Davis Polk & Wardwell Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

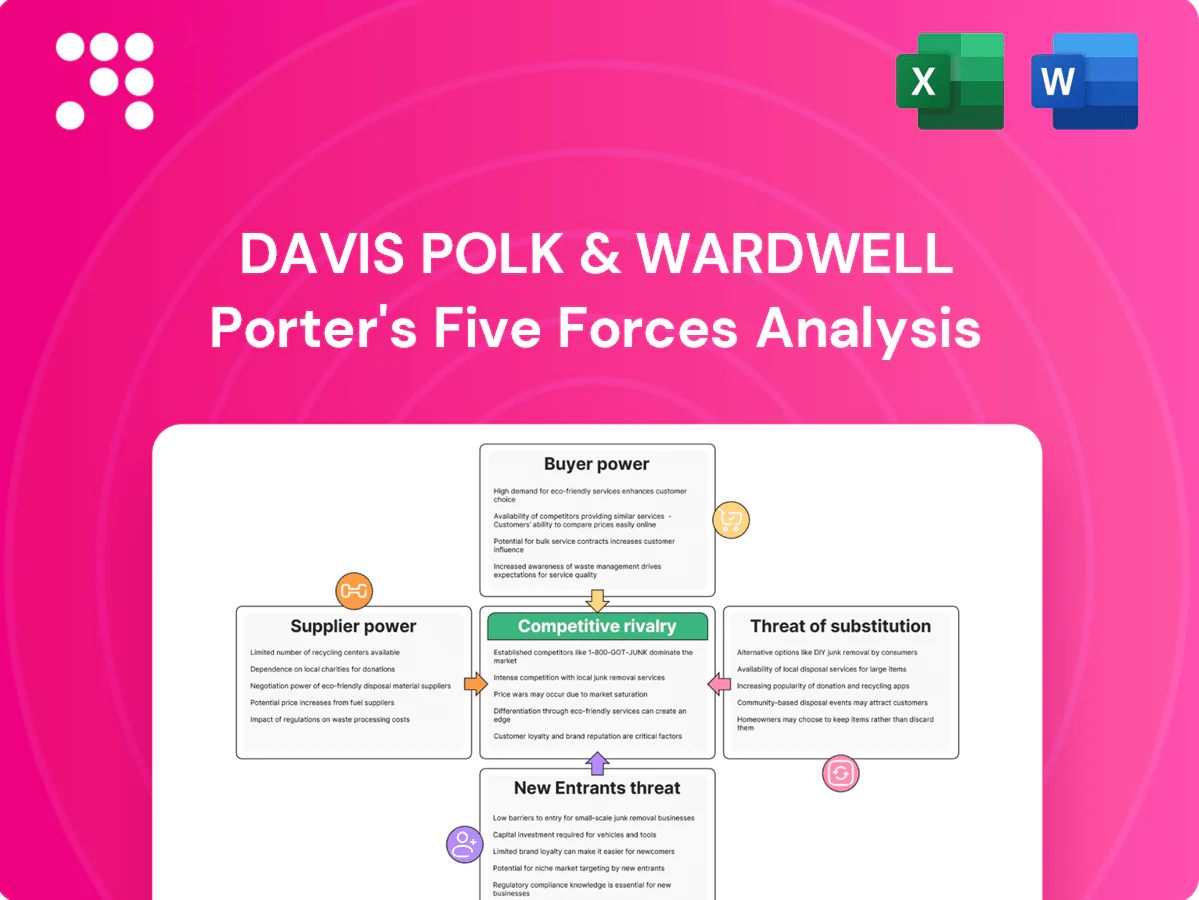

Davis Polk & Wardwell operates in a high-stakes legal market where partner loyalties, boutique rivals, client bargaining power, regulatory shifts, and substitute advisory services shape profitability. Our snapshot highlights key competitive pressures and strategic levers for growth. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Davis Polk & Wardwell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Elite legal talent scarcity

Star partners and senior associates are the critical input for Davis Polk; top-tier lawyers command seven-figure compensation at the partner level and remain scarce and mobile in 2024, boosting supplier leverage.

