Daktronics Porter's Five Forces Analysis

From Overview to Strategy Blueprint

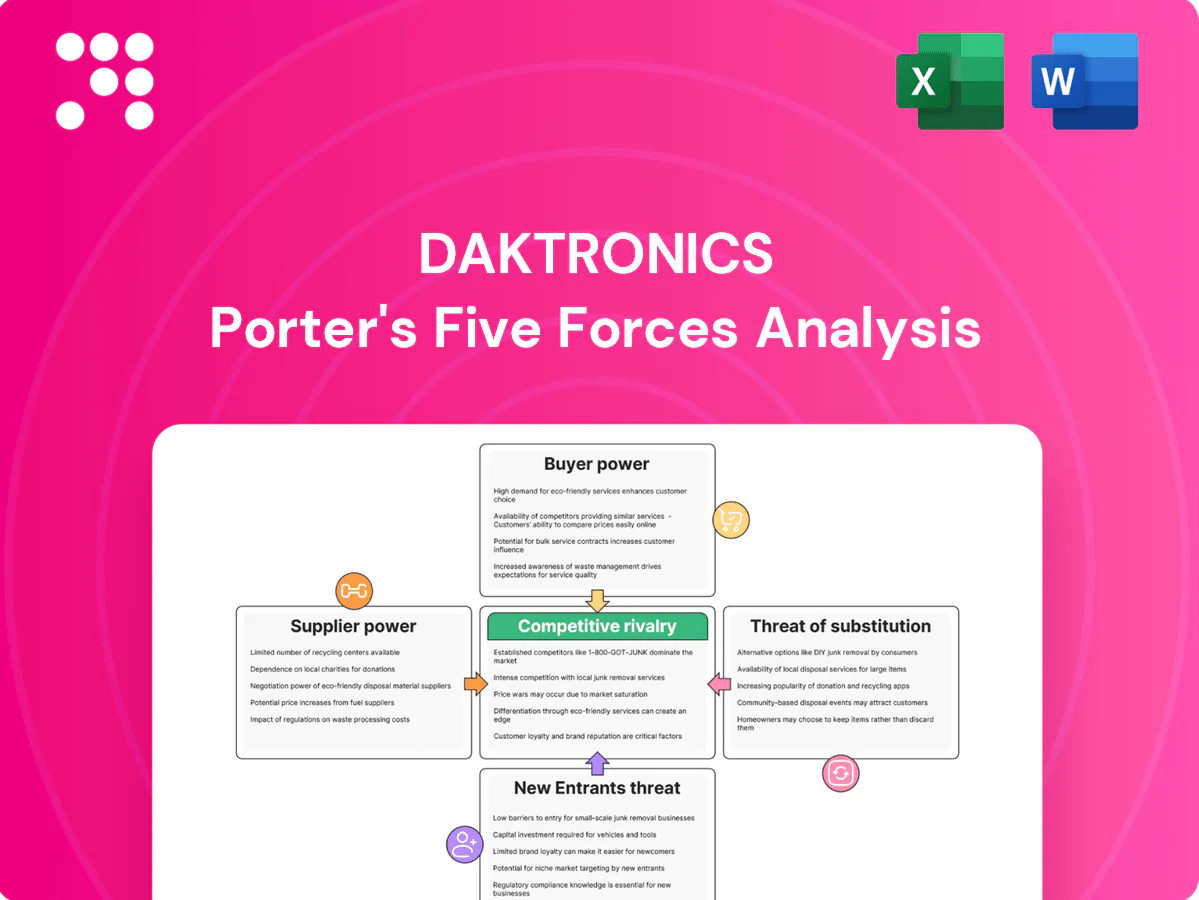

Daktronics faces moderate buyer power and supplier leverage, intense rivalry in signage/display markets, and a medium threat from substitutes and new entrants driven by tech shifts. Our snapshot highlights strategic vulnerabilities in pricing and innovation cadence. This brief overview hints at market pressures and growth levers. Unlock the full Porter's Five Forces Analysis to explore Daktronics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated LED components

High-brightness LEDs, drivers and controllers are sourced from a limited set of global suppliers—Nichia, Osram, Samsung and Seoul Semiconductor are among the largest in 2024—giving suppliers elevated pricing power and the potential to elongate lead times. Daktronics reports multi-sourcing and long-term agreements in its 2024 filings to mitigate risk, but substitution costs and qualification time remain non-trivial. Any supplier disruption directly delays production schedules and pressures margins.

