Dalipal Pipe Co. Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Dalipal Pipe Co. faces moderate buyer power and raw-material-driven supplier leverage, while industry rivalry is intensified by price competition and capacity expansion. Barriers to entry are mixed—steady capex but niche technical know-how limits newcomers. Substitute threats are moderate given alternatives in piping materials. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Dalipal Pipe Co.’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated steel and alloy inputs

Seamless OCTG depends on high-grade billets and alloying Ni, Mo, Cr from concentrated upstreams—China produced ~56% of global crude steel in 2023 and Indonesia supplied ~38% of mined nickel in 2023—so disruptions or price spikes transmit directly to margins. Dalipal can mitigate via multi-sourcing and long-term contracts, but strict quality specs limit supplier flexibility. EU CBAM and low‑carbon steel incentives further narrow eligible suppliers.

Energy and utilities intensity

Hot rolling, heat treatment and finishing tie Dalipal Pipe Co. margins to electricity and gas suppliers, with energy often representing 15–25% of steel/pipe production costs in 2024. Volatile industrial power prices in 2024 (roughly $0.06–0.22/kWh across major regions) can erode margins quickly. Green manufacturing commitments may force premium PPAs, typically 10–20% above spot grid rates. Regional energy policies and subsidies shift suppliers’ bargaining leverage.

Critical equipment and spares

Dependence on specialized piercers, mandrel mills, heat-treatment furnaces and premium-threading machines gives OEMs outsized bargaining power, with proprietary spares and fixed maintenance cycles creating strong switching frictions; industry lead times of 6–12 months for replacement capital and spares in 2024 further constrain capacity planning. Predictive maintenance can cut unplanned downtime by up to 40% but does not eliminate supplier leverage.

Digital and consumable dependencies

- High license/service fees

- Consumables spec-bound

- Qualification reduces substitutes

- Bundled contracts increase lock-in

Logistics and raw material timing

Seamless pipes and billets are bulky, making freight a meaningful cost component, often accounting for 5–15% of delivered mill price in 2024; port congestion and limited rail/truck capacity give logistics providers situational leverage, with some major ports reporting on-time berthing near 80% in 2024. Just-in-time programs heighten exposure to delays, while strategic inventory buffers (weeks of cover) materially reduce carriers’ bargaining power.

- Freight share: 5–15%

- Port on-time berthing: ~80% (2024)

- JIT exposure: higher delay risk

- Inventory buffers: lower carrier leverage

OCTG margins exposed to China/Indonesia input shocks, energy premiums and NDT frictions

Seamless OCTG raw inputs concentrated: China ~56% of crude steel (2023) and Indonesia ~38% of mined nickel (2023), so input shocks transmit to margins. Energy costs represent ~15–25% of production (2024) and VPPAs add 10–20% premiums. Specialized equipment, NDT and consumables (NDT market ~USD13.8B; sensors ~USD64B in 2024) create switching frictions.

| Metric | Value |

|---|---|

| China share crude steel (2023) | ~56% |

| Indonesia nickel (2023) | ~38% |

| Energy cost share (2024) | 15–25% |

| Freight of delivered price (2024) | 5–15% |

| NDT market (2024) | USD13.8B |

What is included in the product

Tailored Porter's Five Forces analysis for Dalipal Pipe Co. uncovering key drivers of competition, buyer and supplier power, substitute risks, and entry barriers, with strategic commentary on disruptive threats and market dynamics that influence its pricing and profitability.

One-sheet Porter's Five Forces for Dalipal Pipe Co.—instantly spot supplier, buyer, entrant, substitute and rivalry pressures with a clean spider chart and customizable scores, ready for decks or Excel dashboards; no macros, swap in your data to model pre/post-regulation scenarios and relieve strategic decision-making pain points.

Customers Bargaining Power

Large oil and gas buyers

OCTG buyers are predominantly majors, national oil companies, and large drillers with centralized, sophisticated procurement teams, using competitive tenders and framework agreements that amplify their bargaining power. Their scale and multiyear volume visibility enable them to secure significant pricing leverage once suppliers clear stringent qualification barriers. Qualification reduces supplier pool but intensifies price pressure and demands for delivery, quality and warranty concessions.