Lateral markets and compensation wars keep bargaining power high as firms compete for rainmakers and origination-heavy talent.

Mitigation requires elevated spending on retention, training, and culture; in cyclical upswings or hot practices supplier power intensifies further.

Information and research oligopoly

Legal databases such as Westlaw and Lexis dominate the market, supplying the majority of primary-source and analytics access and granting them significant pricing power. Enterprise subscriptions and integration needs create high switching costs—large firms often incur six-figure annual spend on research platforms. Volume discounts mitigate per-user cost, but limited alternatives and new AI-license fees (added in 2023–24) have reinforced vendor leverage.

Technology and infrastructure vendors

Cloud, e‑discovery ($5.8B market in 2024), cybersecurity (global spend ~$207B in 2024) and collaboration platforms are mission‑critical for Davis Polk, concentrating supplier power: AWS (31%), Azure (23%) and GCP (11%) in 2024 narrow viable choices and boost vendor leverage. Long implementations and data residency rules create client lock‑in, while premium support and strict uptime SLAs command measurable cost premiums.

Expert, local counsel, and niche providers

Complex cross-border matters routinely require local counsel, expert witnesses, and specialist boutiques; in 2024 market reports detail rising demand and fee premiums in constrained jurisdictions. Limited court calendars and tight timelines reduce negotiation room, and deep firm relationships lower but do not eliminate supplier leverage.

- High reliance on niche providers

- Fee premiums in constrained jurisdictions

- Calendars limit bargaining

- Relationships mitigate but not remove leverage

Real estate and professional services

- Landlords: high rent pressure (~$80/sq ft)

- Vendors: court reporting $100–200/hr; recruiting 20–30% fees

- Hybrid: ~25–30% lower utilization

- Contracts: multi-year terms reduce negotiation leverage

Scarce top legal talent; partners earn seven-figure; cloud market 31/23/11; e-discovery $5.8B

Top legal talent is scarce and mobile, with partner compensation often seven‑figure in 2024, keeping supplier leverage high. Research vendors and cloud providers concentrate pricing power (Westlaw/Lexis dominant; AWS 31%, Azure 23%, GCP 11% in 2024). Critical services (e‑discovery $5.8B, cybersecurity ~$207B, NYC/Wash rent ~$80/sq ft, recruiting fees 20–30%) raise switching costs and lock‑in.

| Supplier | Metric | 2024 |

|---|---|---|

| Legal talent | Partner pay | Seven‑figure |

| Cloud | Market share | AWS 31% / Azure 23% / GCP 11% |

| e‑discovery | Market size | $5.8B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Davis Polk & Wardwell, uncovering competitive intensity, client and supplier bargaining power, threat of entrants and substitutes, and regulatory dynamics shaping profitability and strategic positioning.

Ready-to-use Davis Polk & Wardwell Porter's Five Forces one-sheet—condenses competitive pressure into a clear visual so teams make faster, confident strategic decisions.

Customers Bargaining Power

Institutional clients with scale

Global corporates, financial institutions and governments purchase large recurring services from Davis Polk, running competitive RFPs, panel counsel reviews and strict billing guidelines. Their scale and brand prestige translate into leverage on rates, staffing and indemnities, with 2024 industry surveys citing average negotiated fee concessions of roughly 15–25%. Consolidation onto preferred panels amplifies this bargaining power across mandates.

High stakes, high switching costs

For bet-the-company matters clients face substantial switching costs driven by entrenched trust, proprietary knowledge, and strict confidentiality, so Davis Polk’s engagement economics allow premium pricing when outcomes are critical. Clients routinely accept higher fees for reduced execution risk; in complex M&A and capital markets work premium fees are common. Conflicts and regulatory constraints further narrow buyer options, moderating customer bargaining power despite scale.