Specialized materials and optics

Custom optics, weatherproof enclosures and thermal materials for Daktronics are specialized and often not interchangeable, creating supplier leverage; lead times commonly run 12–20 weeks and qualification cycles 6–18 months. Suppliers holding proprietary specs can negotiate favorable terms and command price premiums up to 15%, raising switching costs and impacting cost and delivery reliability.

Electronics and semiconductor cycles

Cyclical semiconductor tightness affects availability of controllers, ICs and power modules, with global semiconductor sales ~USD 580B in 2024 and lead times that surged in prior cycles still averaging 8–12 weeks for specialty parts. During shortages allocation typically favors large OEMs, pressuring mid-cap manufacturers like Daktronics. Price volatility can compress gross margins on fixed-price contracts, though strategic inventory and design flexibility partially offset exposure.

Logistics and large-format integration

Large-format LED screens require heavy logistics, structural components, and precise integration services, giving specialized freight carriers, fabricators, and installers leverage in project negotiations.

Limited regional alternatives increase client dependence, while bundled logistics contracts stabilize costs but lock customers into less flexible arrangements.

- supplier-concentration

- specialized-capabilities

- regional-dependence

- bundled-contracts-reduce-flexibility

Content and software partners

Third-party content tools, media processors and integrations add supplier touchpoints; in 2024 the global digital signage market exceeded $25 billion, increasing supplier influence. Platform certifications create soft lock-in; vendors levy premium support for mission-critical arenas. Building in-house software cuts vendor leverage but raises development and maintenance cost.

- Third-party touchpoints

- Soft lock-in via compatibility

- Premium mission-critical fees

- In-house reduces leverage, ups cost

Supplier concentration drives 8-20 week LED lead times and up to 15% pricing risk

Supplier concentration (Nichia, Osram, Samsung, Seoul) and specialized components give suppliers pricing and lead-time power; LED/driver lead times 8–20 weeks and qualification 6–18 months. Daktronics' 2024 multi-sourcing and long-term contracts reduce but do not eliminate 15% price-premium risk; semiconductor market ~USD 580B (2024), digital signage >USD 25B (2024).

| Metric | 2024 |

|---|---|

| Semiconductor sales | ~USD 580B |

| Digital signage market | >USD 25B |

| Lead times | 8–20 weeks |

| Price premium | up to 15% |

What is included in the product

Tailored Porter's Five Forces analysis for Daktronics that uncovers key drivers of competition, customer and supplier power, and market entry risks, while identifying disruptive substitutes and emerging threats to its market share. Includes strategic commentary on pricing influence, barriers protecting incumbents, and implications for Daktronics’ profitability and positioning.

A clear, one-sheet Porter's Five Forces summary for Daktronics—perfect for quick strategic decisions and investor briefings; customize force intensities based on new market data and swap in your own notes for immediate boardroom use.

Customers Bargaining Power

Concentrated marquee customers

Major sports leagues, stadiums and large DOOH networks are few and high-value; for context NFL average attendance is about 67,000 and MLB about 29,000 per game in recent seasons, amplifying their purchasing leverage. Their scale and visibility grant strong negotiating power on price and SLAs, and competitive bidding forces concessions. Losing a marquee deal can materially dent backlog and market signaling.

Professional procurement

Professional procurement for Daktronics-facing contracts runs detailed RFPs with strict specs and penalty clauses, and buyers routinely pit vendors to extract better commercial terms. Warranty scope, financing options, and uptime SLAs — often targeting 99.9% availability — become decisive levers. This sophistication drives discount pressure (commonly exceeding 10%) and higher ongoing service obligations.