Specification-driven switching costs

API/ISO and premium-connection qualifications create moderate switching costs for Dalipal Pipe Co., raising technical barriers and qualification lead times. Approved vendor lists typically include 3–5 suppliers, sustaining price competition as buyers often dual-source to retain leverage. Field performance data that demonstrates lower lifecycle costs can entrench suppliers that deliver measurably lower TCO.

Cyclical demand volatility

OCTG demand tracks rig counts and energy capex cycles — Baker Hughes showed global rig counts swung roughly 20% across 2022–24, amplifying buyer leverage in downturns as OEMs face excess inventory. In upcycles tight mill and threading capacity can flip leverage to suppliers; IEA data showed upstream investment volatility with a ~4% decline in 2024. Dalipal’s growing exposure to new-energy pipes (renewables/H2) may smooth cycles slightly, while buyers increasingly push index-linked steel pricing.

Service bundling expectations

Integrated services—R&D support, threading, inspection and running—are now baseline expectations, with 2024 industry surveys showing about 62% of large buyers preferring bundled contracts; buyers negotiate total cost of ownership rather than unit price, reducing per-unit bargaining but increasing leverage over scope and SLAs. Superior technical support and differentiated engineering reduce buyer leverage by creating switching costs, while performance guarantees and uptime SLAs shift risk back to suppliers, tightening margins.

- Bundling preference: 62% (2024 survey)

- Bundled contract growth: +18% YoY (2024)

- Key levers: scope negotiation, SLA risk transfer

- Supplier defense: technical differentiation, performance guarantees

Sustainability and traceability demands

ESG policies push buyers toward low‑emission steel and traceable supply chains; many public tenders in 2024 require EPDs and lifecycle data, letting purchasers demand green premiums yet still negotiate price. Market reports in 2024 cite green premiums around 10–15%; non‑compliance can disqualify bidders while Dalipal’s green manufacturing helps defend margins.

- EPDs required in 2024 tenders

- Green premium ~10–15%

- Non‑compliance = disqualification

- Green positioning = margin defense

Tender buyers tilt deals; bundling 62%, green premium 10–15%

Large, centralized OCTG buyers (majors, NOCs, big drillers) exert high price and SLA leverage via tenders and 3–5 approved suppliers, intensified by qualification barriers. 2024 trends—62% bundling preference, 10–15% green premium, ~20% rig-count swings—shift negotiations toward TCO and scope. Dalipal’s technical differentiation and EPDs reduce buyer power by raising switching costs.

