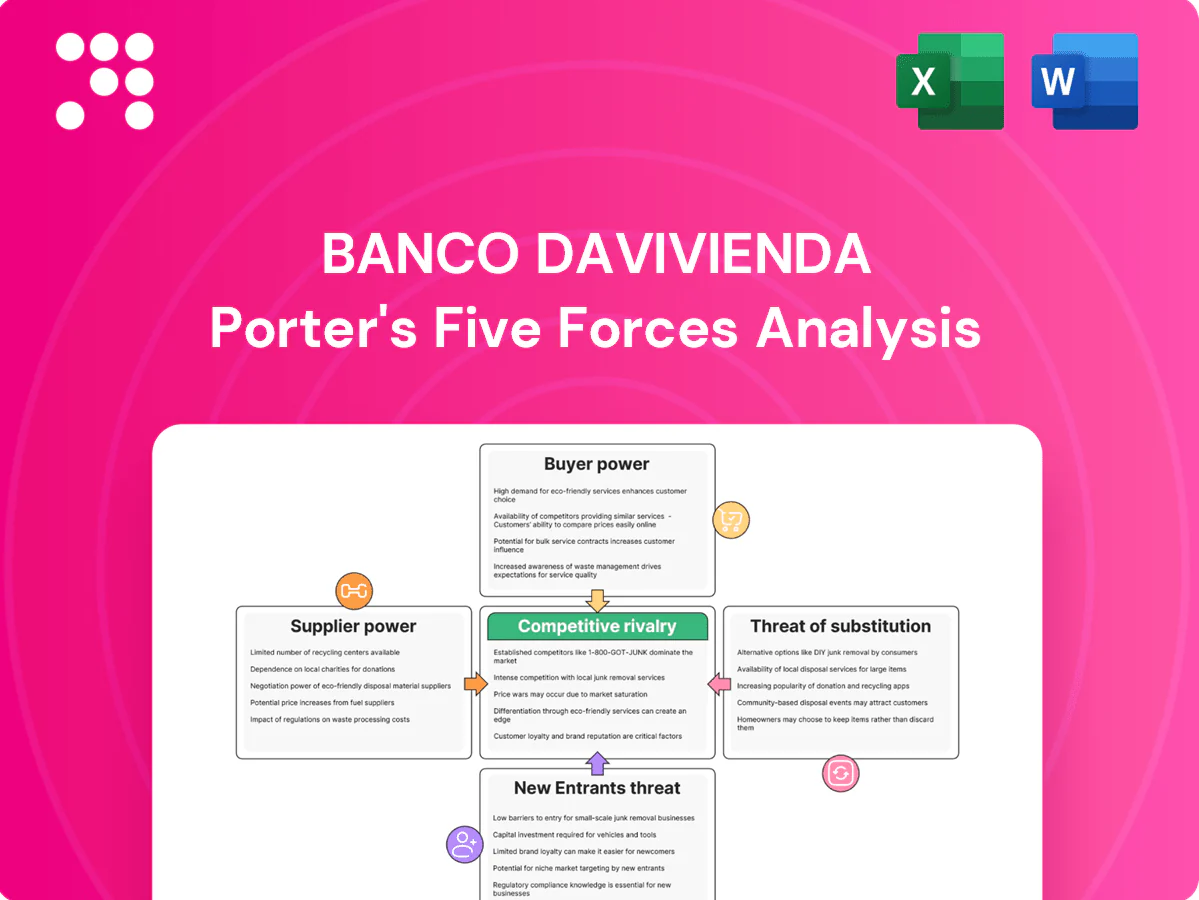

Banco Davivienda Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Banco Davivienda operates in a competitive, regulatory-heavy banking market where borrower bargaining, fintech substitutes, and capital requirements shape margins and growth. Our snapshot highlights key pressures—supplier concentration, entry barriers, and buyer sensitivity—that influence strategy and profitability. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for granular ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Wholesale and retail funding dependence

Davivienda relies heavily on retail deposits and wholesale market funding; fragmented, sticky retail deposits moderate supplier power by providing a stable base. In tight liquidity cycles wholesale lenders and large depositors gain leverage to demand higher rates. Such repricing increases funding costs and compresses net interest margins.