Switching costs with legacy systems

Installed bases and proprietary control software create moderate switching costs for Daktronics customers, especially for stadium and transit integrations. In 2024, wider adoption of HTML5 content and IP-based signage protocols made retrofits and content portability easier, tempering vendor lock-in. Buyers often time replacements to capital cycles, raising bargaining power at refresh events. Strong service records and favorable TCO help Daktronics preserve pricing discipline.

Global options and transparency

Global options and transparency increase customer leverage: international rivals and ODMs expand choice while public case studies and benchmarks make comparisons easier. Buyers now push price cuts by benchmarking pixel pitch, nits and lifetime; the LED display market was estimated at about $11.6B in 2024, raising pressure on margins. Daktronics must bundle services to offset pure hardware pricing.

- ODM competition: broader choice

- Transparency: public benchmarks

- Buyer metrics: pixel pitch, nits, lifetime

- Mitigation: value-added services

Demand cyclicality and budgeting

Demand cyclicality gives buyers timing leverage in Daktronics' markets: advertising and sports capex is highly timing-sensitive, so downturns prompt project deferrals or requests for financing. Vendors often extend payment terms, pressuring cash flow, while flexible leasing wins deals but compresses margins; higher 2024 US policy rates (Fed funds 5.25–5.50%) raised financing costs for buyers and vendors alike.

- Capex sensitivity: buyers defer projects

- Extended terms: cash-flow strain on vendors

- Leasing: higher win-rate, lower margins

Buyers press >10% discounts; HTML5/IP lowers switching costs; Fed funds 5.25–5.50%

Major buyers (NFL avg attendance ~67,000; MLB ~29,000) wield strong price/SLAs leverage, forcing >10% discounts and strict uptime demands. HTML5/IP adoption in 2024 reduced switching costs, increasing competitive bids while Daktronics protects TCO-based pricing. Leasing and extended terms amid 2024 Fed funds 5.25–5.50% raise financing strain on vendors.

| Metric | 2024 |

|---|---|

| NFL avg attendance | ~67,000 |

| MLB avg attendance | ~29,000 |

| LED market size | $11.6B |

Preview Before You Purchase

Daktronics Porter's Five Forces Analysis

This preview shows the exact Daktronics Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual deliverable; once you complete your purchase you'll get instant access to this identical file.

From Overview to Strategy Blueprint

Daktronics faces moderate buyer power and supplier leverage, intense rivalry in signage/display markets, and a medium threat from substitutes and new entrants driven by tech shifts. Our snapshot highlights strategic vulnerabilities in pricing and innovation cadence. This brief overview hints at market pressures and growth levers. Unlock the full Porter's Five Forces Analysis to explore Daktronics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated LED components

High-brightness LEDs, drivers and controllers are sourced from a limited set of global suppliers—Nichia, Osram, Samsung and Seoul Semiconductor are among the largest in 2024—giving suppliers elevated pricing power and the potential to elongate lead times. Daktronics reports multi-sourcing and long-term agreements in its 2024 filings to mitigate risk, but substitution costs and qualification time remain non-trivial. Any supplier disruption directly delays production schedules and pressures margins.

Specialized materials and optics

Custom optics, weatherproof enclosures and thermal materials for Daktronics are specialized and often not interchangeable, creating supplier leverage; lead times commonly run 12–20 weeks and qualification cycles 6–18 months. Suppliers holding proprietary specs can negotiate favorable terms and command price premiums up to 15%, raising switching costs and impacting cost and delivery reliability.

Electronics and semiconductor cycles

Cyclical semiconductor tightness affects availability of controllers, ICs and power modules, with global semiconductor sales ~USD 580B in 2024 and lead times that surged in prior cycles still averaging 8–12 weeks for specialty parts. During shortages allocation typically favors large OEMs, pressuring mid-cap manufacturers like Daktronics. Price volatility can compress gross margins on fixed-price contracts, though strategic inventory and design flexibility partially offset exposure.