| Metric | 2024 |

|---|---|

| Approved suppliers | 3–5 |

| Bundling preference | 62% |

| Green premium | 10–15% |

| Rig-count volatility | ~20% |

Full Version Awaits

Dalipal Pipe Co. Porter's Five Forces Analysis

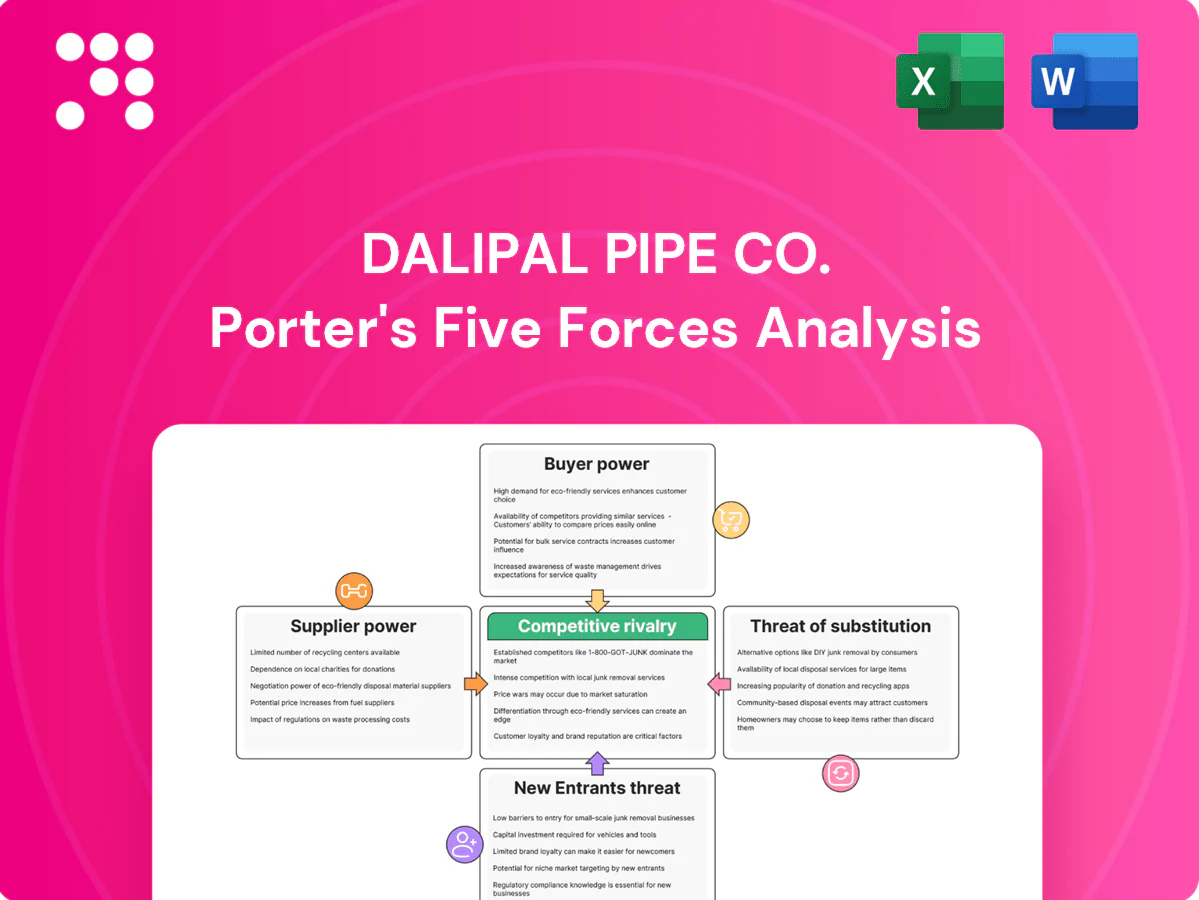

This Porter's Five Forces analysis for Dalipal Pipe Co. evaluates competitive rivalry, bargaining power of suppliers and buyers, threat of substitutes, and barriers to entry, offering strategic insights and data-driven recommendations to guide investment and business decisions. The document shown is the exact, fully formatted file you’ll receive instantly after purchase—no samples, no placeholders, ready for immediate use.

Go Beyond the Preview—Access the Full Strategic Report

Dalipal Pipe Co. faces moderate buyer power and raw-material-driven supplier leverage, while industry rivalry is intensified by price competition and capacity expansion. Barriers to entry are mixed—steady capex but niche technical know-how limits newcomers. Substitute threats are moderate given alternatives in piping materials. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Dalipal Pipe Co.’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated steel and alloy inputs

Seamless OCTG depends on high-grade billets and alloying Ni, Mo, Cr from concentrated upstreams—China produced ~56% of global crude steel in 2023 and Indonesia supplied ~38% of mined nickel in 2023—so disruptions or price spikes transmit directly to margins. Dalipal can mitigate via multi-sourcing and long-term contracts, but strict quality specs limit supplier flexibility. EU CBAM and low‑carbon steel incentives further narrow eligible suppliers.

Energy and utilities intensity

Hot rolling, heat treatment and finishing tie Dalipal Pipe Co. margins to electricity and gas suppliers, with energy often representing 15–25% of steel/pipe production costs in 2024. Volatile industrial power prices in 2024 (roughly $0.06–0.22/kWh across major regions) can erode margins quickly. Green manufacturing commitments may force premium PPAs, typically 10–20% above spot grid rates. Regional energy policies and subsidies shift suppliers’ bargaining leverage.

Critical equipment and spares

Dependence on specialized piercers, mandrel mills, heat-treatment furnaces and premium-threading machines gives OEMs outsized bargaining power, with proprietary spares and fixed maintenance cycles creating strong switching frictions; industry lead times of 6–12 months for replacement capital and spares in 2024 further constrain capacity planning. Predictive maintenance can cut unplanned downtime by up to 40% but does not eliminate supplier leverage.