Technology and core banking vendors

Core systems, cloud infrastructure and payment rails for Banco Davivienda largely come from concentrated providers: leading core banking vendors such as Temenos, FIS, Finastra and Oracle dominate implementations, while AWS, Microsoft Azure and Google Cloud held about 67% of the cloud IaaS market in 2024 and Visa plus Mastercard processed over 75% of global card transactions in 2024. Switching core platforms is risky and costly, with long contracts and certification requirements deepening supplier leverage. Multi-vendor strategies and open API adoption can rebalance negotiating power by enabling incremental replacement and fintech integration.

Skilled talent and compliance expertise

Risk, data, cybersecurity and compliance talent remain scarce—ISC2 estimated a global cybersecurity workforce gap of about 3 million in 2023—driving supplier power for Banco Davivienda. Competition from fintechs and global tech firms raises wage pressure and talent poaching. Regulatory complexity in Colombia increases reliance on specialized staff and external advisors. Retention programs and internal academies reduce turnover and curb supplier leverage.

Payment networks and correspondents

Card schemes and correspondent banks provide essential connectivity for Davivienda, setting fee structures and rules that constrain pricing and product flexibility; major schemes control network access and dispute processes, limiting Davivienda’s negotiation leverage. Volume discounts and negotiated merchant rates lower costs as transaction scale grows, but true alternative global rails are limited. Domestic low-cost payment rails and instant payments are expanding and can gradually reduce dependency over time.

- Supplier concentration: card schemes and correspondents dominate network access

- Cost rigidity: fee rules limit pricing flexibility

- Scale benefit: volume discounts mitigate fees

- Substitution outlook: domestic instant rails reduce long-term dependency

Regulatory capital and licenses

Supervisors supply permissions and capital frameworks that shape Banco Davivienda’s growth; Basel III minimum CET1 of 4.5% plus a 2.5% conservation buffer (in force by 2024) raises the effective capital input requirement and cost of funding. Stricter buffers and macroprudential add-ons increase capital costs and limit leverage, while compliance timelines and model approvals delay product rollout; strong governance shortens approval times and reduces frictions.

- Regulatory inputs: CET1 min 4.5%

- Conservation buffer: 2.5% (Basel III, 2024)

- Impact: higher capital cost, slower product launches

- Mitigation: stronger governance = faster approvals

Moderate supplier power: retail deposits vs wholesale lenders; cloud ~67%, cards >75%

Supplier power is moderate: sticky retail deposits stabilize funding but wholesale lenders gain leverage in tight markets. Core systems/cloud are concentrated—AWS/Azure/GCP ~67% IaaS (2024)—and Visa+Mastercard >75% of card flows (2024), raising switching costs. Talent gap (~3M cybersecurity shortfall, 2023) and regulatory capital (CET1 4.5% + 2.5% buffer, 2024) further strengthen suppliers.

| Supplier | Metric | 2023/24 | Impact |

|---|---|---|---|

| Retail deposits | Stability | High | Lower power |

| Cloud/IaaS | Market share | ~67% | High switching cost |

| Card schemes | Transaction share | >75% | High fee power |

| Cybersecurity talent | Workforce gap | ~3M | Wage pressure |

| Regulators | CET1 + buffer | 4.5% + 2.5% | Capital cost |

What is included in the product

Tailored Porter's Five Forces analysis for Banco Davivienda, uncovering key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats—all supported by industry data and strategic commentary.

A concise, one-sheet Porter's Five Forces analysis for Banco Davivienda that clarifies competitive pressures and actionable mitigation strategies—ready to copy into decks, customize with your data, or integrate into broader reports for faster, clearer decision-making.

Customers Bargaining Power

Corporate clients negotiate hard

Large enterprises and public sector entities press Davivienda—the third-largest bank in Colombia by assets in 2024—for pricing and service concessions, leveraging volume to extract fee waivers and run multi-bank RFPs. Davivienda counters with tailored corporate solutions, FX execution and cash-management platforms. Deep account relationships and cross-sell of treasury products partially offset buyer power.

Retail base is fragmented

Millions of individuals and SMEs dilute customers bargaining power, with Davivienda serving over 8 million clients across its markets in 2024; bundled products and payroll-linked accounts raise switching costs, while loyalty programs and digital channels (mobile penetration above 70% in 2024) increase stickiness; nonetheless rate-sensitive savers pushed deposit pricing during the high-rate cycle in 2024, keeping funding costs elevated.

Price transparency via digital channels

Apps and comparison platforms make fees and interest spreads highly visible, and with Colombia's smartphone penetration around 70% in 2024 this information is broadly accessible.

