical trade restrictions, tariffs and freight disruptions continue to pressure Daikin’s suppliers; in 2024 container rates stayed roughly 50% below 2021 peaks while episodic port congestion raised costs. Regionalization adds redundancy but increases sourcing costs; nearshoring and buffer inventory have tempered shocks. Volatility intermittently strengthens supplier bargaining power.

- Trade risks: tariffs and restrictions

- Cost of regionalization: higher OPEX

- Mitigants: nearshoring, buffer stock

- Effect: intermittent supplier leverage

China-heavy supply, >12-month quals raise supplier leverage; scale and integration counteract

Concentrated suppliers for compressors, power electronics and rare earths (China >60% of production) give vendors price leverage; qualification cycles >12 months raise switching costs. Daikin’s in‑house fluorochemicals and ¥3.3 trillion FY2024 scale reduce supplier power via vertical integration and volume deals. Trade volatility (container rates ~50% below 2021 peaks) intermittently strengthens supplier bargaining.

| Metric | Value |

|---|---|

| FY2024 consolidated sales | ¥3.3 trillion |

| Rare earth production (China) | >60% |

| Container rates vs 2021 | ≈-50% |

| HVAC qualification cycle | >12 months |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptive forces facing Daikin Industries, with strategic commentary on pricing and profitability. Tailored insights highlight barriers protecting incumbency and vulnerabilities that could erode market share.

A clear, one-sheet Porter's Five Forces summary for Daikin—perfect for quick decision-making and pinpointing supplier, buyer and competitive pressure pain points. Swap in your own data to model refrigerant-regulation or new-entrant scenarios with a clean layout ready for pitch decks.

Customers Bargaining Power

Fragmented retail buyers

Residential buyers are highly fragmented—over 2 billion households globally—so individual leverage against manufacturers is minimal; Daikin’s scale (FY2024 consolidated sales around ¥2.7 trillion) relies on brand and product efficiency rather than retail price pressure. Purchase decisions are driven by brand reputation, energy-efficiency ratings and installer recommendations, creating moderate switching costs. Price sensitivity exists, but overall buyer power in retail channels remains low.

Powerful commercial accounts

Large commercial and industrial clients buy Daikin systems via tenders and framework agreements, demanding customization, performance guarantees and lifecycle pricing; consolidated volumes in major projects grant buyers significant negotiating leverage. Daikin reported consolidated sales of ¥3,421.0 billion for FY2024, and project contracts often represent double-digit percentages of regional sales, increasing buyer power. Buyer bargaining is high on major projects and public tenders.

Distributor and installer influence

Distributor and installer influence is strong as Daikin’s channel network across 60+ countries shapes product selection and after-sales, with local partners holding inventory risk and granular market knowledge that increases bargaining clout. Incentive programs and co-marketing—allocated in 2024 as a prioritized channel spend—help balance influence and secure shelf space. Tight management of channel margins remains critical to retain pull-through and protect end-customer pricing.

Total cost of ownership focus

Regulatory and subsidy effects

Fragmented buyers, FY2024 sales ¥3,421.0bn, reach 60+ countries

Residential buyers are fragmented (>2 billion households) so retail bargaining is low; FY2024 consolidated sales ¥3,421.0 billion underpin brand pricing power. Commercial tenders and large projects give buyers high leverage, often representing double‑digit shares of regional sales. Distributor/installer networks (60+ countries) and TCO/sustainability demands raise buyer sophistication and price/spec pressure.

| Metric | Value |

|---|---|

| FY2024 consolidated sales | ¥3,421.0 billion |

| Household market | >2 billion households |

| Channel reach | 60+ countries |

| Project impact | Double‑digit % regional sales |

Preview Before You Purchase

Daikin Industries Porter's Five Forces Analysis

This preview shows the exact Daikin Industries Porter's Five Forces analysis you’ll receive—no samples or placeholders. The full document is fully formatted and ready for immediate download upon purchase. What you see here is precisely the deliverable you’ll get, instantly and unchanged.