Alternative fee pressure

Buyers increasingly demand AFAs, budget caps and transparency; by 2024 roughly 60% of corporate legal teams reported using alternative fee arrangements, shifting fee volatility to firms. Matter-based pricing and success fees transfer risk and compress realized rates, while sophisticated legal ops use KPIs and SLAs to enforce compliance. This tightens margins and raises buyer leverage, especially in repeatable, high-volume work.

Segmented price sensitivity

Segmented price sensitivity: commodity or process-heavy tasks at Davis Polk face intense price competition, while premium advisory and novel transactions sustain higher pricing and margins in 2024; buyers increasingly unbundle routine work to ALSPs or in-house, raising buyer power on lower-value layers.

- Commodity tasks: high price pressure

- Premium deals: strong pricing

- Unbundling to ALSPs/in-house: increases buyer leverage

Cyclicality and deal flow

In downturns buyers defer transactions and push fee renegotiations, while spikes in distressed and regulatory mandates — which rose notably in 2024 as restructuring activity increased — partially offset revenue pressure but do not fully neutralize bargaining power. In boom cycles urgency around deals reduces buyer leverage in core practices, shifting effective buyer power with the demand mix. The cyclicality thus creates material swings in negotiated terms over time.

- 2024: restructuring and regulatory work share rose relative to peak-deal practices

- Buyer leverage increases in market slowdowns

- Urgency in booms compresses buyer bargaining power

Buyers force 15–25% concessions; ~60% use AFAs, premium holds for high-stakes

Large corporates, financial institutions and governments exercise strong leverage on Davis Polk over rates, staffing and indemnities, driving typical negotiated fee concessions of 15–25% in 2024. High-stakes mandates retain premium pricing due to switching costs and confidentiality, while ~60% of corporate legal teams used AFAs in 2024, increasing buyer push for fixed fees and KPIs. Cyclical shifts (rise in 2024 restructuring/regulatory work) partially offset but do not eliminate buyer power.

| Metric | 2024 |

|---|---|

| Avg fee concessions | 15–25% |

| Corporate teams on AFAs | ~60% |

| Restructuring/regulatory share | ↑ vs peak-deal era |

Full Version Awaits

Davis Polk & Wardwell Porter's Five Forces Analysis

This preview shows the exact Davis Polk & Wardwell Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The analysis is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the complete, final file as shown, with instant access upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Davis Polk & Wardwell operates in a high-stakes legal market where partner loyalties, boutique rivals, client bargaining power, regulatory shifts, and substitute advisory services shape profitability. Our snapshot highlights key competitive pressures and strategic levers for growth. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Davis Polk & Wardwell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Elite legal talent scarcity

Star partners and senior associates are the critical input for Davis Polk; top-tier lawyers command seven-figure compensation at the partner level and remain scarce and mobile in 2024, boosting supplier leverage.

Lateral markets and compensation wars keep bargaining power high as firms compete for rainmakers and origination-heavy talent.

Mitigation requires elevated spending on retention, training, and culture; in cyclical upswings or hot practices supplier power intensifies further.

Information and research oligopoly

Legal databases such as Westlaw and Lexis dominate the market, supplying the majority of primary-source and analytics access and granting them significant pricing power. Enterprise subscriptions and integration needs create high switching costs—large firms often incur six-figure annual spend on research platforms. Volume discounts mitigate per-user cost, but limited alternatives and new AI-license fees (added in 2023–24) have reinforced vendor leverage.

Technology and infrastructure vendors

Cloud, e‑discovery ($5.8B market in 2024), cybersecurity (global spend ~$207B in 2024) and collaboration platforms are mission‑critical for Davis Polk, concentrating supplier power: AWS (31%), Azure (23%) and GCP (11%) in 2024 narrow viable choices and boost vendor leverage. Long implementations and data residency rules create client lock‑in, while premium support and strict uptime SLAs command measurable cost premiums.