Customers can rapidly benchmark loans and deposits across banks, shortening decision cycles and increasing switching behavior.

This transparency compresses margins on commoditized products, forcing pressure on net interest spreads.

Competitive differentiation therefore shifts toward UX, execution speed, and personalized advisory services.

Multi-product relationships lock in

Cross-selling mortgages, cards and insurance raises switching costs for Banco Davivienda: 2024 reported about 7.2 million active digital customers and an average of 1.8 products per client, deepening multi-product lock-in.

End-to-end digital journeys cut churn—multi-product clients show roughly 30% lower attrition in 2024—yet service failures can prompt simultaneous exits across products.

Proactive retention, real-time issue resolution and personalized offers remain critical to preserve lifetime value and prevent cascade losses.

- Cross-sell: 1.8 products/client (2024)

- Digital reach: ~7.2M active users (2024)

- Churn reduction: ~30% lower for multi-product clients

- Risk: service failures trigger multi-product exits

SMEs demand flexibility

SMEs demand faster credit decisions and flexible collateral, pushing Banco Davivienda to match fintechs that in 2024 increasingly offer near-instant underwriting and digital onboarding; tailored risk-based pricing helps defend spreads against price competition. Integrating payments and ERP links reduces perceived total cost and raises switching costs for clients.

- SME speed expectations: digital underwriting in 2024

- Flexible collateral requests: higher than retail

- Risk-based pricing: protects margins

- Non-credit integrations: lower total cost perception

High customer bargaining power and digital transparency compress spreads; cross-sell offsets

Customers exert moderate-to-high bargaining power: large corporates win fee concessions via volume while millions of retail/SME clients dilute individual power but force rate sensitivity during the 2024 high-rate cycle. Digital transparency (≈70% smartphone penetration) and comparison tools compress spreads; Davivienda offsets through cross-sell, digital UX and tailored SME offerings.

| Metric | 2024 |

|---|---|

| Clients | >8.0M |

| Active digital users | 7.2M |

| Products per client | 1.8 |

| Multi-product churn | -30% |

| Smartphone penetration | ~70% |

What You See Is What You Get

Banco Davivienda Porter's Five Forces Analysis

This preview shows the exact Banco Davivienda Porter's Five Forces analysis you'll receive upon purchase—no placeholders or sample pages. The document provides a fully formatted, professional assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. It's ready for immediate download and use after payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Banco Davivienda operates in a competitive, regulatory-heavy banking market where borrower bargaining, fintech substitutes, and capital requirements shape margins and growth. Our snapshot highlights key pressures—supplier concentration, entry barriers, and buyer sensitivity—that influence strategy and profitability. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for granular ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Wholesale and retail funding dependence

Davivienda relies heavily on retail deposits and wholesale market funding; fragmented, sticky retail deposits moderate supplier power by providing a stable base. In tight liquidity cycles wholesale lenders and large depositors gain leverage to demand higher rates. Such repricing increases funding costs and compresses net interest margins.

Technology and core banking vendors

Core systems, cloud infrastructure and payment rails for Banco Davivienda largely come from concentrated providers: leading core banking vendors such as Temenos, FIS, Finastra and Oracle dominate implementations, while AWS, Microsoft Azure and Google Cloud held about 67% of the cloud IaaS market in 2024 and Visa plus Mastercard processed over 75% of global card transactions in 2024. Switching core platforms is risky and costly, with long contracts and certification requirements deepening supplier leverage. Multi-vendor strategies and open API adoption can rebalance negotiating power by enabling incremental replacement and fintech integration.

Skilled talent and compliance expertise

Risk, data, cybersecurity and compliance talent remain scarce—ISC2 estimated a global cybersecurity workforce gap of about 3 million in 2023—driving supplier power for Banco Davivienda. Competition from fintechs and global tech firms raises wage pressure and talent poaching. Regulatory complexity in Colombia increases reliance on specialized staff and external advisors. Retention programs and internal academies reduce turnover and curb supplier leverage.

Payment networks and correspondents

Card schemes and correspondent banks provide essential connectivity for Davivienda, setting fee structures and rules that constrain pricing and product flexibility; major schemes control network access and dispute processes, limiting Davivienda’s negotiation leverage. Volume discounts and negotiated merchant rates lower costs as transaction scale grows, but true alternative global rails are limited. Domestic low-cost payment rails and instant payments are expanding and can gradually reduce dependency over time.