Logistics and large-format integration

Large-format LED screens require heavy logistics, structural components, and precise integration services, giving specialized freight carriers, fabricators, and installers leverage in project negotiations.

Limited regional alternatives increase client dependence, while bundled logistics contracts stabilize costs but lock customers into less flexible arrangements.

- supplier-concentration

- specialized-capabilities

- regional-dependence

- bundled-contracts-reduce-flexibility

Content and software partners

Third-party content tools, media processors and integrations add supplier touchpoints; in 2024 the global digital signage market exceeded $25 billion, increasing supplier influence. Platform certifications create soft lock-in; vendors levy premium support for mission-critical arenas. Building in-house software cuts vendor leverage but raises development and maintenance cost.

- Third-party touchpoints

- Soft lock-in via compatibility

- Premium mission-critical fees

- In-house reduces leverage, ups cost

Supplier concentration drives 8-20 week LED lead times and up to 15% pricing risk

Supplier concentration (Nichia, Osram, Samsung, Seoul) and specialized components give suppliers pricing and lead-time power; LED/driver lead times 8–20 weeks and qualification 6–18 months. Daktronics' 2024 multi-sourcing and long-term contracts reduce but do not eliminate 15% price-premium risk; semiconductor market ~USD 580B (2024), digital signage >USD 25B (2024).

| Metric | 2024 |

|---|---|

| Semiconductor sales | ~USD 580B |

| Digital signage market | >USD 25B |

| Lead times | 8–20 weeks |

| Price premium | up to 15% |

What is included in the product

Tailored Porter's Five Forces analysis for Daktronics that uncovers key drivers of competition, customer and supplier power, and market entry risks, while identifying disruptive substitutes and emerging threats to its market share. Includes strategic commentary on pricing influence, barriers protecting incumbents, and implications for Daktronics’ profitability and positioning.

A clear, one-sheet Porter's Five Forces summary for Daktronics—perfect for quick strategic decisions and investor briefings; customize force intensities based on new market data and swap in your own notes for immediate boardroom use.

Customers Bargaining Power

Concentrated marquee customers

Major sports leagues, stadiums and large DOOH networks are few and high-value; for context NFL average attendance is about 67,000 and MLB about 29,000 per game in recent seasons, amplifying their purchasing leverage. Their scale and visibility grant strong negotiating power on price and SLAs, and competitive bidding forces concessions. Losing a marquee deal can materially dent backlog and market signaling.

Professional procurement

Professional procurement for Daktronics-facing contracts runs detailed RFPs with strict specs and penalty clauses, and buyers routinely pit vendors to extract better commercial terms. Warranty scope, financing options, and uptime SLAs — often targeting 99.9% availability — become decisive levers. This sophistication drives discount pressure (commonly exceeding 10%) and higher ongoing service obligations.

Switching costs with legacy systems

Installed bases and proprietary control software create moderate switching costs for Daktronics customers, especially for stadium and transit integrations. In 2024, wider adoption of HTML5 content and IP-based signage protocols made retrofits and content portability easier, tempering vendor lock-in. Buyers often time replacements to capital cycles, raising bargaining power at refresh events. Strong service records and favorable TCO help Daktronics preserve pricing discipline.

Global options and transparency

Global options and transparency increase customer leverage: international rivals and ODMs expand choice while public case studies and benchmarks make comparisons easier. Buyers now push price cuts by benchmarking pixel pitch, nits and lifetime; the LED display market was estimated at about $11.6B in 2024, raising pressure on margins. Daktronics must bundle services to offset pure hardware pricing.

- ODM competition: broader choice

- Transparency: public benchmarks

- Buyer metrics: pixel pitch, nits, lifetime

- Mitigation: value-added services

Demand cyclicality and budgeting

Demand cyclicality gives buyers timing leverage in Daktronics' markets: advertising and sports capex is highly timing-sensitive, so downturns prompt project deferrals or requests for financing. Vendors often extend payment terms, pressuring cash flow, while flexible leasing wins deals but compresses margins; higher 2024 US policy rates (Fed funds 5.25–5.50%) raised financing costs for buyers and vendors alike.