Digital and consumable dependencies

- High license/service fees

- Consumables spec-bound

- Qualification reduces substitutes

- Bundled contracts increase lock-in

Logistics and raw material timing

Seamless pipes and billets are bulky, making freight a meaningful cost component, often accounting for 5–15% of delivered mill price in 2024; port congestion and limited rail/truck capacity give logistics providers situational leverage, with some major ports reporting on-time berthing near 80% in 2024. Just-in-time programs heighten exposure to delays, while strategic inventory buffers (weeks of cover) materially reduce carriers’ bargaining power.

- Freight share: 5–15%

- Port on-time berthing: ~80% (2024)

- JIT exposure: higher delay risk

- Inventory buffers: lower carrier leverage

OCTG margins exposed to China/Indonesia input shocks, energy premiums and NDT frictions

Seamless OCTG raw inputs concentrated: China ~56% of crude steel (2023) and Indonesia ~38% of mined nickel (2023), so input shocks transmit to margins. Energy costs represent ~15–25% of production (2024) and VPPAs add 10–20% premiums. Specialized equipment, NDT and consumables (NDT market ~USD13.8B; sensors ~USD64B in 2024) create switching frictions.

| Metric | Value |

|---|---|

| China share crude steel (2023) | ~56% |

| Indonesia nickel (2023) | ~38% |

| Energy cost share (2024) | 15–25% |

| Freight of delivered price (2024) | 5–15% |

| NDT market (2024) | USD13.8B |

What is included in the product

Tailored Porter's Five Forces analysis for Dalipal Pipe Co. uncovering key drivers of competition, buyer and supplier power, substitute risks, and entry barriers, with strategic commentary on disruptive threats and market dynamics that influence its pricing and profitability.

One-sheet Porter's Five Forces for Dalipal Pipe Co.—instantly spot supplier, buyer, entrant, substitute and rivalry pressures with a clean spider chart and customizable scores, ready for decks or Excel dashboards; no macros, swap in your data to model pre/post-regulation scenarios and relieve strategic decision-making pain points.

Customers Bargaining Power

Large oil and gas buyers

OCTG buyers are predominantly majors, national oil companies, and large drillers with centralized, sophisticated procurement teams, using competitive tenders and framework agreements that amplify their bargaining power. Their scale and multiyear volume visibility enable them to secure significant pricing leverage once suppliers clear stringent qualification barriers. Qualification reduces supplier pool but intensifies price pressure and demands for delivery, quality and warranty concessions.

Specification-driven switching costs

API/ISO and premium-connection qualifications create moderate switching costs for Dalipal Pipe Co., raising technical barriers and qualification lead times. Approved vendor lists typically include 3–5 suppliers, sustaining price competition as buyers often dual-source to retain leverage. Field performance data that demonstrates lower lifecycle costs can entrench suppliers that deliver measurably lower TCO.

Cyclical demand volatility

OCTG demand tracks rig counts and energy capex cycles — Baker Hughes showed global rig counts swung roughly 20% across 2022–24, amplifying buyer leverage in downturns as OEMs face excess inventory. In upcycles tight mill and threading capacity can flip leverage to suppliers; IEA data showed upstream investment volatility with a ~4% decline in 2024. Dalipal’s growing exposure to new-energy pipes (renewables/H2) may smooth cycles slightly, while buyers increasingly push index-linked steel pricing.

Service bundling expectations

Integrated services—R&D support, threading, inspection and running—are now baseline expectations, with 2024 industry surveys showing about 62% of large buyers preferring bundled contracts; buyers negotiate total cost of ownership rather than unit price, reducing per-unit bargaining but increasing leverage over scope and SLAs. Superior technical support and differentiated engineering reduce buyer leverage by creating switching costs, while performance guarantees and uptime SLAs shift risk back to suppliers, tightening margins.

- Bundling preference: 62% (2024 survey)

- Bundled contract growth: +18% YoY (2024)

- Key levers: scope negotiation, SLA risk transfer

- Supplier defense: technical differentiation, performance guarantees

Sustainability and traceability demands

ESG policies push buyers toward low‑emission steel and traceable supply chains; many public tenders in 2024 require EPDs and lifecycle data, letting purchasers demand green premiums yet still negotiate price. Market reports in 2024 cite green premiums around 10–15%; non‑compliance can disqualify bidders while Dalipal’s green manufacturing helps defend margins.