- Supplier concentration: card schemes and correspondents dominate network access

- Cost rigidity: fee rules limit pricing flexibility

- Scale benefit: volume discounts mitigate fees

- Substitution outlook: domestic instant rails reduce long-term dependency

Regulatory capital and licenses

Supervisors supply permissions and capital frameworks that shape Banco Davivienda’s growth; Basel III minimum CET1 of 4.5% plus a 2.5% conservation buffer (in force by 2024) raises the effective capital input requirement and cost of funding. Stricter buffers and macroprudential add-ons increase capital costs and limit leverage, while compliance timelines and model approvals delay product rollout; strong governance shortens approval times and reduces frictions.

- Regulatory inputs: CET1 min 4.5%

- Conservation buffer: 2.5% (Basel III, 2024)

- Impact: higher capital cost, slower product launches

- Mitigation: stronger governance = faster approvals

Moderate supplier power: retail deposits vs wholesale lenders; cloud ~67%, cards >75%

Supplier power is moderate: sticky retail deposits stabilize funding but wholesale lenders gain leverage in tight markets. Core systems/cloud are concentrated—AWS/Azure/GCP ~67% IaaS (2024)—and Visa+Mastercard >75% of card flows (2024), raising switching costs. Talent gap (~3M cybersecurity shortfall, 2023) and regulatory capital (CET1 4.5% + 2.5% buffer, 2024) further strengthen suppliers.

| Supplier | Metric | 2023/24 | Impact |

|---|---|---|---|

| Retail deposits | Stability | High | Lower power |

| Cloud/IaaS | Market share | ~67% | High switching cost |

| Card schemes | Transaction share | >75% | High fee power |

| Cybersecurity talent | Workforce gap | ~3M | Wage pressure |

| Regulators | CET1 + buffer | 4.5% + 2.5% | Capital cost |

What is included in the product

Tailored Porter's Five Forces analysis for Banco Davivienda, uncovering key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats—all supported by industry data and strategic commentary.

A concise, one-sheet Porter's Five Forces analysis for Banco Davivienda that clarifies competitive pressures and actionable mitigation strategies—ready to copy into decks, customize with your data, or integrate into broader reports for faster, clearer decision-making.

Customers Bargaining Power

Corporate clients negotiate hard

Large enterprises and public sector entities press Davivienda—the third-largest bank in Colombia by assets in 2024—for pricing and service concessions, leveraging volume to extract fee waivers and run multi-bank RFPs. Davivienda counters with tailored corporate solutions, FX execution and cash-management platforms. Deep account relationships and cross-sell of treasury products partially offset buyer power.

Retail base is fragmented

Millions of individuals and SMEs dilute customers bargaining power, with Davivienda serving over 8 million clients across its markets in 2024; bundled products and payroll-linked accounts raise switching costs, while loyalty programs and digital channels (mobile penetration above 70% in 2024) increase stickiness; nonetheless rate-sensitive savers pushed deposit pricing during the high-rate cycle in 2024, keeping funding costs elevated.

Price transparency via digital channels

Apps and comparison platforms make fees and interest spreads highly visible, and with Colombia's smartphone penetration around 70% in 2024 this information is broadly accessible.

Customers can rapidly benchmark loans and deposits across banks, shortening decision cycles and increasing switching behavior.

This transparency compresses margins on commoditized products, forcing pressure on net interest spreads.

Competitive differentiation therefore shifts toward UX, execution speed, and personalized advisory services.

Multi-product relationships lock in

Cross-selling mortgages, cards and insurance raises switching costs for Banco Davivienda: 2024 reported about 7.2 million active digital customers and an average of 1.8 products per client, deepening multi-product lock-in.

End-to-end digital journeys cut churn—multi-product clients show roughly 30% lower attrition in 2024—yet service failures can prompt simultaneous exits across products.

Proactive retention, real-time issue resolution and personalized offers remain critical to preserve lifetime value and prevent cascade losses.

- Cross-sell: 1.8 products/client (2024)

- Digital reach: ~7.2M active users (2024)

- Churn reduction: ~30% lower for multi-product clients

- Risk: service failures trigger multi-product exits

SMEs demand flexibility

SMEs demand faster credit decisions and flexible collateral, pushing Banco Davivienda to match fintechs that in 2024 increasingly offer near-instant underwriting and digital onboarding; tailored risk-based pricing helps defend spreads against price competition. Integrating payments and ERP links reduces perceived total cost and raises switching costs for clients.