- Capex sensitivity: buyers defer projects

- Extended terms: cash-flow strain on vendors

- Leasing: higher win-rate, lower margins

Buyers press >10% discounts; HTML5/IP lowers switching costs; Fed funds 5.25–5.50%

Major buyers (NFL avg attendance ~67,000; MLB ~29,000) wield strong price/SLAs leverage, forcing >10% discounts and strict uptime demands. HTML5/IP adoption in 2024 reduced switching costs, increasing competitive bids while Daktronics protects TCO-based pricing. Leasing and extended terms amid 2024 Fed funds 5.25–5.50% raise financing strain on vendors.

| Metric | 2024 |

|---|---|

| NFL avg attendance | ~67,000 |

| MLB avg attendance | ~29,000 |

| LED market size | $11.6B |

Preview Before You Purchase

Daktronics Porter's Five Forces Analysis

This preview shows the exact Daktronics Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual deliverable; once you complete your purchase you'll get instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Daktronics faces moderate buyer power and supplier leverage, intense rivalry in signage/display markets, and a medium threat from substitutes and new entrants driven by tech shifts. Our snapshot highlights strategic vulnerabilities in pricing and innovation cadence. This brief overview hints at market pressures and growth levers. Unlock the full Porter's Five Forces Analysis to explore Daktronics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated LED components

High-brightness LEDs, drivers and controllers are sourced from a limited set of global suppliers—Nichia, Osram, Samsung and Seoul Semiconductor are among the largest in 2024—giving suppliers elevated pricing power and the potential to elongate lead times. Daktronics reports multi-sourcing and long-term agreements in its 2024 filings to mitigate risk, but substitution costs and qualification time remain non-trivial. Any supplier disruption directly delays production schedules and pressures margins.

Specialized materials and optics

Custom optics, weatherproof enclosures and thermal materials for Daktronics are specialized and often not interchangeable, creating supplier leverage; lead times commonly run 12–20 weeks and qualification cycles 6–18 months. Suppliers holding proprietary specs can negotiate favorable terms and command price premiums up to 15%, raising switching costs and impacting cost and delivery reliability.

Electronics and semiconductor cycles

Cyclical semiconductor tightness affects availability of controllers, ICs and power modules, with global semiconductor sales ~USD 580B in 2024 and lead times that surged in prior cycles still averaging 8–12 weeks for specialty parts. During shortages allocation typically favors large OEMs, pressuring mid-cap manufacturers like Daktronics. Price volatility can compress gross margins on fixed-price contracts, though strategic inventory and design flexibility partially offset exposure.

Logistics and large-format integration

Large-format LED screens require heavy logistics, structural components, and precise integration services, giving specialized freight carriers, fabricators, and installers leverage in project negotiations.

Limited regional alternatives increase client dependence, while bundled logistics contracts stabilize costs but lock customers into less flexible arrangements.

- supplier-concentration

- specialized-capabilities

- regional-dependence

- bundled-contracts-reduce-flexibility

Content and software partners

Third-party content tools, media processors and integrations add supplier touchpoints; in 2024 the global digital signage market exceeded $25 billion, increasing supplier influence. Platform certifications create soft lock-in; vendors levy premium support for mission-critical arenas. Building in-house software cuts vendor leverage but raises development and maintenance cost.