- EPDs required in 2024 tenders

- Green premium ~10–15%

- Non‑compliance = disqualification

- Green positioning = margin defense

Tender buyers tilt deals; bundling 62%, green premium 10–15%

Large, centralized OCTG buyers (majors, NOCs, big drillers) exert high price and SLA leverage via tenders and 3–5 approved suppliers, intensified by qualification barriers. 2024 trends—62% bundling preference, 10–15% green premium, ~20% rig-count swings—shift negotiations toward TCO and scope. Dalipal’s technical differentiation and EPDs reduce buyer power by raising switching costs.

| Metric | 2024 |

|---|---|

| Approved suppliers | 3–5 |

| Bundling preference | 62% |

| Green premium | 10–15% |

| Rig-count volatility | ~20% |

Full Version Awaits

Dalipal Pipe Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis for Dalipal Pipe Co. evaluates competitive rivalry, bargaining power of suppliers and buyers, threat of substitutes, and barriers to entry, offering strategic insights and data-driven recommendations to guide investment and business decisions. The document shown is the exact, fully formatted file you’ll receive instantly after purchase—no samples, no placeholders, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Dalipal Pipe Co. faces moderate buyer power and raw-material-driven supplier leverage, while industry rivalry is intensified by price competition and capacity expansion. Barriers to entry are mixed—steady capex but niche technical know-how limits newcomers. Substitute threats are moderate given alternatives in piping materials. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Dalipal Pipe Co.’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated steel and alloy inputs

Seamless OCTG depends on high-grade billets and alloying Ni, Mo, Cr from concentrated upstreams—China produced ~56% of global crude steel in 2023 and Indonesia supplied ~38% of mined nickel in 2023—so disruptions or price spikes transmit directly to margins. Dalipal can mitigate via multi-sourcing and long-term contracts, but strict quality specs limit supplier flexibility. EU CBAM and low‑carbon steel incentives further narrow eligible suppliers.

Energy and utilities intensity

Hot rolling, heat treatment and finishing tie Dalipal Pipe Co. margins to electricity and gas suppliers, with energy often representing 15–25% of steel/pipe production costs in 2024. Volatile industrial power prices in 2024 (roughly $0.06–0.22/kWh across major regions) can erode margins quickly. Green manufacturing commitments may force premium PPAs, typically 10–20% above spot grid rates. Regional energy policies and subsidies shift suppliers’ bargaining leverage.

Critical equipment and spares

Dependence on specialized piercers, mandrel mills, heat-treatment furnaces and premium-threading machines gives OEMs outsized bargaining power, with proprietary spares and fixed maintenance cycles creating strong switching frictions; industry lead times of 6–12 months for replacement capital and spares in 2024 further constrain capacity planning. Predictive maintenance can cut unplanned downtime by up to 40% but does not eliminate supplier leverage.

Digital and consumable dependencies

- High license/service fees

- Consumables spec-bound

- Qualification reduces substitutes

- Bundled contracts increase lock-in

Logistics and raw material timing

Seamless pipes and billets are bulky, making freight a meaningful cost component, often accounting for 5–15% of delivered mill price in 2024; port congestion and limited rail/truck capacity give logistics providers situational leverage, with some major ports reporting on-time berthing near 80% in 2024. Just-in-time programs heighten exposure to delays, while strategic inventory buffers (weeks of cover) materially reduce carriers’ bargaining power.

- Freight share: 5–15%

- Port on-time berthing: ~80% (2024)

- JIT exposure: higher delay risk

- Inventory buffers: lower carrier leverage

OCTG margins exposed to China/Indonesia input shocks, energy premiums and NDT frictions

Seamless OCTG raw inputs concentrated: China ~56% of crude steel (2023) and Indonesia ~38% of mined nickel (2023), so input shocks transmit to margins. Energy costs represent ~15–25% of production (2024) and VPPAs add 10–20% premiums. Specialized equipment, NDT and consumables (NDT market ~USD13.8B; sensors ~USD64B in 2024) create switching frictions.

| Metric | Value |

|---|---|

| China share crude steel (2023) | ~56% |

| Indonesia nickel (2023) | ~38% |

| Energy cost share (2024) | 15–25% |

| Freight of delivered price (2024) | 5–15% |

| NDT market (2024) | USD13.8B |

What is included in the product

Tailored Porter's Five Forces analysis for Dalipal Pipe Co. uncovering key drivers of competition, buyer and supplier power, substitute risks, and entry barriers, with strategic commentary on disruptive threats and market dynamics that influence its pricing and profitability.