- SME speed expectations: digital underwriting in 2024

- Flexible collateral requests: higher than retail

- Risk-based pricing: protects margins

- Non-credit integrations: lower total cost perception

High customer bargaining power and digital transparency compress spreads; cross-sell offsets

Customers exert moderate-to-high bargaining power: large corporates win fee concessions via volume while millions of retail/SME clients dilute individual power but force rate sensitivity during the 2024 high-rate cycle. Digital transparency (≈70% smartphone penetration) and comparison tools compress spreads; Davivienda offsets through cross-sell, digital UX and tailored SME offerings.

| Metric | 2024 |

|---|---|

| Clients | >8.0M |

| Active digital users | 7.2M |

| Products per client | 1.8 |

| Multi-product churn | -30% |

| Smartphone penetration | ~70% |

What You See Is What You Get

Banco Davivienda Porter's Five Forces Analysis

This preview shows the exact Banco Davivienda Porter's Five Forces analysis you'll receive upon purchase—no placeholders or sample pages. The document provides a fully formatted, professional assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. It's ready for immediate download and use after payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Banco Davivienda operates in a competitive, regulatory-heavy banking market where borrower bargaining, fintech substitutes, and capital requirements shape margins and growth. Our snapshot highlights key pressures—supplier concentration, entry barriers, and buyer sensitivity—that influence strategy and profitability. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for granular ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Wholesale and retail funding dependence

Davivienda relies heavily on retail deposits and wholesale market funding; fragmented, sticky retail deposits moderate supplier power by providing a stable base. In tight liquidity cycles wholesale lenders and large depositors gain leverage to demand higher rates. Such repricing increases funding costs and compresses net interest margins.

Technology and core banking vendors

Core systems, cloud infrastructure and payment rails for Banco Davivienda largely come from concentrated providers: leading core banking vendors such as Temenos, FIS, Finastra and Oracle dominate implementations, while AWS, Microsoft Azure and Google Cloud held about 67% of the cloud IaaS market in 2024 and Visa plus Mastercard processed over 75% of global card transactions in 2024. Switching core platforms is risky and costly, with long contracts and certification requirements deepening supplier leverage. Multi-vendor strategies and open API adoption can rebalance negotiating power by enabling incremental replacement and fintech integration.

Skilled talent and compliance expertise

Risk, data, cybersecurity and compliance talent remain scarce—ISC2 estimated a global cybersecurity workforce gap of about 3 million in 2023—driving supplier power for Banco Davivienda. Competition from fintechs and global tech firms raises wage pressure and talent poaching. Regulatory complexity in Colombia increases reliance on specialized staff and external advisors. Retention programs and internal academies reduce turnover and curb supplier leverage.

Payment networks and correspondents

Card schemes and correspondent banks provide essential connectivity for Davivienda, setting fee structures and rules that constrain pricing and product flexibility; major schemes control network access and dispute processes, limiting Davivienda’s negotiation leverage. Volume discounts and negotiated merchant rates lower costs as transaction scale grows, but true alternative global rails are limited. Domestic low-cost payment rails and instant payments are expanding and can gradually reduce dependency over time.

- Supplier concentration: card schemes and correspondents dominate network access

- Cost rigidity: fee rules limit pricing flexibility

- Scale benefit: volume discounts mitigate fees

- Substitution outlook: domestic instant rails reduce long-term dependency

Regulatory capital and licenses

Supervisors supply permissions and capital frameworks that shape Banco Davivienda’s growth; Basel III minimum CET1 of 4.5% plus a 2.5% conservation buffer (in force by 2024) raises the effective capital input requirement and cost of funding. Stricter buffers and macroprudential add-ons increase capital costs and limit leverage, while compliance timelines and model approvals delay product rollout; strong governance shortens approval times and reduces frictions.