- Third-party touchpoints

- Soft lock-in via compatibility

- Premium mission-critical fees

- In-house reduces leverage, ups cost

Supplier concentration drives 8-20 week LED lead times and up to 15% pricing risk

Supplier concentration (Nichia, Osram, Samsung, Seoul) and specialized components give suppliers pricing and lead-time power; LED/driver lead times 8–20 weeks and qualification 6–18 months. Daktronics' 2024 multi-sourcing and long-term contracts reduce but do not eliminate 15% price-premium risk; semiconductor market ~USD 580B (2024), digital signage >USD 25B (2024).

| Metric | 2024 |

|---|---|

| Semiconductor sales | ~USD 580B |

| Digital signage market | >USD 25B |

| Lead times | 8–20 weeks |

| Price premium | up to 15% |

What is included in the product

Tailored Porter's Five Forces analysis for Daktronics that uncovers key drivers of competition, customer and supplier power, and market entry risks, while identifying disruptive substitutes and emerging threats to its market share. Includes strategic commentary on pricing influence, barriers protecting incumbents, and implications for Daktronics’ profitability and positioning.

A clear, one-sheet Porter's Five Forces summary for Daktronics—perfect for quick strategic decisions and investor briefings; customize force intensities based on new market data and swap in your own notes for immediate boardroom use.

Customers Bargaining Power

Concentrated marquee customers

Major sports leagues, stadiums and large DOOH networks are few and high-value; for context NFL average attendance is about 67,000 and MLB about 29,000 per game in recent seasons, amplifying their purchasing leverage. Their scale and visibility grant strong negotiating power on price and SLAs, and competitive bidding forces concessions. Losing a marquee deal can materially dent backlog and market signaling.

Professional procurement

Professional procurement for Daktronics-facing contracts runs detailed RFPs with strict specs and penalty clauses, and buyers routinely pit vendors to extract better commercial terms. Warranty scope, financing options, and uptime SLAs — often targeting 99.9% availability — become decisive levers. This sophistication drives discount pressure (commonly exceeding 10%) and higher ongoing service obligations.

Switching costs with legacy systems

Installed bases and proprietary control software create moderate switching costs for Daktronics customers, especially for stadium and transit integrations. In 2024, wider adoption of HTML5 content and IP-based signage protocols made retrofits and content portability easier, tempering vendor lock-in. Buyers often time replacements to capital cycles, raising bargaining power at refresh events. Strong service records and favorable TCO help Daktronics preserve pricing discipline.

Global options and transparency

Global options and transparency increase customer leverage: international rivals and ODMs expand choice while public case studies and benchmarks make comparisons easier. Buyers now push price cuts by benchmarking pixel pitch, nits and lifetime; the LED display market was estimated at about $11.6B in 2024, raising pressure on margins. Daktronics must bundle services to offset pure hardware pricing.

- ODM competition: broader choice

- Transparency: public benchmarks

- Buyer metrics: pixel pitch, nits, lifetime

- Mitigation: value-added services

Demand cyclicality and budgeting

Demand cyclicality gives buyers timing leverage in Daktronics' markets: advertising and sports capex is highly timing-sensitive, so downturns prompt project deferrals or requests for financing. Vendors often extend payment terms, pressuring cash flow, while flexible leasing wins deals but compresses margins; higher 2024 US policy rates (Fed funds 5.25–5.50%) raised financing costs for buyers and vendors alike.

- Capex sensitivity: buyers defer projects

- Extended terms: cash-flow strain on vendors

- Leasing: higher win-rate, lower margins

Buyers press >10% discounts; HTML5/IP lowers switching costs; Fed funds 5.25–5.50%

Major buyers (NFL avg attendance ~67,000; MLB ~29,000) wield strong price/SLAs leverage, forcing >10% discounts and strict uptime demands. HTML5/IP adoption in 2024 reduced switching costs, increasing competitive bids while Daktronics protects TCO-based pricing. Leasing and extended terms amid 2024 Fed funds 5.25–5.50% raise financing strain on vendors.

| Metric | 2024 |

|---|---|

| NFL avg attendance | ~67,000 |

| MLB avg attendance | ~29,000 |

| LED market size | $11.6B |

Preview Before You Purchase

Daktronics Porter's Five Forces Analysis

This preview shows the exact Daktronics Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You're looking at the actual deliverable; once you complete your purchase you'll get instant access to this identical file.