Expert, local counsel, and niche providers

Complex cross-border matters routinely require local counsel, expert witnesses, and specialist boutiques; in 2024 market reports detail rising demand and fee premiums in constrained jurisdictions. Limited court calendars and tight timelines reduce negotiation room, and deep firm relationships lower but do not eliminate supplier leverage.

- High reliance on niche providers

- Fee premiums in constrained jurisdictions

- Calendars limit bargaining

- Relationships mitigate but not remove leverage

Real estate and professional services

- Landlords: high rent pressure (~$80/sq ft)

- Vendors: court reporting $100–200/hr; recruiting 20–30% fees

- Hybrid: ~25–30% lower utilization

- Contracts: multi-year terms reduce negotiation leverage

Scarce top legal talent; partners earn seven-figure; cloud market 31/23/11; e-discovery $5.8B

Top legal talent is scarce and mobile, with partner compensation often seven‑figure in 2024, keeping supplier leverage high. Research vendors and cloud providers concentrate pricing power (Westlaw/Lexis dominant; AWS 31%, Azure 23%, GCP 11% in 2024). Critical services (e‑discovery $5.8B, cybersecurity ~$207B, NYC/Wash rent ~$80/sq ft, recruiting fees 20–30%) raise switching costs and lock‑in.

| Supplier | Metric | 2024 |

|---|---|---|

| Legal talent | Partner pay | Seven‑figure |

| Cloud | Market share | AWS 31% / Azure 23% / GCP 11% |

| e‑discovery | Market size | $5.8B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Davis Polk & Wardwell, uncovering competitive intensity, client and supplier bargaining power, threat of entrants and substitutes, and regulatory dynamics shaping profitability and strategic positioning.

Ready-to-use Davis Polk & Wardwell Porter's Five Forces one-sheet—condenses competitive pressure into a clear visual so teams make faster, confident strategic decisions.

Customers Bargaining Power

Institutional clients with scale

Global corporates, financial institutions and governments purchase large recurring services from Davis Polk, running competitive RFPs, panel counsel reviews and strict billing guidelines. Their scale and brand prestige translate into leverage on rates, staffing and indemnities, with 2024 industry surveys citing average negotiated fee concessions of roughly 15–25%. Consolidation onto preferred panels amplifies this bargaining power across mandates.

High stakes, high switching costs

For bet-the-company matters clients face substantial switching costs driven by entrenched trust, proprietary knowledge, and strict confidentiality, so Davis Polk’s engagement economics allow premium pricing when outcomes are critical. Clients routinely accept higher fees for reduced execution risk; in complex M&A and capital markets work premium fees are common. Conflicts and regulatory constraints further narrow buyer options, moderating customer bargaining power despite scale.

Alternative fee pressure

Buyers increasingly demand AFAs, budget caps and transparency; by 2024 roughly 60% of corporate legal teams reported using alternative fee arrangements, shifting fee volatility to firms. Matter-based pricing and success fees transfer risk and compress realized rates, while sophisticated legal ops use KPIs and SLAs to enforce compliance. This tightens margins and raises buyer leverage, especially in repeatable, high-volume work.

Segmented price sensitivity

Segmented price sensitivity: commodity or process-heavy tasks at Davis Polk face intense price competition, while premium advisory and novel transactions sustain higher pricing and margins in 2024; buyers increasingly unbundle routine work to ALSPs or in-house, raising buyer power on lower-value layers.

- Commodity tasks: high price pressure

- Premium deals: strong pricing

- Unbundling to ALSPs/in-house: increases buyer leverage

Cyclicality and deal flow

In downturns buyers defer transactions and push fee renegotiations, while spikes in distressed and regulatory mandates — which rose notably in 2024 as restructuring activity increased — partially offset revenue pressure but do not fully neutralize bargaining power. In boom cycles urgency around deals reduces buyer leverage in core practices, shifting effective buyer power with the demand mix. The cyclicality thus creates material swings in negotiated terms over time.