- Regulatory inputs: CET1 min 4.5%

- Conservation buffer: 2.5% (Basel III, 2024)

- Impact: higher capital cost, slower product launches

- Mitigation: stronger governance = faster approvals

Moderate supplier power: retail deposits vs wholesale lenders; cloud ~67%, cards >75%

Supplier power is moderate: sticky retail deposits stabilize funding but wholesale lenders gain leverage in tight markets. Core systems/cloud are concentrated—AWS/Azure/GCP ~67% IaaS (2024)—and Visa+Mastercard >75% of card flows (2024), raising switching costs. Talent gap (~3M cybersecurity shortfall, 2023) and regulatory capital (CET1 4.5% + 2.5% buffer, 2024) further strengthen suppliers.

| Supplier | Metric | 2023/24 | Impact |

|---|---|---|---|

| Retail deposits | Stability | High | Lower power |

| Cloud/IaaS | Market share | ~67% | High switching cost |

| Card schemes | Transaction share | >75% | High fee power |

| Cybersecurity talent | Workforce gap | ~3M | Wage pressure |

| Regulators | CET1 + buffer | 4.5% + 2.5% | Capital cost |

What is included in the product

Tailored Porter's Five Forces analysis for Banco Davivienda, uncovering key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats—all supported by industry data and strategic commentary.

A concise, one-sheet Porter's Five Forces analysis for Banco Davivienda that clarifies competitive pressures and actionable mitigation strategies—ready to copy into decks, customize with your data, or integrate into broader reports for faster, clearer decision-making.

Customers Bargaining Power

Corporate clients negotiate hard

Large enterprises and public sector entities press Davivienda—the third-largest bank in Colombia by assets in 2024—for pricing and service concessions, leveraging volume to extract fee waivers and run multi-bank RFPs. Davivienda counters with tailored corporate solutions, FX execution and cash-management platforms. Deep account relationships and cross-sell of treasury products partially offset buyer power.

Retail base is fragmented

Millions of individuals and SMEs dilute customers bargaining power, with Davivienda serving over 8 million clients across its markets in 2024; bundled products and payroll-linked accounts raise switching costs, while loyalty programs and digital channels (mobile penetration above 70% in 2024) increase stickiness; nonetheless rate-sensitive savers pushed deposit pricing during the high-rate cycle in 2024, keeping funding costs elevated.

Price transparency via digital channels

Apps and comparison platforms make fees and interest spreads highly visible, and with Colombia's smartphone penetration around 70% in 2024 this information is broadly accessible.

Customers can rapidly benchmark loans and deposits across banks, shortening decision cycles and increasing switching behavior.

This transparency compresses margins on commoditized products, forcing pressure on net interest spreads.

Competitive differentiation therefore shifts toward UX, execution speed, and personalized advisory services.

Multi-product relationships lock in

Cross-selling mortgages, cards and insurance raises switching costs for Banco Davivienda: 2024 reported about 7.2 million active digital customers and an average of 1.8 products per client, deepening multi-product lock-in.

End-to-end digital journeys cut churn—multi-product clients show roughly 30% lower attrition in 2024—yet service failures can prompt simultaneous exits across products.

Proactive retention, real-time issue resolution and personalized offers remain critical to preserve lifetime value and prevent cascade losses.

- Cross-sell: 1.8 products/client (2024)

- Digital reach: ~7.2M active users (2024)

- Churn reduction: ~30% lower for multi-product clients

- Risk: service failures trigger multi-product exits

SMEs demand flexibility

SMEs demand faster credit decisions and flexible collateral, pushing Banco Davivienda to match fintechs that in 2024 increasingly offer near-instant underwriting and digital onboarding; tailored risk-based pricing helps defend spreads against price competition. Integrating payments and ERP links reduces perceived total cost and raises switching costs for clients.

- SME speed expectations: digital underwriting in 2024

- Flexible collateral requests: higher than retail

- Risk-based pricing: protects margins

- Non-credit integrations: lower total cost perception

High customer bargaining power and digital transparency compress spreads; cross-sell offsets

Customers exert moderate-to-high bargaining power: large corporates win fee concessions via volume while millions of retail/SME clients dilute individual power but force rate sensitivity during the 2024 high-rate cycle. Digital transparency (≈70% smartphone penetration) and comparison tools compress spreads; Davivienda offsets through cross-sell, digital UX and tailored SME offerings.

| Metric | 2024 |

|---|---|

| Clients | >8.0M |

| Active digital users | 7.2M |

| Products per client | 1.8 |

| Multi-product churn | -30% |

| Smartphone penetration | ~70% |

What You See Is What You Get

Banco Davivienda Porter's Five Forces Analysis

This preview shows the exact Banco Davivienda Porter's Five Forces analysis you'll receive upon purchase—no placeholders or sample pages. The document provides a fully formatted, professional assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. It's ready for immediate download and use after payment.