One-sheet Porter's Five Forces for Dalipal Pipe Co.—instantly spot supplier, buyer, entrant, substitute and rivalry pressures with a clean spider chart and customizable scores, ready for decks or Excel dashboards; no macros, swap in your data to model pre/post-regulation scenarios and relieve strategic decision-making pain points.

Customers Bargaining Power

Large oil and gas buyers

OCTG buyers are predominantly majors, national oil companies, and large drillers with centralized, sophisticated procurement teams, using competitive tenders and framework agreements that amplify their bargaining power. Their scale and multiyear volume visibility enable them to secure significant pricing leverage once suppliers clear stringent qualification barriers. Qualification reduces supplier pool but intensifies price pressure and demands for delivery, quality and warranty concessions.

Specification-driven switching costs

API/ISO and premium-connection qualifications create moderate switching costs for Dalipal Pipe Co., raising technical barriers and qualification lead times. Approved vendor lists typically include 3–5 suppliers, sustaining price competition as buyers often dual-source to retain leverage. Field performance data that demonstrates lower lifecycle costs can entrench suppliers that deliver measurably lower TCO.

Cyclical demand volatility

OCTG demand tracks rig counts and energy capex cycles — Baker Hughes showed global rig counts swung roughly 20% across 2022–24, amplifying buyer leverage in downturns as OEMs face excess inventory. In upcycles tight mill and threading capacity can flip leverage to suppliers; IEA data showed upstream investment volatility with a ~4% decline in 2024. Dalipal’s growing exposure to new-energy pipes (renewables/H2) may smooth cycles slightly, while buyers increasingly push index-linked steel pricing.

Service bundling expectations

Integrated services—R&D support, threading, inspection and running—are now baseline expectations, with 2024 industry surveys showing about 62% of large buyers preferring bundled contracts; buyers negotiate total cost of ownership rather than unit price, reducing per-unit bargaining but increasing leverage over scope and SLAs. Superior technical support and differentiated engineering reduce buyer leverage by creating switching costs, while performance guarantees and uptime SLAs shift risk back to suppliers, tightening margins.

- Bundling preference: 62% (2024 survey)

- Bundled contract growth: +18% YoY (2024)

- Key levers: scope negotiation, SLA risk transfer

- Supplier defense: technical differentiation, performance guarantees

Sustainability and traceability demands

ESG policies push buyers toward low‑emission steel and traceable supply chains; many public tenders in 2024 require EPDs and lifecycle data, letting purchasers demand green premiums yet still negotiate price. Market reports in 2024 cite green premiums around 10–15%; non‑compliance can disqualify bidders while Dalipal’s green manufacturing helps defend margins.

- EPDs required in 2024 tenders

- Green premium ~10–15%

- Non‑compliance = disqualification

- Green positioning = margin defense

Tender buyers tilt deals; bundling 62%, green premium 10–15%

Large, centralized OCTG buyers (majors, NOCs, big drillers) exert high price and SLA leverage via tenders and 3–5 approved suppliers, intensified by qualification barriers. 2024 trends—62% bundling preference, 10–15% green premium, ~20% rig-count swings—shift negotiations toward TCO and scope. Dalipal’s technical differentiation and EPDs reduce buyer power by raising switching costs.

| Metric | 2024 |

|---|---|

| Approved suppliers | 3–5 |

| Bundling preference | 62% |

| Green premium | 10–15% |

| Rig-count volatility | ~20% |

Full Version Awaits

Dalipal Pipe Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis for Dalipal Pipe Co. evaluates competitive rivalry, bargaining power of suppliers and buyers, threat of substitutes, and barriers to entry, offering strategic insights and data-driven recommendations to guide investment and business decisions. The document shown is the exact, fully formatted file you’ll receive instantly after purchase—no samples, no placeholders, ready for immediate use.