- 2024: restructuring and regulatory work share rose relative to peak-deal practices

- Buyer leverage increases in market slowdowns

- Urgency in booms compresses buyer bargaining power

Buyers force 15–25% concessions; ~60% use AFAs, premium holds for high-stakes

Large corporates, financial institutions and governments exercise strong leverage on Davis Polk over rates, staffing and indemnities, driving typical negotiated fee concessions of 15–25% in 2024. High-stakes mandates retain premium pricing due to switching costs and confidentiality, while ~60% of corporate legal teams used AFAs in 2024, increasing buyer push for fixed fees and KPIs. Cyclical shifts (rise in 2024 restructuring/regulatory work) partially offset but do not eliminate buyer power.

| Metric | 2024 |

|---|---|

| Avg fee concessions | 15–25% |

| Corporate teams on AFAs | ~60% |

| Restructuring/regulatory share | ↑ vs peak-deal era |

Full Version Awaits

Davis Polk & Wardwell Porter's Five Forces Analysis

This preview shows the exact Davis Polk & Wardwell Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The analysis is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the complete, final file as shown, with instant access upon payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Davis Polk & Wardwell operates in a high-stakes legal market where partner loyalties, boutique rivals, client bargaining power, regulatory shifts, and substitute advisory services shape profitability. Our snapshot highlights key competitive pressures and strategic levers for growth. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore Davis Polk & Wardwell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Elite legal talent scarcity

Star partners and senior associates are the critical input for Davis Polk; top-tier lawyers command seven-figure compensation at the partner level and remain scarce and mobile in 2024, boosting supplier leverage.

Lateral markets and compensation wars keep bargaining power high as firms compete for rainmakers and origination-heavy talent.

Mitigation requires elevated spending on retention, training, and culture; in cyclical upswings or hot practices supplier power intensifies further.

Information and research oligopoly

Legal databases such as Westlaw and Lexis dominate the market, supplying the majority of primary-source and analytics access and granting them significant pricing power. Enterprise subscriptions and integration needs create high switching costs—large firms often incur six-figure annual spend on research platforms. Volume discounts mitigate per-user cost, but limited alternatives and new AI-license fees (added in 2023–24) have reinforced vendor leverage.

Technology and infrastructure vendors

Cloud, e‑discovery ($5.8B market in 2024), cybersecurity (global spend ~$207B in 2024) and collaboration platforms are mission‑critical for Davis Polk, concentrating supplier power: AWS (31%), Azure (23%) and GCP (11%) in 2024 narrow viable choices and boost vendor leverage. Long implementations and data residency rules create client lock‑in, while premium support and strict uptime SLAs command measurable cost premiums.

Expert, local counsel, and niche providers

Complex cross-border matters routinely require local counsel, expert witnesses, and specialist boutiques; in 2024 market reports detail rising demand and fee premiums in constrained jurisdictions. Limited court calendars and tight timelines reduce negotiation room, and deep firm relationships lower but do not eliminate supplier leverage.

- High reliance on niche providers

- Fee premiums in constrained jurisdictions

- Calendars limit bargaining

- Relationships mitigate but not remove leverage

Real estate and professional services

- Landlords: high rent pressure (~$80/sq ft)

- Vendors: court reporting $100–200/hr; recruiting 20–30% fees

- Hybrid: ~25–30% lower utilization

- Contracts: multi-year terms reduce negotiation leverage

Scarce top legal talent; partners earn seven-figure; cloud market 31/23/11; e-discovery $5.8B

Top legal talent is scarce and mobile, with partner compensation often seven‑figure in 2024, keeping supplier leverage high. Research vendors and cloud providers concentrate pricing power (Westlaw/Lexis dominant; AWS 31%, Azure 23%, GCP 11% in 2024). Critical services (e‑discovery $5.8B, cybersecurity ~$207B, NYC/Wash rent ~$80/sq ft, recruiting fees 20–30%) raise switching costs and lock‑in.

| Supplier | Metric | 2024 |

|---|---|---|

| Legal talent | Partner pay | Seven‑figure |

| Cloud | Market share | AWS 31% / Azure 23% / GCP 11% |

| e‑discovery | Market size | $5.8B |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Davis Polk & Wardwell, uncovering competitive intensity, client and supplier bargaining power, threat of entrants and substitutes, and regulatory dynamics shaping profitability and strategic positioning.

Ready-to-use Davis Polk & Wardwell Porter's Five Forces one-sheet—condenses competitive pressure into a clear visual so teams make faster, confident strategic decisions.

Customers Bargaining Power

Institutional clients with scale

Global corporates, financial institutions and governments purchase large recurring services from Davis Polk, running competitive RFPs, panel counsel reviews and strict billing guidelines. Their scale and brand prestige translate into leverage on rates, staffing and indemnities, with 2024 industry surveys citing average negotiated fee concessions of roughly 15–25%. Consolidation onto preferred panels amplifies this bargaining power across mandates.

High stakes, high switching costs

For bet-the-company matters clients face substantial switching costs driven by entrenched trust, proprietary knowledge, and strict confidentiality, so Davis Polk’s engagement economics allow premium pricing when outcomes are critical. Clients routinely accept higher fees for reduced execution risk; in complex M&A and capital markets work premium fees are common. Conflicts and regulatory constraints further narrow buyer options, moderating customer bargaining power despite scale.

Alternative fee pressure

Buyers increasingly demand AFAs, budget caps and transparency; by 2024 roughly 60% of corporate legal teams reported using alternative fee arrangements, shifting fee volatility to firms. Matter-based pricing and success fees transfer risk and compress realized rates, while sophisticated legal ops use KPIs and SLAs to enforce compliance. This tightens margins and raises buyer leverage, especially in repeatable, high-volume work.

Segmented price sensitivity

Segmented price sensitivity: commodity or process-heavy tasks at Davis Polk face intense price competition, while premium advisory and novel transactions sustain higher pricing and margins in 2024; buyers increasingly unbundle routine work to ALSPs or in-house, raising buyer power on lower-value layers.

- Commodity tasks: high price pressure

- Premium deals: strong pricing

- Unbundling to ALSPs/in-house: increases buyer leverage

Cyclicality and deal flow

In downturns buyers defer transactions and push fee renegotiations, while spikes in distressed and regulatory mandates — which rose notably in 2024 as restructuring activity increased — partially offset revenue pressure but do not fully neutralize bargaining power. In boom cycles urgency around deals reduces buyer leverage in core practices, shifting effective buyer power with the demand mix. The cyclicality thus creates material swings in negotiated terms over time.

- 2024: restructuring and regulatory work share rose relative to peak-deal practices

- Buyer leverage increases in market slowdowns

- Urgency in booms compresses buyer bargaining power

Buyers force 15–25% concessions; ~60% use AFAs, premium holds for high-stakes

Large corporates, financial institutions and governments exercise strong leverage on Davis Polk over rates, staffing and indemnities, driving typical negotiated fee concessions of 15–25% in 2024. High-stakes mandates retain premium pricing due to switching costs and confidentiality, while ~60% of corporate legal teams used AFAs in 2024, increasing buyer push for fixed fees and KPIs. Cyclical shifts (rise in 2024 restructuring/regulatory work) partially offset but do not eliminate buyer power.

| Metric | 2024 |

|---|---|

| Avg fee concessions | 15–25% |

| Corporate teams on AFAs | ~60% |

| Restructuring/regulatory share | ↑ vs peak-deal era |

Full Version Awaits

Davis Polk & Wardwell Porter's Five Forces Analysis

This preview shows the exact Davis Polk & Wardwell Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The analysis is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the complete, final file as shown, with instant access upon payment.